Dad, husband & investor. Passionate about running, photography, fine food & wine. Giving back. Living life to the fullest. Mainly own $UPST $LMND $HIMS $IREN

$IREN Edge:

Larger power portfolio

NVIDIA DSX flagship and

Lower starting valuation today #IYKYK

More asymmetric long-term optionality if execution catches up.

can deliver multi-baggers in a continued AI tailwind scenario

2026 will be decisive

This space rewards execution speed over promises.

Zero promises, Zero delays !

@Agrippa_Inv $IREN 2026 is the prove-it year: Microsoft handoff + uncontracted fill + financing clarity are the real catalysts. Misses here keep the bear case alive; clean hits unlock the base/bull.

$LMND – #earnings out of doghouse

Boring stock that underpromises & overdelivers again

🚀 10th straight quarter of accelerating growth

🔥 Revenue +71%, Gross Profit +159%, IFP $1.33B (+32%)

🐶 Pet exploding: $500M+ run-rate, now #4 US carrier

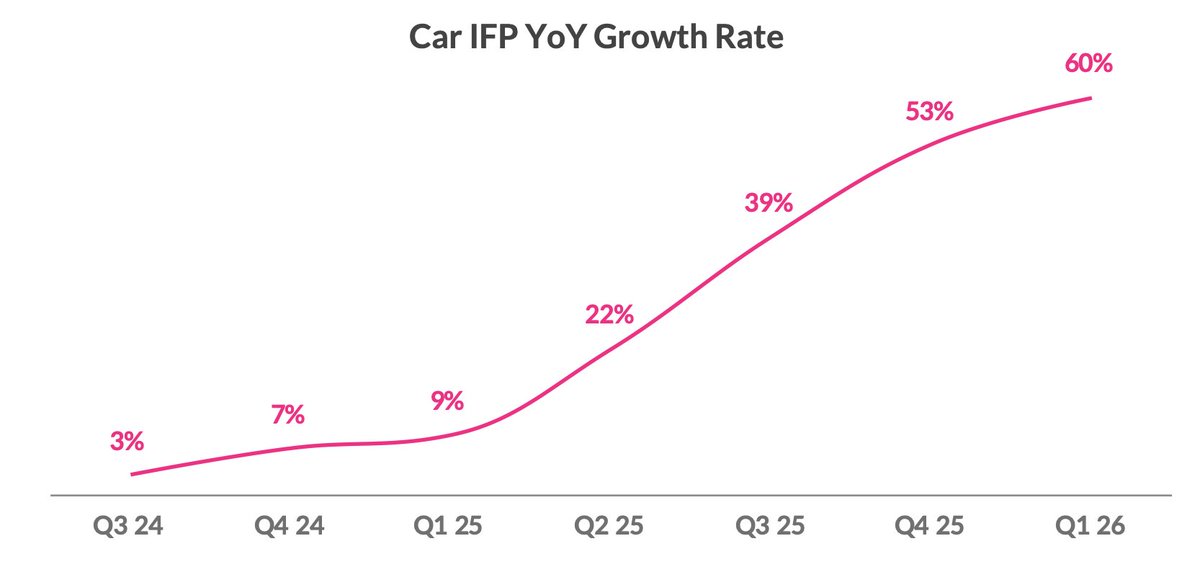

🚗 Car accelerating: 60% YoY, loss ratio down 14pts

💰 Adj. FCF +$17M, raising guidance, path to Q4 EBITDA positive

Bears worry:

• Still unprofitable overall

• High valuation on growth bets

• Execution risk if AI edge fades

Lemonade’s Q1 results are 🔥. So much to share, where do I start?

First, get into the AI mood, click this, + volume ⏫

https://t.co/IDPCvrTHge (by @kidfrancescoli)

🚀10th consecutive quarter of accelerating IFP growth

🔥 Topline at $1.33 Billion (IFP +32%)

🔥 Revenue grew 71% to $258M

🔥 Gross Profit increased 159% to $100M

🔥 3.14M Customers

🔥 Adj. Free Cash Flow $17M

Lemonade Pet exploding!

