🎉 Happy 3 years of Liquity! 🎈

What a journey it's been:

• From pioneering immutable, interest-free borrowing ✅

• To becoming the first protocol to reach $1B within the first 10 days 👀

• To being one of the most forked protocols 😅

A heartfelt THANK YOU to our community for placing your trust in code, decentralization, and immutability 🙏

But the journey is far from over

Liquity v2 awaits, and brings with it a new primitive: user-set interest rates.

Onward!

Liquity v2: Why user-set interest rates are a BOLD move forward 🔵

To date there is no protocol that has created an efficient interest-rate market between borrowers and stablecoin holders.

This is about to change. ⛓️

In DeFi we have:

- Fixed one-time origination fee - e.g. Liquity v1

- Governance based interest rates - e.g. MakerDAO

- Algorithmically controlled interest rates - e.g. crvUSD

All these systems have different trade-offs:

- Fixed rate protocols cannot adjust to high interest rate environments

- Governance can be slow and arbitrary

- Algorithmic controllers create volatile and unpredictable rates.

We’re yet to see a market-driven mechanism….. till now.

Why should you care, and how does Liquity v2 solve this? 🤔👇

In contrast to money markets where there is a significant spread between lenders and borrowers, Liquity v2’s unique user-set interest rate mechanism will enable swift, adaptive adjustments that tighten the disparity between the two. Over time, we anticipate that DeFi interest rates will converge towards the Liquity v2 model, establishing a new standard for borrowing and capital efficiency within DeFi.

To see how user-set interest rates work and why borrowers would want to pay a higher rate than 0%, we first need to understand what keeps Liquity’s stablecoin stable in the first place

A quick lesson in Liquity mechanics👇

In April 2021, Liquity v1 pioneered the first CDP system with a built-in redemption mechanism and introduced a stablecoin with a strong downward peg protection with no dependency on centralized collateral.

The redemption feature allows any LUSD holder to exchange their stablecoins for $1 worth of ETH.

When LUSD is <$1, users can buy it for e.g. $0.99 off the market and sell to the protocol for $1.00.

While this mechanism maintains a hard price floor around $1 (minus fees) through direct arbitrage, it impacts the riskiest borrowers since the redeemed LUSD is used to pay back the loans with the lowest collateral ratio in exchange for an equivalent amount of ETH.

The affected borrowers see their collateral and debt go down by the same value, implying no net loss but a reduced exposure to ETH.

Why has this been an issue? 👇

Due to rapidly increasing market rates in the last few months, borrowing volumes have outweighed the demand for holding LUSD, resulting in excessive selling pressure, and thus redemptions. As a consequence, many LUSD borrowers have increased their collateral ratios to previously unseen levels, just to avoid redemptions.

This has seriously impaired Liquity v1’s ability to offer capital-efficient loans in the current environment of excessively high DeFi interest rates.

Being interest-free in nature and with its fixed-cost and reward system, Liquity v1 has shown to work reliably in low interest environments, and it continues to be a viable option for borrowers in such scenarios. But in high interest rate situations, users tend to seek stablecoins with higher yields.

It has become clear that variable interest rates are better suited to deal with a variety of market scenarios in a sustainable and flexible way. At the same time, we also realize the importance of the redemption mechanism to prevent a stablecoin from losing its peg: many existing stablecoins have suffered from downward peg deviations due to high sell pressure.

