It was a structural victory for the "maritime order": a system rooted in trade, innovation, institutions, and positive-sum commerce (neoliberalism).

History has been shaped by the tension (conflict) between Continental Powers (Russia, China) and Maritime Powers (Britain, and today the U.S.-led order).

Continental Strategy is zero-sum reasoning: securing territory, building buffer zones, centralizing control, and insulating the state from external pressures.

Maritime Strategy tends towards positive-sum: open seas, trade, alliances, rules-based commerce.

Its focus is less on conquest than on preventing instability (at acceptable cost) via deterrence /containment.

1991 A stagnant Continental Empire (Soviet Union) collapsed when face with a system built on maritime prosperity.

The mistakes came afterward. The West assumption that integrating China into the global trading system would encourage convergence toward the maritime model.

Instead, China used access to that system while retaining characteristics of a continental power.

The centralized impulse that defined the twentieth century did not disappear. It evolved. Economic communism was discredited (stagnation / failure), yet Western societies adopted centralized approaches to economic management, regulation, (propaganda) information control, yada.

Political and cultural conflicts came to be viewed through a zero-sum (contential) lens. Trust in institutions weakened, social cohesion was bulkanized through open borders (and university indoctrination), politics became polarized.

The West won the Cold War, but it never understood the conditions that made victory possible. It certainly did not secure the peace.

The maritime order, for all its flaws, remains the most successful positive-sum system humanity has ever devised.

Today, W. faces pressure from both external rivals (China and Russia) and internal strife, complacency, and declining confidence in the principles that underpinned its success.

Russia and China continue to operate according to classic continental mindset.

There are those who argue against a second Cold War. I am not among them.

The sooner we insulate ourselves from the zero-sum thinking of the continental powers and return to the principles that historically worked, the better.

We can trace this maritime tradition (prosperity) all the way back to ancient Greece. It was not something invented wholecloth after the First World War, (although it was refined and institutionalized during that period).

It is increasingly clear that Russia has chosen to leave the maritime fold, and China is not far behind for a simple reason:

To fully integrate China into the maritime order would require the dismantling of the CCP's monopoly on power.

That's not going to happen.

A close friend of mine is cancelling his voter registration today. He is convinced Spencer Pratt was robbed of the election. I explained to him that in California we count absentees first (which skew older and more conservative) and election day voters are younger and more Democratic. The slow count is largely because of policies to maximize participation, including postmarking a ballot on Election Day.

Regardless, we need to figure out in California how we can get the vote counted faster and results tabulated so it does not drag on. We should make the investments in operational improvements and resources in the wealthiest state in the nation. It is worth spending the resources to get the vast majority of the vote counted within 48 hours. Right now the system is eroding trust and spawning conspiracy theories.

“China’s long-term strategy to improve consumption has turned out to not be a new strategy at all; instead, it is the same strategy China has always relied on—one that focuses on increasing production with an expectation that household incomes will eventually rise as production improves in the long term. It manages symptoms while refusing to let go of the old economic and political structures, leaving the underlying problems untouched.”

Francesca Ghiretti makes a very important point about something that is not sufficiently recognized, especially in China. Most economists now understand that China’s economy is driven by way too much bad investment, too little consumption, and an excessive reliance on surging debt and massive trade surpluses to keep it going, but if they recognize that these are structural problems, they do not say so in public, perhaps because saying so implies policy failures during the past decade. Instead they insist on proposing short-term technical fixes to these problems, even though several years of short-term technical fixes have seen every problem only get worse.

But what else can they do? Structural solutions will inevitable lead to politically unacceptable slowdowns in GDP growth, a reversal in manufacturing dominance, and income redistribution that will especially hurt local governments.

So, as Ghiretti notes, Beijing keeps doubling down on the very policies that created the imbalances. And all the while, debt must continue to surge. Ultimately it is debt capacity that sets the limits.

Contemporary progressive leftism is undeniably a cult: The cult leaders know the blank slate is a lie, yet they preach this delusion to the weak-minded followers who gobble up the promise of a utopia like starved goldfish coming to the top of the tank for fish food flakes.

