Quote of the Day:

"The big money is made by 'the sitting and the waitin'' — not the thinking. Wait until all the factors are in your favor before making a trade. Once a position is taken the next difficult task is to be patient and wait for the move to play out. The temptation is strong to take fast profits or cover your trade solely out of fear of losing the profit on a correction. This error has cost millions of speculators millions of dollars."

— Livermore

I’m surprised crypto even thought tokenization would go through in the form the headlines presented this week.

The SEC’s reported “innovation exemption” apparently opened the door for third parties, unaffiliated with the companies themselves, to create tokenized versions of public stocks (Apple, Tesla, Nvidia, etc.) across multiple venues and products, without issuer consent or approval.

Being able to spin up not one but multiple synthetic wrappers or crypto-native versions of the same company’s shares, traded on parallel rails with lighter oversight, never mind the exotics and perps on top, feels like it could easily lead to the equivalent of 2008’s CDOs.

You’d get unlimited notional exposure, layered leverage through DeFi primitives, and products that often lack proper settlement, custody linkage, or the same shareholder rights as the traditional market, all while retail might think they’re buying the “real” thing.

Tokenization is still the path forward, but it needs to be done to complement and improve the current system, with clear guardrails, proper integration where possible, and real economic rights, not just create another layer of unchecked gambling and market fragmentation.

The news today is not negative in my opinion, it’s moving right along the institutional and gov backed line. We do not want another round of 20/21 shitcoins, scams and alike, we want a solid system that is unlikely to fail that will democratize owning US-listed businesses for the world.

The goal should be to enable fractional shares, worldwide access, lower transaction costs, instantaneous settlement, and true 24/7 global participation, all while preserving transparency, proper custody, and the economic rights that actually matter.

The thought that the casino view was fully logical to most shows the disconnect between the old 2020/21 vision and what’s actually happening and being built around the clarity act and institutionalization of blockchain tech.

Stock Market Wizards Quotes (32/117)

I represent the average guy out here in rural America, in the U.S. Midwest. I sit in my great-grandfather’s farmhouse, staring at a computer screen, and I can make a living trading. That’s why I believe there is hope for people anywhere to do this. But you have to be willing to work hard and pay your tuition, which is the money you lose while you’re learning how to trade.

Mark Cook

https://t.co/PnHdRVrNxg

THE SHORTEST TIMEFRAMES HAVE THE MOST EDGE!

This is a view I’ve mentioned before in interviews, but I’ve never taken the time to fully expand on.

In general, you want to be an expected value maximalist (within risk constraints). And the shortest human timeframes offer that. Yes, I mostly do bigger picture trades now but that’s due to scalability and quality of life, not bc they offer the most edge.

The paradox of markets is this:

-The shortest timeframes often have the biggest dislocations (most “edge per minute”)

-The longest timeframes often have the biggest tailwind (asset prices tend to rise over time)

-The middle is where many traders get chopped up

This principle is the reason why there were traders at Trillium that could be positive hundreds of days in a row. You’ll never see that with a swing trader or value investor.

1. Why short timeframes can have so much edge

At very short horizons, markets can be temporarily inefficient because of:

-forced behavior (stops, liquidations, margin pressure)

-delayed human interpretation of information

-mechanical flows around opens/closes

-short-lived supply/demand vacuums

Those create moments where price can be “wrong” for seconds/minutes relative to where it’s about to reprice.

In fact, at the extreme short end of human discretionary trading like the two following examples, you can find opportunities that approach 100% win rate with a profit factor of 10+. Of course there is a trade-off which I’ll get into.

2. Order flow imbalances

One of the biggest short-term edges is understanding order flow imbalance. Yes, these happen far less of the now than they used to as discussed in my interview yesterday with Serge. But they still exist particularly during times of market extremes.

-aggressive buyers/sellers temporarily overwhelm passive liquidity

-one-sided flow causes price to overshoot or stall

-liquidity can disappear at key moments, then refill at new levels

You’ll see this around:

-opening auctions

-panic flushes / squeezes

-large fund rebalancing windows

-crowded positioning unwinds

This is where the tape can get dislocated from “fair” value in the short run and where active traders can extract edge. It is also why some of those hyperscalpers like @EdBarry4 are positive so many days in a row.

