TAX MAN: Hey you! Your W-2 is ready. Pumped for tax season.

ME: Awesome, so I can file my taxes now?

TAX MAN: Nope, your wife’s W2 isn’t ready yet.

ME: Cool. I'll see if she knows her ADP login.

TAX MAN: Hey. Your 1098 is ready.

ME: Great, that’s my mortgage interest right?

TAX MAN: Yep. But your loan got sold last year haha. So you’ll get two 1098s, one from each bank.

ME: Yea I remember getting a letter about that at some point…that's like the 3rd time our mortgage has been sold.

TAX MAN: Btw only 1 of your 1098s is ready. The other isn't.

ME: Cool, so I still can't really file yet.

TAX MAN: Yep. But your brokerage account 1099s will come out in mid-Feb.

TAX MAN: Go look for a Consolidated 1099, or separate 1099-INT, 1099-DIV, 1099-B, 1099-R.

ME: I thought 1099s were for people who were contract-based employees or gig workers?

TAX MAN: Nah, 1099s are for so many things man.

TAX MAN: Did you sell RSUs last year? If so, you'll get a 1099-B that shows $0 basis, so you'll want to go get a Supplemental Information document from your broker.

ME: Cool, thanks for the heads up. Someone will tell me that explicitly, right?

TAX MAN: Not at all.

ME: Cool. What’s the difference between 1099-MISC and 1099-NEC?

TAX MAN: 1099-NEC (Non-Employee Compensation) reports payments to contractors. 1099-MISC (Miscellaneous) reports other types of payments like rent, royalties, and prizes, etc.

TAX MAN: They changed it a few years ago but didn't really tell anyone.

ME: Why are you the way you are?

TAX MAN: Nobody knows.

ME: Looks like I got a 1099-K this year?

TAX MAN: Did you sell something online?

ME: I sold a couch on Facebook Marketplace

TAX MAN: For how much?

ME: $600...

TAX MAN: Congratulations, you’re a business now.

ME: Okay I have all my 1099s, I’m ready to file.

TAX MAN: Did you check for corrected forms?

ME: What?

TAX MAN: Sometimes they prepare a corrected one to recharacterize income or fix mistakes.

TAX MAN: They come like a few weeks later.

ME: So should I wait?

TAX MAN: Up to you man.

TAX MAN: File now and maybe amend later?

TAX MAN: Or wait, and maybe it never comes.

ME: Cool.

ME: Oh btw, I invested in a private company last year.

TAX MAN: Ah, you’ll be getting a K-1 now LOL.

ME: Great, when?

TAX MAN: LOL.

ME: Taxes are due in a couple months...

TAX MAN: Right.

ME: But the form comes in October?

TAX MAN: Sometimes September if you’re lucky!

ME: So what do I do?

TAX MAN: File an extension and make a payment.

ME: I filed an extension, but I think we owe money.

TAX MAN: Yeah you'll need to pay that by 4/15.

ME: But I don’t know how much I owe?

ME: Because I don’t have all my forms...

TAX MAN: You estimate. 100% of last year's tax or 90% of this year's tax....or else you get slapped with thousands in underpayment penalties/interest.

ME: What if I make over $150,000?

TAX MAN: Then you have to pay in 110% of last year's tax....or 90% of this year's tax.

ME: What if I estimate wrong?

TAX MAN: Penalty.

ME: What if I overpay?

TAX MAN: They’ll refund it eventually.

ME: With interest?

TAX MAN: LOL no.

ME: I did everything right.

ME: I have all my forms

ME: I filed on time

ME: I’m getting a refund

TAX MAN: Congratulations

ME: When will I get it?

TAX MAN: The IRS says 21 days

TAX MAN: It’s been 12 weeks

TAX MAN: Your return is “still being processed”.

ME: Can I call someone?

TAX MAN: You can try.

TAX MAN: They’re experiencing higher than normal call volume.

ME: For how long?

TAX MAN: Since 2019.

ME: What if I just don’t file?

TAX MAN: Prison.

ME: What if I file wrong?

TAX MAN: Also prison, but less likely.

ME: What if my accountant files wrong?

