For those unaware, SpaceX has already shifted focus to building a self-growing city on the Moon, as we can potentially achieve that in less than 10 years, whereas Mars would take 20+ years.

The mission of SpaceX remains the same: extend consciousness and life as we know it to the stars.

It is only possible to travel to Mars when the planets align every 26 months (six month trip time), whereas we can launch to the Moon every 10 days (2 day trip time). This means we can iterate much faster to complete a Moon city than a Mars city.

That said, SpaceX will also strive to build a Mars city and begin doing so in about 5 to 7 years, but the overriding priority is securing the future of civilization and the Moon is faster.

$IREN ? Zero. Zero. Zero. Every peer has delay stories.

Quietly, without fanfare or excuses, $IREN has built the most flawless execution track record in the entire data center / mining / AI infrastructure space.

Watch this receipts thread:

2020–2021: Canal Flats (30MW) → promised energization → delivered exactly on time.

2021–2022: Mackenzie expansions → every single phase energized on or ahead of schedule.

2022–2023: Prince George (50MW) → guided date → hit it to the exact month.

Then they went to Texas and turned Childress into a monster.

2023–2025: Childress 750MW ultimate site

→ Phase after phase, substation after substation, transformers arriving early, 600MW+ energized in ~18 months flat. Management kept saying “on track”… and then quietly over-delivered every single time.

Hashrate ramp (the ultimate proof of execution):

Guided 10 EH/s → hit early → immediately raised to 30 EH/s → smashed early → raised again → 50 EH/s fully installed & operating right on the upgraded 2025 timeline. Not one miss, not one “supply chain issue” excuse.

AI pivot in 2024–2025:

Announced liquid-cooled Horizon 1 (50MW HPC, Childress) mid-2025 → foundations poured, long-lead items secured, second bulk substation transformer energized early specifically for it → November 6 earnings call: “Horizon 1 on schedule for Q4 2025 delivery.” Still zero slippage three weeks later.

Sweetwater 1.4GW (West Texas): originally targeting Oct 2026 → management straight-up accelerated it to April 2026 because… well, that’s just what they do.

Horizon 2 (another 50MW liquid-cooled) already breaking ground behind it.

Every peer has at least one public delay story since 2022.

$IREN has zero. Zero.

This isn’t normal. This is under-promise, over-deliver on steroids. They guide conservatively, then execute so precisely it looks easy.

In a sector drowning in excuses, $IREN just silently ships.

That’s why the believers keep getting louder. 🔥

Some people still think they can “protect” Bitcoin by blocking protocols or restricting what they don’t understand.

But Bitcoin was never designed to be a static system. It’s not just digital goldit’s a distributed, programmable database capable of supporting full layers of infrastructure.

From Atomicals, we see it clearly:

if an idea can be executed within the UTXO model, then it belongs on Bitcoin.

Innovation doesn’t stop because a node adopts restrictive policies.

Innovation happens when we build.

And what’s coming will completely change how we interact with Bitcoin.

It has a name: @bitmetabtc

In this ecosystem, progress doesn’t ask for permission.

It simply gets deployed.

@bitcoincoreorg@BitcoinKnots

$IREN In-depth review of Q3 Earnings Call, MSFT Deal, Profitability

First I want to acknowledge where my previous posts were wrong:

1. I stated 4.3m capex for IREN's liquid cooled DC which was way off (3). Written in Sept, I had used total load so if I used IT load it still would have been 6-7m. The estimation was based on this Data Center Dynamics Article which had stated Childress buildout was 300-350m (1) which had likely taken the figure IREN's prev for non T-3 datacenters. The actual is 14-16m. 9-11m of it is the data center itself. It's reasonable the extra 3-4m was for a T3 datacenter as the previous 6-7m figure did not state T3 datacenter. Furthermore, training clusters cost more than inference clusters which is a 3m charge. I now think both clusters are training and each training cluster is 100MW so there are two training clusters with each Horizon making up one training cluster.

2. I had wrongly mentioned that no ATM dilution is needed on my first take of the slides. I had over looked the part from the earnings where focus is on maintaining a "prudent balance of debt and equity" (4).

