[Media Feature: Bloomberg] Maritime Jones Act Fight Escalates With New Lobbying Push

I don’t know that I truly earned the title of “former ship broker” but it was an incredible way to learn how the business of shipping really works — especially if you’re lucky enough to have a mentor like Tom Roberts of Compass Maritime Services, LLC.

...

June 10, 2026 @Bloomberg article excerpts, featuring Cavalier Shipping insights. Written by @ZachReports in Washington, D.C.

“Both sides can be right,” said James Lightbourn, a former ship broker with experience managing hundreds of vessels who writes about maritime issues. He said the Jones Act waiver does undermine the long-term viability of domestic businesses while giving shippers cheaper options.

“This is the first time you’ve really seen sort of a chink in its armor,” he said of the law and the escalating battle for public support. “That, I think, has got a lot of folks sort of up in arms.”

America’s edge is innovation. Even in maritime, as history shows. For the first time in 70 years, America is positioned to lead a maritime revolution — this time with nuclear power. https://t.co/7rlS4mfnXB

Everyone Is Right About The Jones Act Waiver

And that’s the problem.

Whether you’re for or against the Jones Act, the waiver enacted during the past three months provided new data points to validate your prior belief. So far, it doesn’t seem as if we’re any closer to a widely-accepted stance on the Jones Act.

Did the Jones Act waiver lower gas prices? No.

Did the Jones Act waiver displace American jobs? No.

Did the Jones Act waiver demonstrate that the Jones Act constrains U.S. maritime trade? Yes.

Did the waiver allow a Chinese state-owned vessel to move what would have otherwise been a Jones Act cargo? Yes.

Where do we go from here?

If we’ve learned anything from the Jones Act waiver, it should be that working in worlds of absolutes, when it comes to the Jones Act, has very real trade-offs. Maritime trade within the U.S. is not at its full potential under the current legislation. However, a blanket waiver can result in vessels controlled by our economic adversaries moving what would have otherwise been protected cargoes.

The answer isn’t to end the waiver. The answer also isn’t to fully repeal the Jones Act.

A framework that prioritizes vessels based on their investment in the U.S. maritime sector — ownership, flag, crew, build — isn’t complicated to imagine.

America first. Allied nations second. State-owned vessels from economic adversaries: not at all.

https://t.co/lP9gIrN8Ac

@FrederikDu65139@OOOO39711442 Through their charters with DHT and Hunter, Mercuria were effectively short TD3C which went through the roof when the Strait of Hormuz got shut which prompted them to then sue the Baltic Exchange about the accuracy of the index.(https://t.co/XP0o1kBazs)

One VLCC, five charter contracts, and huge amounts of money changing hands.

The DHT Puma and its web of commercial contracts is a complex case study on how skyrocketing supertanker rates after U.S. and Israeli attacks on Iran (February 28, 2026) produced unprecedented winners and losers.

To follow the money, we need to untangle the web of commercial contracts that lead back to the 2016-built Very Large Crude Carrier (VLCC) at the center of this story: the DHT Puma.

https://t.co/Lqf9cQlsAU

Running a profitable ship finance business is becoming harder and harder.

The interest rate margins for shipowners borrowing money from banks, funds, and leasing houses have decreased by as much 1.5-2.0% in recent years. Great news for shipowners who are already enjoying a booming market stoked by geopolitical disruptions; not-so-great news for ship finance providers who are feeling the pinch in their profitability.

A quick primer (or refresher) on vessel financings:

(1) Vessel financings are typically quoted at an interest rate margin above the prevailing risk-free rate.

(2) Shipowners pay a total interest rate on the borrowed funds equal to the risk-free rate plus the quoted interest rate margin.

(3) Ship finance providers set and negotiate the margin so they can be suitably rewarded for the added risk of lending out their money, instead of investing it into other safer instruments such as U.S. Treasury bills.

A capital provider must be compensated with a higher return — in the case of ship finance providers, higher margins — for taking on increased risk.

One of the simplest ways to estimate risk is by looking at a transaction’s loan-to-value (LTV) ratio. LTV is the loan amount divided by the value of the collateral (in our case, a vessel) securing the loan. The more money one lends against the collateral/a vessel, the more money that vessel will need to make to pay off the loan. If the vessel doesn’t make enough earnings to repay the loan, it may be more challenging to sell the vessel to pay off the outstanding debt.

