$DRX.TO CFO retiring on December 31st, and will remain a strategic advisor beyond that. Clearly an orderly retirement and I am not reading anything into it.

$DRX.TO Had the State of Defense procurement of Canada in their facility yesterday, at the same time as new F35 maintenance hangars were announced in Quebec. is it a coincidence? it would probably be a small contract but it showcases ADF's growing place in the defense ecosystem

I recently bought $DRX.TO - ADF Group, a Canadian fabricator of complex structural steel. They have 2 fabrication facilities in Quebec and 1 in Montana.

The stock recently sold off on near-term margin noise tied to steel tariffs and their LAR acquisition, creating what I think is a really good entry point

Why It's exciting:

1. Trades under 4x depressed EBITDA with a clean net cash balance sheet

2. Backlog has more than doubled in a year from $300m to $650M+, with strong bidding activity continuing.

3. Beneficiary of the "Build Canada" Thematic

4. A recent acquisition I believe will look like a no-brainer in hindsight

ADF is one of the best-positioned names to play the 'Build Canada' theme. They stand to benefit from a wave of infrastructure spend: airports, Ontario nuclear, hydro expansion in Quebec, BC, and Newfoundland, and energy/industrial buildout in the west. A "Buy Canadian" mandate further improves their competitive position and will spur industria/constructionl projects

Historically, they were 90% US, 10% Canada. However, with last year's tariffs, the company has aggressively pivoted its backlog which now sits at 60% Canadian and 40% US with a good chunk of the work segregated between the two countries. I expect Canada to make-up a bigger percentage of the mix overtime.

The most exciting part of the story is the LAR Group acquisition. Historically, ADF Group did primarily industrial & commercial projects. Think airports, warehouses, bridges and some industrial plants. LAR was a distressed, over-levered steel fabricator for the hydro sector. A specific contract blew them up and ADF stepped in as the white knight through a reverse vesting order approved by the government. It allowed them to acquire LAR's assets while having all liabilities extinguished, BUT keeping all certifications intact.

ADF is now certified to operate in both the hydro AND nuclear markets two of the most infrastructure-intensive sectors in Canada's near-term pipeline, in addition to potentially bidding for some of the big 'nation-building' projects the Canadian government has proposed.

The near-term overhang: LAR is working through a tail of low-margin legacy projects, which weighed on Q4 results. LAR currently runs ~10% gross margins vs. ADF's mid-20s. Management doesn't expect margins to deteriorate further from here, but the meaningful inflection only comes in H2 2026 and into 2027, as ADF deploys ~$35M to automate LAR's facilities. LAR is understood to be the preferred vendor for virtually all Hydro-Québec projects and so I expect more work to come their way. And let's not forget the government of Quebec approved the CCAA proceeding at record speed. Clearly Hydro-Quebec was pretty desperate to have ADF acquire LAR group as there aren't many companies capable of doing that type of work.

The second near-term overhang is the recent US steel tariff changes which puts a 10% tariff on the total value of steel transformed outside of US, but that uses US Steel. For some jobs, it made economical sense to ship US steel to Terrebonne and then ship it. It will impact their Q1/Q2 results, which caused last week's sell-off.

The market is focused on near-term headwinds but It's missing the forest for the trees.

Canada is entering one of the largest infrastructure build cycles in its history and ADF is one of a handful of Canadian companies capable of fabricating the complex steel structures these projects demand:

=> Hydro-Québec: $35–45B capex plan over the next decade

=> BC Hydro: $36B in regional investments over the next decade

=> Ontario & Atlantic provinces ramping hydro capacity

=> Ontario nuclear: plant refurbishments, SMRs, and Bruce Power expansion

And none of that includes the 15 'nation-building' projects the federal government has fast-tracked or the hundred of projects that will emerge from Canada's defense spend goal of 5% of GDP.

Despite the headwinds, the company expects to have stable gross margin, with a much bigger revenue number. There is a clear path here for the company to achieve 15% EBITDA margin on potentially over $500m of revenue which would get me to a target price of $17 at 6x EBITDA over the next 2-3 years.

$OGD.TO this is going to drive significant utilization and ultimately a big pricing tailwind for the drilling services cos....earnings have yet to move while valuation is completely undemanding

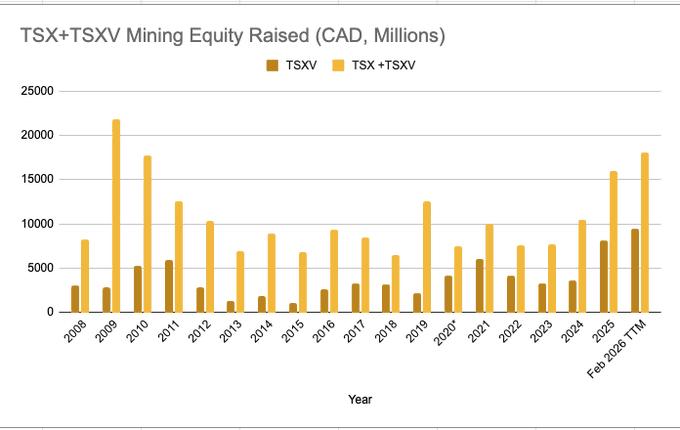

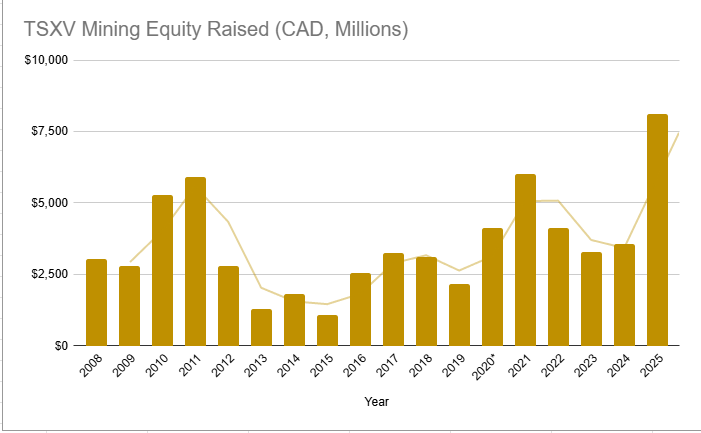

Mining companies raised ~1.3b CAD on the TSXV in March. This was only slightly below the 1.36b they raised in February 2026 & >4x what they raised in March 2025 (292m).

