Growth in the digital economy is supported by many themes - AI, Cloud , Automation, Energy Transition & Edge Computing.

Underpinning it all...semi-equipment companies. They have high barriers to entry & have dominated their niches for a long time.

$ASML $AMAT $KLAC $TEL $LRCX

Game theory is perfectly optimal here

AMZN/GOOG chasing scale with in-house chip programs with fat ROIs. Chosen providers. Scarcity on the horizon. Jamming it

MSFT/META - severe threat of their productivity suite and feed products. MSFT also 3rd cloud now staring down being sub scale. Gotta go. META continues to chase a platform they own

ORCL/Neos - chose to play this game and its a scale one. You need to 1) be in NVDAs good graces 2) chase the big boys. Nasty hole to be in. ORCL legit needs to bow out

Then at the national security level. This + intelligence data collection prob the most powerful weapon since the nuke. China will not let this go, no matter the constraints. 300b into domestic prob just the beginning. They WILL find a way

Foundry level. TSM tried to exercise prudence against capacity and ASML and let Samsung/Intel come back from the dead. Memory shortages are being chased with capacity because also need logic dies going forward + Samsung has never been the #2 to Hynix and wants their share back. They are all going to go in front of equipment tightness potentially materializing

Corporate spending is either experimental or defensive. Startups attacking incumbent software from below. Major enterprises with fat budgets attacking operational efficiency / differentiation from above. Maybe wasteful, but tail chance if you don't play you die

The capability is enough that people don't have an option across the board. Everyone has someone elses gun to their head

The Earnings Trap

One of the most misunderstood metrics in investing is the P/E ratio. That does not mean it is bad or useless. It simply means that many investors stop their analysis at the number itself without asking where those earnings actually came from. Two companies can report identical earnings and deserve dramatically different valuations because the source of those earnings is completely different.

Take $TOST as an example. Last year it generated $305 million of operating income, which represents the profit produced by the actual business. Yet pretax income was $346 million. So where did the extra $41 million of earnings come from?

Most of it came from intrest income. $TOST has a large cash balance and virtually no debt, allowing it to earn roughly $51 million simply by holding cash on its balance sheet. After accounting for a few smaller one time items, pretax income ended up $41 million higher than operating income.

There is absolutely nothing wrong with this, and in fact it is a positive. The company is generating additional profit from an asset it already owns. The important point, however, is that these earnings are fundamentally different from operating earnings because they are not being produced by the core business itself.

If $TOST spent a significant portion of its cash on an acquisition, interest income would decline. If management launched a large share repurchase program, interest income would decline. If interest rates moved materially lower, interest income would decline as well, even if the underlying business continued performing exactly as before.

This creates a fascinating problem for investors because accounting treats all earnings equally while economics often does not. Imagine two companies that each earn $100 million. The first company generates every dollar by serving customers and selling products. The second company generates $70 million from operations and $30 million from interest earned on excess cash.

The income statement treats those earnings as identical, but should investors? Most people spend countless hours debating whether a stock trades at 20x earnings or 25x earnings. Far fewer stop to ask whether those earnings deserve the same multiple in the first place.

The quality of earnings is often far more important than the quantity of earnings. This is why great investors spend so much time studying the source of earnings rather than simply accepting the headline number. Some earnings are generated by durable competitive advantages. Some come from excess cash. Some come from investment gains. Others come from accounting adjustments, tax benefits, or one-time events. The income statement combines them together, but the investor should still understand where every dollar originated.

The broader lesson has very little to do with $TOST. $TOST is simply the example for a business I have been studying recently. The real lesson is that not all earnings are created equal, and understanding that fact can completely change how you think about valuation. A dollar earned from a durable competitive advantage is often worth far more than a dollar earned from temporary circumstances.

Most investors treat earnings as a destination. The best investors treat earnings as the beginning of an investigation. They understand that the number itself is rarely the story because the story is where the number came from. The greatest investors do not simply ask how much a company earned. They ask how it earned it, and that question often makes all the difference.