In recent years, as interest rate margins decreased, did the risk in ship finance transactions decrease as well? Let’s examine a bank’s net interest margin in relation to its portfolio to find out.

Continued on Freight + Fortune: https://t.co/JFmulIMFBs

USD fuels today’s shipping market; CNY aims to overtake it.

The international shipping market runs on U.S. dollars — even if none of the companies involved in a voyage are American — reminding us daily of the fact that the dollar remains the world’s reserve currency. China is actively working to change this reality.

Global container ship lessor Costamare signed a contract with CSSC (Hong Kong) Shipping Company Limited’s subsidiary Dalian Shipbuilding Industry Co for 16 newbuilding vessels (12 with 9,200 TEU capacity and 4 with 3,100 TEU capacity) to be delivered between the fourth quarter of 2027 and the second quarter of 2030. The order is worth USD 1.3 billion, or rather CNY 9 billion, because the payment will be in Chinese Renminbi — not U.S. dollars.

Costamare, an Athens-based and NYSE-listed company, is the second large Western container ship lessor to enter into a large CNY-denominated newbuilding vessel order with China's state-owned shipping complex CSSC. Seaspan, the world's largest container ship lessor, already procured a total of 18 containerships from CSSC across orders in 2024 and 2025 — all with payment in yuan.

Full post: https://t.co/eA4uGgy7d2

Join me at the @tradewindsnews Shipowners Forum USA 2026 on May 5 in Houston. At the day-long forum, participants will assess the energy shipping outlook and delve into the debates driving U.S. policy forward. The day begins at 10am and I’ll be on a panel at 4:15pm during the ship finance session.

Titled “Financing Energy Shipping in a High-Risk World”, my panel will touch on rising geopolitical tensions, lender and investor risk calculation factors, and how capital providers are navigating the current environment.

Joe Brady (TradeWinds) will moderate, and my fellow panelists are Omar Nokta (@Clarksons_CRSL), Evan Cohen (@firstcitizens), and David Herman (SSY).

Together we’ll discuss financing energy shipping and I look forward to talking about investing in nuclear power as the future “energy” of shipping.

Please reach out if you plan on attending TradeWinds Shipowners Forum USA 2026. I hope to see you in Houston on May 5!

Who’s cashing Uncle Sam’s Maritime Security Program (MSP) checks?

Of the 60 ships in the MSP fleet, 46 (77%) are operated by U.S. subsidiaries of four European shipping conglomerates and the remaining 14 (23%) are U.S.-owned.

U.S. shipping companies collect only $81.2 million of the $348 million paid annually by MSP.

Read on Freight + Fortune why this matters beyond the math: https://t.co/OJkPtR3Vn2

[In-Person Event] CMA Shipping Annual Meeting Lunch | April 23 at Noon

This year’s CMA Annual Meeting Lunch on April 23 in Darien, Connecticut features Keynote Speaker Josh Shapiro, President & CEO of Liberty Maritime, the New York-based commercial shipping company specializing in global logistics and providing transport services for military and commercial cargo.

Shapiro oversees Liberty Maritime Corporation’s business operation and executes the company’s strategic business activities. Prior to joining Liberty, he obtained his Master’s Degree in Shipping, Trade and Finance at the Cass Business School of City University in London and has worked with various commercial shipping brokerage firms in London in addition to his government experience as a Personal Aide and Legislative Policy Advisor to a Congressman.

Shapiro is an elected member of the American Bureau of Shipping (ABS) and an associate member of the Association of Shipbrokers and Agents (ASBA).

The CMA Annual Meeting Lunch opens at 12pm at The Water’s Edge at Giovanni’s and is free for all Connecticut Maritime Association (CMA) members in good standing.

RSVP to LParsons (at) MarineMoney (dot) com by April 21 to join us.

I hope to connect with you at the CMA Annual Meeting Lunch at noon on Thursday, April 23!

