When the Federal Reserve creates new money, it does not helicopter it evenly onto every lawn in America. That fantasy lives only in economics textbooks, where money is a neutral veil and printing $1 raises all prices by the same tiny fraction at the same convenient moment. Reality works differently. Money enters at specific points, in specific hands, at specific times. And whoever touches it first wins.

Richard Cantillon figured this out in the 1730s, watching how mining wealth and paper credit rippled through the French economy. The new money spreads unevenly, and the order matters enormously.

Picture the mechanism. The Fed buys Treasuries and mortgage-backed securities from primary dealers: JPMorgan, Goldman Sachs, Citigroup. Those institutions get the fresh dollars first, while prices across the economy still reflect yesterday's smaller money supply. They lend, they buy assets, they pay bonuses, all at old prices. The money then trickles outward to hedge funds, to corporations issuing cheap bonds, to the government contractor, and eventually, months or years later, to the nurse in Ohio and the retiree living on fixed savings. By the time it reaches them, rents have jumped, groceries cost more, the S&P 500 sits at a record. They receive diluted dollars and pay inflated prices. They bought nothing and lost anyway.

Every expansion of the money supply transfers real purchasing power from the periphery to the center, from wage earners to asset holders, from savers to the leveraged. From 2020 to 2022 the Fed grew its balance sheet from roughly $4 trillion to nearly $9 trillion, and asset prices detonated while the median family watched its grocery bill climb 20 percent. Then they blamed "greedy corporations" and supply chains, as if the printing had nothing to do with it.

You were told inflation is a rising tide that lifts all boats. Look again at who owns the yachts and who is bailing water.

Can you heat a fire hall with a Bitcoin miner? (part 1)

I tested it in a real volunteer firehall:

- 1 miner

- A vintage 1950s fire truck

- A thermal camera

- A tripped breaker

- A storm outage

The result: yes, a miner made a difference in a 5000 cu ft room. ~30,000 cu ft next!

🚨 Billionaire investor Ron Baron explains the silent math destroying your wealth.

Your money loses 4 to 5% of its purchasing power every single year. The economy grinds higher at roughly 2%. That is a relentless 7% headwind against you, annually.

What that really means. Prices double every 10 to 12 years. Your savings are cut in half in real terms within about 15 years. Cash sitting idle is not safe, it is decaying.

The system is structurally engineered to punish savers and force capital into risk just to survive.

It seems to me that most people are hooked on news items that last about a day or two and are then forgotten about, as other news items replace them, while failing to see how things are evolving and why. That’s not good for anyone.

There are big cycles unfolding almost exactly how they have repeatedly unfolded in the past, and they are being missed. If you’re interested in seeing these big cycles presented in an entertaining way, I am offering an overview of them here in my 5-minute animated video, Principles for Dealing with The Changing World Order. And if you'd like to see a more complete picture, you can watch the full 45-minute version here: https://t.co/1NjhMYQyaS

MILTON FRIEDMAN:

"CONSUMERS DON’T PRODUCE INFLATION."

"PRODUCERS DON’T PRODUCE INFLATION.

"INFLATION IS PRODUCED ONLY BY TOO MUCH GOVERNMENT SPENDING AND TOO MUCH GOVERNMENT CREATION OF MONEY, AND NOTHING ELSE."

JUST IN: Shareholder vote on Adam Back’s #Bitcoin Standard Treasury $BSTR merger with Cantor Equity Partners I has been postponed to July 2.

They could potentially buy over 23,000 BTC once the merger is completed. 🔥

We’ve only dropped below purple range once before and it was in 2022 after FTX took the entire crypto market down.

Bitcoin returned 700% over the next three years.

Social Security is already adding to federal deficits and debt today. Absent reform, the Social Security program is projected to add $5.1 trillion to federal debt by 2032, warn Cato’s @RominaBoccia and Ivane Nachkebia.

https://t.co/gnqF1puYRV

I don't even pay attention to politics anymore. I just find it so wasteful & dysfunctional & stupid. Save it. I don't want to hear it. The only thing that I care about is sound money. Bitcoin is the soundest form of money we’ve ever had.

@LawrenceLepard

Before the sun sets take 7-1/2 minutes and watch this video of @DrJackKruse and then research the Landauer principle. If what’s he’s saying is relevant (and I believe it is) we now understand the Core attack vector on the baselayer of Bitcoin and that it is indeed existential.