✅ Surpassed $500M top line early in Q2

✅ #1 most searched pet insurance brand in the U.S.

✅ @lemonade_inc is now the 4th largest pet carrier in the U.S.

✅ AI-powered automation drives record claim handling efficiency (LAE: ~4%)

✅ Our data + tech edge lets us lower prices while boosting profitability

Car picking up speed

✅ Now at 60% YoY growth, $214M IFP

✅ Loss ratio improved to 74% (14 pts better YoY)

✅ Autonomous Car for @Tesla FSD conversion rate 70% higher than standard

And more...

↗️ Raising 2026 top & bottom line guidance

↗️ IFP per employee > $1M (3x improvement in 4 years)

↗️ Positive Adj. EBITDA in Q4

↗️ Investor Day in NYC November 17

$IREN = Zero. Zero. Zero.

Every peer has delay stories.

Quietly, without excuses, @IREN_Ltd has built the most flawless execution track record in the entire data center / #AI infra space.

Watch this receipts thread:

2020–2021: Canal Flats (30MW) → promised energization → delivered exactly on time.

2021–2022: Mackenzie expansions → every single phase energized on or ahead of schedule.

2022–2023: Prince George (50MW) → guided date → hit it to the exact month.

Then they went to Texas and turned Childress into a monster.

2023–2025: Childress 750MW ultimate site

→ Phase after phase, substation after substation, transformers arriving early, 600MW+ energized in ~18 months flat. Management kept saying “on track”… and then quietly over-delivered every single time.

Hashrate ramp (the ultimate proof of execution):

Guided 10 EH/s → hit early → immediately raised to 30 EH/s → smashed early → raised again → 50 EH/s fully installed & operating right on the upgraded 2025 timeline. Not one miss, not one “supply chain issue” excuse.

AI pivot in 2024–2025:

Announced liquid-cooled Horizon 1 (50MW HPC, Childress) mid-2025 → foundations poured, long-lead items secured, second bulk substation transformer energized early specifically for it → November 6 earnings call: “Horizon 1 on schedule for Q4 2025 delivery.” Still zero slippage three weeks later.

Sweetwater 1.4GW (West Texas): originally targeting Oct 2026 → management straight-up accelerated it to April 2026 because… well, that’s just what they do.

Horizon 2 (another 50MW liquid-cooled) already breaking ground behind it.

Every peer has at least one public delay story since 2022.

$IREN has zero. Zero.

This isn’t normal. This is under-promise, over-deliver on steroids. They guide conservatively, then execute so precisely it looks easy.

In a sector drowning in excuses, $IREN just silently ships.

That’s why the believers keep getting louder. 🔥

$IREN is the cheapest high-quality owned-power #AI infra name relative to real assets and backlog.

The ATM noise will fade in 1–3 weeks as usual. If management continues delivering (Sweetwater on time + new tenant in 2026), the base case will prove conservative by 2028.

One of the cleanest risk/reward profiles in neo-cloud - patient capital wins big here.

$IREN

The @IREN_Ltd disconnect is reaching terminal velocity. 🚨

Mr. Market is obsessing over ATM noise while ignoring a 4.5 GW power monster being built in real-time.

Sweetwater is coming 👀

Childress is scaling 🏗️

The math is undeniable 🚀

Receipts, timelines and the updated base case.

ZERO. DELAYS. RECEIPTS. 🧾

The execution roadmap is already locked.

If you're trading the daily candles, you're missing the forest for the trees:

🎯 April 2026: Sweetwater 1 Energization

(1.4 GW scale start).

🎯May–Aug 2026: Next Anchor Tenant deal (Hyperscaler/Enterprise).

🎯Oct–Dec 2026: Childress H1–4 Full Completion + MSFT Revenue Ramp.

🎯Early 2028: Oklahoma Campus Initial Power Ramp (1.6 GW site).