The Jones Act debate often centers on domestic versus foreign vessels, but that framing misses the true existential threat to oil-carrying tankers in the Jones Act fleet: oil pipelines carrying refined liquids over long distances, from the production site to the consumption site.

The Colonial Pipeline moves more than 100 million gallons of fuel per day between the U.S. Gulf coast and the Northeast. Moving fuel across the Colonial Pipeline’s full length—from Houston, TX to Linden, NJ (just outside of New York City)—costs 7.6 cents per gallon.

A Jones Act MR product tanker transporting fuel from Houston to New York harbor has recently been quoted as high as 14.5 cents per gallon, according to Overseas Shipholding Group CEO Sam Norton.

One of the Jones Act tankers’ largest markets is fuel delivery to Florida, a state with 23 million people but no refineries and no pipeline connectivity. Without any pipelines in place, the cheapest option to get fuel into Florida is transport by tanker.

The current 60-day Jones Act waiver expires in May. The prospect for pipeline expansion might be just getting started.

[Video] The Business of Shipping

Watch my discussion from the CMA Shipping conference on how to rationalize investments in shipping alongside industry expert panelists.

The panel was a hit at the conference and the organizers generously allowed me to share the video with my Freight + Fortune subscribers.

https://t.co/SASnD6BqEu

I hope you enjoy The Business of Shipping panel video and I hope to see you at CMA Shipping 2027 in Houston!

Shipping and stocks have an on-again, off-again relationship. Lately, it’s in the “off-again” status, with many shipping companies leaving stock exchanges. These shipping companies typically depart when large private investors (and often company insiders) bid to buy all the outstanding shares.

But this one-way tide pulling companies away from public markets suddenly reversed with not one, but two, shipping initial public offerings (IPOs) in Oslo in March 2026.

Which company—(1) a conventional shipping company or (2) a ship leasing company—do you think raised more money from investors?

https://t.co/b3Nfmml7DH

@JBlack151@cpgrabow The more interesting question might be what the relet market for Jones Act tonnage is today to have a more apples-to-apples comparison for spot voyages.

"American tankers cost about $50,000 a day more to hire than foreign vessels, said @JLightbourn...Using non-American ships could cut transportation costs by about 5 cents per gallon of oil, Mr. Lightbourn estimates."

@healy_trader Ah - yes, in that sense they are taking steps towards vertical integration. The plan to use ammonia as a vessel's fuel, well, that's another discussion...

Shipping companies are encouraged to remain simple, while being valued at a discount to the market value of their own vessels. But some nontraditional companies escape this paradoxical framework.

Navigator Gas (“Navigator”; NYSE: $NVGS) is a useful example of what a more robust and value-add shipping company can look like in practice.

Continued on Freight + Fortune: https://t.co/mJZHN8PFGl

@healy_trader It is an interesting comparison but I think there is some nuance in that $CMBT is horizontally integrated across different vessel types while $NVGS is vertically integrated along the liquefied gas supply chain.

It was only a matter of time before publicly-traded @ZimShipping became an acquisition target: enter @HapagLloydAG.

The acquisition has more consequential effects in geopolitics than in market consolidation.

More on this deal and considerations for the US via my Freight + Fortune substack.

