For the Fed, May’s inflation report settles nothing

• Core was mild, but a soft monthly print buys less when it's drowned out by a hot headline and a "boomier" demand backdrop. The case for patience now needs a run of cool reports, not one.

• The forces pushing up prices have changed character. No longer just tariffs but the energy shock, plus an AI buildout and wealth effects letting firms keep passing costs through. It's harder to wave that off.

• Net for Warsh's first meeting next week: it leaves the Fed's recent hawkish lurch intact without forcing it any hawkier today. The debate still runs from hold-longer to whether a hike belongs back on the table, unthinkable when the year opened with markets pricing cuts. https://t.co/2zsY63glno

Good news just became bad news again.

Friday’s NFP report didn’t just beat expectations — it broke the market’s entire short-term narrative.

The U.S. economy added 172,000 jobs in May, more than double the 80,000 consensus. March and April were revised higher by a combined 93,000. Unemployment held at 4.3%, wages rose 0.3% MoM / 3.4% YoY, and this was the fourth jobs print above 150K in five months.

In a normal cycle, that would be bullish.

More jobs. More income. More spending. More growth.

But this is not a normal cycle.

This is an inflation-led, Fed-sensitive regime — and in that regime, strong data is not read through the “growth” lens first.

It is read through the Fed lens.

And the Fed lens said: fewer cuts, higher-for-longer, and maybe even hikes.

That is why the reaction was so violent:

• Nasdaq had its worst session since April 2025

• Semiconductors lost more than 10% in one day

• S&P 500’s nine-week winning streak ended

• 2Y yield hit a new 52-week high

• 10Y yield jumped to 4.54%

• Gold fell sharply

• Market-implied odds of a 2026 Fed hike jumped from 25% to 52%

This was not just a red Friday.

This was a full repricing.

The market had spent weeks building a soft-landing narrative: inflation cooling, Fed pressure easing, risk appetite returning, AI momentum carrying equities higher.

Then NFP landed and reminded everyone that the labor market is still too firm for the Fed to comfortably pivot dovish.

But the details matter.

The headline was strong, yet the composition was much less impressive.

Two sectors — leisure/hospitality and local government — accounted for roughly 73% of the hiring. Strip those out, and the rest of the economy added only about 47,000 jobs.

Financial activities actually lost jobs.

Long-term unemployment now represents 27.5% of all unemployed workers, the highest share of this cycle.

So the labor market is not exactly booming everywhere.

It looks more like a low-hire, low-fire economy:

Stable if you already have a job.

Difficult if you are trying to get back in.

Strong enough to keep the Fed cautious.

Uneven enough to make the real economy feel worse than the headline suggests.

That is the uncomfortable setup.

The Fed will see the headline first and the details second. Markets know this. That is why yields moved, the dollar firmed, gold sold off, and high-duration equity got hit hardest.

The semiconductor sell-off is especially important.

This was not only about NFP. The pressure started earlier in the week when Broadcom failed to raise its full-year AI chip outlook. That shook confidence in the AI trade, then Friday’s rates repricing hit the most crowded, expensive, momentum-heavy parts of the market.

When the cost of capital rises, valuation discipline returns fast.

AI can still be real.

Semiconductor demand can still be structural.

But positioning matters. Multiples matter. Expectations matter.

A great long-term story can still get crushed short-term if the market is over-owned and the macro regime turns against it.

That is what Friday showed.

The bigger lesson:

In inflation-led regimes, markets do not ask, “Is the economy strong?”

They ask, “Will this make the Fed more hawkish?”

That one question explains the entire move.

Same NFP number, different regime, totally different market reaction.

In a growth-scare regime, +172K jobs might have sparked a rally.

In this regime, it ended a nine-week S&P 500 winning streak.

Good news became bad news because the market was priced for relief — and got resilience instead.

The next few weeks will be about whether this was a healthy reset after a 20%+ rally, or the start of a broader unwind in crowded risk trades.

