Liquidity provisioning on Pact Swap just got a whole lot more efficient.

Now with Partial Order Taking, small orders can now tap into much larger LP positions seamlessly.

It’s no longer all-or-nothing. It’s constant, fluid execution.

Better fills. Zero waste. Cross-chain trading at its peak. ⚡️

Out of the last 19 weekends:

- 10 pumped into Sunday

- 4 dumped

- 5 had no directional movement

Saturdays are usually slow, while late Sunday is when volatility picks up.

Every weekend that dumped led to further $BTC downside during the following week, and every weekend that pumped eventually reversed.

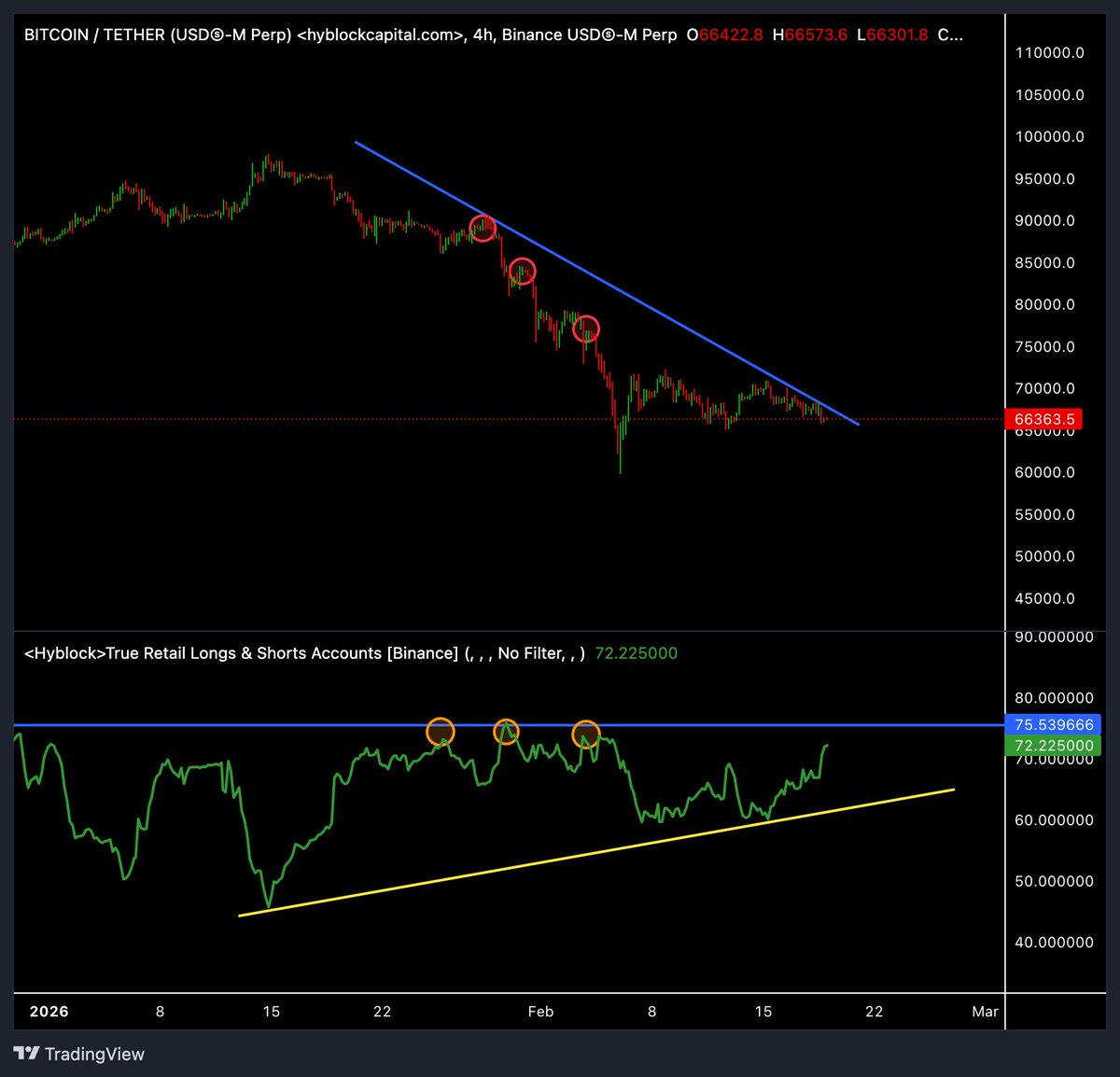

$BTC

Price making lower highs since $98K. Yet retail is making higher lows in Long Positioning since the January capitulation.

