Multi-assets strategist with actionable trading ideas based on global macro trend. Managed international institutional & High Net Worth individuals’ portfolios

Volatility is returning—and 2026 will reward those who understand cycles, not narratives.

In this Monthly Meditation, @TheMacroButler lays out 10 clear, historically grounded forecasts to help you position ahead of a turbulent year.

https://t.co/POdjf6P6ld

🚨 OIL PRICE MANIPULATION OR BIGGEST ENERGY MISPRICING OF 2026? 🚨

Everyone is celebrating lower #oil prices...

Meanwhile:

⛽️ Global #inventories are shrinking

🚢 #Shipping disruptions are growing

🇨🇳 #China isn't even back in the market yet

🛢 Strategic reserves are being drained

And somehow we're supposed to believe oil is headed lower?

When the fundamentals and the price disagree, one of them is lying.

🎥 Watch until the end to understand why the next move in oil could shock the market.

Learn to Earn with The Macro Butler Financial Academy: https://t.co/rSi9cfTYxA

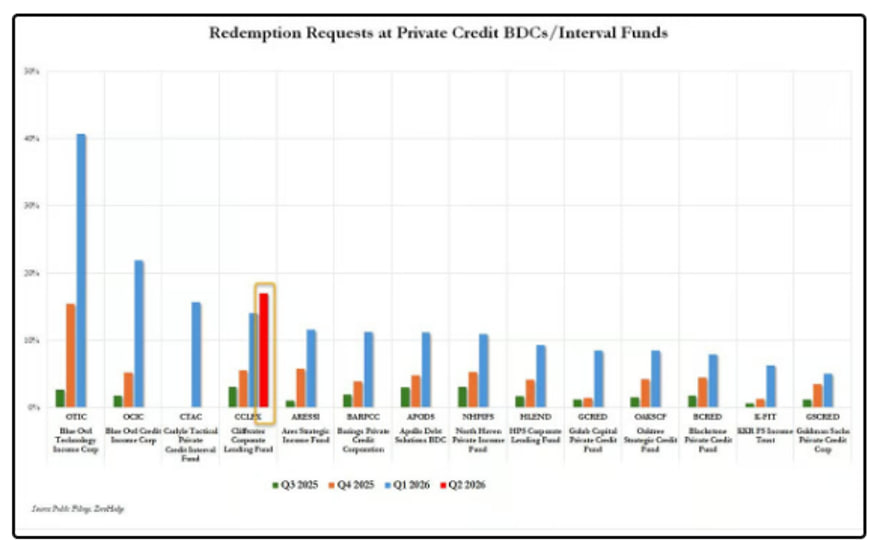

As anyone possessing even a passing acquaintance with common sense could have predicted, the private credit gates are swinging shut once again. After a wave of redemption requests overwhelmed nearly every marquee private credit fund in Q1, Q2 is shaping up as a rerun. Just days after Cliffwater capped withdrawals at 5% despite investors requesting 17% back, @blackstone has now joined the club, limiting redemptions from its $79 billion flagship private credit fund after investors sought to pull 10% of assets. Blackstone says redemption requests slowed toward the end of the tender period. Conveniently, that claim will only be testable once the next redemption figures arrive. Until then, investors can take comfort in knowing that the exit door remains available—just at half speed.

https://t.co/2dloMF9UkC

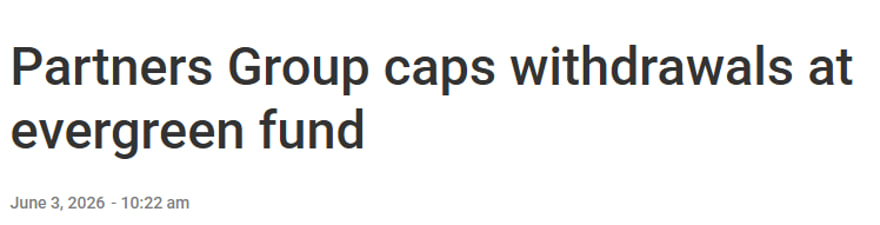

The redemption wave hitting Partners Group comes at an awkward time. Just weeks after dismissing short-seller allegations that some evergreen funds may be significantly overvalued, the firm now finds itself imposing withdrawal limits as investors rush for the exits. What began as a private credit problem is increasingly looking like a broader private markets phenomenon.

The usual suspects—@Apollo, @KKR_Co , @BlackRock , @BlueOwlCapital , #Cliffwater, and now Partners Group—have all discovered that "evergreen" liquidity works best when investors remain evergreen themselves. Cliffwater's latest redemption requests jumped to 17%, forcing another 5% gate, while concerns over credit quality, AI-disrupted software borrowers, and asset valuations continue to spread across the sector. Partners Group insists the Grizzly report is largely irrelevant and that valuations remain independently verified. Perhaps. But when investors start questioning both liquidity and valuations simultaneously, the distinction quickly becomes academic.

So, while private markets tighten the gates and public markets trim valuations, central banks are doing what they’ve always done: quietly buying insurance and calling it “diversification.”

