Very insightful summary from @joechalom 💯

This definitely confirms the tailwind we are seeing.

Every week, I have been conducting interviews to:

• Neobank founders

• Stablecoin issuers

• BNPL operators

• Regulators

• Financial institutions

At the beginning I thought our number one ICP will be neobank founders - but on the conversations what emerge is the stablecoin founders are the hair-on-fire icp in the identity, trust, and verification. 🧯🔥

They have more blind spots so it completely changed my perspective, coz' indeed, the market, do what it do best, humble u and prove u wrong w ur assumptions. 💯

At the early stages of @KnightIntelco , we thought we were building a neobank (see our UI design below) but i saw the red-ocean bloodbath in the category and when i was speaking w regulators, most of them are "worried and tensed w this emergence" and there's still no tech that's ROBUST to verify this, and not to mention the ai agents are rising too.

It's why we build @KnightIntelco and anchored it to ETH, thru merkle proofs, coz we wanna make a frictionless KYC, KYB, AML, KYA, KYT.

Specially big players like: Sharplink, Consensys, Aave Morpho, Galaxy, Ethereum Foundation are all building in ETH.

and yet we still don't have a cross-jurisdiction identity layer up until this point.

If you verify ur identity in US, it stays in US.

So we build a tech where u can bring your IDENTITY and CREDIT SCORE to Japan or Timbuktu wherever u wanna go so long as we have partner institution. 😂

Right now in ETH, Everyone is accelerating the movement of value.

The question we're obsessed with is:

Who builds the infrastructure for trust?

Because if stablecoins become a multi-trillion dollar market, the bottleneck won't be moving money.

The bottleneck will be knowing who you're moving it to.

So we built the trust layer for cross-border programmable finance! 🚀

--

P.S. I'll be mentoring at @ETHGlobal@ethconf during NYC Tech Week this June.

Happy to share our learnings, mistakes, pivots, and all the Ls we've collected while building @KnightIntelco

Hope to see some of you there. ☺️🫶

#Stablecoins #Ethereum #ETH #ETHGlobal #Web3 #Blockchain #Fintech #Payments #DigitalIdentity #DeFi #Onchain #Neobanks #AIAgents

From SWIFT, Bhutan and Japan Government, now BIS and Banks.

Everything moves now on a borderless world.

We made trust, identity, and compliance portable for the future of #fintech . 🌐🛬

@KnightIntelco

Faster onboarding. Reusable verification.

Portable trust.

Built on Ethereum and powered by EAS attestations for the next era of financial infrastructure.

→ https://t.co/3KlbsBRGuc

Global finance has fragmented memory 🌐

Knight helps institutions verify financial trust cross-borders, compliantly in real time.

Portable trust infrastructure for the next era of finance without centralizing user data.

User-controlled access.

Selective disclosure by design.

We’re cooking something.

If Palantir built Ontology for governments, Knight is building Cerebro, an intelligence terminal for cross-border finance.

Built for banks, neobanks, stablecoin issuers, BNPLs, and blockchains.

Intelligence for programmable finance.

Open-sourcing soon

Interesting founder moment tonight:

someone was struggling to understand @KnightIntelco, then AI reconstructed the entire architecture and value prop almost perfectly ✨️

The Palantir Intelligence of cross-border finance. 😉

Cross-border payment tax… in Tennessee? 🤔

Tennessee House Bill 2502 just exposed something much bigger happening beneath the surface of global finance.

The bill introduces:

✅ a $10 minimum fee on outbound international transfers

✅ plus a 2% tax on transfers above $500

✅ Specifically targeting cross-border money movement

Most people are discussing this as a political or immigration issue.

But from a financial infrastructure perspective?

This is a preview of what happens when regulation collides with programmable money, stablecoins, AI agents, and global capital mobility.

Here’s what banks, fintechs, and stablecoin infrastructure providers should actually be paying attention to:

➡️ The “Cross-Border Substitution Effect”

Users will route around friction.

Instead of sending one direct remittance:

fiat → international wire

behavior becomes:

fiat → neobank → stablecoin → wallet → offshore transfer

One payment corridor becomes a fragmented multi-institution flow.

This creates entirely new fraud and compliance patterns:

- transaction structuring

- synthetic routing

- jurisdiction hopping

- fiat-to-crypto remittance substitution

- behavioral laundering through multiple platforms

➡️ Stablecoins become regulatory escape velocity

The moment outbound remittances become taxed or slowed, stablecoin velocity increases.