🌹

$TSM CEO Pushes Back on @GavinSBaker, Clarifying That TSMC's Bottlenecks Are Organic, Not Self-Imposed

"When asked by a reporter, Gavin Baker, a technology investor who previously managed over $17 billion in assets at Fidelity and is now the chief investment officer at Atreides Management, described TSMC as being managed by a group of very stubborn and experienced people in their 70s who had personally witnessed Taiwan's semiconductor industry go from lagging behind Intel to gradually establishing itself as a global leader. Therefore, they were very clear about the cost of tech bubbles and crashes.

In response to the above statement, TSMC's CEO stated that Baker originally meant that TSMC was applying the brakes because AI would not become a bubble. A group of experienced seniors were applying the brakes. But to be honest, TSMC did not deliberately control it, nor did TSMC intend to apply the brakes. They may be a bit stubborn and old, but they really did not deliberately apply the brakes.

TSMC's CEO said that his company tried its best to increase production capacity for its customers, but who knew that the customers' businesses would grow so fast? The development since the launch of GPT in 2023 has far exceeded expectations. C.C. Wei also revealed that he asked NVIDIA CEO Jensen Huang why he was so smart and hadn't told him earlier, but Huang replied that he didn't know either. No one, including TSMC, can predict this now, and all these demands are going to TSMC, which can't see it coming either.

C.C. Wei also stated frankly that TSMC has been increasing production, with more than a dozen construction sites underway in Taiwan."

It's actually interesting that Wei chose to discuss this narrative, and he specifically quoted Gavin's comments.

$NVDA

Capex/FCF -> Debt/Leverage

Most ROI analysis on AI has focused on Big Tech capex and FCF.

But as more companies approach zero or negative FCF, I think the focus needs to shift toward net debt and leverage.

Given the ROI we are seeing from AI investments, I suspect companies will not pause spending simply because FCF hits zero - which is already happening for some names. The real constraint is more likely to come when companies (first) move into net debt, and (then) when leverage reaches a level that is no longer sustainable.

The complication is that many Big Tech companies now have meaningful off-balance-sheet obligations - finance leases, operating leases, JVs, purchase commitments, and cloud/infrastructure commitments. These may not show up as debt today, but they will likely become a drag on FCF over time.

-------------------

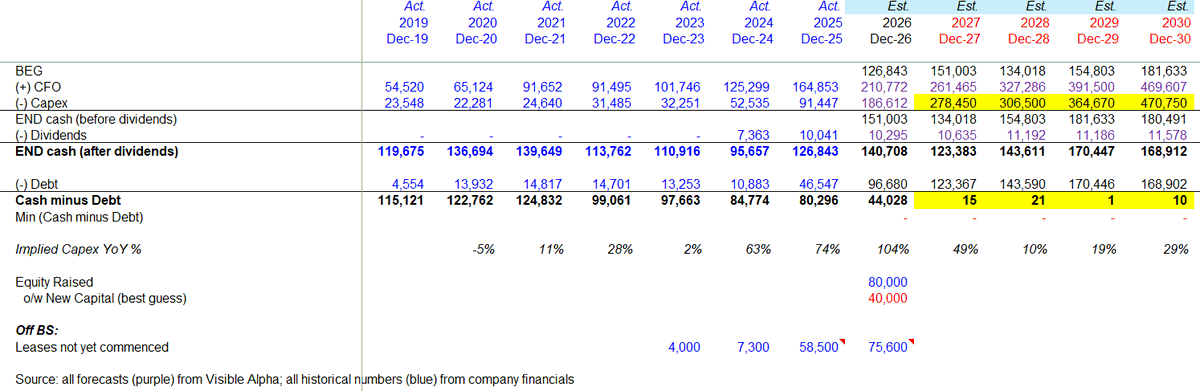

$GOOGL

$GOOGL is relatively clean from an off-balance-sheet perspective, other than approximately $76B of leases not yet commenced.