For now, the message is clear:

The Fed is back in control of the tape.

And until inflation risk is fully buried, every strong data print comes with a catch.

#NFP #JobsReport #FederalReserve #Fed #SP500 #Nasdaq #Semiconductors #AI #Markets #Macro #Investing #Trading #Bonds #Yields #Gold #RiskAssets

Not financial advice.

Bloomberg:

“The world has burned through oilinventories at a record speed as the Iran war throttles flows from the Persian Gulf…

The rapidly shrinking stockpiles mean that the risk of even more extreme price spikes and shortages is getting ever-closer, leaving governments and industries with fewer options to cushion the impact of the loss of more than a billion barrels of supply, two months into the near-closure of the Strait of Hormuz.”

#economy #oil #markets #middleeastwar

Rick Rieder isn’t an academic or a headline economist…he’s a markets person who’s spent his entire career watching where things actually break. At BlackRock, he runs global fixed income and sits at the center of rates, credit, and multi asset allocation decisions that move trillions. Before that, he came up through Lehman Brothers and later founded R3 Capital during the financial crisis, which BlackRock acquired. That matters because his instincts were forged in moments when liquidity disappears and refinancing risk suddenly becomes the story.

He’s known less for grand theories and more for understanding transmission and how policy decisions flow through funding markets, credit spreads, housing, and the cost of capital. He’s the kind of investor who cares whether the pipes are shaking, not whether the model looks clean.

Where He Stands On Policy And Why It Resonates Now

On monetary policy, Rieder tends to be pragmatic. He’s generally argued that once rates cross from restrictive into outright constrictive, they start doing damage..especially to housing, small businesses, and credit!dependent parts of the economy. That’s why he’s been more open than many to rate cuts in this phase of the cycle. Not because easy money is good, but because tightening into a refinancing wall is how accidents happen.

On fiscal policy, he’s more measured. You don’t hear him cheering deficits, but you do hear him acknowledge reality that when debt loads are large, the cost of capital matters enormously. His focus is usually on whether policy..monetary or fiscal is making the system more fragile at the margin.

On crypto, his tone has been unusually sober for someone from traditional fixed income. He’s described Bitcoin as durable, has compared it favorably to gold as a store of value, and has treated it as something that belongs in modern portfolios..not as a trade, but as a structural asset. That’s less about hype and more about recognizing how markets evolve.

Why His Name Keeps Coming Up

It’s not hard to see why someone like Trump would be drawn to Rieder. Trump has always favored operators over bureaucrats, people who’ve run real money and understand markets from the inside. Rieder fits that mold..a Wall Street winner, comfortable with scale, and openly critical of policy staying too tight for too long. Picking someone like him would signal a shift toward growth first thinking while still giving markets a sense of credibility.

The bigger point, though is Rieder’s speciality is management during times of stress. He’s spent decades managing through moments when credit turns, liquidity dries up, and policy mistakes get exposed. In a cycle where refinancing risk, credit strain, and term premium are quietly becoming the main characters, that skill set suddenly looks very relevant.

Ray Dalio: "Global monetary order is breaking."

Dalio thinks the US and the allies are losing trust in one another, so central banks don't want to hold the US bonds.

This is why commodities are skyrocketing, and it's not going to reverse anytime soon.

His advice? Buy gold.

Understating depreciation by extending useful life of assets artificially boosts earnings -one of the more common frauds of the modern era.

Massively ramping capex through purchase of Nvidia chips/servers on a 2-3 yr product cycle should not result in the extension of useful lives of compute equipment.

Yet this is exactly what all the hyperscalers have done. By my estimates they will understate depreciation by $176 billion 2026-2028.

By 2028, ORCL will overstate earnings 26.9%, META by 20.8%, etc. But it gets worse. More detail coming November 25th. Stay tuned.

UK long-dated bond yields are off their highest levels (chart), but they have settled in a range that significantly increases debt-servicing costs for both new issuance and rolled-over debt.