They averaged down at $88K. Again at $78K. Again at $68K. Getting more bullish with every leg down.

Every peak in their Long Positioning over this period has been followed by a flush. They reload, price drops, they reload again, price drops again. The pattern hasn't broken once.

72% of retail accounts are long right now. Into a descending trendline with no structural reversal.

Either they're catching the bottom perfectly for the first time ever, or they're building the liquidation pool for another leg down.

The end of profitable airdrop farming ≠ the end of Perp DEXs

Let’s separate two narratives that people keep mixing up:

🔸 The airdrop farming narrative

🔸 The perpetual DEX adoption narrative

I think the first one is getting exhausted.

The second one is just getting started.

1️⃣ The market reality (CEX vs DEX, in numbers)

- CEXs still dominate ~85–90%+ of total crypto derivatives volume

- Binance alone does ~$40B+ per day in perps

Total CEX derivatives: $300B–$400B+ daily (depending on the day)

Meanwhile:

- Perp DEXs do roughly $15B–$25B daily in normal conditions

Even in peak moments, DEXs are still a minority of total volume

Hyperliquid, the #1 DEX, does ~$5–6B daily → still tiny vs Binance alone

👉 Translation: the addressable market for perp DEXs is massive.

They don’t need hype. They just need flow to migrate.

2️⃣ The airdrop farming trade is overcrowded

Look at what’s happening:

- New perp DEXs launching on every chain

- Most compete on points and incentives, not product quality

- A huge % of “users” are actually farmers, not organic traders

This creates:

- Inflated activity

- Short-term usage

And a lot of mercenary capital that leaves once incentives end

We’ve seen this movie many times in DeFi.

3️⃣ The real top signal: the “excuse phase”

A narrative usually doesn’t die when returns go down.

It dies when excuses start:

“Market conditions were bad”

“Too many people farmed it”

“The distribution wasn’t fair”

“This one was an exception”

“Next one will be better”

That’s rarely an exception.

That’s the new normal kicking in.

4️⃣ Why Hyperliquid is the perfect contrast

Hyperliquid:

- Had 2 point campaigns

- Used a simple, linear distribution

- No exotic rules

- No hidden mechanics

And still became one of the biggest airdrops in crypto history.

That wasn’t magic.

That was:

- Right timing

- Explosive growth

- And an underfarmed narrative

As more DEXs launch, with worse market conditions and way more farmers, the average airdrop will NOT cover:

- Trading losses

- Fees

- Opportunity cost

- Time spent farming

When people start losing money net-net → the complaints explode → the meta is over.

5️⃣ The key distinction most people miss

✅ Profitable airdrop farming can die

❌ That does NOT mean perp DEXs die

These are two completely different things.

Even today:

🔸 DEXs = ~5–15% of perp volume most of the time

🔸 CEXs = ~85–90%+ of perp volume

So the upside for real adoption is still huge, even if farming returns go to zero.

6️⃣ Why structural migration still makes sense

Long-term forces pushing users from CEXs → DEXs:

- More regulation and restrictions on CEXs

- Custody and counterparty risk awareness

- Demand for permissionless access

- Better on-chain UX and execution (Hyperliquid shows this clearly)

- More capital living natively on-chain

But let’s be honest:

Users won’t go to “random chain #58 perp DEX”.

They will concentrate in:

- The most liquid venues

- The safest and simplest UX

- The platforms that feel CEX-like in performance

- The top winners (Hyperliquid + maybe a few others)

Liquidity and trust always concentrate.