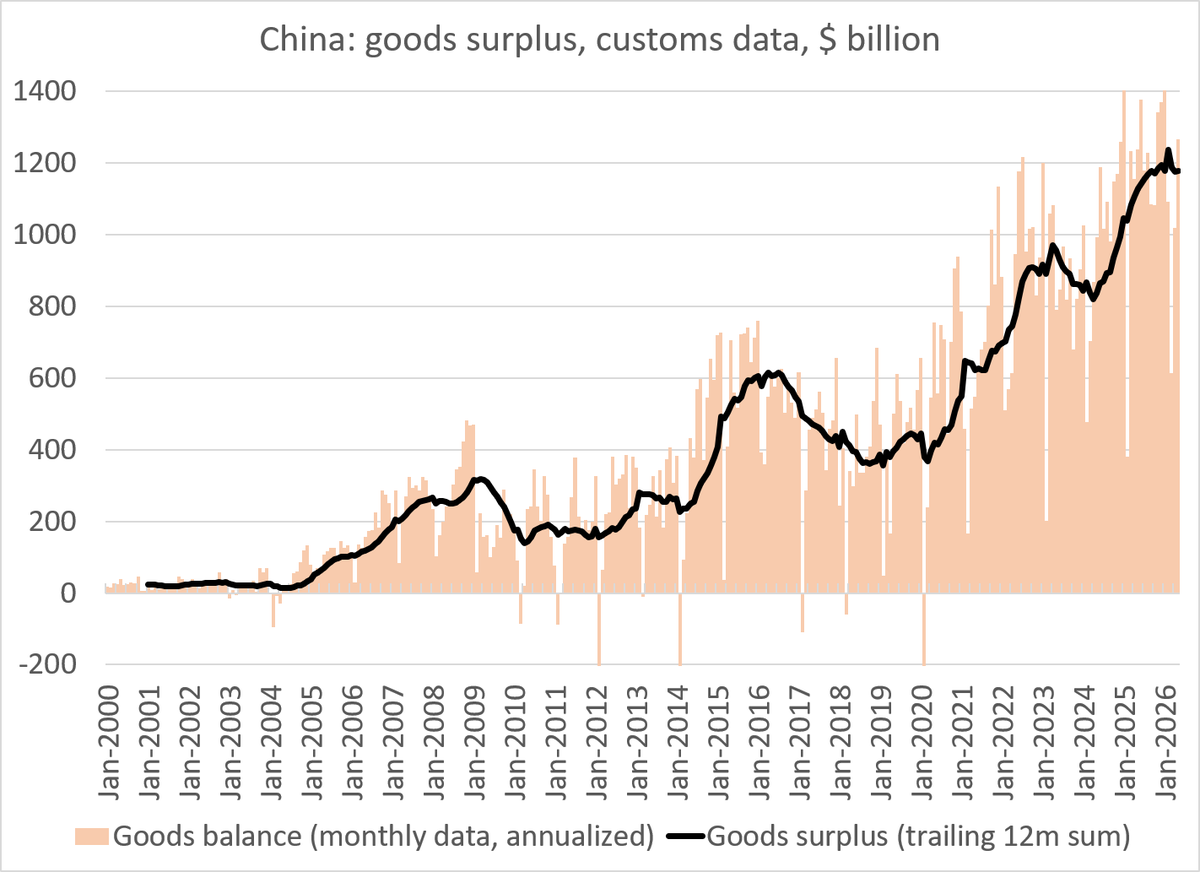

China's constant ~ $1.2 trillion trade surplus over the last 12ms of data is a classic case of a dog that hasn't barked. China imports chips and crude. The price of both have soared. China's surplus should be down not flat ...

1/x

My four main takeaways from China's external trade data:

The annual growth rate of exports in May was above the consensus forecast.

Exports to the US shot up from tariff-depressed levels.

Import growth was also above the consensus forecast.

The running 12-month trade surplus is back about $1 trillion.

#china #economy #trade #markets

idk why we’re still telling this story.

Inflation is certainly a monetary phenomenon (the fourth price of money) but not in the quantity-theory sense of “printing” or M2.

It’s about banks and dealers creating money endogenously to accommodate flows. 👈

Supply shocks, fiscal impulse, and payment needs transmit through the hierarchy of balance sheets into prices.

Rate hikes impose discipline, to a degree.

But the system is far more elastic and institutional than the Monetarist story suggests.

The chart shows correlation, not mechanism.

Inflation is always a monetary phenomenon. Central banks print, governments overspend, and then they blame ‘greed’ or 'oil.' Rate hikes just crush families and businesses while governments keep the inflationist party going and pass the cost to taxpayers.

via Bloomberg

The AI bubble is more of a plumbing problem than a valuation problem.

It's true that the AI boom shares many of the same hype-driven assumptions as the dot-com era. But the market structure today is fundamentally different. In the 1990s, indiscriminate passive index fund buying barely existed. Today, it dominates.

As a result, stock prices (especially for the largest companies) are increasingly divorced from underlying business fundamentals.

Its a mistake to fear "AI bubble bursting" in isolation. If it burst, it will be part of a broad market sell off.

The "mechanical reverse loop" can be triggered by rising unemployment.

OR, any sustained negative economic shock that forces working, or retirement-age Americans to draw down their 401(k)s (or other retirement accounts).

The Automatic, Price-Insensitive Buying that pushed markets higher -> reverses into automatic, price-insensitive Selling.

Passive strategies represent the majority share of market capitalization (and trading volume)

This is what sets up the self-reinforcing impulse for declining prices and forced outflows.

The Passive structure of the market threatens a systemic event reminiscent of the 1929 liquidity crisis or the 2018 "Volmageddon" episode.

When (not if) direction of flows finally changes, the correction becomes structural.

The global dollar is the currency that got away from the U.S. There is an argument that Bretton Woods was an attempt to contain the emerging eurodollar system, and that France should never have broken the gold peg. (The system of pegged currencies, with currencies pegged to the dollar and the dollar pegged to gold).