3. Breaking news is where discretionary human traders still have the edge over algos in interpreting novel headlines.

There’s usually a sequence:

-headline reaction

-second-order interpretation

-positioning unwind/chase

-stabilization

If you’re prepared and fast, these windows can be highly asymmetric. In fact, breaking news can offer some of the best opportunities in existence, especially when applied to liquid instruments (think April 2025 tariff headlines!).

In fact, I’d argue tariff headlines due to their massive impact on global markets are some of the best expected value opportunities I’ve ever seen.

4. But there’s a tradeoff: liquidity + scalability

The shorter the timeframe, the more your edge depends on:

-execution speed

-order optimization

-fee minimization

-slippage minimization

So yes, edge can be highest in short windows but liquidity becomes the constraint. Many short-duration edges don’t scale without degrading returns.

That is why many traders post eye-watering returns in small caps but then you constantly see them doing their dumb small account challenges. It’s because their strategies don’t scale!

5. Beware the middle ground.

Take this thought experiment. Let’s say $AAPL flash crashes 90%. With near-certainty, Apple will bounce within minutes close back to the unaffected price. What happens overnight is more of a toss-up. What does the market do? Does news come out? Yet over the course of 5-10 years, it’s likely the $AAPL goes up.

In that middle ground, you take on variance from overnight risk, headline risk, and market risk. But don’t benefit much from the fact that over years, markets go up. It’s much more of a coin flip whether we go up or down any given day.

If I had to guess, the most edge is in tenths of seconds and seconds for humans. The least edge is in the window of weeks. Why not compete at even faster timeframes? Bc then you fight with HFT, commission structures, co-location, and more.

6. So how to apply this?

First, this is useful for the sniff test. Understanding that there is a trade-off between edge and liquidity is critical!

There is a reason why you see small cap traders that can scale a small account over 1,000% in a year (think early days of @theshortbear). There is also a reason why Warren Buffett has approached market returns.

It’s that trade-off between edge and scale. Similar to the general trade-off between win-rate and profit factor, it’s a safe assumption that these often tend to move inverse to each other. It’s the reason why that if I managed $1B my returns would probably get quartered and if I managed $10B my returns would approach market returns or worse.

This framework is also useful for finding the most edge and understanding your strategies. If you’re moving to a higher timeframe, you generally SHOULD expect more variance. That comes with the benefit of scalability.

Similarly, if you want to study micro-inefficiencies, particularly in less efficient markets like crypto, you can find some insane edges there.

TJR is a racist fraud scamming people on a fake dream. Yes, any real trader knows that, but here’s the sad truth:

If you talk to high school kids, college students, uber drivers, and more… they follow TJR not knowing any better. He causes true financial harm to a young, vulnerable population. And despite that, companies still choose to partner with him bc greed and influencer reach outweigh ethics.

Most of TJR’s followers will learn the hard way, but that doesn’t mean we shouldn’t speak out when people are being wronged.

Great video, particularly the points regarding the off-shore CFD broker scams. That is exactly how @tradesbysci pulls off his fraud w “Liquid Brokers”, an off-shore unregulated shell co that he uses to send his sheep followers to the slaughterhouse.

I've used OpenClaw for over 210 hours the last month

More than anyone on Earth

In this video I go over EVERY single lesson I've learned about OpenClaw.

From set up, to use cases, to why VPSs suck, to security. Everything

The only OpenClaw video you'll ever need is here:

EDGE REVEALED: How an Ex-Jane Street Trader Finds Edge in Markets & Life

Agustin Lebron @AgustinLebron3 (former Jane Street trader, author of The Laws of Trading, now working at an AI startup applying reinforcement learning to market execution) breaks down what edge really means — and how to find yours in trading, careers & life.

“Edge is something that either you know or you can do that the marginal participant in that market either doesn’t or can’t.”

