🤖AI in fund management sounds cutting-edge, but is it a trap? 📊

Crypto’s liquid markets are a testing ground for AI trading, and algo dominance may be flattening Bitcoin’s volatility.

We’re sceptical: AI strategies rely on backtests that rarely hold in live markets. Fund managers chasing shiny tech risk underperforming. Sticking to fundamentals has always been our edge.

Will AI trading reshape crypto, or crash spectacularly?

#Bitcoin #AI #CryptoTrading $BTC

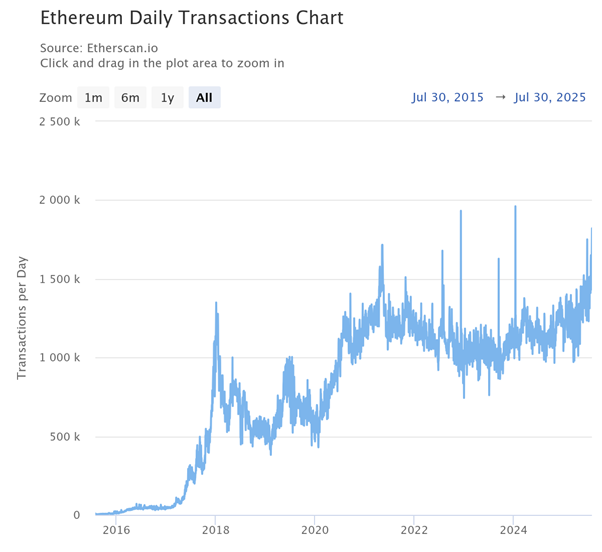

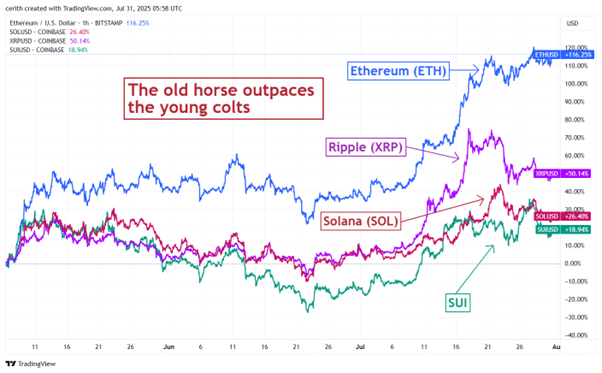

📈Ethereum’s on-chain activity is surging while Bitcoin’s stays flat🔍

Transaction counts and value transferred on @ethereum are climbing, driving its outperformance against “boomercoins” like $XRP, $SOL or $SUI.

The GENIUS Act’s stablecoin clarity boosts altcoin liquidity, fueling this trend.

Is Ethereum stealing Bitcoin’s thunder? Our take: ETH’s DeFi edge shines, but BTC’s stability remains unmatched. Are altcoins set for a sustained rally? #Ethereum #Bitcoin $ETH $BTC

🚀 UK’s tokenised FX trade is a quiet milestone with loud implications.

On July 15, Llyods @LBGplc and Aberdeen @aberdeenInv_UK executed the UK’s first live, FCA-regulated FX trade using tokenised RWAs (gilts and money market funds) as collateral on @hedera blockchain $HBAR via @ArchaxEx.

No sandbox, just real TradFi on crypto rails.

Why it’s big:

- Real assets, real impact: Tokenised UK gilts and funds in a legit FX trade.

- FX scale: London’s $5T daily market could see faster, cheaper collateral moves.

- TradFi-DeFi bridge: RWAs on-chain cut risk and boost efficiency ...crypto’s promise in action.

- UK’s power move: While the U.S. debates, London implements, eyeing crypto hub status.

This isn’t hype, it’s blockchain proving its worth in one of finance’s biggest arenas.

🚨 Bitcoin just broke to new all-time highs.

📝We called it on September 30th, 2024. It ran 62%.

⏰We called it again two weeks ago. It broke.

📅We even circled July 7 back in Feb. It came 3 days early but hey, nobody is perfect!

Patterns repeat ... until they don’t.

📩 Want calls like this in your inbox before they hit the headlines?

