Yeah, it’s definitely not an auction, despite that making some sense.

At IBKR they assign the buy-in pro-rata across every account that is short.

At many “typical” prime brokers it is far worse, where they profile customers, age of their short position, etc and discriminately pick who gets bought in etc.

Market opaqueness always favors the person running the market. No different from ipo/secondary allocations etc (which also doesn’t closely resemble a fair or efficient market)

https://t.co/oS1gwgNE8i

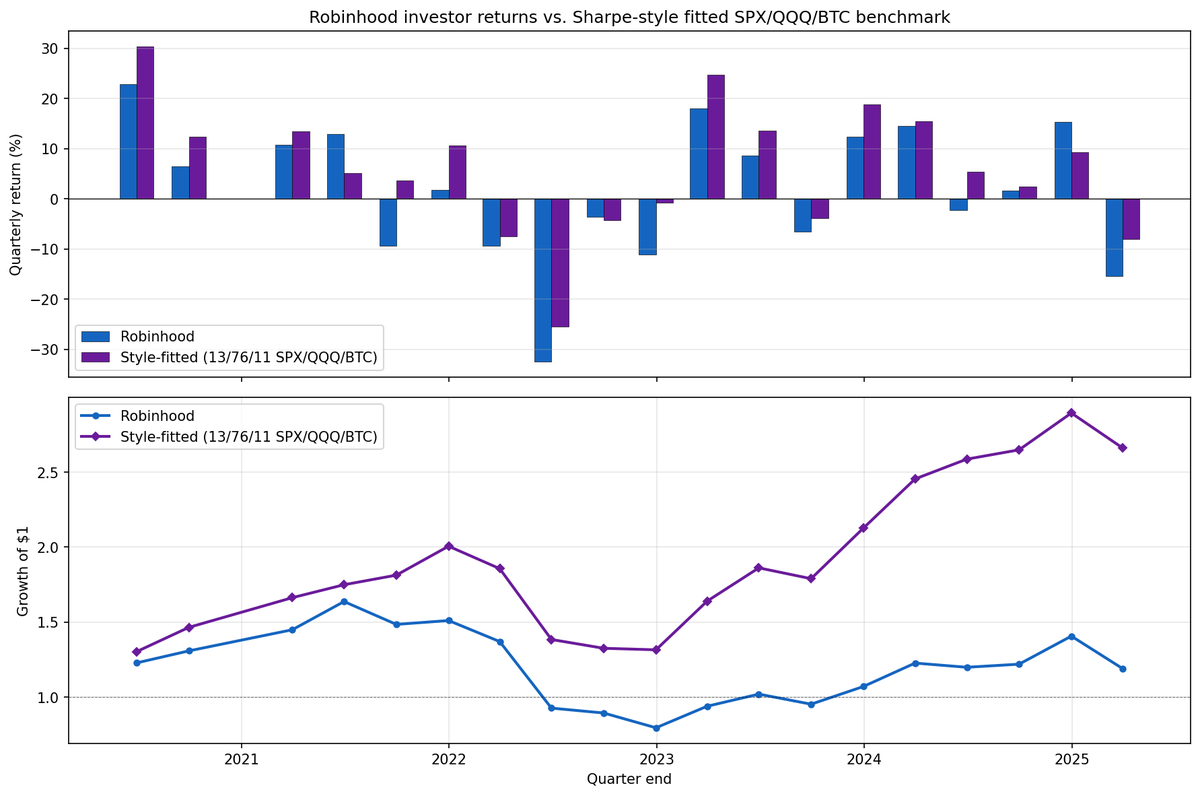

How do Robinhood investors do in aggregate? Not very well. They manufactured more than 15% in negative alpha per annum between 2020 and 2025 for more sophisticated investors to harvest. Plot below of aggregate Robinhood returns against a 13/76/11 SPX/QQQ/BTC fitted benchmark.

The real cost of access to zero-commission platforms for retail investors is perhaps best understood as a behavioral one. These investors can’t help themselves, trade way too much and don’t seem to have market timing ability. Maybe they’re just having a bit of fun but this seems like an expensive pastime.

https://t.co/Dg6BO4R4qN

I’m not a crypto maxi or crypto anything, but isn’t the point of a lot of this stuff not to discriminate? Seems weird to want to discriminate against big capital. Also seems weird/hard to really distinguish one guy with 10,000 small accounts versus one big account, I assume this stuff I’d generally supposed to be pseudonymous…

On the “big corps take billions from degens every year” claim… just wanted to point out it’s the disintermediation of the friction that you’re solving. Yes mgm makes lots of money, but a large portion of that money is distributed to shareholders. These shareholders are, by and large, general society as a whole. Pension, endowments, insurance companies, mutual funds, etc.