Management has also said $Googl does not intend to move into a net debt position. Using consensus estimates from Visible Alpha and assuming $Google is willing to run down to roughly zero net cash, the implied maximum capex for FY27 would be approximately $280B, or roughly 50% YoY growth.

$GOOGL also has some buffers:

- ~$40B from the $80B equity raise (a $15B convert, $15B common equity, $10B private placement, and $40B ATM offering) (source: https://t.co/wAEEfPLeoo)

- ~$10B per year of dividends that could theoretically be adjusted.

-------------------

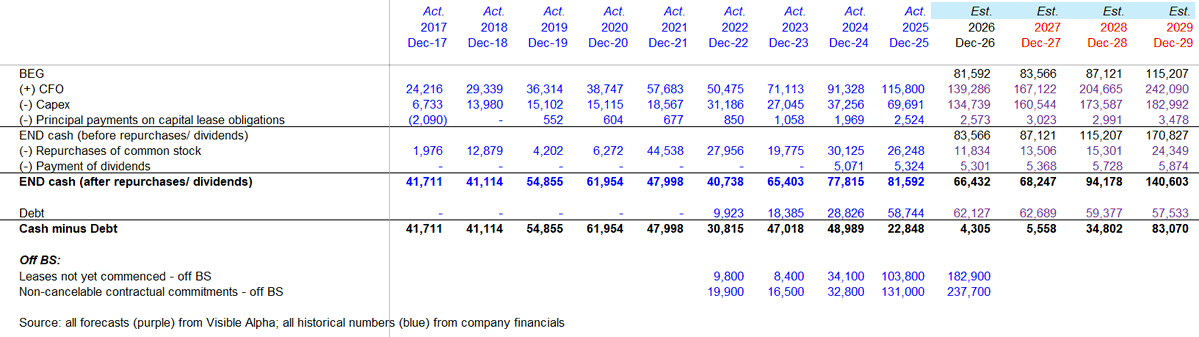

$META

$META has much larger off-balance-sheet commitments.

The two biggest buckets are:

1. Leases not yet commenced - $183B off balance sheet as of 1Q26

2. Non-cancelable contractual commitments - $238B as of 1Q26

Importantly, $42.25B is due in 2026 and $47.65B is due in 2027.

$Meta also disclosed several additional items that are worth tracking separately:

- A contingent obligation to purchase up to $14.72B of cloud capacity over five years

- April 2026 infrastructure contracts that increased non-cancelable commitments by another ~$24B

- Unconsolidated VIE exposure of $46.0B maximum exposure to loss tied to venture economics

It is impossible to know the exact future FCF, cash, and debt impact from these off-balance-sheet items. But directionally, $Meta looks much more likely to move into a net debt position once we account for these obligations - especially given the $42.25B due in 2026 and $47.65B due in 2027.

-------------------

Bottom line

The AI capex debate should not stop at reported capex and FCF. For companies with large off-balance-sheet commitments, the better question is: what does the balance sheet look like once these obligations start flowing through cash? On that basis:

$GOOGL still looks relatively clean and has the most balance-sheet flexibility.

$META has the most meaningful off-balance-sheet risk and is likely to move into a net debt position.

$AMZN has large commitments and seems certain to move into net debt.

Net-net, I actually (weirdly) feel better after going through this exercise.

1/ These companies still have some cash buffers. Even after adjusting for off-balance-sheet commitments, most are not getting to an unsustainable leverage position in the near term.

2/ This analysis is based on consensus cash flow from operations. Actual CFO could come in higher if AI ROI starts showing up more meaningfully.

3/ Companies still have some flexibility - not a ton, but some - if they decide to slow or pause share repurchases and dividends.

So the conclusion is not that Big Tech is immediately constrained. The better question is: how far can they push AI infrastructure spending before the balance sheet, not the income statement, becomes the constraint?