While private equity gates the exits and #IPO s quietly get repriced downward, the “barbaric relic” continues to do what it always does—behave like a very expensive alarm system for monetary anxiety. According to the latest @GOLDCOUNCIL update, central banks flipped back into net buyers in April, adding about 17 tons after March’s sharp sell-off (~30 tons), the largest in years and driven largely by Turkey.

https://t.co/zC1pZAUh4G

Even with the recent rebound, central bank demand is still running well below last year’s average pace—more “supportive bid” than “melt-up engine.” And the real driver of last year’s surge—relentless ETF inflows that helped propel gold above $5,000—has simply not returned. Instead, ETFs remain net sellers, draining liquidity rather than amplifying it. That momentum bid hasn’t vanished—it has just migrated. From bullion vaults to semiconductor fabs and memory chips, the chase for performance has clearly changed asset class.

The broader message is becoming harder to ignore: after years of being sold as smooth, low-volatility alternatives, private markets are now discovering that liquidity tends to disappear precisely when everyone starts looking for it at the same time.

After private credit introduced investors to the exciting world of redemption gates, private equity has decided not to miss the trend. @partnersgroup has capped withdrawals from its $8.6 billion Global Value fund after redemption requests nearly doubled the amount investors were actually allowed to withdraw. Apparently, "evergreen" still means liquid—just not necessarily when investors want their money back. As usual, management insists the gates are there to protect long-term investors, which is industry shorthand for reminding clients that private assets are, in fact, private and illiquid. The irony is that the fund reportedly still holds substantial liquidity and access to additional credit lines, yet redemption pressure from increasingly nervous private wealth clients was enough to trigger restrictions.

https://t.co/7Tg2HQ3jvR

The redemption wave hitting Partners Group comes at an awkward time. Just weeks after dismissing short-seller allegations that some evergreen funds may be significantly overvalued, the firm now finds itself imposing withdrawal limits as investors rush for the exits. What began as a private credit problem is increasingly looking like a broader private markets phenomenon.

The usual suspects—@Apollo, @KKR_Co , @BlackRock , @BlueOwlCapital , #Cliffwater, and now Partners Group—have all discovered that "evergreen" liquidity works best when investors remain evergreen themselves. Cliffwater's latest redemption requests jumped to 17%, forcing another 5% gate, while concerns over credit quality, AI-disrupted software borrowers, and asset valuations continue to spread across the sector. Partners Group insists the Grizzly report is largely irrelevant and that valuations remain independently verified. Perhaps. But when investors start questioning both liquidity and valuations simultaneously, the distinction quickly becomes academic.

In a nutshell, the ISM Services PMI rose on surging new orders, but weakening employment, shrinking backlogs, and rising inflation suggest the celebration may be ending before the bill arrives.

The ISM Services PMI rose to 54.5 in May, suggesting the economy remains wonderfully healthy—provided one only looks at the headline number. New orders surged and lifted the index higher, but beneath the surface the picture was less inspiring. Export orders softened, order backlogs declined, employment contracted further, and inventories continued piling up. Meanwhile, input costs accelerated to their highest level since 2022, reminding everyone that inflation has not yet received the memo about cooling down. In short, businesses appear to be ordering more, hiring less, paying higher prices, and accumulating inventories—a combination that may make May look stronger than June eventually turns out to be.

In a nutshell, EuroStan inflation has climbed back above 3%, proving once again that central bankers may print optimism, but they can't print disinflation.

In a development that will surprise absolutely nobody outside the economics profession, EuroStan ‘CPLIe’ climbed above 3% for the first time since September 2023, making next week's @ecb rate hike look about as optional as paying taxes. Headline CPI rose to 3.2% year-on-year in May, while core inflation accelerated to 2.5% and services inflation surged to 3.5%, its highest level in six months. Energy prices did much of the heavy lifting, but the persistence of services inflation will provide ample ammunition for ECB hawks eager to remind markets that "transitory" remains the most expensive word in central banking. Despite economists assuring everyone that inflation will eventually drift back toward target, the latest data suggest the ECB's battle against rising prices is proving about as successful as Europe's quest for energy independence.

The result is yet another step toward a future where artificial intelligence remains free, innovative, and closely supervised—purely for your safety, of course.

In a reassuring display of voluntary government oversight, Donald Copperfield signed an executive order allowing AI companies to submit their most advanced models to Washington for review before public release. The arrangement is entirely optional, of course—much like many things that eventually become mandatory. Under the order, frontier AI models may be shared with a growing collection of federal agencies tasked with protecting the public from the risks created by the very technologies they are increasingly eager to monitor. A new AI cybersecurity clearinghouse will scan models for vulnerabilities, while the Pentagon and other agencies accelerate efforts to deploy AI-powered defensive tools of their own.

https://t.co/8B8cF0QhYk

@NourAmache@NourAmache in an increasingly weaponized world #gold will remain the only antifragile asset investors must own to protect themselves against more wars and increasingly reckless governments

The #ISM Manufacturing PMI rose to 54.0 in May, its highest level in four years, proving once again that nothing says "economic resilience" quite like stockpiling goods before the next round of inflation arrives. New orders and production accelerated as companies rushed to secure supplies while oil prices, shipping costs, and raw material expenses remained elevated thanks to the Middle East conflict. Nearly every manufacturing sector expanded, even as survey respondents complained about soaring fuel costs, supply-chain disruptions, and shrinking margins. In other words, manufacturers are still buying today because they are increasingly worried about what everything will cost tomorrow. The good news is that demand remains strong. The bad news is that inflation appears equally determined to participate in the recovery.