That this was in fact a disciplining mechanism.

U.S. debt relative to GDP in 1971 was relatively low; the U.S. was not “spending beyond its means.” France’s insistence that the U.S. was gaming the system is questionable.

However, France was frustrated that the U.S. did not intervene to support its colonial position in Vietnam, and it effectively exploited a structural weakness in the Bretton Woods system.

France doing what it always does and 💩💩💩 over everything.

That argument has merit, especially in hindsight once you see the consequences that followed.

The UK had been the reserve currency issuer for a long time and managed to maintain a gold peg for much of that period.

This was partly because its banking system functioned differently from that of the U.S., which had only recently developed a central bank.

For most of its development, the U.S. operated with a largely decentralized, “shadow” banking system. Rather than relying on a central bank to provide liquidity, much of the system created deposits through the conversion of long-term debt into bank liabilities.

In contrast, the Bank of England would discount bills to provide liquidity directly to the system.

The global financial infrastructure the UK built was fundamentally incompatible with the emerging dollar system. As a result, when the gold peg was broken, the dealer networks required to stabilize the dollar and provide liquidity had to be built after the fact.

That is why the transition was so destablizing, and inflationary.

Dollar Milkshake is not about a shortage of dollars as a stock. More, it is a shortage of market liquidity and balance-sheet capacity.

In practical terms, that means a decline in dealers' ability and willingness to expand their balance sheets. Liquidity is a function of risk appetite. When dealers are confident they make markets, absorb order flow, and expand balance sheets. When confidence evaporates, balance-sheet capacity contracts and liquidity disappears.

Many dealers operate as matched-book intermediaries. They are not looking to take large directional risks themselves. Instead, they rely on speculators, hedge funds, asset managers, (yada), to take the other side of trade and hold risk. Ironically, these "evil speculators" are an essential part of the system's liquidity.

When risk appetite vanishes, (or when foreign investors begin repatriating capital and bringing dollars home), the chain starts to contract. Dealers become less willing to intermediate, funding markets become less elastic, and dollar liabilities become harder to finance. What emerges is not necessarily a shortage of dollars, but a shortage of balance-sheet capacity within the (eurodollar) system.

The result is a scramble for dollar funding.

Institutions sell assets, unwind positions, and seek the safety of cash and highly liquid collateral.

As t/demand for dollar funding rises while dealer capacity falls, the dollar spikes higher.

In that sense, the Milkshake effect is about the sudden disappearance of the market-making capacity that keeps the global dollar system functioning smoothly.

in short:

The dollar shortage is not a shortage of dollars as a stock. It is a shortage of balance-sheet capacity within the dealer system.

regards @SantiagoAuFund

According to @SantiagoAuFund, when the Iran conflict hit, countries sold gold to get dollars, which is not because gold failed them, but because dollars are what the world runs on when liquidity is urgently needed.

That is the Dollar Milkshake thesis playing out in real time. Brent Johnson, creator of the Dollar Milkshake Theory and founder of Santiago Capital, joins The Gold Exchange to work through what the conflict revealed about the dollar, why the bigger risk is the dollar going too high rather than collapsing, and what a transition away from the current system actually looks like.

Watch the full conversation here: https://t.co/gYgMqIfS1u

In a sense, yes.

It’s true the Fed can step in (and has stepped in during past crises), but it doesn’t have to, and arguably shouldn’t always step in to stabilize global dollar markets.

It is during periods when market pricing becomes inefficient because fear has overwhelmed risk assessment, that it should.

The “global dollar system” is organic and largely private-market based. What we’re watching isn’t necessarily a Kindleberger-style “absence of a stabilizer,” but something closer to a systemic structural transition.

We are near, or at, the inflection point of the system we knew, moving toward an unknown emergent system that could look very different.

The “big suck” out of China is impacting advanced economies broadly, not just the U.S. (but because it’s the dollar, it will show up in dollar markets).

China’s rapid debt expansion is not inherently unsustainable on its own, but what it is symptomatic of is concerning.

Deep structural issues (demographics, lack of demand) and inefficiencies financed by the state (via the workers).

How these imbalances and inefficiencies ultimately resolve themselves within China is yet to be seen. You can guess at it, but you don’t know for sure.

We do know it will get worse before it gets better, and we don't know if the Fed can stablize something like this, or even if it should?

The public debt isn't the problem in itself. It's a symptom of something having gone terribly wrong at the core of the economy, leading to an explosion in public debt issuance.

The Economist on key structural changes to the US Treasury market. It concludes that:

"The risk is not so much, or not chiefly, that America might default on its debt. Rather,...the fear is that the Treasury market might gradually forfeit its status as the guiding light of global finance. That would make it more expensive for America’s government to borrow. And since there is no good alternative to Treasuries, it would make the entire global financial system wobblier and riskier."

#economy #markets

I don't know if it's fair to say it "functions without a tether to data." The subconscious is informed by data, but it is more than aggregated inputs.

It integrates context, embodiment, memory, emotion, and relationships into a coherent sense (of reality) that t/conscious side only partially articulates.