TAX MAN: Still your fault.

ME: Can I just move somewhere with no income tax?

TAX MAN: You can try!

ME: What if I leave the country?

TAX MAN: You still have to file.

TAX MAN: For ten years after you renounce citizenship.

ME: This is tyranny.

TAX MAN: That's funny because that's actually how this whole thing started.

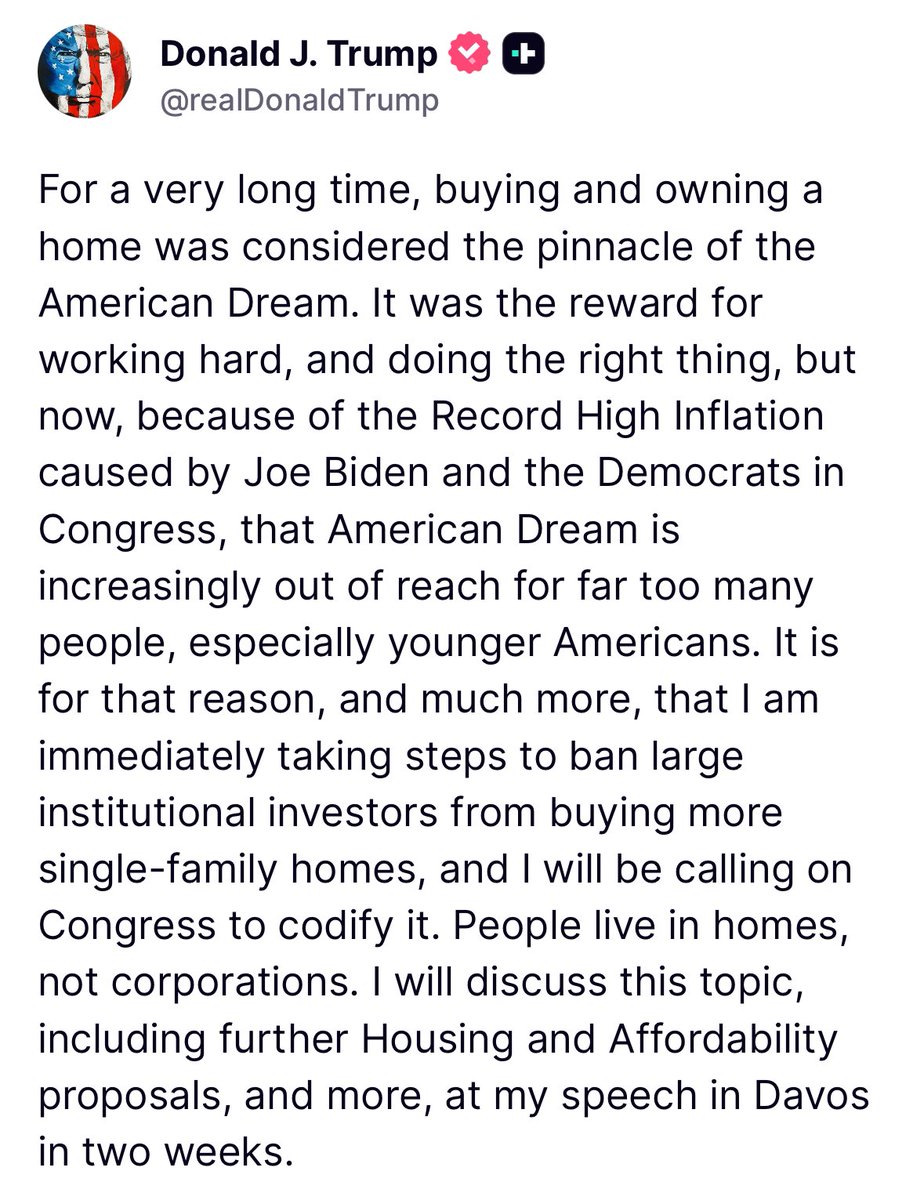

🚨 HOLY SMOKES.

Trump taking immediate steps to ban institutional investors from owning single-family homes.