So TTM TSXV mining equity raised still reached a new all time high in March $OGD.TO $FAR.TO $MDI.TO $GEO.TO

I am back into $OGD.TO after selling it late February. The recent pullback makes for an attractive entry point. I think momentum is materially picking up. Utilization is approaching 70%+ and pricing should start being a material tailwind. cheap (<5x ebitda) no ebitda numbers that could get wild. Still think it ultimately gets acquired. Target price remains $3.75

I am long $OGD.TO - Orbit Garant

They offer Drilling Services for gold and copper companies. 72% Canada, 28% International (Chile primarily) and 65% gold/30% copper

approximately 65m market cap, 100m EV, $25M EBITDA estimated for 2026 or 4x EBITDA

It's a pretty simple thesis - Gold/Copper prices are very strong which will support exploration. Equity raised globally for mining companies accelerated massively starting october (Q4) of 2025, doubling versus 2024... and has continued into Q1. Exploration usually picks up 6 months following significant financing rounds. They have heavy exposure to Juniors exploration (22% of revenue) which has yet to pick-up.

The drillers have seen significant competitive pricing pressure over the last 24 months and as the market tightens, that should turn into a tailwind. OGD is at 55% utilization with a goal to reach 70% and has reached 80% in prior cycles. Management has already confirmed significant pick up in bidding activity in recent months and has been an active buyer of their stock.

Closest peer, and juggernaut $MDI.TO trades at 10x EBITDA and is making new highs daily. MDI trades at over $1.6m EV per rig versus OGD at $540K EV/rig. MDI has been acquisitive in the past, most recently buying a LATAM drilling company for $115m for 92 rigs ($1.25m per rig). I believe OGD would be a clear acquisition target for MDI as they fit perfectly within their strategy (North America & LATAM focus + specialized drilling) and MDI is actively looking to consolidate the market to reduce competition and pricing pressure.

Founder Alexandre Pierre remains on the board, and owns 20% of the shares outstanding. He is a known seller. Selling to MDI would make perfect sense to finally monetize his full stake.

Clear path to $30m of EBITDA (and more) at 6x EBITDA, and assuming $30m of net debt, it would be a $3.75 stock

$BRAG Board Member Thomas Winter just filed his opening stock balance - he bought 250K shares prior to joining the board. Great vote of confidence. Industry juggernauts joins the board of a tiny cap. But clearly not the 1m share buyer from the CEO

In other news... Alberta July 13

6/ given the depressed valuation, both financial and strategic parties would be interested. Matevz is a willing seller, and has been for a decade now. If they put up a few good Qs and show product momentum, this could easily sell for $5.00 USD + using 6x this year's EBITDA.

1/ $BRAG Lots of good stuff happening under the surface. Betcity is now 15% of revenue, down from 45% at its peak 3 years ago! Meanwhile both Brazil & US now represent over 20% of revenue growing 40-50%+. Despite a big anticipated decline from Betcity exiting in May...

5/ When the board ran the strat review, I was of the opinion that the biz would not sell. Now, I think it will. The story has been cleaned up (FCF positive, no revenue concentration, multiple markets opening up, product momentum, legislative momentum), and...

$BRAG - Reported Q4 results. More importantly, the co elected another big shot in the iGaming space, Thomas Winter. Founder of Golden Nugget, and prior CEO of Betclic, and board member of $RSI...Could he be the 1m share buyer from Matevz? I'll post more details on the Q itself

@christankerfund Contracted rates in the presentation for their drybulk sits at 16K, 16.8K and 20K...Their third tanker that was not contracted is now at 35K until july 27. Q2 earnings should be nicely higher than Q4/Q1

I've fully exited $OGD.TO - I think it continues to move higher from here but looking to allocate capital in another high conviction idea. Still dirt cheap and cycle just getting started, but wanted to be transparent. congrats whoever joined!

$OGD.TO reported good results with revenue +10% and EBITDA +13%.

Importantly, Drill utilization hit its highest level in 2 years. The commentary is bullish with utilization rates expected to further improve, and seeing 'accelerated requests for proposals from junior exploration in canada' and expects 'minimal mobilization costs' to improve utilization

Stock trades at 4x NTM EBITDA while peers are 10x in likely one of the biggest exploration boom seen in the last decade

I fully exited $DAC. I have been allocating to other shipping names that have more torque. Still think it works here given the undemanding valuation and a management team that is building a solid foundation to weather all storms, but happy to move on. Congrats to all who joined!

$DAC steady as she goes... BVPS now $207. 100% contracted for 2026, 87% for 2027, and 64% for 2028. $76m buybacks for the year. Earnings has started to grow again and drybulk is becoming a real contributor to the bottom line. On the negative side, they've bought 5 new containership and 2 new drybulk ships + made a new LNG investment. Their capital allocation seem to be more speculative than in the past. Containership orderbook continues to run hot at 36% of the fleet but it likely will not impact them Big position for me so given the above, I will be taking some gain on the strength. However, they have likely returned to earnings growth and discount to BV remains substantial, so I think it likely keeps grinding higher