@FransBakker9812 had found in footnote to confirm that dilution via ATM not convertibles are coming (2). This is warranted because we don't want to be like $CRWV who is issuing overloaded debt which makes their dilution look good but their balance sheet is saddle which makes it harder for them to issue debt in the future. IREN will want a healthy balance sheet to be ready for SW1.

3. I always that IREN could do IaaS at a high level which the MSFT contract did validate that IREN can serve hyperscales but I did not anticipate that the rate would be much lower than Nebius. This is the main reason we are not seeing $IREN stock hit $90+.

4. Finally I did participate in some degen speculation on Wednesday night from a bridge 84 picture posting and took it as a hint for a possible Meta deal. That did not materialize.

Now that we have more data, I will finish this post with more accurate net earnings project and share price for Canada + Childress + SW1 than last projection.

Earnings Call Notes

IREN uses IRR to compare IaaS deals to colocation. They subtract off a $130k/kW-month colocation.

Colocation Net Profit

This is equivalent to 1.56m/MW-yr. IREN has stated that the DC itself is 14m-16m/MW and can be used for 20 years. If we take 15m/MW and divide by 20 we get that the cost for the colo is .75m/MW-yr.

First we calculate (Revenue - Depreciation) which is 1.56m/MW-yr - .75m/MW-yr so that's .81m/MW-yr. If we used 85% project margins, then we get a Net Profit of 688.5m/MW from colocation or 137.7m for 200MW. Note, we don't know what composition of margin is colo and which margin is IaaS we just know the entire project averages out to 85% margins.

Note that the 85 margins includes power, repairs, maintenance but not SGA, financing (5). SGA was high this earnings report due to key employees getting paid in RSUs which did a 10x. Their refresher RSU contracts will be based upon market price. I acknowledge that SGA may be higher in a hot industry but I assert it won't anywhere near 10x higher RSUs.

IaaS IRR

IRR (internal rate of return) and not ARR is the best metric for Neoclouds. IRR is used in real estate where the value of the property is very high compared to the yearly cashflows. This makes absolutely sense because value of GPU depreciation is very high and the elephant in the room. I do like that IREN is very transparent and uses IRR to contextualize their ARR. Every Neocloud should do this.