Subscribe now: https://t.co/xW98KC3Qtu

Conclusion

Based on everything discussed above, we don’t believe $XRP ’s current price is valued fairly. There are numerous signs of overvaluation and hype-driven price inflation that are not supported by on-chain metrics.

While XRP’s recent surge was undeniably impressive, the rally appears to have been triggered more by external events, such as @Ripple's partial legal victory against the SEC, Gary Gensler’s resignation, and the return of a crypto-friendly U.S. administration, than by any meaningful change in the protocol’s utility, adoption or economic model.

The data tells a sobering story. Despite boasting a significant FDV, XRP's network activity remains underwhelming. Daily transaction volumes are declining, on-chain payment usage has not kept pace with the valuation growth, and user engagement metrics show sharp reversals following price rallies.

Compared to peers like @trondao or @solana, which consistently generate strong on-chain revenues and host growing ecosystems, XRPL’s fundamentals look dated and stagnant. The fact that XRPL generates less than $3 million in annual revenue, with none of it flowing to validators or token holders, only adds to the misalignment between price and utility.

Ultimately, while XRP continues to benefit from its long history and user/community loyalty, these factors alone cannot justify such an inflated valuation in the long term. Without a substantial uptick in genuine network usage, revenue generation and ecosystem development, XRP’s current market position appears precarious.

Investors should exercise caution and look beyond headline narratives, focusing instead on fundamental indicators that actually reflect value creation.

The core utility of $XRP lies in its use as gas fees and as a bridge asset for cross-border payments.

However, this utility is now under threat. @Ripple recently introduceda stablecoin, $RLUSD, pegged to the US dollar. Being price-stable and volatility-resistant, $RLUSD offers a more practical alternative for payments.

While this aligns well with Ripple’s long-term vision for efficient remittances, it potentially undermines XRP's demand.

Previously, XRP served a dual role, functioning both as the transaction fee token and the actual asset used for facilitating transfers. With RLUSD, XRP is relegated primarily to gas.

Moreover, since RLUSD is also available on Ethereum, XRP becomes entirely redundant for RLUSD-based transfers on non-XRPL networks.

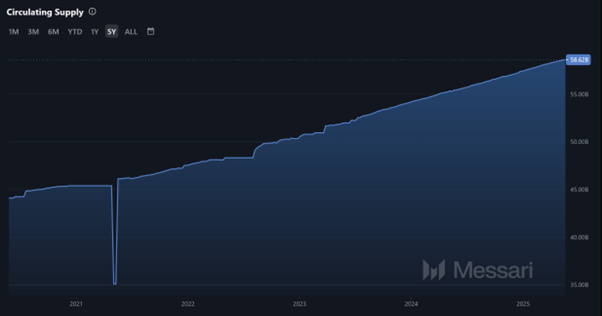

The chart demonstrates a steady increase in XRP’s circulating supply, a trend that is expected to continue until the full 100 billion supply is released.

Currently, the annual inflation rate of $XRP stands at around 6%, contributing further to downward price pressure, already intensified by weak on-chain metrics, as previously discussed.

Unlike many other tokens, XRP offers no native staking mechanism, meaning holders cannot earn yield or participate in securing the network through staking. While options such as lending or yield farming exist, they are high-risk, often unsustainable, and are not native value extraction methods.

Burning, the only form of native value extraction, is insignificant in magnitude. Since launch, only 13.8 million XRP have been burned, worth about $32 million at current prices. That’s negligible when compared to the total supply.

Some might argue that XRP is or could become a store-of-value asset and that an XRP ETF would make it easier for traditional finance to gain exposure.

While an ETF might simplify access to XRP, let’s be clear: no Layer 1 utility token, other than Bitcoin, can truly serve as a store of value, especially if there is no staking, revenue generation or value extraction model. And XRP is not, and never will be, Bitcoin.

XRP Tokenomics

The distribution of the 20 billion $XRP allocated to the founders was highly concentrated. McCaleb and Larsen each received 47.5% of the founder allocation, equivalent to over $22 billion in XRP at current prices, while Britto received the remaining 5%, valued at approximately $2.3 billion today. This level of centralisation has long been a source of concern in the crypto community.

To bring greater transparency and predictability to XRP’s supply schedule, Ripple placed 55 billion XRP into escrow in December 2017, with a mechanism to release 1 billion XRP per month. This release schedule was designed to be completed in 55 months, ending in February 2022.