This is now a common phenomenon in advanced economies, which, for countries like Britain and France, comes at a particularly delicate moment for fiscal accounts and, by implication, domestic politics.

#economy #markets #deficits #debt #france #uk

Average Annual US Inflation Rate over the last...

1 Year: 2.9%

3 Years: 3.1%

5 Years: 4.5%

10 Years: 3.1%

Meanwhile, the Fed is expected to cuts interest rates 3x this year (Today, October, December) and 3 more times next year.

Their 2% inflation target is a complete farce.

The rise in very long-term government bond yields (red) is happening everywhere. There's idiosyncratic trouble spots like Japan, France and the UK, but what's playing out is far bigger than that. Fiscal policy globally has been too loose for too long. That has consequences...

Strong retail sales report today, although probably somewhat distorted by the end of the de minimis tariff exemption on August 29 and higher overall inflation. The key question going forward is whether sales can hold up on the back of slower real income growth. I am skeptical.

The quality of CPI inflation data continues to deteriorate:

In August, 36% of CPI prices were estimated, up from 32% in July.

Normally, BLS calculates CPI inflation by gathering ~90,000 monthly price quotes across 200 product and service categories.

When price data is missing, the BLS fills the gaps with estimates, which usually make up ~10% of all data points.

The share of estimates has rapidly surged over the last few months.

As a result, CPI numbers are becoming less accurate and less reflective of real consumer costs.

Confidence in the economic data is eroding.

This is a key insight into the US economy right now:

The bottom 80% of households are just barely keeping their spending up with inflation.

Meanwhile, the top 20% are doing just fine and growing their spending.

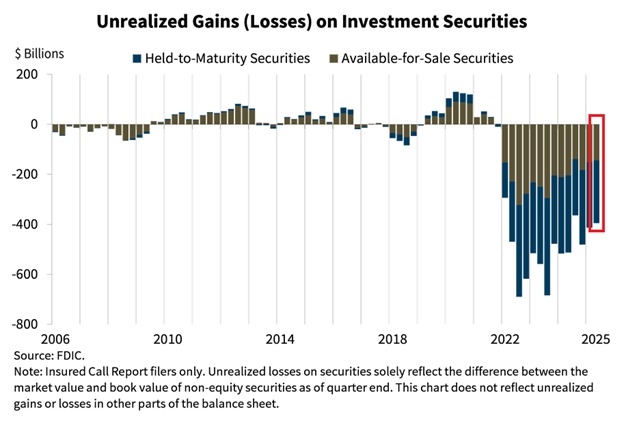

BREAKING: Unrealized losses on investment securities for US banks reached $395.3 billion in Q2 2025.

This is ~6 TIMES higher than at the peak of the 2008 Financial Crisis.

This also marks the 13th consecutive quarter of losses as interest rates remained elevated.

Meanwhile, the number of banks on the FDIC Problem Bank List reached 59 in Q2 2025, or 1.3% of the aggregate.

Unrealized losses at banks continue to pose a significant risk.

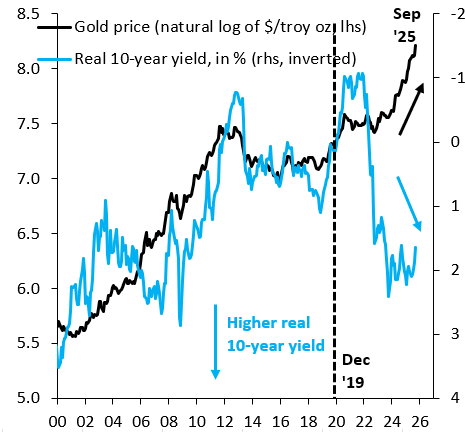

The world is running out of safe havens. Japan used to be a safe haven, but the sharp rise in long yields means it isn't any more. Germany is also seeing an erosion of its safe haven status. Switzerland is tiny, so you can't hide there. All this means gold prices are going crazy.