@StockJabber The Evergrande lawsuit in Hong Kong showed serious knowledge gaps on the judge's part as well, e.g. blindly trusting sell-side analysts and ignoring what their business model is.

These retail investors would probably sue their doctor if they were told one day that they had cancer. ‘Your Honor, I was perfectly healthy until I walked into that clinic!’

https://t.co/zJdbpsgYLN

End 2024, we covered our $EOSE short because we suspected that Cerberus, with their controversial reputation, would manufacture demand. That's exactly what they are doing now with an affiliate. The eternal problem with EOSE remains the same: the zinc technology sucks.

$EOSE Q1 reality check. Gross margin -78% (-96% ex IRA subsidy). 45% of revenue went unbilled into contract assets, up from 1% a year ago. Meanwhile investors are briefly excited about a new JV with Cerberus that burns and dilutes shareholders.

Cerberus already had warrants, preferred, board seats, and senior debt. The new JV adds $50 million of founder units for zero cash, 10% IRR pref on capital they didn’t deploy, controlling equity, the operating contract, and another discount warrant.

Shareholders chip in $150 million through a rights offering.

Cerberus is named for the three-headed dog that guards hell. Shareholders are fully trapped there.

Here is the only key bit in last night's $SMR earnings call:

Management script: Here are all the reasons our reactor is superior to competitors

First question in Q&A: Given that "compelling pitch," why isn't anyone actually buying one from you?

Answer: 100% evasion (below)

1/2

Great energy at the 2026 ANS Student Conference. We had engaging conversations with students, faculty, and industry professionals about NuScale’s SMR technology, deployment progress, and internships. The next generation is ready to shape clean, reliable energy. #ANS2026

$GEVO stock falling after the company withdraws its DOE financing application for the ATJ-30 project that didn’t make any sense. https://t.co/bXXknswIFI

We are short Gevo Inc ($GEVO). The change in the US administration is the obvious threat but problems run deeper, in particular the competitiveness of technology. A lot of room to fall further.

@JigarShahDC@mjbommar EOSE has had the opportunity to clear up the controversy over its battery performance (particularly its inferior RTE) once and for all through independent certification, but it has never done so. Meanwhile, all the 8-hour contracts are going to lithium.

@JigarShahDC@mjbommar Could you disclose whether you or a related party have a financial interest in EOSE, or are you concerned it will be your Solyndra?

32-year old internet influencer who probably did ten minutes of research discovers that $EOSE management is not quite reliable. Something that has been known and documented for years.

No position now, we are waiting Cerberus' exit.

Dear Joe,

I’m writing this as a shareholder who actually wanted to believe in $EOSE is building and who still believes the underlying problem you’re trying to solve is real, urgent & structurally important for the grid. But this quarter wasn’t just a bad print.. it genuinely was a complete trust break.

Small-cap investing is like watching your house catch fire since you already know the risk going in but the only way you survive is if you trust the person guiding you to the front door. Once that trust is gone then you don’t just lose money but you burn with it. That’s what this quarter felt like.

Reaffirming guidance deep into the quarter and then missing it by this much without pre-announcing tells me that you actually didn't know what was happening inside the factory or chose to stick with the story even as the numbers were falling apart. Both are bad. As CEO, that’s on you.

What makes this harder to swallow is the timing since you raised roughly $600M late in the quarter and then turned around and delivered results that were nowhere close to what had been guided. Even if every operational issue you laid out is real then the sequence alone creates a governance problem. You can’t take fresh capital from the market while the quarter is blowing up and then act surprised after the fact. That destroys credibility.

I heard the explanations of supplier issues, downtime way above expectations, automation not hitting quality targets, rework, utilization below plan. These are real problems but from the outside it looks like the manufacturing system still isn’t stable enough to support the confidence you projected publicly. You can’t ask investors to underwrite a scaling story when the engine is still sputtering.

The frustrating part is that demand doesn’t look like the problem. You booked a lot of new orders, backlog grew and the pipeline is big and the tech actually matters. Long-duration, non-flammable zinc batteries solve a real gap that lithium-ion doesn’t since data centers run 24/7 but the grid wasn’t built for that. Eos sits right at the intersection of AI power demand and grid reliability which is why people believed in this story in the first place.

But none of that matters if management credibility is impaired which is exactly what today’s stock action reflects. A 40% drawdown isn’t the market debating long-duration storage but it’s the market GRADING YOU JOE and saying it no longer trusts you on execution.

I hope the company does turn it around. I hope the technology scales. I hope the mission succeeds. But as an investor, I already accept enough uncertainty from markets, supply chains and the normal fog of war but what I cannot accept is uncertainty layered with distrust of management communication. This quarter crossed that line and you should assume many shareholders feel the same.

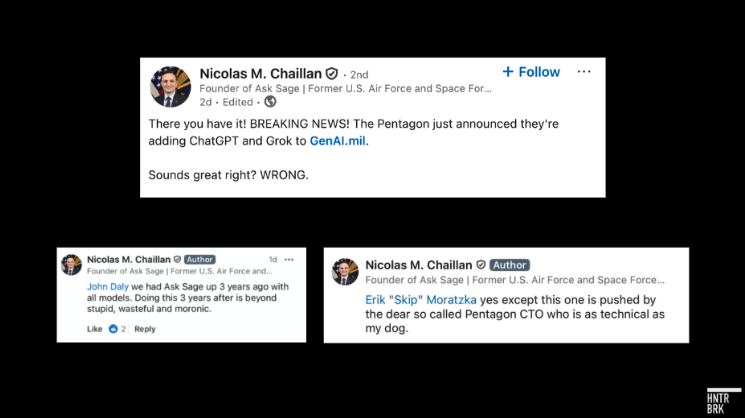

https://t.co/rP2Z68fRS9 ( $BBAI ) spent $250M acquiring a military AI chatbot called Ask Sage. 29 days later, the Pentagon launched a free alternative and ordered 3 million personnel to use it. The Ask Sage founder—recently named BigBear's CTO—is melting down on LinkedIn.

After months of hearing from Sam Altman and others that the world is about to run out of electricity, some sanity backed by real numbers, not outlandish projections. $SMR

NEW ODD LOTS:

The Utilities Analyst Who Says Datacenter Math Doesn't Add Up

@tracyalloway and I talk to CreditSights' co-head of IG credit Andy DeVries who says datacenter power demand will fall short and that utilities are OVERBUILDING for the future https://t.co/dkIcn4XKJU

@TheStalwart@tracyalloway Too much credit has been given to Sam Altman's outlandish projections. Add that utilities are financially incentivized to inflate future capex. From our previous report:

@nordicsky@CedarStResearch Write a report on why and send it to us. Go invest in a companies where ultra-promotional management screwed retail in the past. Good luck. We know how it will end.