We cover:

- What edge actually means & how Jane Street builds organizational edge (their worst skill is still "pretty decent")

- Why you can never truly know if you have edge — the statistical vs intuitive approaches

- The consolidation of quant trading: from dozens of options firms to a handful of giants

- The gamblification of everything — retail trading, sports betting & prediction markets fueling quant profits

- What it was like having Sam Bankman-Fried (@SBF_FTX) as a Jane Street intern: "Day one, I'm going to ask all the questions"

- How to apply edge thinking to your own career: find what you're differentially good at

- Raising teenagers in the AI age: why the traditional path still works, but other paths are opening up

00:00 Introduction

00:44 What is edge in financial markets

01:43 Jane Street and organizational structures for quant trading

03:46 Identifying and validating edge in trading

06:22 Navigating extreme market events and volatility

09:37 Future of quant trading and consolidation

12:15 Why quant firm profits have increased

14:42 The gamblization of everything

15:55 Who should pursue a career in quant trading

18:19 Applying the concept of edge to career and life decisions

20:56 Advice for interns to excel in quant trading

23:44 Predicting long-term success in trading interns

25:08 Sam Bankman-Fried as an intern and FTX reflections

28:15 Reasons people leave Jane Street and what they do next

31:19 Advice for young people in a changing world

36:09 Navigating job insecurity in tech-driven roles

38:55 Where to live if you want to be successful

40:28 Raising kids for a rapidly changing future

42:55 Questions young people should ask themselves

44:45 Outro and book recommendation

R.I.P McKinsey.

You don’t need a $1,200/hr consultant anymore.

You can now run full competitive market analysis using Claude.

Here are the 10 prompts I use instead of hiring consultants:

My favorite @perplexity_ai prompt I’ve made for traders.

Feel free to copy and use.

————————————————

Please analyze [TICKER] for me and provide the following, concise and clearly organized:

1. **Explain what the company does in like I'm 12 years old** - three short bullet points about what it does and any helpful relatable examples and analogies.

2. **Professional summary (max 10 sentences)** - industry, main products/services, primary competitors (list tickers), notable metrics or achievements, competitive advantage/moat, why they are unique and if they are a biotech provide if they have a commercial product or in clinical stages.

3. In a table, provide the follwoing:

* Any hot theme, narrative or story of the stock

* Any catalysts (earnings, news, macro)

* Any significant fundamentals (huge growth in earnings or revenues, moat, unique product or service, superior management, patents etc)

4. **Show all the main news/events for the last 3 months:** - Use a bullet-point table for: - Date (YYYY-MM-DD) - Event type (Earnings, Product Launch, Analyst Upgrade/Downgrade, etc.) - Short summary (max 1-2 sentences) - Direct source link - Mark any major price-moving events (surprise earnings, large guidance shift, top-tier analyst actions).

5. **Mention any recent insider buys/sells or institutional filings if visible.**

6. **Summarize how the stock is moving vs. main competitors and overall sector trend in past month (up/down).**

7. **Flag upcoming catalysts (earnings, product launches, regulatory events) in the next 30 days.**

8. **Note any changes in analyst price targets for this ticker during the period above.** - Format for easy review. If possible, use tables for events and peer moves. - Respond in clear, concise, easily readable style for use in trading decisions.

Overall, Focus on the reasons why the stock can make a big move in the future - earnings, sales, guidance, product launches, analyst upgrades/downgrades, insider buying especially from CEO/Founder and executive team, partnerships, and sector/news catalysts. I want to focus on stocks with catalysts and themes as catalysts are the cause of big moves in the stock market.

Finally, discuss and bring up any relevant previous perplexity queries and conversations.

JAN ‘26 TOP OPPS

A much slower and more difficult month with main focus of course on the metals. Big money to be made but it certainly was not easy. As always these monthly opps are dissected in detail as part of my course.

