1/ We're entering a new healthcare era: virtual-first providers are upending traditional care delivery.

Virtual-first providers recreate real care pathways with a digital mindset, providing end-to-end medical care.

👇 Why virtual-first is the future:

https://t.co/rwfk0V7C0i

@Tom_Cassels I think there's certainly margin in care delivery, just in specialist procedures (ortho, etc.) and not in FFS primary care. HCA's margins aren't bad!

Differentiated care models that deliver better outcomes at a lower cost (& happen to be virtual) will continue to grow.

These models tend to blend condition-specific care models, connected with existing care providers, & new business models to deliver differentiated value.

Lots of buzz around Walmart & Optum exiting virtual care & if telehealth is "over"

"Virtual care" solutions are not all the same. Some elements have certainly been commoditized, like virtual urgent care. "On demand" care from random clinicians to treat sinusitis isn't different.

@adkravetz I think it’s a combination of the CFO wanting to cut costs, HR looking for a simpler patient experience, and vendors struggling to prove value.

💯 Employers are a WAY tougher market than most anticipate.

Tons of employers aren’t adding new offerings, and some are even removing offerings.

You have to really stick out and be easy to implement to be successful.

Here’s a really spicy take but I’ll say it. I don’t not think selling to employers right now is a viable strategy for *most* new health tech companies. It’s noisy, over saturated and most employers are very savvy.

This is a good piece. I would add one more element…

Many clinicians are excited about moving toward value-based care, but CMS and many insurers only permit large groups to participate in the more interesting and lucrative forms of VBC.

Hence: aggregation.

Was in @CNBCTheExchange today discussing CVS announcement of cost plus pricing at its pharmacies. Some initial and admittedly rough thoughts that I shared: There was probably some advantage to CVS’ PBM to continue to do it the old way but now as that advantage erodes, especially as congress is set to act on rebates, then the benefits of paying pharmacies based on complex contracts struck by their PBM that baked in rebates and other considerations is starting to diminish, and the disadvantages placed on their pharmacy network start to become more paramount. They are willing to give up *some* of the declining advantage/margin on the PBM side to provide some competitive edge to their pharmacies and perhaps significantly improve the consumer experience. Pricing at the pharmacy county should become more predictable for patients and pharmacy revenue more stable. The policy should apply to all pharmacies CVS works with not just its own pharmacies. That’s because, as part of Medicare regulations, there is a concept called "related parties" built into the bidding process for Part D drug plans, which CVS also operates. CMS basically makes sure that healthcare entities operated by Part D plan sponsors — like pharmacies and clinical providers — can’t get paid differently than the going market rate for a service, otherwise the worry by CMS was a plan sponsor may overpay its own network to game its medical loss ratio. Of course CVS is not doing that here, but that rule does mean that CVS has to offer stable terms across all pharmacies, its own as well as those its drug and health plans contract with. I do think this move today will make the patient experience at the pharmacy counter more predictable — there will be fewer out of pocket surprises, so consumers may prefer to come to CVS over time. If CVS is no longer paying pharmacies based on some economic derivative that’s calculated off of the terms of its PBM contracts with drug makers, it probably makes those terms — on the margin — less valuable. My sense is what this move signals is that CVS is saying “OK that whole rebating structure is eroding, so we need to stop clinging to it in a circumstance where it could also be hurting the retail experience for our customers.” Kudos to CVS for leading here, and making this move.

While $99/month seems great for OneMedical, consumers may be surprised by how high their per visit fees are, given ONEM's relationship with health systems.

Will be interesting to see how Amazon threads the needle of consumer affordability & health system revenue moving forward.

@nikillinit Yes, $99/year*! Thx.

I'm assuming they're not lowering the price to $99/mo for enterprise offering as it's part of the Prime bundle? Curious how that will play out, too.

We are thrilled to announce our investment in Visana Health!! We are honored to continue supporting @JConnol and the entire Visana team — as they continue to use technology to build a clinically rigorous women’s health company. @vlan8@uma_veerappan

https://t.co/mO0uvR0Xsj

Startup champions within large healthcare companies are the ones really driving early startup success.

Willingness to take risks is rare, especially in large healthcare companies.

the champion at a large company that helps a young startup get their first enterprise deal has no idea how much they’re changing people’s lives and never gets enough credit for taking a risk on a no name company

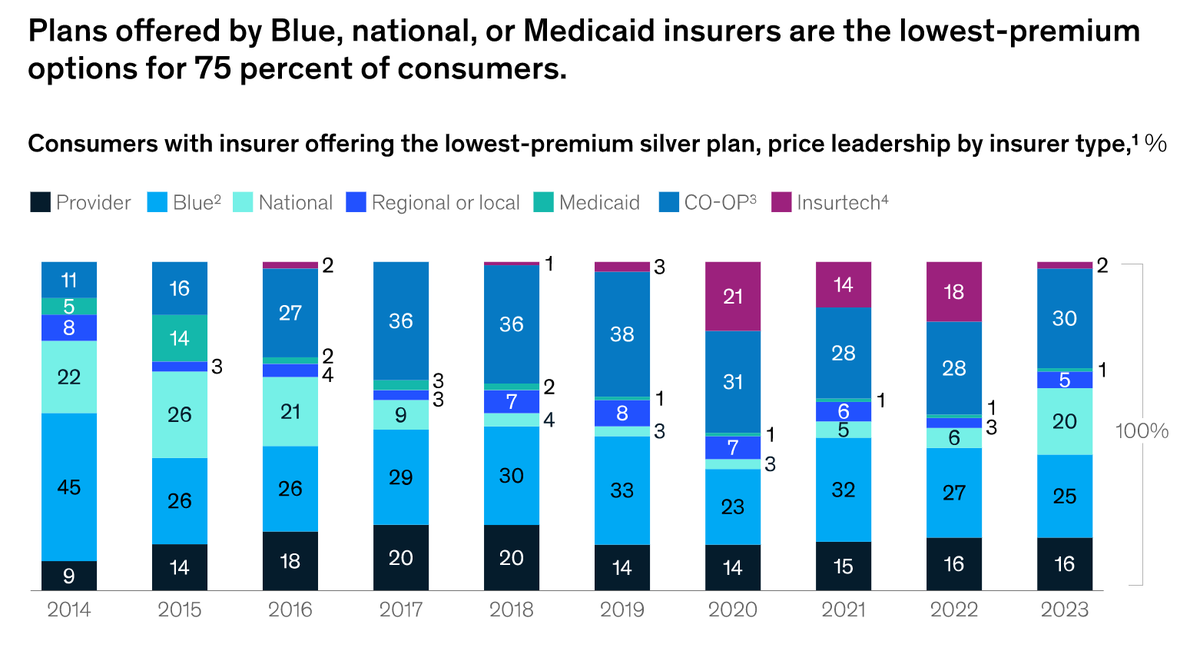

Insurance is hard to disrupt -- and one of the biggest issues for "insurtechs" is keeping costs down.

Despite their promise, many have struggled to control MLR. With the stronger investor appetite for profitability, many are increasing prices in 2023 to improve profitability.