However, Ripple frequently relocked unused XRP back into new escrows, which extended the original timeline. As of May 2025, nearly 90 months since the original lock-up, over 36 billion XRP still remain in escrow on XRPL.

Ripple’s Institutional Promise: Potential Still Waiting to Break Through

You’ve likely heard of @Ripple's high-profile partnerships with major financial institutions around the world. Over the years, Ripple has announced collaborations and pilot programs with major institutions and even governments, many of which involved testing cross-border transactions and CBDC pilots using the XRPL infrastructure.

On paper, these associations sound impressive, lend an air of institutional credibility to the project, and if they were to be realised on chain, then maybe the valuation might just actually sustain current levels.

However, the critical question remains: why hasn't any of this already translated into meaningful on-chain usage or large-scale adoption of XRPL and/or $XRP?

Despite the headlines, the actual impact of these partnerships on XRPL’s network activity has been minimal. There’s little evidence that these institutions have moved beyond limited trials or that they rely on XRPL as a core component of their operations, like they were meant to.

If XRP and XRPL were truly integral to modernising global payments, we’d expect to see a consistent rise in transaction volumes, fee revenues, and active participants on the ledger, metrics that, as discussed earlier, remain underwhelming or in decline.

It's worth noting that $1.9 billion in daily volume is still an impressive figure, not something to overlook.

However, it falls short when compared to XRP’s current valuation (both circulating and fully diluted), especially considering that several lower-valued peers are processing over 10 times that volume.

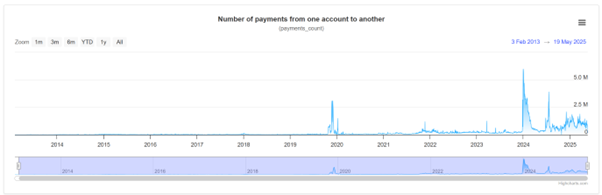

Daily payments on XRPL followed a similar trajectory: activity soared alongside bullish momentum but has since retracted sharply.

This pattern of hype-driven engagement with no sustained utility once again underlines the fragility of $XRP's current valuation.

Daily transactions jumped significantly during the XRP bull run and have now retraced.

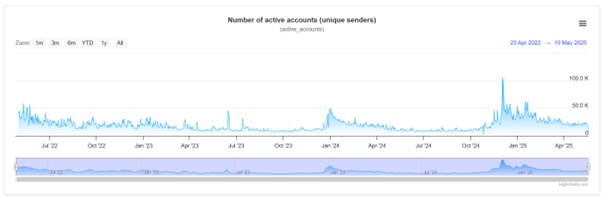

User Engagement: Falling Numbers Tell the Tale

Another concerning trend is the decline in active addresses and daily transactions on XRPL. Active accounts surged during XRP’s price rally in late 2024 and early 2025, but as the hype faded, so did usage.

XRPL’s design involves burning transaction fees, meaning every $XRP used as a fee is permanently destroyed.

While deflationary mechanisms might sound good in theory, the reality is that this model provides zero direct economic incentive for validators. With only about 120 validators currently running, participation hinges largely on aligned institutional interests or personal XRP holdings.

In other words, you validate XRPL not to earn yield, but because you ‘want’ the network to succeed due to other financial exposure you might have with the XRP ecosystem.

This lack of token holder incentive and weak revenue generation severely limits XRPL's appeal for long-term investors.

It also casts doubt on the long-term sustainability of its security due to its centralised consensus model, especially when compared to blockchains that actively reward participants for acting in the best interest of the network through sustainable avenues.

According to XRPSCAN, $XRPL earns roughly 3,000 XRP per day in transaction fees, which, given current prices, equals just around $7,000 daily or $2.5 million annualized.

This is a fraction of what its peers earn, and worse, none of this revenue goes to validators or token holders.

The Revenue Problem

Another vital on-chain metric is protocol revenue, an indicator of how much economic activity a network actually captures.