1/7 $SNDK / $MU / $WDC

1/8 $RGC

1/14 $SLV ah

1/26 $BNAI metals

1/27 $GLD intraday

1/28 $CVNA. /GC /SI AH. $META AH

1/29 /PL /SI /GC

1/30 more metals…

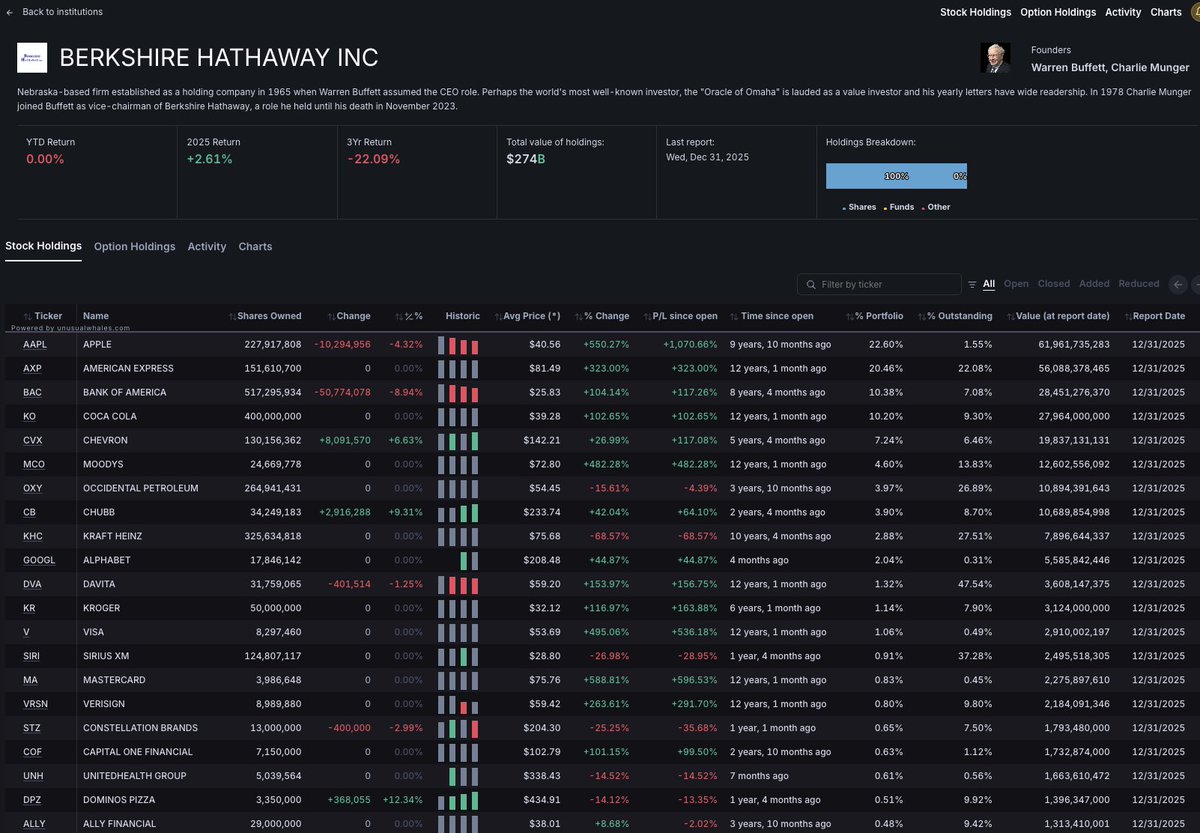

The time leading to the end 80s were his prime.

Influenced by Charlie Munger, Buffett shifted from "cigar-butt" value investing (buying cheap, mediocre companies) to buying wonderful companies at fair prices.

He also partook in merger deals.

Towards the end of the 80s, he leveraged the 1987 crash to build massive positions in dominant brands, most notably a $1 billion investment in Coca-Cola (1988).

He focused on capital-efficient businesses with immense pricing power, such as See’s Candies and Capital Cities/ABC.

In the 80s, Berkshire’s smaller capital base allowed home run stocks to move the needle significantly.

The annual shareholder letters teach a lot about what he was doing then. The snowball (book) and the strategy blueprint do too.