“People live in homes, not corporations.” 🔥

@Marioxjumper@StockMarketNerd I agree but they’re only paying a little over $100M a quarter as of now while buying back $1.5B in shares a quarter. Doesn’t really matter too much and could get a larger amount of etfs to invest.

LEVEL 3 REACHED! That's all prizes unlocked!

✅ MSI RTX 5060

✅ MSI RTX 5070

✅ MSI RTX 5080

Each with a copy of Borderlands 4 for PC! RT & comment with Borderlands4xDLSS4 to enter. Win more prizes in the Borderlands 4 DLSS 4 Challenge on 17th Sep!

@SteamDB@acce@PayPal Can you please address this? Obviously these games deserve to be removed but this can create a dangerous precedent for control by card processors. @Kross_Roads

@bryan_johnson If you’re constantly on a caloric constriction wouldn’t you just continue to lose weight? I think at this point 2,250 is your maintenance weight and not a caloric constriction.

@DataDInvesting@ssamsmit I’m in the exact same position as you. Only problem for me now is that I no longer have a chase “college” account so they charge me a fee if I don’t keep $1,500 in it which isn’t bad but it’s still annoying.

@realmostafah How can you call it fraud when multiple big tech companies are openly stating they are purchasing billions of dollars' worth of NVIDIA hardware? I would agree with you if NVIDIA itself were saying this but the statements are coming from many other companies

Yesterday, the House released a 389-page tax bill that includes trillions in tax cuts.

I read every single page so you don’t have to.

Here’s everything you need to know:

🧵

Yesterday, $RKLB released its Q1 2025 results.

It's one of my largest positions, with an average cost of $4.82/share.

In this thread, I’ll break down everything you need to know about the Earnings Report: 👇🏻🧵

I'm not avoiding your thesis. I'm saying your thesis is myopic.

Your thesis, as I understand it, is this: MAUs and AUC are the gold standard for measuring a one-stop shop.

This thesis is based by your lived experience. Your entire life revolves around public markets. You watch CNBC every day. You listen to earnings calls, watch candles, have meetups with investors, talk to investors, interview investors. That has changed your worldview and leads to certain bias. As a result, your view of a one-stop shop is one that aggregates Assets Under Custody and leads people to actively trade those assets. That's objectively false when you look at the data as a whole.

Let's tackle those individually. FIrst, the MAUs. Let's just look at raw numbers. 58% of US households own stocks directly or indirectly. About 20% of them own single stocks. Of that subset, well under 10% actively trade. So if you are using monthly active users as your measure of whether you qualify as a one-stop shop, then you are actually missing over 90% of the TAM. I'm willing to bet that less than 2% of the US population have ever listened to a full earnings call from any company in their entire life.

The vast majority of millionaires in the United States do not actively trade stocks. My parents have done extremely well in life, they've been lifelong Schwab customers, I'm sure Schwab has made a ton of money off of them. They check their balance once a month via a financial aggregator tool when they do their finances and leave it alone. They probably log in to their Schwab account once or twice a year. They are not MAUs, but they are extremely valuable customers. They are the norm, not the exception. You are the exception. The vast majority of people are passive investors, not active investors. The overall TAM of passive investors is larger than the TAM of active investors even after taking into account the higher ARPU from active investors.

Monthly actives are a terrible proxy for a one-stop shop because it does not measure the 90% of people who will never be a monthly active user of any platform. $SOFI is seeking to build a one-stop shop for 100% of people who want to have a bank, which includes that 90%, whether they get their AUC right now or not. $HOOD is seeking to aggregate every last one of the less than 10% of active traders. MAUs are not a good proxy for a one-stop shop for most people

Now, on to AUC:

This builds on the discussion above, but your argument that AUC is the best proxy for a one-stop shop is pretty easily disproven by a simple comparison. What is the best one-stop financial shop for Americans. There is only one true answer, and it's $JPM.

Here is a comparison of AUC for large firms from Grok:

Charles Schwab: $10.33 trillion in client assets (AUM) as of January 31, 2025.

Vanguard: $10.1 trillion in AUM as of December 31, 2024.

Fidelity Investments: $15.1 trillion in Assets Under Administration (AUA) and $5.8 trillion in AUM as of 2024.