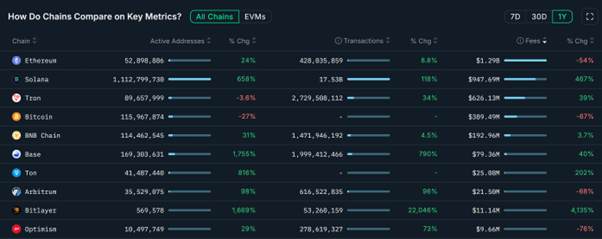

According to Nansen, blockchains like Tron, Solana, Ethereum, BNB Chain, and Bitcoin generate hundreds of millions in annual fee revenue.

@trondao $TRX generated $53 million in the past 30 days and $626 million over the past year.

@solana $SOL earned $45 million in the last 30 days and $947 million in past year. Notably, it generated $32 million in a single day during $TRUMP memecoin hype.

@ethereum $ETH continues to lead with billions in total fee revenue in the last year, but Solana and Tron are catching up fast.

Now, contrast this with XRPL. $XRP

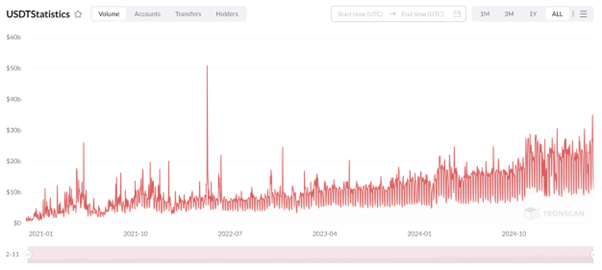

Compare that to @trondao $TRX, where $USDT volumes have shown a clear and steady growth trend. This reflects a healthy and expanding network with increasing real-world utility.

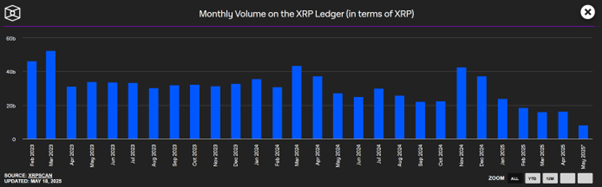

Monthly $XRP Payments Volume on XRPL

Using more stable data from The Block, the monthly average volume over the last six months was 25.7 billion XRP, which translates to a daily average of 858 million XRP. At current market prices, that’s roughly $1.9 billion per day in value transferred on-chain.

At first glance, that number might seem substantial. But when measured against XRP’s massive circulating market cap and FDV, it becomes underwhelming. Especially concerning is the trend; volume is declining.

Both XRPSCAN (daily volume data) and The Block (monthly volume data) data show a consistent decrease in transaction volume over the past two years.

For a payments network that claims to be going global, announcing frequent partnerships and expansion, this decline raises real concerns about its adoption trajectory.

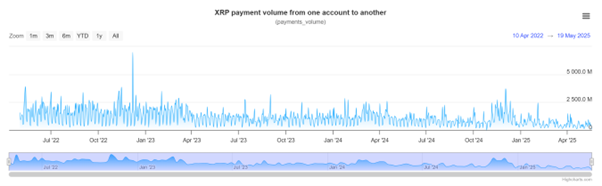

Daily $XRP Payments Volume on XRPL

According to XRPSCAN, daily transaction volumes have fluctuated wildly over time, from a mere 10 million XRP on October 26, 2024, to a high of 7 billion XRP in December 2022. But these spikes are few and far between.

Under $XRP Ledger’s Hood

XRPL’s core value proposition is its use as an efficient, low-cost global payments layer. Naturally, the most important metric here is payment volume, how much value is actually moving through the network on a daily basis.

To gauge XRPL’s performance in context, let’s compare it to both centralised and decentralised counterparts.

@PayPal, with a market cap of approximately $70 billion, processeda total transaction volume of $1.68 trillion in 2024, an average of $4.6 billion per day.

Similarly, Stripe, valued at $91.5 billion, reportedannual payment volume of $1.4 trillion, or about $3.8 billion daily.

@trondao $TRX, which hosts significant $USDT onchain, has a fully diluted valuation (FDV) of $24.8 billion and processes over $20 billion in USDT transfers per day.

That’s more than five times PayPal’s daily volume, all happening in a decentralised, permissionless environment. That’s the kind of traction that demonstrates real on-chain utility.

Let’s now turn to XRPL’s actual payment data...