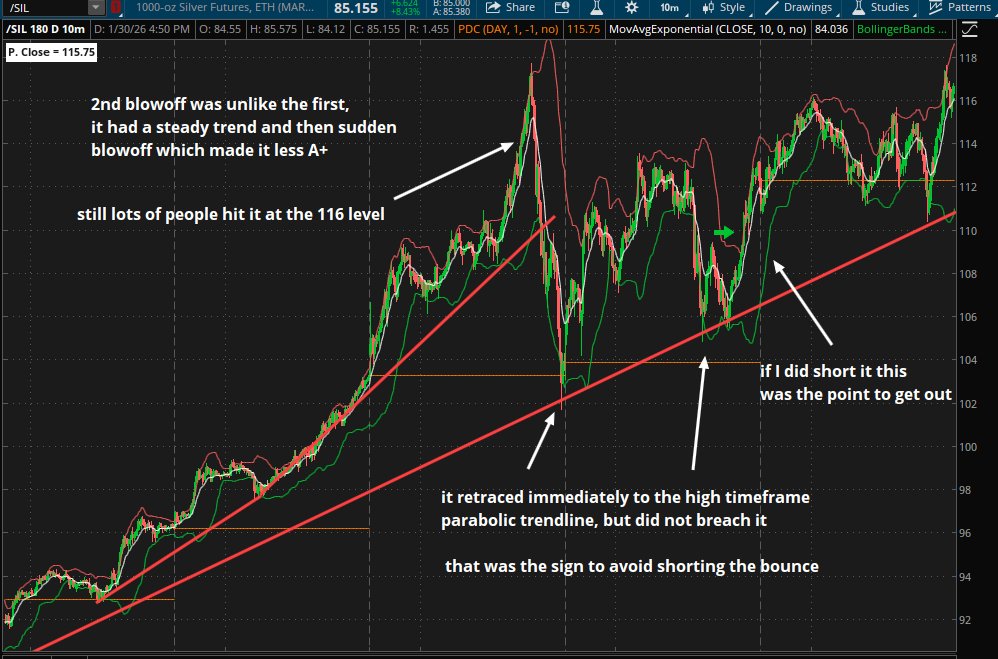

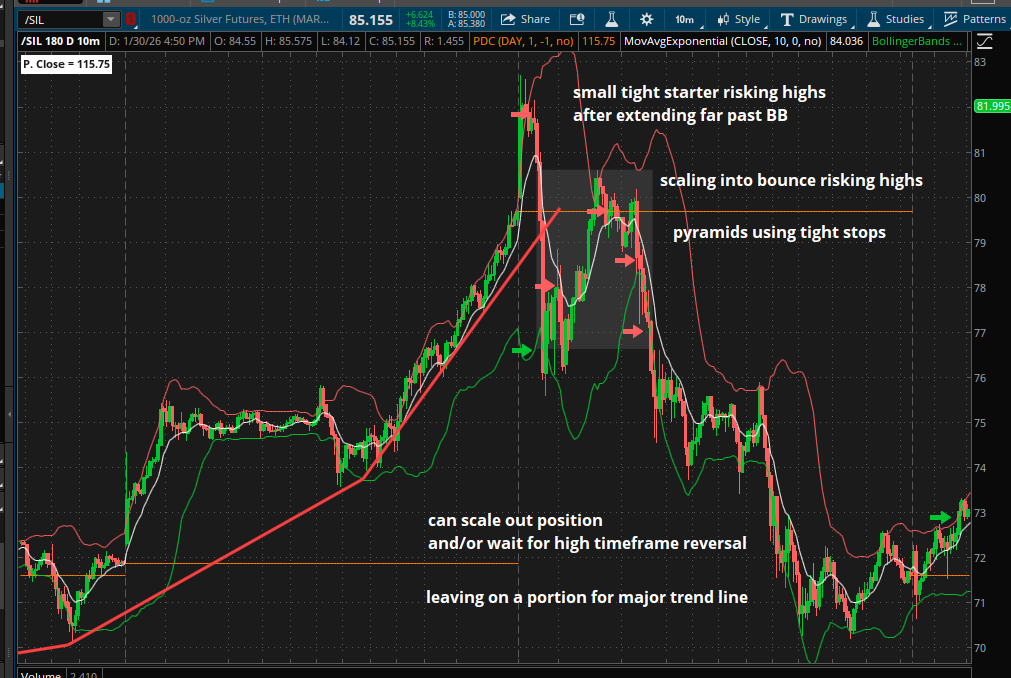

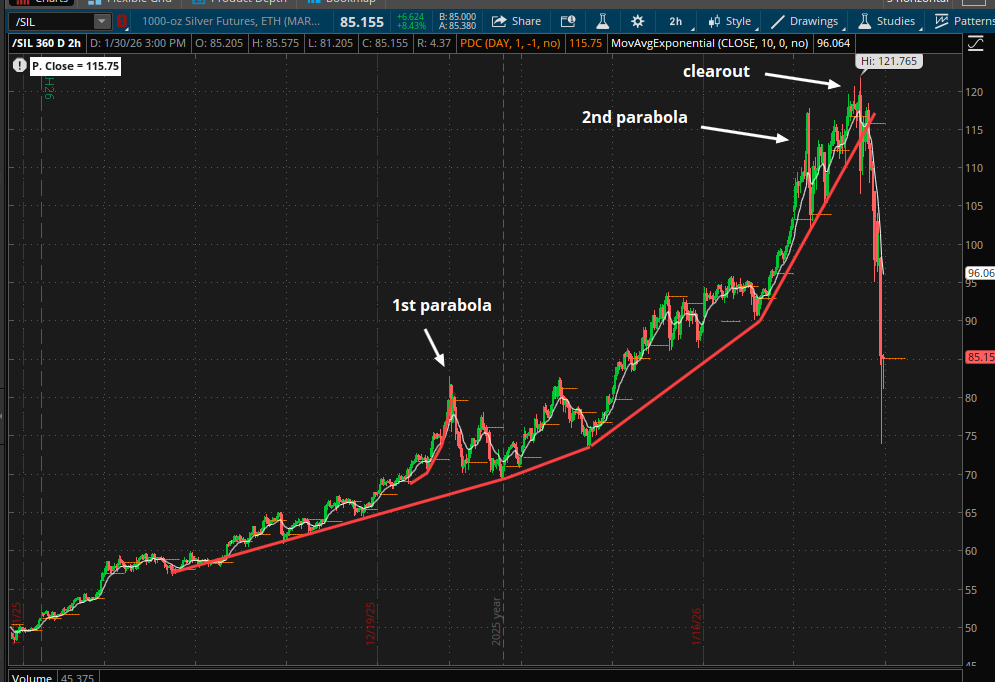

My Recap of Silver $SLV:

I only played small parts of the move and ultimately avoided silver after December. I'm up slightly on it and decided to avoid the rest of the move expecting a huge headache. I also had some other stuff in the works so decided my focus would be best on that. Hindsight definitely a mistake but nonetheless a huge learning experience. I think the mechanics of this move were extremely clear in hindsight and opportunities like this will appear all the time (even if to a smaller degree).

With major parabolic moves like this I think the best approach is a big picture one where you get a starter into the blowoff moves, but don't get most size until the parabolic trendline is broken and it has a major bounce (which can be over 75% retracement).

During the run there were several parabola's that seemed like the top at the time. However, the eventual top was in form of a clear out.

Using the big picture with indefinite hold you would've taken 2 cuts prior to catching the big panic. However, watching the parabolic TL can be a helpful guideline.

The first one was probably the most straightforward and cleanest. It happened during the overnight session on Sunday at midnight.

We had a very clean parabolic trend, clean break of that trend, and bounced towards 75% retracement.

I think the best execution approach is scaling into bounce risking highs and pyramiding aggressively/trimming deep backsides.

The 2nd blow off was unlike the first. The action leading up to the 2nd blowoff did not have a clean parabolic trend. Also, after the initial pullback there were signs such as watching the major trend line to avoid getting chopped on the bounce.