https://t.co/71EnMYwkLZ

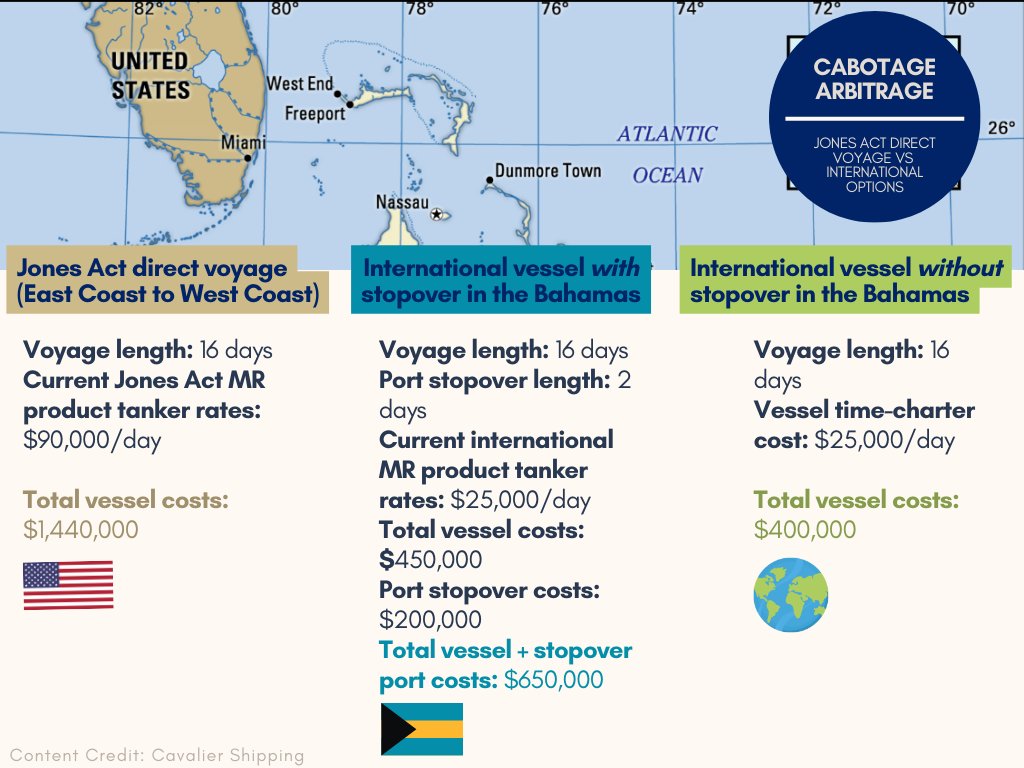

Cabotage Arbitrage: Circumventing the Jones Act |

How the economics of the Jones Act direct voyage—from U.S. port to U.S. port—and alternative routings compare. (Inspiration drawn from @Bloomberg article by @wkubz@lkassai)

https://t.co/l09dWwG3JH

![JLightbourn's tweet photo. [Media Feature: Bloomberg] Maritime Jones Act Fight Escalates With New Lobbying Push

I don’t know that I truly earned the title of “former ship broker” but it was an incredible way to learn how the business of shipping really works — especially if you’re lucky enough to have a mentor like Tom Roberts of Compass Maritime Services, LLC.

...

June 10, 2026 @Bloomberg article excerpts, featuring Cavalier Shipping insights. Written by @ZachReports in Washington, D.C.

“Both sides can be right,” said James Lightbourn, a former ship broker with experience managing hundreds of vessels who writes about maritime issues. He said the Jones Act waiver does undermine the long-term viability of domestic businesses while giving shippers cheaper options.

“This is the first time you’ve really seen sort of a chink in its armor,” he said of the law and the escalating battle for public support. “That, I think, has got a lot of folks sort of up in arms.”](https://pbs.twimg.com/media/HKyDYfAXoAA3X2J.jpg)

![JLightbourn's tweet photo. [In-Person Event] CMA Shipping Annual Meeting Lunch | April 23 at Noon

This year’s CMA Annual Meeting Lunch on April 23 in Darien, Connecticut features Keynote Speaker Josh Shapiro, President & CEO of Liberty Maritime, the New York-based commercial shipping company specializing in global logistics and providing transport services for military and commercial cargo.

Shapiro oversees Liberty Maritime Corporation’s business operation and executes the company’s strategic business activities. Prior to joining Liberty, he obtained his Master’s Degree in Shipping, Trade and Finance at the Cass Business School of City University in London and has worked with various commercial shipping brokerage firms in London in addition to his government experience as a Personal Aide and Legislative Policy Advisor to a Congressman.

Shapiro is an elected member of the American Bureau of Shipping (ABS) and an associate member of the Association of Shipbrokers and Agents (ASBA).

The CMA Annual Meeting Lunch opens at 12pm at The Water’s Edge at Giovanni’s and is free for all Connecticut Maritime Association (CMA) members in good standing.

RSVP to LParsons (at) MarineMoney (dot) com by April 21 to join us.

I hope to connect with you at the CMA Annual Meeting Lunch at noon on Thursday, April 23!](https://pbs.twimg.com/media/HF3i1SFasAEdyGC.jpg)