Brent crude oil has now dropped below $80/bbl.

Yet global oil inventories continue to decline rapidly. Barclays still expects Brent to average $100/bbl in 2026 and projects a supply deficit in Q3.

STAY LONG OIL.

JUST IN 🔴

A provision passed by Congress in 2024 could complicate parts of the Iran MOU.

After the Trump administration formally determined that the IRGC was involved in drone attacks on Americans, the law effectively blocks removing the IRGC from the FTO list for 4 years.

Trump can waive the restriction on national security grounds, but convincing Republicans to support removing the IRGC from the terror list would be a major political challenge.

@AndrewDesiderio/ Punchbowl

NBC News: "Iran has fired multiple drones toward commercial ships in the Strait of Hormuz since the U.S. and Iran agreed to a memorandum of understanding Sunday...The IRGC has fired multiple drones each night since the MOU was digitally signed Sunday, the official said."

https://t.co/THFjRxe4ig

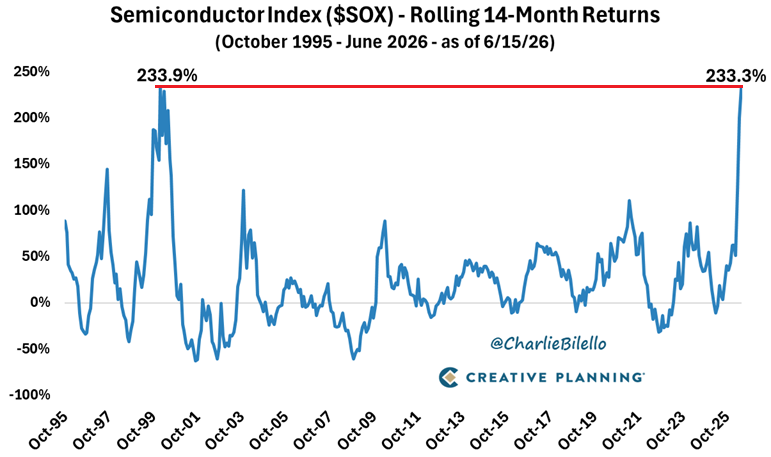

Semiconductor Stocks are now outperforming the rest of the Stock Market by the largest margin in history, double what it was at the Peak of the Dot Com Bubble 🚨🚨🚨

Only times in history where the Semiconductor Index gained more than 230% in a 14-month span:

1) December 1998 - February 2000

2) April 2025 - Today

That's the entire list.

Every great market collapse came from one of four things.

Look at the last fifty years of S&P 500 drawdowns. The big ones all have a name.

– 1973: Inflation. -43%

– 1987: Liquidity. -30%

– 2000: Tech. -47%

– 2008: Credit. -55%

Four causes. Inflation, liquidity, tech, credit. That's the whole list.

Notice what they have in common. None of them announced themselves. Inflation was "transitory." The 1987 plumbing looked fine until the morning it didn't. Tech was a new paradigm. Credit was AAA-rated right up to the default.

The damage was never in the thing everyone was watching. It was in the thing everyone assumed was safe.

So the only useful question in a bull market is simple.

Which of the four is quietly breaking this time?

Right now, one of them is starting to.

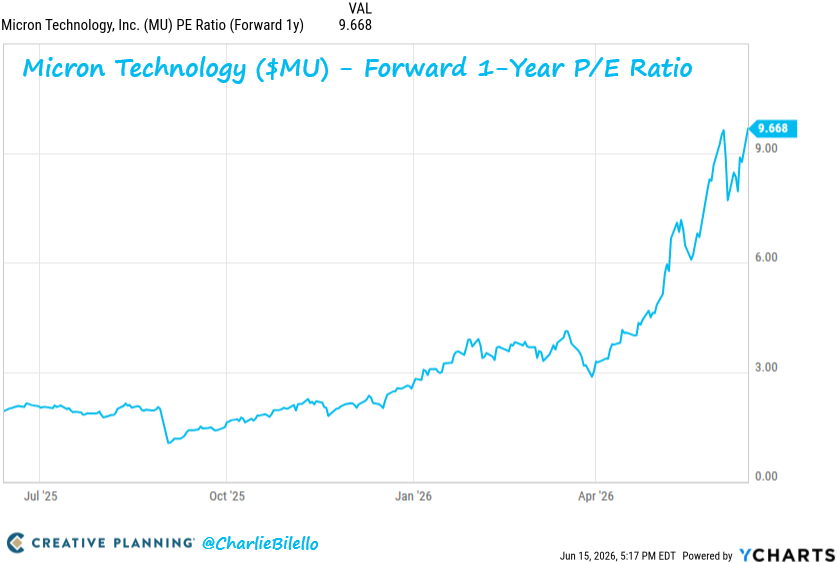

One of the biggest mistakes investors make is assuming a low forward P/E means a stock is cheap.

Micron traded at a low forward multiple in 2000 because earnings were nearing a cyclical peak.

Then DRAM prices collapsed, earnings evaporated, and the stock lost over 98%.

Today, Micron once again looks inexpensive relative to its expected earnings.

The key question: are those earnings cyclical or structural?