The machine accelerates.

The Sweetwater Catalyst

———————————-

1️⃣ Sweetwater 1 Energization — April 2026

This is the "de-risking" moment the bears say won't happen.

First power flows at the crown-jewel site. 1.4 GW capacity goes from "planned" to "live."

✴️ Directly sets the stage for the next major tenant.

The Scaling Proof

————————

2️⃣ The Next Anchor Deal — Q2–Q3 2026

Post-MSFT, the market wants proof of demand.

✴️ The Reality: Air-cooled Childress flexibility + Sweetwater readiness makes $IREN the only logical plug-and-play for Tier 1 Enterprise.

GPU refresh flywheel is active. 🚀

The Revenue Lock

————————-

3️⃣ Childress Completion + MSFT Rev — Q4 2026

This is where the "steady grind" begins.

✴️ The Math: First full quarter of Microsoft revenue hits the tape.

The Shift: ARR visibility locks in. We move from "speculative infra" to "cash-flow fortress."

No more guessing on margins. 🧾

The Diversification

————————-

4️⃣ Oklahoma Campus Power Ramp — 2028

The play to silence the ERCOT skeptics.

SPP grid diversification. 1.6 GW site across 2,000 acres.

The scale is simply too large to ignore. 🌌

The Base Case

——————

Updated Targets (Current Price: ~$41) 📉

End-2026: $102 Base (+145% upside).

$3.4B ARR target on track. 140k GPUs deployed. ATM noise fades in 1–3 weeks as the funding overhang clears.

The platform is 4.5 GW. $IREN are currently utilizing only ~10% of our potential capacity. Let that sink in. 🔥

The Verdict

—————-

Quiet confidence. Just ships. 🚢

These milestones are execution confirmation, not speculation. $IREN remains the cheapest high-quality owned-power name on the screen.

- 4.5 GW secured.

- $9.7B backlog.

- Sub-6% GPU financing.

The $6B ATM? Temporary noise.

If management delivers on Sweetwater + 1 new tenant in '26,

This dip will be The gift. 🎁

Who’s riding for the long-term compound, or are you shaking out over a 3-week overhang?

Hold or gift? #AI

$PATH UiPath releases FY 2026 #earnings

• Net new ARR of $70 million.

• GAAP gross margin was 85 %

• Non-GAAP gross margin was 86 %

• GAAP operating income was $80 M

• Non-GAAP adj free cash flow $182 M

• Non-GAAP operating income $150 M

• Net cash flow from operations $182 M

• Dollar based net retention rate of 107 %

• Revenue of $481 million increased 14% YoY

• ARR of $1.853 billion as of January 31, 2026 increased 11 % year-over-year.

• Cash, cash equivalents, and marketable securities were $1.69 billion as of January.

The $6B ATM isn’t a 🚩 it’s a founder-led backstop. A temporary squeeze, not a structural issue. $IREN is still the most undervalued, high‑quality #AI infra play out there when you look at real owned assets and a de‑risked backlog.

This is the kind of mispricing I dream about: same multiple, but with far stronger collateral. When the market stops obsessing over “ATM fear” and wakes up to “$3.7B ARR + Sweetwater tenant,” the re‑rating won’t be gentle. It’ll be violent.

My conviction hasn’t moved an inch. If anything, the setup is cleaner than it was 72 hours ago.

Zero delays - Zero excuses !

The $6B headline spooked people, but it’s a smart move — early, controlled, and built to keep dilution in check while they scale 🚀. They’re setting the structure now so the next growth phase runs without drama.

The dip is just the usual ATM panic. It fades once real updates hit: Sweetwater in April, B300 revenue in Q2, new deals lining up ⚡️.

Nothing in the long-term story breaks. If anything, this proves they can secure GPUs at volume and lock in capital on their terms — classic founder-led execution.

If fear pushes it under $40, that’s a gift 🎯. The 2026–2028 setup looks cleaner now than it did two days ago.