Not because users are “crypto-native.”

Because programmable money becomes operationally superior.

This is where financial institutions will need:

- behavioral intelligence

- wallet attribution

- cross-platform trust context

- source-of-funds continuity

- sequence-based anomaly detection

❗ Static KYC checks won’t solve this.

TN HB 2502 is not just a regulation story.

It’s a preview of what happens when finance fragments at the state level while money becomes programmable and borderless.

For banks and fintechs, the litigation phase itself becomes operational risk.

They can’t wait years for courts to decide.

They need infrastructure that adapts in real time.

This is where AI-native trust infrastructure becomes critical:

- dynamic compliance logic that updates instantly across jurisdictions

- detection of “state-hopping” and geo-arbitrage behavior

- behavioral intelligence across fiat, wallets, neobanks, and stablecoins

- sequence-based anomaly detection instead of static rules

The moment one state introduces friction, users reroute behavior elsewhere.

That creates a fragmented regulatory environment too complex for manual systems to manage.

Which means:

Trust intelligence becomes infrastructure.

Exactly why we built @KnightIntelco 🫡

#TennesseeHB2502 #CrossBorderTax #CrossBorderPayments #Fintech #LegalTech #RegTech #Compliance #AML #KYC #FraudPrevention #AI #AIInfrastructure #Stablecoins #DigitalIdentity #Web3

