You can read about the sad fate of poor Archie Gallienne (pictured) and his twin Adolphus within the opening feature of my new LOOKback series focusing on good old Guernsey surnames - starting with the Galliennes tomorrow in the @GuernseyPress

Loving this new Podcast - ‘Too Young For This Too Old for That!’ where two lives 30 years apart meet in conversation. Usual channels via https://t.co/WRE5h47sB5

So excited to announce that I will be ‘Mistress Ford’ in ‘The Merry Wives of Windsor’ directed by Steve Grihault in The Mack Theatre

The ‘CHER’ cast:

Saturday 11th May 2.30pm

Tuesday 14th May 7.30pm

Thursday 16th May 2.30pm

Friday 17th May 7.30pm

Saturday 18th May 7.30pm

@thedogsheffield @omid9 Lyle had strong religious beliefs, which is why the tin’s famous logo depicts strongman Samson’s ‘lion and bees’ from the Bible’s Old Testament

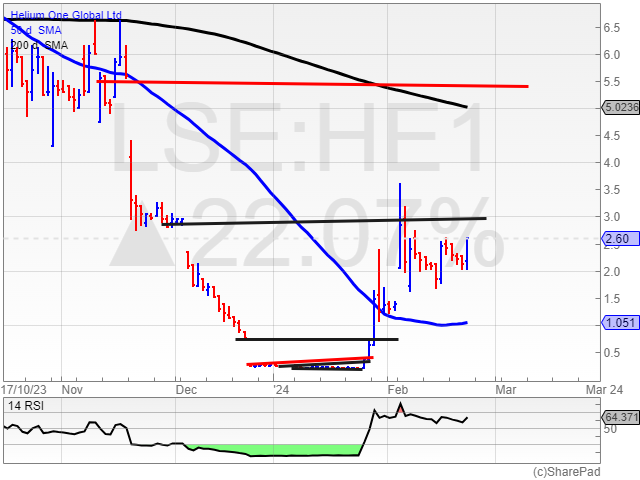

Helium One (HE1): Remains constructive. consolidation above a rising 50dma, higher lows above Feb gap. Above Dec 3p gap could hit top of Nov gap at 5.5p by end of March. Ideally, remains above 2p from now. #HE1

I've been doing a bit of work on #AUDIOBOOM#BOOM's valuation.

M&A in the podcasting space tends to be based on enterprise value/sales ratio (or price-to-sales ratio, which is the same except that it does not account for cash or debt on the balance sheet).

Transactions in the space over the past five years for which there is publicly available financial data include:

- iHeartMedia acquiring Triton Media for an enterprise value of $228m (an EV/Sales ratio of 5.0x)

- Amazon acquiring Wondery for an enterprise value of $300m (an EV/Sales ratio of 7.5x)

- Sirius XM acquiring Stitcher for an enterprise value of $325m (an EV/Sales ratio of 4.5x)

- Spotify acquiring Gimlet Media for an enterprise value of $230m (an EV/Sales ratio of 10.2x)

That's a mean EV/Sales ratio of 6.8x.

In the graph below, I have charted Audioboom's quarterly revenues over the past 5 years / 20 quarters from Q1 2019 to Q4 2023 (y-axis, left side) against the average weighted market capitalization for each quarter (y-axis, right side).

I have used a PSR over EV/Sales as BOOM did not have any significant debt in the period, nor did it ever have surplus cash (in fact, it relied on cash injections from equity raises until 2020). Accordingly, PSR in BOOM's case is an adequate proxy for EV/Sales, when comparing against the aforementioned M&A activity.

On average, across the 5-year period, BOOM has traded on a current year PSR of 1.85x (and a median PSR of 1.55x).

The combination of the share price collapse throughout last year (which bottomed in early November), coupled with the return to strong topline growth in Q4, means that the stock is now trading at a 62% discount to where it has traded over the past five years, on a PSR basis. Or to put it another way, just to be trading in line with where it has (relative to its revenues) over the pat five years, BOOM should currently be priced at 717p.

Now consider the known M&A valuations of the past five years. A mean EV/Sales ratio of 6.8x - versus BOOM's currently at 0.68x.

Based purely on previous M&A activity and using the peer group average, BOOM's "premium takeover" valuation would be 10x / 900% higher than it is: 2,500p.

The challenge is to understand why the share price collapsed over the past two years, and if the collapse was too extreme / unwarranted. My own view is that a temporary topline contraction in 2023 - caused by both the loss of a key podcast (Morbid) in 2022, and by a major downturn in the global advertising market between Q3 2022 and Q3 2023 - caused major uncertainty and yes, did drive an unwarranted sell off.

The next challenge is to understand what could catalyze a major (and sustained) share price rerating again. For me, this is very simple: continued topline growth (following the excellent Q4 2023), and a return to healthy profitability, which leads to forecast upgrades.

My own view is that BOOM smashes the consensus revenue forecast for 2024 of $79m, and even more so the EBITDA forecast of $1.3m. The RNS of 16 Feb suggests that the Company is already building on the Q4 revenue figure of $19.2m. Furthermore, the Company has become much leaner over the past 12 months (headcount reduced), and has reduced minimum guarantee obligations for its podcast creators (will be over $2.5m throughout 2024).

Beating market forecasts is the way to go. @Audioboom's management is acutely aware of this, following that remarkable share price run over 2 years that began in H2 2020.

Over the past 4-5 months, the Company has been trading at the steepest discount it ever has, relative to its own revenues. If it were tracking its own historic valuation, it should be at over 700p right now. In contrast, the Company is now arguably in its strongest ever position. Its topline is growing rapidly once more - outstripping the growth of the wider podcasting industry, in fact; and is likely to move into healthy profitability this year. Management is openly signposting that 2024 will be a record year.

Forecast upgrades will come, and will drive BOOM's share price much higher over the next 12 months, I believe.

N.B. I do have a significant holding and I will continue to add as and when I can, at sub 300p.

Too much “business-as-usual” in Rishi Sunak’s remarks about the sub-postmasters this morning. He doesn’t get the scale of the national outrage. He should have announced Alan Johnson as head of new compensation agency, with all claims generously settled this year and bill sent to Post Office. Plus instructed government lawyers to resolve all miscarriages of justice this year too, with additional compensation. And encouraged NCA to pursue criminal charges against Post Office executives.

@PeteWatermanOBE the closing credits theme tune for #littletrainsandbignames, remind me what long list TV programme was that from? It’s now an ear worm I need to extract 🥴