After the clearout over highs, we broke the highest timeframe trend and had a very clean bounce up into the 75% retracement level. From there the backside was butter.

All the executions shown were hindsight expectations for how I would've liked to have traded this.

It's very hard to do but with big movers like these I think moving to higher time frames can cut out most the noise and ensure you capture the most EV.

$SLV $AGQ $SILVER

The morning opened with a clear regime shift.

Trump nominated Kevin Warsh for Fed Chair. Warsh is widely viewed as a hard-money hawk. At the same time, a U.S. government shutdown was averted at the last minute.

Gold and silver had effectively been propping each other up over the past week. Silver looked vulnerable, but gold’s parabolic move prevented a breakdown, resulting instead in a double-top structure.

This setup has historical precedent, most notably in 2006 and 2011.

Quietly behind the scenes topping macro news added up: Greenland resolution, Tariff step back, FED chair hawk(ish)...

As the macro narrative flipped, the “chaos premium” and “debasement trade” evaporated almost instantly. This came on top of rising margin requirements and billions of dollars in call options being offered throughout the week.

With today being Friday, those call positions became trapped. Market makers were then able to delta-hedge back toward neutral by selling underlying shares.

That’s when the dominoes began to accelerate.

As silver broke below key whole-number levels, where the largest call strikes were concentrated, selling pressure increased exponentially. Billions of dollars in call options rapidly went to zero.

The selloff intensified into the 1:30 PM window, driven in part by the $AGQ rebalancing mechanism.

As a 2x leveraged ETF, AGQ must rebalance daily to maintain its leverage ratio. A 10% drop in silver leaves the fund over-leveraged, forcing it to sell futures into weakness.