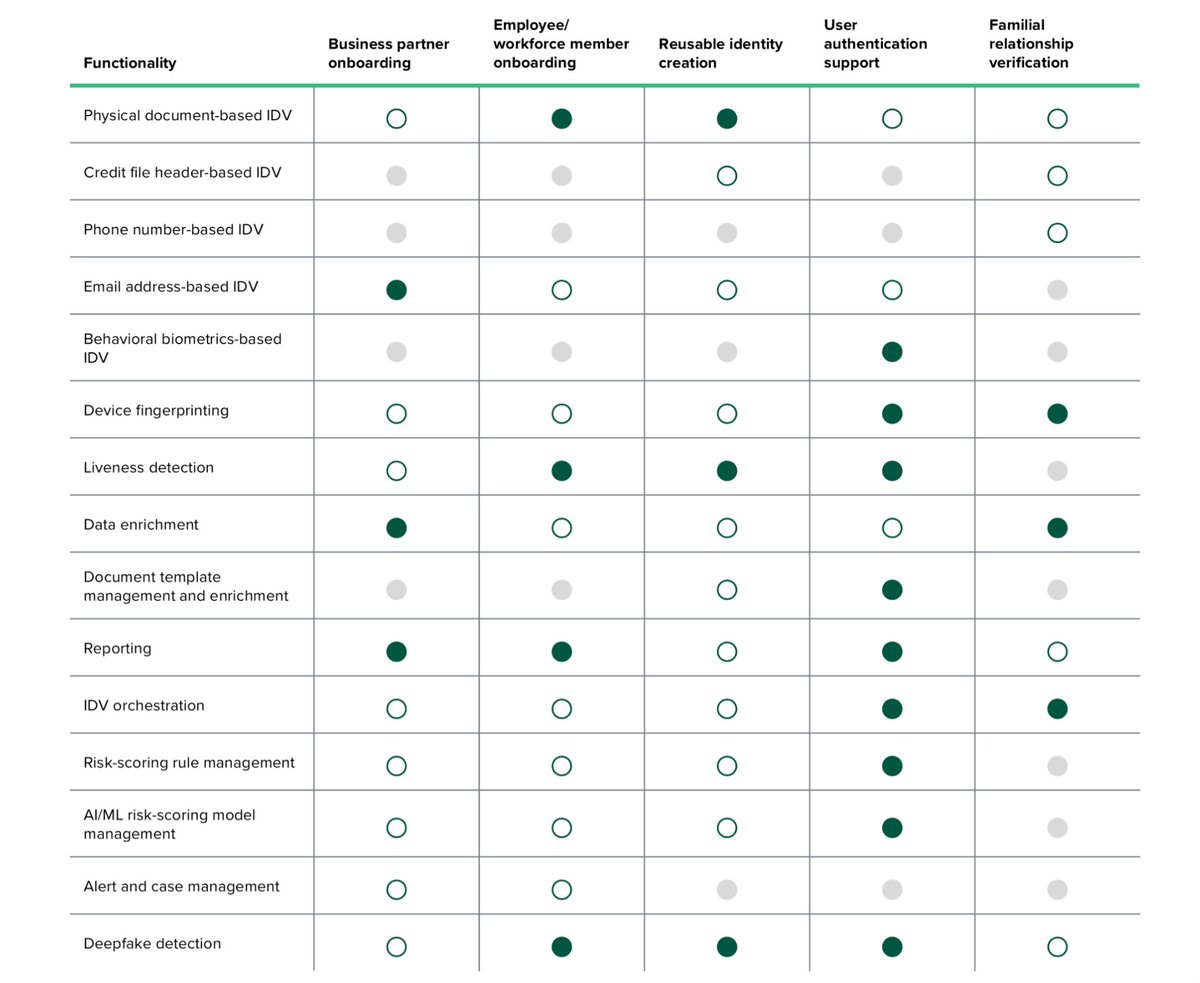

The market is ripe for a new KYC provider… or are KYC providers slowly becoming a one-trick pony? 🐴

The latest #Forrester Identity Verification revealed something interesting:

We now have 30+ KYC/IDV providers competing for essentially the same market.

Almost everyone now offers:

✅ liveness detection

✅ reusable identity

✅ AI/ML risk scoring

✅ orchestration

✅ device fingerprinting

✅ onboarding automation

✅ fraud monitoring

The biggest selling point now?

Convenience.

Faster onboarding.

Less repetitive KYC.

Better UX.

Fewer onboarding drop-offs.

Cool.

Amazing for users.

But what about financial institutions operating in an era of:

deepfakes

synthetic identities

AI-generated documents

mule account networks

agentic fraud

Because while onboarding UX improved, fraud evolved exponentially faster.

#Forrester itself highlights that the industry’s biggest challenge is defending against deepfakes, genAI-driven fraud, and fragmented compliance systems operating across siloed infrastructure.

Today, fraudsters can scrape:

selfies,

voice recordings,

social media videos,

and public data

to generate increasingly convincing synthetic identities at scale.

Which is why we started thinking differently at Knight Intel.

Instead of relying purely on uploaded PDFs and isolated onboarding flows, we’re building API-native trust infrastructure connected directly to live financial systems and open banking rails.

Meaning verification no longer asks:

“Does this selfie and passport look real?”

It starts asking:

✅ Does this banking relationship make sense?

✅ Does transaction behavior align?

✅ Does account ownership stay consistent?

✅ Does this identity behave like a legitimate financial participant over time?

That changes the economics of fraud dramatically.

Because now fraudsters don’t just need a fake passport.

They would need to simulate:

real banking connectivity,

transaction history,

behavioral continuity,

financial consistency,

and cross-jurisdiction legitimacy simultaneously.

That is exponentially harder to fake.

The result?

✅ onboarding reduced from 2–5 business days to under 10 minutes

✅ repetitive KYC flows reduced by 60–80% across connected ecosystems

✅ lower manual compliance review costs through API-native verification

✅ stronger fraud detection through live banking signals instead of static documents

I am very so sorry to the fraudsters,

But we may have a NEW SHERIFF in town. ⛓️👮♂️

and its name is @KnightIntelco 😎

#KYC #KYB #AML #FraudPrevention #IdentityVerification #DigitalIdentity #CyberSecurity #Fintech #FintechStartup #Ai #Aistartup #web3 #vc #CrossBorderPayments #FinancialCrime #Blockchain

Honored to be selected as a Mentor for @ETHGlobal NYC this June 🗽🍎

Repping Southeast Asia in the Ethereum Ecosystem and excited to share everything we’ve learned building @KnightIntelco around cross-border finance, trust infrastructure, and how compliance, identity, and money travel across jurisdictions.

Inviting top builders, hackers, and founders, especially those building:

- neobanks

- stablecoin infrastructure

- identity / KYC layers

- AI agents + finance

- compliance protocols

- cross-border payment rails

- fintech x crypto infrastructure

Come say hi and let’s jam on the future of financial infrastructure! 🏦

apply here: https://t.co/pO25j28MWb

See you in NYC. Power to the builders ✊

#ETHGlobal #Ethereum #Web3 #Fintech #Crypto #Stablecoins #AI #CrossBorderPayments #NYCTechWeek #ETHGlobalNYC #WomenInTech #WomenInWeb3 #Blockchain #AIInfrastructure

Web2 finance optimized for surveillance. Web3 overcorrected to anonymity.

Both failed in the same way: cross-border transactions & the agents of the next decade.