7️⃣ The most likely outcome

🪙 The airdrop farming gold rush fades

😤 The complaint cycle increases as returns drop

🧟 Many low-quality perp DEXs lose activity after incentives end

🏆 A few winners keep growing based on real usage, not points

In short:

The speculative meta dies. The infrastructure stays.

8️⃣ Final thought

Perpetual DEXs are no longer a toy narrative.

They’re a real, growing slice of the derivatives market.

But the era of:

“Just farm points and get paid”

is probably close to over.

That’s not bearish.

That’s what maturation looks like.

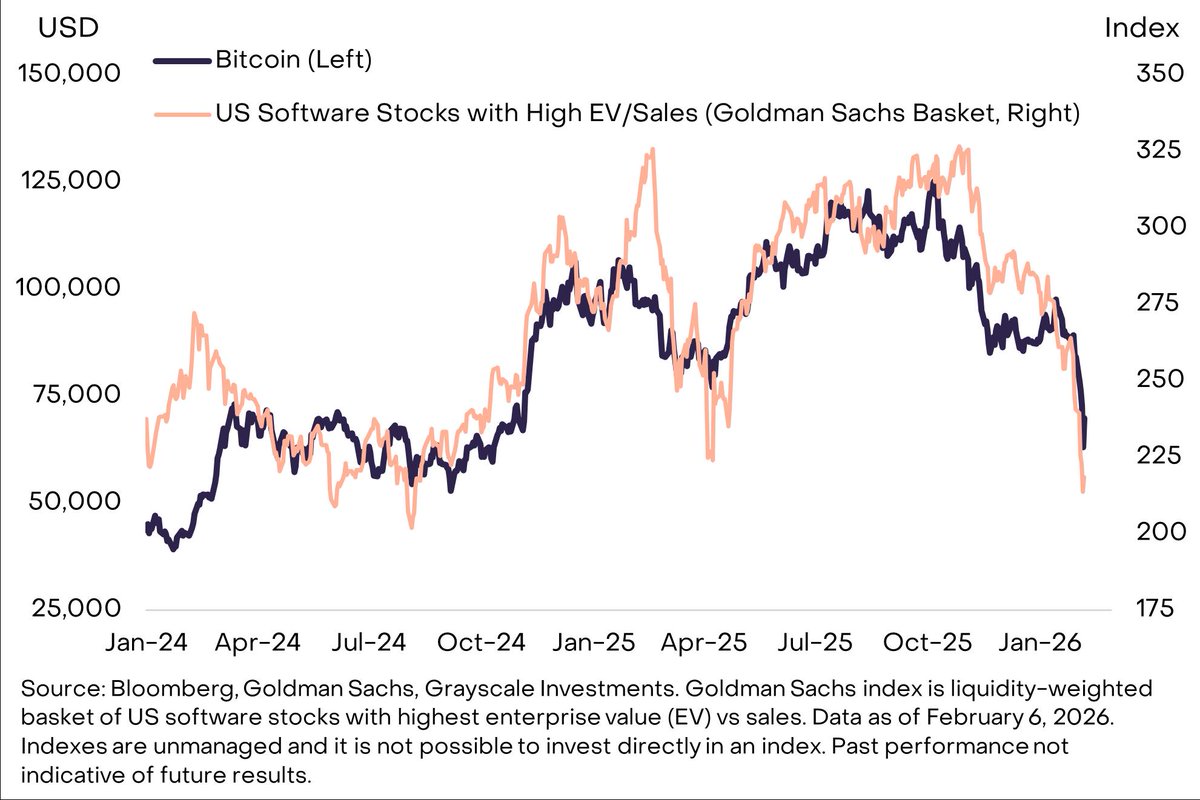

1.The Private Lending Crisis as a Hidden Cause of the Decline

A Grayscale chart shows a tight correlation between software stocks and Bitcoin since early 2024. This relationship points to the shared fundamental forces driving both markets over the past two years.

Help shape WalletConnect Pay by participating in a product research survey.

We’re building crypto payments - and we want to deliver the best UX.