+++

Full analysis: https://t.co/2ZzO8YJ9xy

my big revelation this past week is that the clearest opportunities in the market to me are in semicap - $ONTO $MKSI $AMAT $ASML $LRCX $KLAC. things will stay tight for the foreseeable future which is / will be reflected in a lot of folks but not here yet. Terrafab is also pretty real

$SPGI Bernstein event

a key concern: if LLMs get better, clients may bypass SPGI & just buy raw data to clean & process themselves—potentially weakening data-layer defensibility & pressuring pricing

mgmt: clients r willing to pay 35-45% premium at renewal for AI-ready data

Morgan Stanley just published the most important data package of the AI cycle (Save this).

Four companies, Google, Amazon, Microsoft, Meta are on track to spend $1 trillion in a single year in 2027.

To understand how we got here, look at the progression.

$250 billion in 2024, $413 billion in 2025, $737 billion in 2026 and $1.018 trillion in 2027.

Combined, these four companies will have spent over $2 trillion on AI infrastructure between 2024 and 2027.

Now look at the capacity chart because the dollars alone miss the most important story.

In 2025, hyperscalers added roughly 6.7 GW of incremental compute capacity globally, in 2027, they will add 19.5 GW.

That is 3x more physical AI infrastructure coming online in a single year than came online just two years prior.

Google leads the entire buildout adding an estimated 6.8 GW in 2027 alone.

Morgan Stanley's note puts that number in staggering context, AWS's total installed base at the end of 2024 was roughly 4 to 6 GW and that capacity supported a $108 billion annual revenue business.

Google is adding more new capacity in a single year than Amazon built in its entire history and the cost per GW data is where the investment thesis sharpens into something actionable.

The cost to build one gigawatt of AI compute capacity is falling from $62 billion per GW in 2024 to $52 billion per GW in 2027 even as the compute density per GW is rising dramatically.

Google builds at $44 billion per GW, Microsoft builds at $59 billion per GW.

That $15 billion gap per gigawatt is almost entirely explained by one decision, Google uses custom ASICs, Microsoft uses NVIDIA GPUs.

NVIDIA's current GB300 racks cost roughly $19 billion per GW of compute capacity. Vera Rubin, the next generation pushes that to around $25 billion per GW as rack power density climbs to 600 kilowatts.

Custom ASIC racks built by Broadcom for Google, Marvell for Amazon cost between $6 and $11 billion per GW.

At the scales being discussed here, the companies that shift to custom silicon do not just save money on chips, they structurally outcompete every hyperscaler still running on merchant silicon because they get exponentially more compute for the same dollar.

Here is what that means as an investor.

The orders are placed, power contracts are signed, land is acquired and the hyperscalers have already committed the capital, the only question is whether the supply chain can keep up.

That supply chain bottleneck is the exact thesis we have been building.

Broadcom designs the ASICs, Marvell designs the custom silicon and the optical DSPs, AAOI makes the InP lasers that move the data and every single one of those companies is directly in the path of $1 trillion per year in committed spending by the most cash-rich companies on Earth.

Milk Road is already positioned, come join Pro (link below) and get the full breakdown of how we are mapping the $2 trillion capex cycle onto the specific supply chain names and why we think the compounding from here is still in the early innings.

The global semiconductor market will surge 90% to US$1.51 trillion in 2026 led by AI-related computing and the “extraordinary memory expansion”, WSTS said, up sharply from the $1.0T forecast in March. $NVDA $MU $TSM #Samsung#semiconductors

Pulak Prasad (founder Nalanda Capital - AUM $5 Billion)

In September 2023, he wrote this remarkable 4 pager on ‘What Darwin can teach you about Investing’

It has potential to change your perspective on Investing for a lifetime, just as it changed mine.

Incredible 👏🏻

Wonder what Jensen has been cooking so much in Asia lately:

It is also about who controls the supply chain before everyone else realizes it is scarce.

TSMC 3nm may be the next major AI bottleneck.

TrendForce says AI chips will largely transition from 4nm to 3nm between 2H 2025 and 2026.

At the same time, high-end smartphone and PC chips have not broadly moved to 2nm yet.

