5-min tactical stock pitches for investors & position traders across global equities.

Sharing portfolio weekly, performance monthly.

Former analyst at $6B fund.

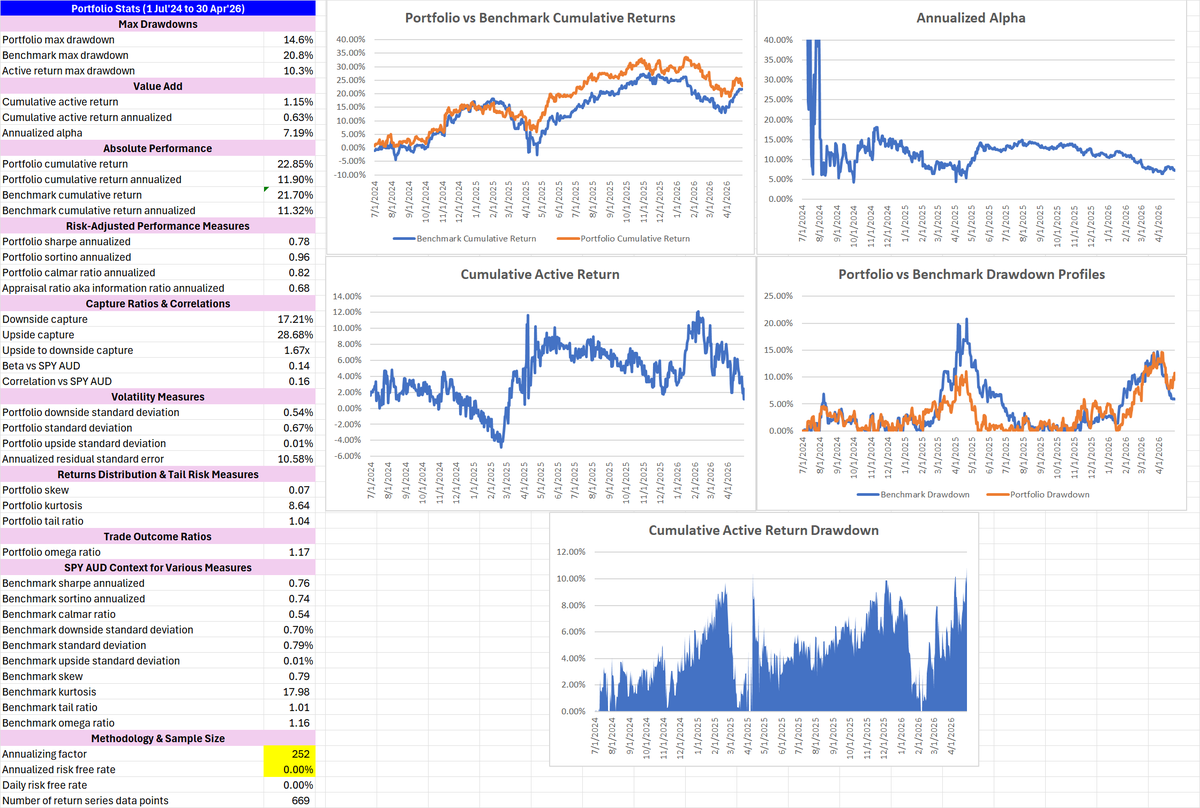

Apr'26 Portfolio Update

I track metrics that help separate skill from luck in portfolio performance

View full update and also get this portfolio analytics template for free by signing up to my newsletter:

https://t.co/FrviAPsV8a

@orrdavid There are good reasons to be extra skeptical of sell-side research when it is around any capital markets activity (IPO, M&A, equity or debt raise, etc).

@spacanpanman Is this just based on momentum?

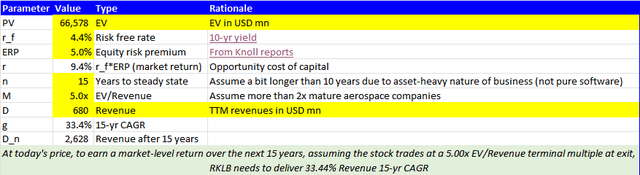

The valuations say $RKLB must grow like a massive outlier: 33% 15-yr rev CAGR needed to match market returns

@ns123abc This is a pretty neat way to bet on the broad industry trend but avoid picking winners

SpaceX and xAI will dominate the space services ecosystem

1/ $GOOGL is spending $185B on AI capex this year, with FY27 guided even higher. FCF margins have compressed sharply and buybacks have gone to zero.

But I'm still bullish

5/ At a 1-yr fwd PE of 28.7x, $GOOGL looks expensive vs peers on surface metrics.

But the market is only pricing in a ~15% 7-yr earnings CAGR, while actual PAT growth is running at 29-44%.

So the stock's prolly undervalued now.

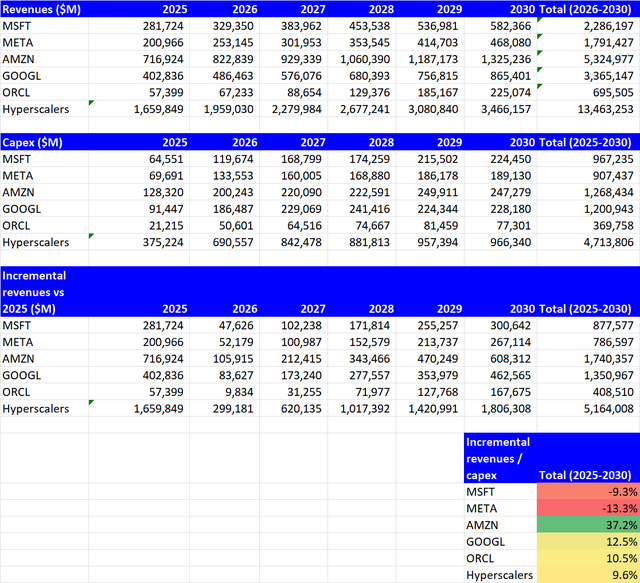

@Midnight_Captl The biggest risk is more cautious capex spending by hyperscalers. I estimate ~9.6% ROI before costs looking out 5 years.

Did the CFO say anything about what they're seeing on that front?

You may have seen a Financial Times article about negative capex ROIs for hyperscalers

I ran my own calculation and don't get quite as bleak a result:

Hyperscalers' capex ROI of 9.6%, which is close to US equity market return expectations

But this is before costs so actual ROI numbers may be worse

$AMZN is an exception, probably because of a higher % of custom chips use.

$GOOGL does this too but its numbers are likely understated as they don't monetize custom chips as much as $AMZN. But it will be reflecting in profit-based ROI metrics via lower cost.

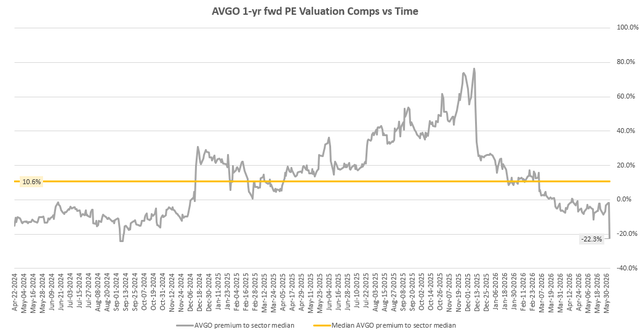

5/ On valuation, $AVGO trades at a 1-yr fwd PE of ~26.8x post-selloff. The semiconductor peer median sits at 34.5x. This implies a relative ~22% discount, near trough levels. $AVGO has historically commanded a 10.6% premium to peers.