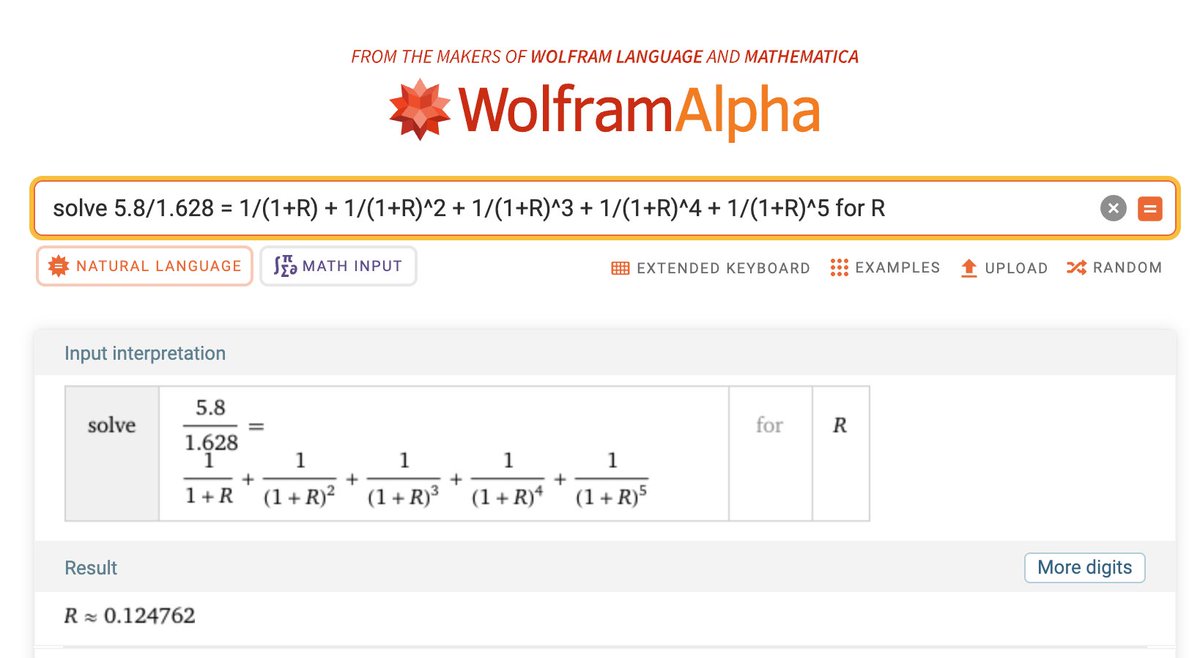

Thanks to @GlobalCollapse for original IRR calculations. I have calculated IREN's unleveled IRR to be 12.47% using Wolfram Alpha as shown in picture 1 (calculations available in source 6 for modification). Wolfram Alpha was ChatGPT for math before LLMs were cool and is classical algorithm based so it doesn't hallucinate and is has calculator precision. I check with @MarkosAAIG and this is inline with DC projects.

In real estate, leveraged is often used in the form of debt. Note that debt is secured by the asset which in real estate has stable value so this is not degen margin - every single DC project is levered whether it's GCP, Meta, Microsoft, NBIS, CRWV, or IREN. I have calculated IREN's leveraged rate of return to be 25.76% subtracting off the prepayment and then using a 7% interest rate shown in picture 2 (calculations available in source 7 for modification). I don't have the exact interest rate they are getting from Dell, but the earnings call explicitly stated with 2.5B of leverage, they are getting 25-30% IRR on 2.5B of leverage and if they use 3B of leverage then IRR is 35%-40%.

The above IRR assumes 0 residual value on GB300s after 5 years. With 20% residual value, Unleavered IRR becomes high teens and with 3B leverage IRR becomes 50%.

IaaS Net Profit

I will subtract off deprecation of GPUs and then multiply by 85% project EBDITA margins to get EBITA since we already subtract off depreciation of GPUs. Then I will subtract of interest to get EBTA. There's no significant amortization from a cost of a software team so EBTA = EBT. So I will get EBT which is just missing taxes a proxy for Net Profit. Note IREN has tax abatements on everything except the land which they bought for cheap.

We have 9.7B - 1.56B colocation = 8.14B IaaS revenue. 5.8B - 1.94B prepayment = 3.86B which over 5 years at 7% is 3.86 * 0.7 + 4/5 * 3.86 * 0.7 -> etc. Note that 4/5 is the remaining principal on year 4, etc. This gives us 810.6m of interest payment.

(8.14B IaaS Revenue - 5.8B GPU+Networking) * .85 = 1.989 - .8106 = 1.1784B over 5 years which comes out to 235m for 200MW IT per year.

Topline/GPU Comparison to NBIS, Nscale

Now that earnings call clarify 76k GPUs, we can compare topline per GB300 which is the most accurate. Let's do per 100k GPU for round numbers.

NBIS = 17.4B per 100k GB300

IREN = 9.7B * 100/76 = 12.76B per 100k GB300

Nscale = 14B * 100/104 = 13.46B per 100k GB300 (10)

Thus IREN is earning 73% of NBIS's topline/GPU which I attribute to uptime or credibility of uptime (9). Note that this is Nscale's second deal with MSFT where they were previously getting 6.2B for unknown amount of GPUs (10).

Notes from Earnings Calls

1. Dell has financed IREN for GPUs. Payment is due 30 days after shipping -> I'm assuming it will cover a portion with prepayment and cash from IREN covering the rest.

2. Other miners are giving up equity for colocation deals, while IREN gives up zero equity and gets huge a pre-payment worth 1/3 of the entire GPU+Networking+Cables cost.

3. Microsoft started shifting to negotiating for IaaS instead of Colocation 6 weeks prior to earnings.

4. Other HS more interested in colo SW but open for combination of both.

5. Other HS have interest in Horizon 5-10.

6. Contract obligations cannot be revealed.

7. Horizon 1-4 is 76k GPUs total.

8. Superclusters makes 2m extra charge for training only, not required for inference.

9. For Canada, 11k contracted from news released, 1k more contracted for 12k total contracted. Non-contracted ones are because of delivery timeline from Nvidia is far out.