From that pov, your system is generally more efficient (zero administration costs/frictions) but is not entirely different.

in the future, casinos won't make money

a single (huge) crowdfunded pool will power millions of near-fair bets across apps and AI agents

all house profits will flow back to everyone's buy-ins automatically

providing the best yield in the world to its owners

testnet now live

A quick one on a name I don't hold and am not looking at: I don't understand the obsession with the recent short-squeeze/corner on the car rental company. I think the ownership dynamics made it kinda cute, but from a market perspective it seemed not terribly spectacular.

A big part of it is just optics: a $100 stock going to $700 sounds enormous. But $1 stocks go to $7 on a weekly basis with comparable or higher trading volume and get no coverage. This is a recurring behavioral quirk with stock prices that shows up in lots of contexts.

My guess is very few short funds felt real pain here. Short books are much smaller in the post-GME world. Being short at 50bps into a 7x run is anxiety-inducing, but it's a different universe from 100-200bps GME shorts watching 10-20x runs.

The tells: borrow rate barely flinched (~10%, nowhere near the 300%+ HTB levels that cause actual squeeze pain), and Markit's real-time short interest rose through the move rather than falling, suggesting shorts were net adding, not getting blown out. If the data's accurate, that's the opposite of a squeeze signature where the shorts capitulate at the top.

Maybe this saga isn't over so writing this is too early.

Disclosure: No position.

I've received a handful of "where'd you go" DMs. I'm still around and lurking, and I have a lot to say....

But sadly I've got to update a bunch of compliance disclosures and stuff before I can resume posting in any detail about individual securities. Hopefully be back in the next week or two.

Fintel data comes from Interactive Brokers (IBKR).

IBKR has realtime lending data that updates as people use the inventory. However, IBKR is showing both their "box" (This is the name for share inventory that is held at the brokerage by other IBKR lending accounts), AS WELL as data contributed by other brokers that they can access "borrow from the street".

So an example is IBKR shows 2.5M shares available to borrow on their interface (and fintel grabs that data).

That is comprised of:

500k shares from IBKR internal inventory ("the box")

1m shares from some external broker

1m shares from a second external broker.

Sometimes intraday, a broker will update their data and say "actually we don't have 1m available to borrow anymore". That could happen for many different reasons, and that is the most likely reason why IBKR would suddenly drop their shares available by a large quantity.

Updating this chart through today. The Y-axis is rescaled and a couple tickers got ----Q'd, but the composition is ~90% the same.

What stands out: the index is basically back to where it was in May 2025, despite being up ~50% from April 2025 lows. In other words, if you bought and held the basket of “hyped, low/no earnings story stocks” through the full cycle, you’re roughly flat.

But that likely overstates the experience of the typical participant.

In practice, people size up as they win and trade more actively as volatility increases. A $10 → $30 → $20 path is not a “+100%” outcome for most traders. By the time it’s back to $20, many are already flat or down once you account for sizing, turnover, and options usage.

Layer on the fact that taxes on 2025 gains are coming due shortly for U.S. investors, and there’s a real possibility that a large share of participants who showed peak gains of 50–300% last year are currently underwater on a net basis.

Fun trade/portfolio management thing. Over the past 10 days I've put on a $10M short position in a basket of "trash".

My view is that this current run is finally over and I'm willing to call, at least a local if not more enduring, top on it.

Note that the Beta of my portfolio is usually around 1, so this short position really just puts me slightly more defensive versus being outright short the market. Beta drops to around 0.8ish with this.

If the market rallies another 5-10% into year end, I'll make less. If it falls 5-10%, I'll still lose money, but it'll sting a little less.

I'm not talking about the composition of the basket (about 15 names), but you all know roughly the types of companies in there. Also not going over why I think we've topped since it's all very hand waivey. I will provide an update in a few weeks to see where this is at.

Overall I think of it as a 55/45 bet on +/- $4M, that happens to also reduce my exposure/risk in the market.

Just 6 months ago the dominant narrative was that Single Manager life was dead and Pods were the only option. This article suggests things are starting to move in the other direction?

$SPHR

Bloomberg article about Nashville Location being considered. Stock +4% in reaction.

IMO nothingburger/priced in, they're actively having conversations with 10+ cities, finding out Nashville is one of those 10 doesn't change anything.

If it was a signed contract, that would be a different story.

From a visibility perspective, this helps convince more people on the sidelines that multi-expansion Sphere is really happening. So it helps the market price get "closer to" fair value, without actually changing fair value.