JPMorgan Chase: $4.05 trillion in client assets as of 2024.

$JPM has less AUM than $SCHW, Vanguard, or $FNF. Yet JPM is, in every respect, obviously a better financial one-stop shop. Here are the market caps of those companies.

$SCHW: $148B

$FNF: $17B

$JPM: $686B

(Vanguard is private)

AUC is not the best measure of a one-stop shop, or Fidelity, a company most people are unaware of, would be the best one-stop shop in the US. They are not. Aggregating more AUC does not make you a one-stop shop and it is not a measure of what makes a financial institution valuable as $JPM is 40x more valuable than $FNF despite having less AUM.

A couple other points:

1) You actually don't know what $SOFI's AUC is or how much it has grown. Neither do I. The "deposits" you are referring to exclude any AUC growth. Additionally, they include CDs that SoFi is intentionally letting expire that are offered through Vanguard.

2) "Net deposits into the platform are all that matter to drive the lifeline of a financial technology company." Nope, you are trying to distil an incredibly complex topic, namely what makes a financial institution a one-stop shop into a single number, assets under custody. That is A way to measure it, it is not THE way to measure it. If it were just about AUC, then that's all any fintech would target, yet the majority don't even track it. That should make you question whether it's the most important metric to track. It isn't. Complex issues take more than just one metric to understand properly.

3) "Sofi cant disclose them because their engagement is garbage and if it wasnt they would put it out there like a regular tech company would."

I know you don't follow the company closely, so you wouldn't have heard this, but they've been asked this on multiple conferences or firesides. They don't disclose them because they are not correlated with the company's revenues, profits, or performance. It isn't because engagement is garbage, it's because engagement is a poor measure of success. Your worldview about MAUs in financial institutions is biased.

4) "The other reason AUC is valid is because people bringing over their assets to HOOD could bring it to SOFI!"

This is true, but it's focusing on a KPI that is only important to HOOD right now. SoFi's focus and priorities are elsewhere. Their plan is to get the user and let the AUC come organically. HOOD's focus is aggregating deposits right now and is paying handsomely for them. You are also looking at this as a zero sum game, which it's not. There are probably something like $60T-$80T in assets to bring over. The $18B that HOOD got this quarter is around 0.02% of the assets available. SoFi isn't worried about losing 0.02% market share to HOOD right now because they are implementing strategy that they think will lead to long-term aggregation of assets of much greater amounts if they focus on aggregating individuals with the potential to be of high net worth in the future rather than paying for those dollars right now.

@amitisinvesting@eje1219@DataDInvesting Idk how $HOOD classifies this but for banks (SoFi) deposits sit as a liability on the balance sheet. I think your very confused about all this 😂😂

If I'm $SOFI and I want to tell $HOOD to get off my turf, here is what I do:

Crypto was 53% of HOOD's transaction revenue in Q4.

It was 0% of SoFi's revenue for two years since the OCC made them divest.

If I were creating a strategic plan, these are the three things I'd advocate for:

1) Undercut HOOD on fees.

HOOD is the cheapest place to buy and sell crypto for retail, but their margin is SoFi's opportunity. Offer crypto at lower fees than HOOD. SoFi doesn't need massive crypto profits right now, this is a new product for them and they have nothing to lose by making it only marginally profitable. HOOD's take rate has been increasing, undercutting them would be a shot across the bow.

2) Offer a 1% match for anybody transferring crypto to get people to to switch and build AUM fast. This works especially well because you connect it with #3...

3) Crypto-backed lending. This one is the kicker, and the one that SoFi is UNIQUELY positioned to do. One of the ways that rich people leverage their wealth is by never realizing gains and never paying taxes. Instead they borrow against their assets. Do this in a responsible way with low risk, but do it now and make it your BIGGEST differentiating factor.

SoFi is uniquely positioned, as a fully chartered bank, to offer loans using crypto as collateral, giving crypto holders the same benefit as those with large stock portfolios. Roll this out with the crypto launch and market this like along with the 1% transfer match.

If you are making money on the loans, then it makes it even easier to not have to worry too much about the fee revenue.

If HOOD wants to come after banking, SoFi can respond by going after their crypto.