Knight's perspective on Web2, Web3, & AI as the next architecture is outlined here↓

https://t.co/UkyROsyuz9

Tokenization is solved. Verification is not.

Knight powers both sides of the RWA transaction — on-ramp and off-ramp.

We verify the asset. We score the investor.

Across jurisdictions. Across platforms.

The chain proves the asset.

Knight proves the humans.

If you're building a category-defining startup, you don't sell to the market.

You educate the market about the dragon you're slaying. 🏹🐉

Ours is a #fintech $290 trillion cross-border payments industry running on trust infrastructure designed in 1899.

@KnightIntelco now has a Google AI-generated knowledge panel.

Type it in your search bar and Google's AI will explain what we're building (without us ever submitting a single word).

No PR agency. No media budget.

No SEO team.

Just a solo founder educating the market one article at a time until even the algorithms understood the vision.

When an AI can explain your startup better than most humans can, the category is landing.

Marketing done right. 💯😉

#foundermode #ai #google #googlesearch

1.4 billion people are financially invisible.

Not because they aren't trustworthy. Because the financial system wasn't designed for the modern earner.

Move countries. Switch platforms.

Knight makes your financial identity verifiable anywhere.

Be bankable beyond borders. ✈️🌐

#a16zcrypto just mapped the future of global finance. But they also named the gaps.

And who bridges those gaps?

Let's find out.

1. The Banking Choke Point

#a16z describes banking as the layer "where crypto-native financial services hit a wall." Bank connectivity companies are building the translation layer between stablecoin infrastructure and legacy systems.

But translation without trust verification is just plumbing without a filter. Who verifies that the sender is compliant, the receiver is legitimate, and the transaction meets regulatory requirements across BOTH jurisdictions — in real time?

@KnightIntelco That's who.

2. The Liquidity Last-Mile Problem

Stablecoin liquidity between local fiat currencies remains thin, especially in emerging markets. FX providers like OpenFX and regional exchanges are closing the gap.

But liquidity without trust is just money moving blindly. Who ensures that each counterparty across every corridor is verified, compliant, and not a sanctions risk — continuously, not just at onboarding?

@KnightIntelco That's who.

3. The Institutional Privacy Paradox

Institutional networks need "programmability and privacy without surrendering compliance frameworks." Regulated entities need to prove compliance claims without exposing full customer data.

Who enables selective disclosure — proving a customer meets AML requirements in jurisdiction B without revealing their complete financial history from jurisdiction A?

@KnightIntelco That's who.

4. AI Agents Without a Trust Layer

AI agents are converging with stablecoin rails to "disintermediate the transaction." Autonomous systems moving funds, executing FX, managing treasury across borders.

But an AI agent transacting in global finance without a trust profile is a compliance nightmare. Who authorized it? Under which jurisdiction? What behavioral history validates it? Who attests it's auditable?

@KnightIntelco That's who.

5. The Credit Layer Needs Trust

On-chain credit is described as "the second and perhaps more consequential act." Lending against real assets. Working capital for underserved markets.

But credit requires trust profiles. Not static scores from one jurisdiction. Dynamic, longitudinal behavioral intelligence that travels across borders, platforms, and financial ecosystems.

@KnightIntelco That's who.

6. Dollar Access at Scale

"Every stablecoin wallet holding dollars is a new node in the dollar-based financial system." Billions gaining dollar access for the first time.

But regulators won't allow unbounded dollar access without a trust layer. The GENIUS Act proves regulation follows adoption. Who provides the verification infrastructure that keeps dollar access open, compliant, and privacy-preserving before regulators shut it down?

@KnightIntelco That's who.

7. The Convergence Gap

Fintech neobanks and crypto wallets are converging into unified financial applications. But convergence without standardized trust fragments identity across every platform.

A user verified on one platform starts from zero on another. Who builds the interoperable trust layer that makes verified identity reusable and portable across the entire stack?

@KnightIntelco That's who.

--

a16z mapped every layer of the new financial stack.

Rails. Issuers. Liquidity. Banking. Applications. Credit.

At every junction, the same unnamed gap appears.

The infrastructure to move money is being built.

The infrastructure to TRUST the movement isn't.

We're building that layer.

AI-native. On-chain anchored. Provider-agnostic.

@a16zcrypto

Knight's trust attestation layer will be built on Ethereum.

Powered by @eas_eth

Your identity stays private.

Your trust travels everywhere.

Selective disclosure via Merkle proofs.

AI-native. On-chain anchored.

The trust layer for cross-border finance is coming🏇

@ethereum