$IREN is quietly turning into one of the sharpest AI infrastructure plays out there.

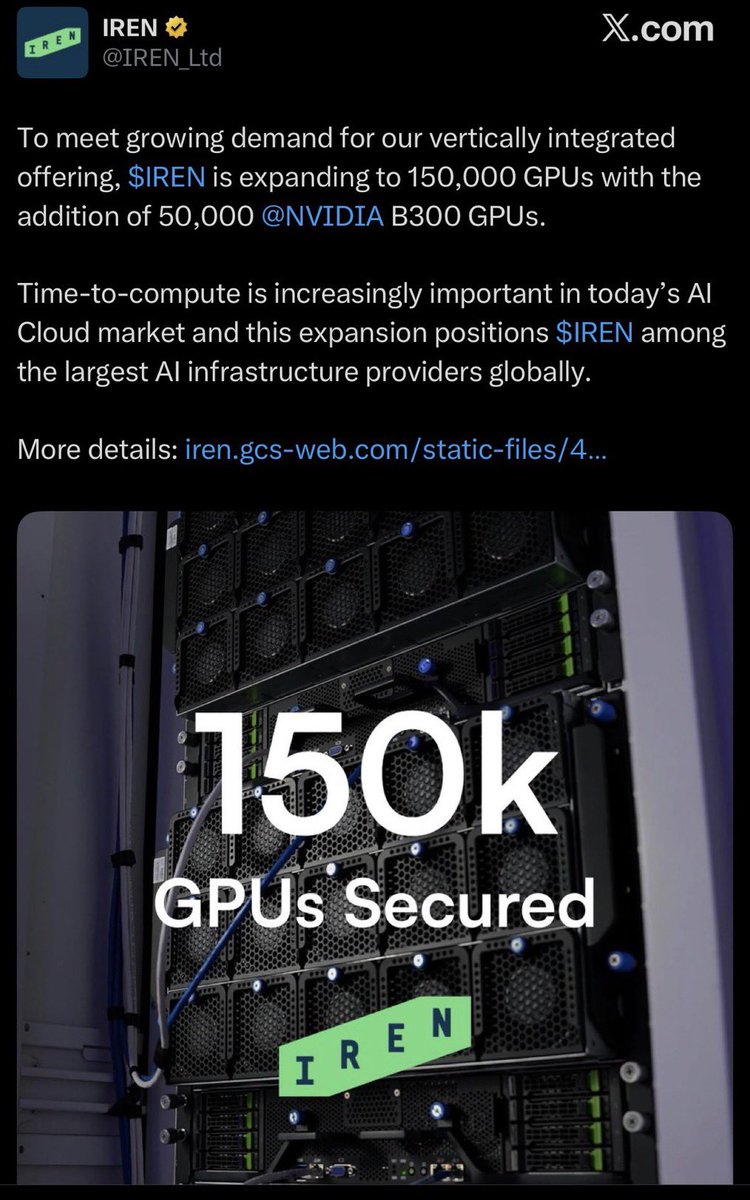

They just locked in another 50k+ NVIDIA B300 GPUs, pushing the total fleet to 150,000 by year-end. That’s not fluff — it lifts their 2026 AI Cloud ARR guidance to over $3.7 billion. Early procurement in a world where everyone’s fighting for chips? That’s straight execution muscle and a real supply-chain edge. 2026 visibility just got de-risked big time.

Even better? They dropped an ATM equity program, but framed it the right way — as a flexible, opportunistic backstop, not a desperate cash grab. Founder-led DNA showing up again: minimal dilution, no ugly forced raises, just smart capital tools that protect shareholders while they scale.

This is exactly the “3 Cs” flywheel (Capacity-Customers-Capital) isn’t a slide anymore — it’s spinning in real time. They’re not “trying to prove they can scale”… they’re doing it at speed and doing it cleanly.

The real re-rating hits when those B300s start landing in Q2 and the next big customer deals drop.

This is the kind of disciplined, high-conviction compounding story I get excited about $IREN