So a lot of high-compute demand will crowd into 3nm in a very short window.

Samsung and Intel are still behind TSMC in 3nm foundry capability, which means TSMC effectively controls the scarce supply.

TrendForce expects global 3nm capacity to surpass 5/4nm by the end of 2026.

By 2027, 3nm could become the second-largest key process node after 28nm.

But the bottleneck is not only wafers.

CoWoS, substrates, PCBs, HBM, SSDs, T-glass, packaging equipment and raw materials are all becoming strategic resources.

NVIDIA saw this early and reserved large amounts of wafer, packaging and component capacity ahead of others.

That may be one of the most under-appreciated parts of NVIDIA’s moat.

I'm suspicious of that that whole story about Uber blowing their AI budget and being disappointed in the results - I dug into it and it appears to have been built on very shaky foundations

Some insights on $NOW from the Jefferies Conference today. ServiceNow is changing Now Assist from just AI summarization into an agentic system that can run full tasks end to end. They built the AI Control Tower to handle security and compliance for AI agents. They launched 20 different AI specialists that act like human workers in support and HR roles.

They changed their pricing to three levels named Foundation, Advanced, and Autonomous. They are putting AI features into every level of their products instead of only selling it as a premium add-on.

They use their existing CMDB platform to find, track, and manage AI agents across the enterprise. The AI Control Tower connects with agents made by other companies including $CRM and $WDAY.

They created Action Fabric so outside AI agents can call into ServiceNow to complete tasks. They bought Moveworks to create a single conversational interface for voice and multimodal use. Their post-breach cybersecurity business is now worth more than $1B and is growing quickly. They bought Armis to track and secure physical devices, medical equipment, and factory floor AI within their database. They bought Veza to manage non-human identities and secure what AI agents are allowed to access. They bought Logik ai to improve their software for configuration, pricing, and quoting workflows.

They rebuilt RaptorDB to handle both transactional and analytical data. The premium version called RaptorDB Pro works 17x faster than the standard version. RaptorDB Pro made $100M in new contract value during its first four quarters on the market.

Their Workflow Data Fabric software connects to 300 different data systems. Workflow Data Fabric lets customers analyze data from $SNOW, Databricks, and BigQuery without moving the files. Management expects the data analytics and Workflow Data Fabric business to grow to over $1B and their CRM customer service business is already worth a couple of billion dollars and is growing very fast.

ServiceNow has a base revenue target of $30B for the year 2030. The four main growth areas to hit this goal are AI tools, security, data analytics, and customer service software.

The most popular AI subscription will run you about $20/month and it gives you access to most of the models and is good enough for the average daily user. But for a company like Anthropic how much does it cost the company to be servicing the user? It's safe to assume that the majority of users aren't going to be hitting the usage limits but hypothetically let us say they did. Depending on the workload, the same $20 subscription can range from insanely profitable to barely breaking even.

Interview with a Former $AMZN AWS employee and AI enterprise integrator explaining how dominant hyperscalers $AMZN, $GOOGL and $MSFT are in AI production workloads:

1. According to him, because of compliance, security, and a long-term view, all enterprises start with the primary cloud as a pattern of AI adoption. Even the clients that start with open-source end up moving into the hyperscaler world. He is observing the trend that enterprises build AI on top of the hyperscaler layer.

2. According to him, any production-level thinking for customers or its roadmap for the next five years typically is knitted to the hyperscalers, unless it's a startup.

3. For what he has had experience when it comes to AI model consumption, customers in the majority go via hyperscaler native AI platforms like Bedrock, Azure AI Foundry, or Vertex. The hyperscaler layer is the control plane where the security, logging, and scaling everything is put, while the model provider becomes a very interchangeable layer: »Companies rarely bypass the hyperscaler once the scaling begins«.

4. In his view, because of the data gravity handling, compliance going via a hyperscaler AI model offering is better than going directly to the AI model provider.

found on @AlphaSenseInc