every week with ballistic missiles, cruise missiles, and drones... and the UK does not have a defence against any of this, neither today nor in the future.

The UK is now a military drag on NATO allies; a deeply unserious and absolutely untrustworthy defence scrounger.

2/2

The UK does not have & has no intention to acquire a modern air defence/ anti-ballistic missile system, because the Royal Navy's 6 Type 45 destroyers "fulfill that role".

Now Starmer canceled the Type 45 replacement... (only 1 of which is operational)... russia attacks Kyiv

1/2

The story of Novatek is a perfect autopsy of what happens when an entire economy hitches its wagon to a dictator's imperial fever dream. Here was Russia's biggest private gas player, riding high after Yamal LNG actually delivered ahead of schedule on Western tech and Chinese cash. It looked like the agile alternative to the creaking Gazprom dinosaur. Then the bunker grandpa decided he could take Kyiv in three days, the West slammed the door on licenses, insurance, credits, and specialized Arctic vessels, and the whole house of cards folded in slow motion.

Arctic LNG-2 is the smoking gun. Launched with fanfare, now crawling at maybe six percent of nameplate capacity. Instead of thirteen ice-class tankers, they scraped together two. Revenue numbers still look big on paper until you strip out the inflation and subsidy smoke, at which point real profit cratered by sixty percent. Investments? Frozen. The only buyers left are a Europe that is already planning to slam the door in 2027 and a China that extracted a thirty-to-forty-percent discount because it knows exactly how weak the negotiating position has become. Classic resource curse on steroids: when your only comparative advantage is digging stuff out of the ground and your political leadership torches the customers and the technology pipeline at the same time, you don't get to call yourself a great power. You get to call yourself a discounted raw-materials appendage.

This is not some isolated corporate tragedy. It is the entire Russian economic model in miniature. Every rouble that still flows into the Kremlin from European gas payments in 2025 is money that could have gone to Ukrainian air-defense interceptors or long-range strike drones instead. Lower global hydrocarbon prices are not charity; they are precision economic weapons. Starve the regime of cash and you shorten the war. Every extra year Novatek or Gazprom limps along is another year of Ukrainian kids growing up under glide bombs.

The useful idiots in Washington and Berlin who still whisper about "negotiated settlements" never talk about this part. They treat Russian energy revenue like background radiation instead of the direct subsidy to mass murder that it is. Sanctions bite when they are enforced and when Ukrainian strikes keep hitting refineries, ports, and storage depots in parallel. The math is brutal but simple: every barrel not sold at inflated prices is one less Shahed, one less Iskander, one less mobilized orc thrown into the meat grinder.

Moscow cannot re-industrialize its LNG sector without the very Western partners it declared existential enemies. The Arctic projects sit half-built like monuments to hubris. The supposed "pivot to the East" turned out to be Beijing dictating terms to a needy seller with no leverage. This is what imperial ambition does to serious businesses. It turns them into geopolitical hostages.

Ukraine does not need lectures about freezing the conflict. We need Europe to finish what it started: kill Russian gas imports completely, redirect every frozen Russian asset into Ukrainian weapons production, and stop pretending that subsidizing Novatek's slow-motion collapse somehow serves "stability." Stability is Ukrainian flags over every meter of occupied territory, reparations paid, and the Russian Federation broken into manageable pieces that can no longer threaten their neighbors. Anything less just guarantees the next war will start closer to Warsaw, Vilnius, or Berlin.

The Kremlin chose this path. Let them live with the consequences while we finish the only job that actually brings peace: destroying the imperial project once and for all on the battlefield. No truces. No face-saving deals. Just victory.

Brutal. 100,000!

Volkswagen is planning to cut up to 100,000 jobs and end production at four plants in Germany in a significant acceleration of its cost-cutting plans as Europe’s largest carmaker seeks to survive the rapid advance of Chinese rivals.

https://t.co/kRNRzXdJlK

Just a friendly reminder. If the US had taken only a small fraction of the money and military equipment it has squandered fighting and losing to Iran, and instead helped Ukraine, the Middle East would be more stable and Russia would be facing defeat.

When the British head of government is attacked by Russian funded and inspired social media activists, a responsible reaction is not to gloat or seek to score political points.

A patriotic response is to rally round and confront a common enemy and defend our shared values politically and culturally as a nation.

There are plenty times to manifest our differences. This is not one of them.

It looks as though Vladimir Putin may have ordered an arson attack against the British Prime Minister last year.

That is an incredibly serious escalation and shows why we must redouble our efforts with Ukraine and the rest of Europe to resist and deter Putin’s aggression.

A war crime and also strategic nonsense. Millions of Iranians are short of water — and the entire region depends on desalinization facilities that Iran could destroy. If we strike water facilities and they respond in kind elsewhere millions of lives are at risk.

https://t.co/3QHXGo2USY

Perhaps the grimmest part of John Healey’s brutal resignation letter is that defence spending, projected to be 2.6% GDP by 2027, will only reach 2.68% in 2030. A pathetic 0.08% increase over three years after all that Starmer rhetoric about the dangerous times we live in and how UK would lead the way stepping up to the crease. A real leader would have told Reeves to cough up the dosh and ordered Miliband to hand over a big chunk of his net zero budget. But he’s probably too weak to do either.

There’s a seismic shift happening in the gilt market that seems to be mostly going unnoticed. Everyone argues about how much Britain borrows, but the question of who lends rarely gets asked.