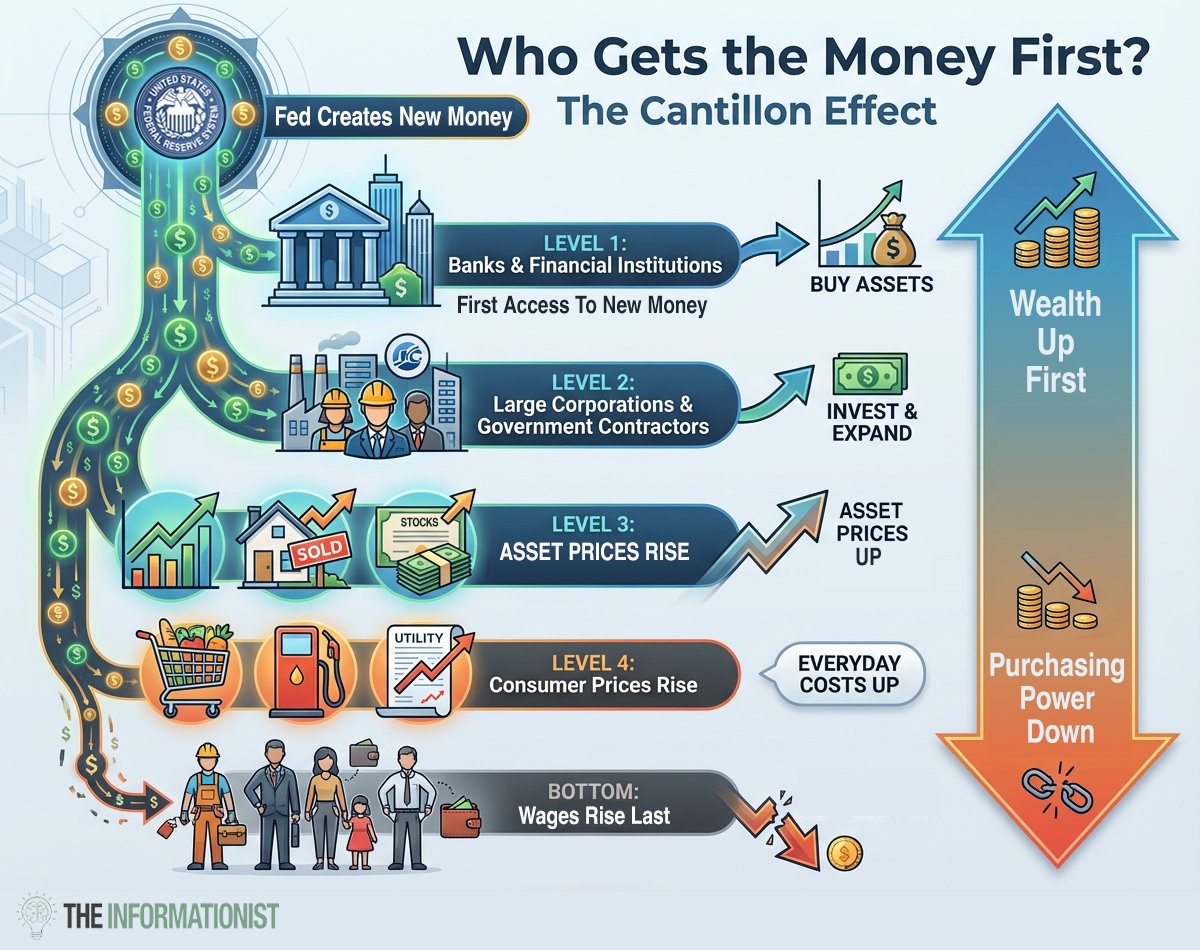

Most people have never heard of the Cantillon Effect.

But once you understand it, you’ll see the world of investing differently.

What is it?

In the early 1700s, Richard Cantillon noticed a simple pattern:

When new money enters an economy, it doesn’t reach everyone at once.

And whoever gets it first benefits the most.

Here’s how it works today:

New liquidity enters through the Fed and through bank lending.

Both follow a similar pattern:

→ Markets and large balance sheets get first access

→ Large corporations and well-connected borrowers tap cheap credit next, they invest and expand at today’s prices

→ Asset prices tend to rise as new liquidity chases finite assets

→ Consumer prices often follow

→ Wages rise last, usually after purchasing power has already declined

Fed data shows how lopsided the playing field is:

- The top 10% hold nearly 90% of equities.

- The bottom 50% holds about 1%.

It’s a simple but powerful monetary transmission.

Understanding this won’t change the system.

But it might change how you think about where to store your savings.

For those of you who don't know, I write all about topics like this every week in The Informationist. Last week, we dove deep on this one.

Link in bio if you want to read the full explanation.