The “Kill Zone” (1:00–1:25 PM ET) is where the mechanics turned brutal:

1:00 PM: Order cut-off

1:25 PM: NAV calculation

HFTs and authorized participants knew AGQ would be forced to unload significant volume. They front-ran the 1:25 PM window, stripping remaining liquidity.

Silver didn’t merely decline, it gapped through multiple support levels. Selling pressure peaked precisely at the 1:25 PM NAV print. Once the mechanical rebalancing was complete, price finally found a floor.

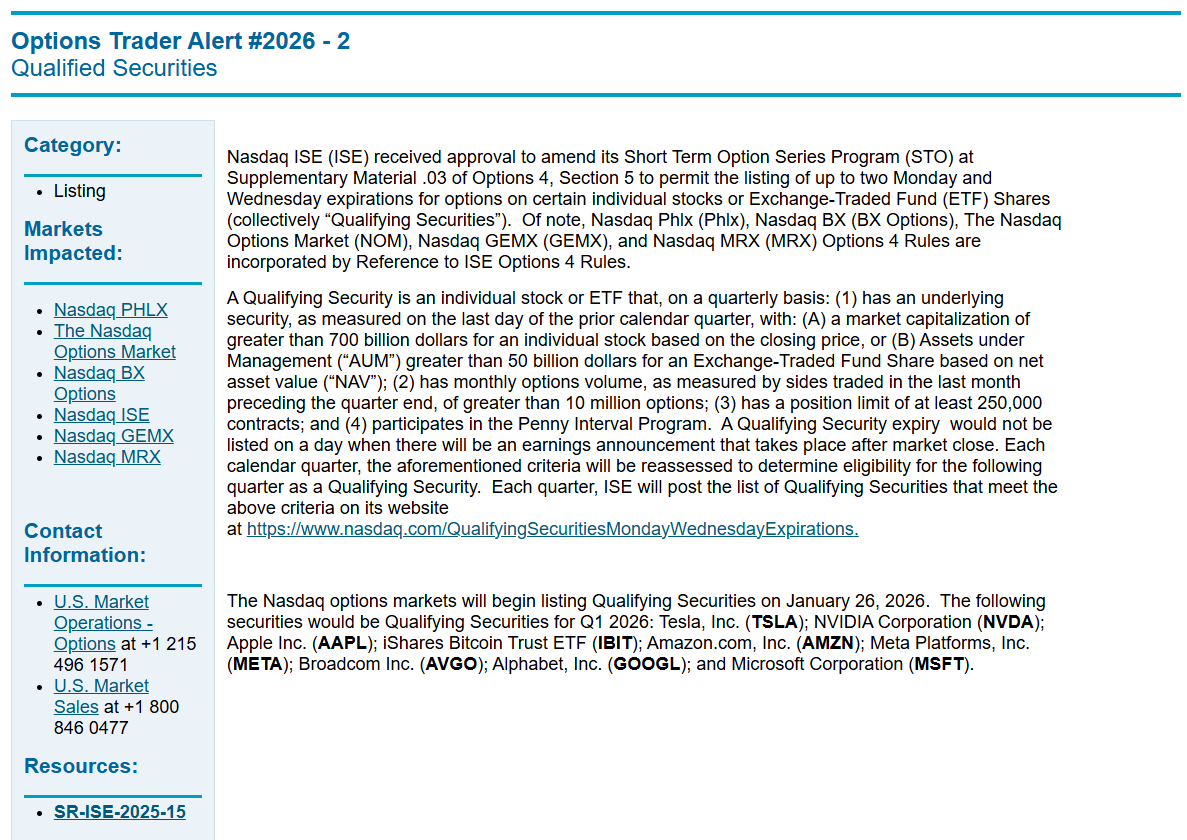

🚨 BREAKING 🚨

Monday and Wednesday expirations have been approved for a specified set of equities under strict eligibility criteria, beginning listing on January 26th.

This is a major step toward a complete expiration cycle, enabling 0DTE trading on Mondays and Wednesdays for qualifying names.

Initial Q1 2026 tickers:

$TSLA, $NVDA, $AAPL, $IBIT, $AMZN, $META, $AVGO, $GOOGL, $MSFT

Wonderful lesson for traders...

"Be your own best friend.

Cheer yourself on.

Nobody is gonna treat you better than you.

If you are in the best headspace your (chances of) success go higher." @MookieBetts 👇👊