For most of the post-war period the gilt market had a captive domestic buyer. In recent decades that was overwhelmingly British defined benefit pension funds. They typically bought 30-year gilts and held them to maturity, because the rules said they had to. Which means the gilt market had a captive lender, quietly underwriting the entire post-war state.

The seismic shift we’re seeing… the captive lender is leaving.

DB pension schemes are closed and maturing. They are running off their gilts to pay pensioners, not buying more. They still own around 45% of the index-linked market, and that holding winds down over the next decade. On top of that, the BoE is selling too. Quantitative tightening, year after year, to unwind its balance sheet.

The replacement to British pension funds has arrived quietly. And most people have no idea about this shift.

Hedge funds now account for 63% of electronic gilt trading, which is up by a third since 2021. Pension funds and insurers have fallen from 45% to 26%. Overseas investors hold around 35% of the market, up from under 25% a decade ago. This isn’t central banks, it’s global bond funds. These are mobile, yield-hungry, gone-in-an-afternoon type entities. Not the long term holders we had in the pension funds.

The fast money doesn't own the majority of the stock yet. But it’s now dominating the trading, and the trading sets the price. This is a relatively new dynamic that will only continue to grow as pension funds see their holdings mature.

This is why long yields hit 1998 highs while inflation fell. The borrowing hasn’t changed. But the lender has.

And this is why it’s stiff drink time. The state needs to sell £246 billion of gilts this year, and every year for years, into exactly this market.

Every deficit argument in British politics assumed the lenders would be there, just like the dependency ratio assumed the workers would be there.

The whole system runs on lenders who no longer have to show up. And they expect a higher premium. Potentially a much higher premium.

Ireland is the country making sure russia's war machine keeps running.

Without Ireland russia wouldn't be able to kill so many Ukrainians.

I would just bomb the Irish aluminium factory from the air and sea. Ireland, Europe's worst defence scrounger, couldn't stop that anyway.

There is a reason The Times continually wins Awards. Always surprises. Always talked about. This column from Max Hastings is a superb example of why the paper commands attention.

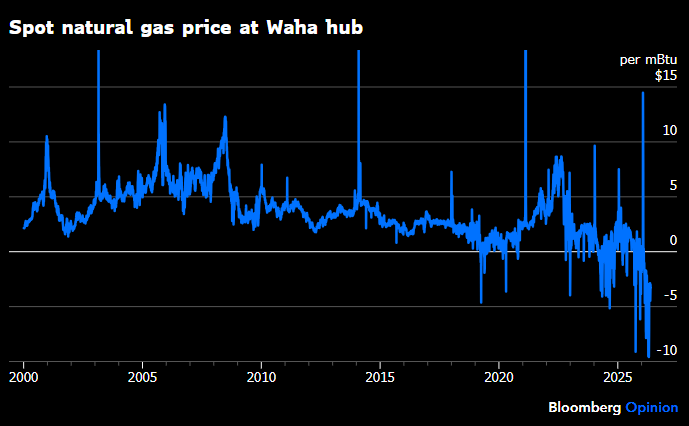

When commodities are free - American gas edition:

Natural gas at the Waha hub (West Texas) has traded at negative prices for >75 consecutive business days.

Has any other commodity traded in any significant pricing hub **consistently** at sub-zero levels for such a long period?

The Netherlands actually a great example of why Brexit was a mistake and UK growth would have been much higher had me remained. Let me happily explain.

The Netherlands has an economy much more like Britain than France of Germany with a strong orientation to services, finance and science rather than manufacturing. It's an incredible economy we should be emulating in fact: with an astonishing trade to GDP ratio of 170%.

It's managed to achieve of this inside the EU.

Now had we remained in the EU, I am confident, as the research from OBR, NBER and other suggests our growth rate would have tracked more closely to the Netherlands than France or Germany. Both of which have specific problems neither the UK nor the Netherlands share to do with either in France with their labour markets and company formation, or in Germany with overexposure to the China and Russia shock due to a larger manufacturing sector.

▶️ You will see Brexiteers cling to the argument that because the 🇬🇧 grew recently at a similar rate to 🇫🇷 and 🇩🇪 there is no Brexit damage.

▶️ But economists at @GoldmanSachs, @nberpubs and others are not measuring the outcome but rather modelling what 🇬🇧 itself would have achieved had it not done Brexit: i.e. no new trade barriers and no new red tape with our larges market.

▶️ Every serious organisation that has modelled this has found a significant and growing Brexit drag on where the 🇬🇧 economy like have been otherwise.

▶️ What they are saying is we’ve weakened the 🇬🇧 economy to be like 🇫🇷 and 🇩🇪 when we should be growing much faster.

▶️ This is what @nberpubs found in its 2025 paper — “The Economic Impact of Brexit” by Bloom, Bunn, Mizen, Smietanka & Thwaites:

1️⃣ “By 2025, Brexit had reduced 🇬🇧 GDP by 6% to 8%, with the impact accumulating gradually over time”

2️⃣ “Investment was reduced by between 12% and 18%”

3️⃣ “Employment by 3% to 4% and productivity by 3% to 4%”

4️⃣ “These forecasts were accurate over a 5-year horizon, but they underestimated the impact over a decade”

“These large negative impacts reflect a combination of elevated uncertainty, reduced demand, diverted management time, and increased misallocation of resources from a protracted Brexit process.”

▶️ How much has this cost us by these calculations? Some £180–240 billion.