- For WCT + stablecoin holders

- Discord role + WCT for meaningful insights

Join the AMA to learn more!

https://t.co/NeGUwQJxU8

4."Bitcoin has a strong correlation with IT stocks due to their common source of funding—private debt." The sector has been under stress since 2025, which explains the deviation of the cryptocurrency price from global liquidity charts,” notes Dan, head of research at Coinbureau.

1.The Private Lending Crisis as a Hidden Cause of the Decline

A Grayscale chart shows a tight correlation between software stocks and Bitcoin since early 2024. This relationship points to the shared fundamental forces driving both markets over the past two years.

3.Investor concerns are heightened by the development of AI systems. The emergence of advanced models and automated coding tools could reduce demand for traditional software. This threatens companies' regular revenues, leading to an increased risk of loan defaults.

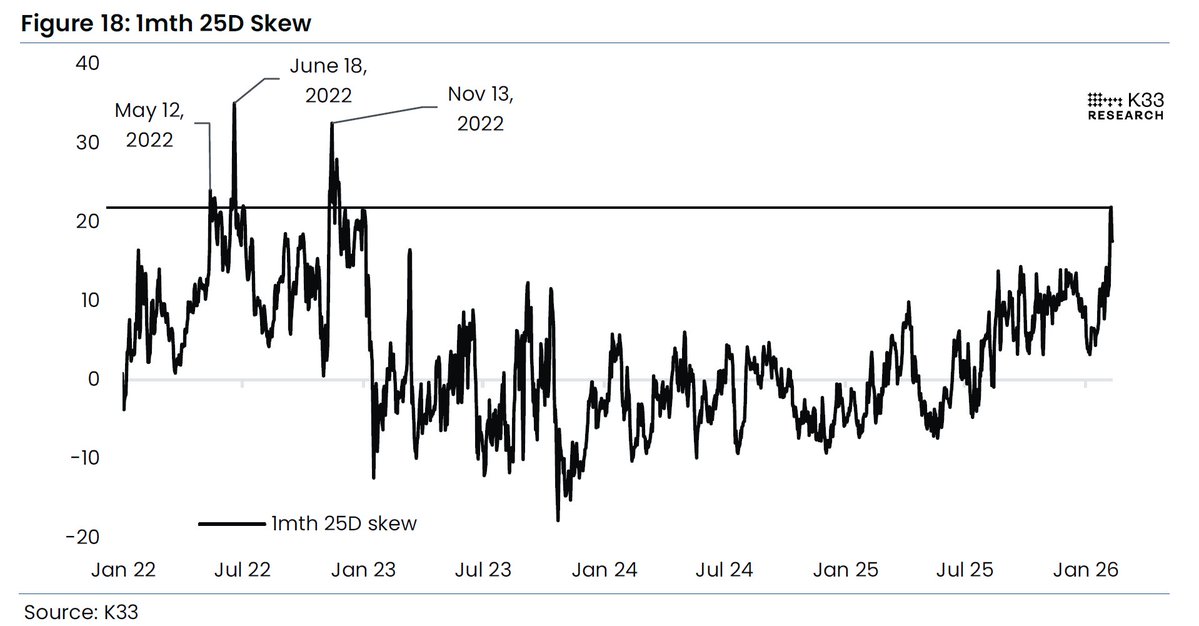

Bitcoin Option Skew is in Deep Bear Market Territory.

Skew measures the implied volatility of Puts vs. Calls. The higher the skew, the more buyers are paying for Puts (downside) relative to Calls (upside).

The higher the skew, the more people are willing to pay for downside protection.

The last time it was this high, was during FTX / Luna / 3AC collapse.

Fear is still permeating through.

🚨 $BTC PRICE ACTION SCENARIO FOR THE NEXT 12 MONTHS!

You are NOT ready for this:

1. Right now we are in a sideways consolidation phase.

2. Next, we will see a final impulsive move down.

3. The end of the bear trend will be marked by a Falling Wedge pattern that breaks to the upside.

4. This will start a new bullish trend.

Reminder: a new 4-year cycle has started – 2026-2027-2028-2029.

In 2029, $BTC will set its final ATH and that will complete the cycle.

TURN ON NOTIFICATIONS, FOLLOW ME AND BOOKMARK THIS!