10. Both AI native + enterprise customers in BC.

11. Hyperscalers and AI natives only want bare metal GPUs and want to bring their own orchestration layer.

12. Only smaller, less sophisticated customers want orchestration layer.

13. IREN is only focused on bare metal offerings because that’s the best way to scale their offerings to utilize their power assets.

Net Profits for Canada + Childress + SW1

Assumptions: Canada IaaS + H1-4 at 73% of NBIS Topline + H5-10 at % of NBIS Topline + 1.4GW SW Colocation

Canada IaaS Net Profits

Capex for Prince George is as follows for 500m ARR then we will subtract by capex and multiply by .85% margins. 7.1k NVIDIA B300s, 4.2k NVIDIA B200s and 1.1k AMD MI350Xs for approximately $674m (11). 1.2k B300 and 1.2k GB300 for $168m (12). 4.2k B200s for 193m (13). 1.2k B200, 1.2k for 130m (14). Total is 1.165B, over 5 years lifespan that's 233m depreciation. (500m - 233m) * .85 = 226.95m. Canada has two other sites projected for 1.5B net profit so we total net profits for all Canada 3 sites is 680.85m.

Childress

H1-4: 235m + 137.7m = 372.7m

H5-10

Note IREN got 73% of NBIS's Topline/GPU for H1-4. Let's assume that IREN gets 86% of NBIS's Topline/GPU for H5-10. This is very important because the 13% is pure profit if we assume same rate of cost of GPUs and DC. Then H5-8 would be 200MW for 11.42B instead of 9.7B for H1-4. H1-4 has 372.7m profit while for H5-8 an additional 11.42B - 9.7B = 1.72B would go bottom line so net profit for 5-8 would be 2.0927B. Now that's for H5-8, we can multiply by 1.5 to include H9-10 so H5-10 = 3.139B.

Childress: 3.5117B

Sweetwater

For colocation of 1.56m/MW-yr, we get a Net Profit of 688.5m/MW-yr. However, CIFR got 1.83m/MW-yr from MSFT while IREN is conservatively giving internal colocation numbers. If we take a 1.83m/MW-yr and apply the delta as profit then we get an additional 270m/MW-yr of profits for a total of 958.5m/MW-yr. For 1.4GW that's 1.3419B for Colocation. Now I know why Dan says colocation deals are bad.

Canada + Childress + SW1 Share Price

Adding all 3 sites, total net profit is 5.53B. Take whatever P/E you want but I'll use conservative 20 P/E. Note the 5.53B doesn't include the 2-3GW confirmed pipeline. That's 110.6B market cap. We have 281m diluted shares today. Assuming more 40% more dilution for finishing SW1 and H5-10 that gets us to 393.4m diluted shares or a share price of $281 by 2027.

This is Atomicals x BitMeta in a nutshell.

And not a single penny from outside sources.

Self funded together with blood, sweat and tears from a small community of loyalists.

First take notes on $IREN Q3 Earnings (Thread)

- 140k GPU expansion by end of 2026, conservative figure as includes Horizion 1-4 MSFT contract and 63k GPUs in Canada. H5-10 and SW not included. Clues of 50MW extra at PG and Childress 50MW expansion.

🚨BREAKING🚨

$IREN CEO Dan Roberts answering the $NBIS CTO and the FinX community regarding the software question:

🔴“1. You know, these are all highly advanced Al and software companies like $MSFT.

🔴2. They have significant experience in the space and they want the raw compute and the performance benefits that that brings.

🔴3. Having access to a bare metal offering and then being able to layer their own orchestration platform over the top of that. So that has been, you know, by design that we have been offering a bare metal service. It lends itself. Exactly to what our customers are looking for.

🔴4. Having said all of that, you know, we obviously are continuing to monitor the space, continuing to look at what customers want. And we're certainly able to to go up the stack and layer. In additional software if it is required by customers over time. But today, you know, as I said, we haven't really seen any material levels of demand for anything other than the bare metal service that we're currently offering.“

🟢Bottom line: $IREN was built to serve giants of the AI who have their own softwares.