Enter the innovation: user-set interest rates 👇

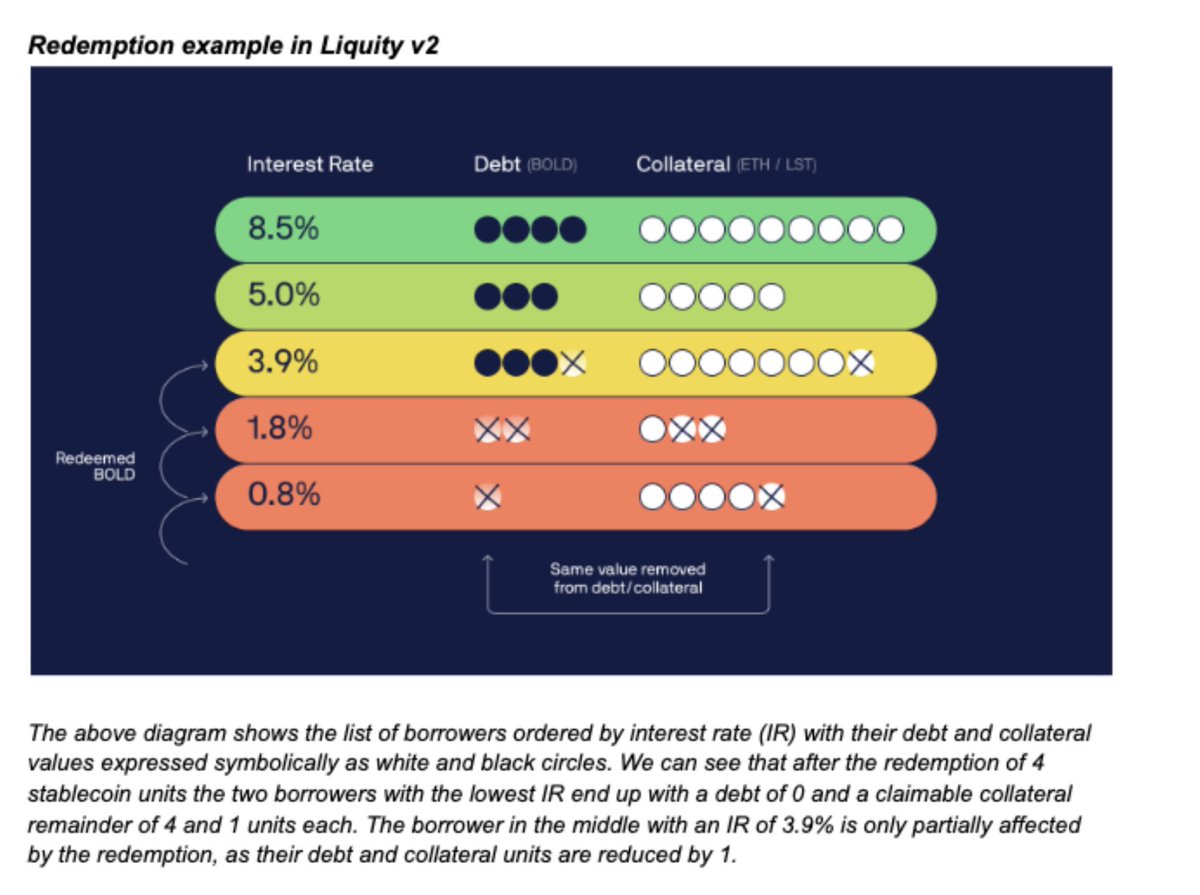

Through user-set interest rates, redemptions can be neatly married with dynamic interest rates: instead of targeting the loans with the lowest collateral ratio, redemptions in Liquity v2 will be performed in an ascending order of individual interest rates.

Borrowers with low interest rates thus have the highest risk of being affected by redemptions. Users can freely manage their redemption risk by adjusting their interest rates relative to their peers (or delegate the management to third parties; more on this below).

Based on the borrowers’ individual risk tolerance, the market will establish a range of individual interest rates. Borrowers willing to risk redemptions may set below-average rates for capital efficiency, whereas more risk averse or “set-and-forget” borrowers may opt for an above-average rate for peace of mind.

As opposed to most existing CDP protocols, the interest revenue in v2 will be used to incentivize stablecoin demand and liquidity autonomously with minimal human governance. For safety and efficiency reasons most of the revenue is funneled to the Stability Pools, incentivizing stablecoin demand as well as protocol solvency.

In addition to that, a sizable part of the revenue is sent to LPs on external AMMs to ensure sufficient stablecoin liquidity as PIL (protocol incentivized liquidity) across multiple pairs. As fees are collected in the form of interest, this ensures a continuous and smoothed flow of incentives to SP and LP depositors.

And this brings us to BOLD ⚫ 👇

In light of this, we’re excited to announce the new stablecoin at the heart of Liquity v2 will be named BOLD. This name mirrors our resolve to pioneer a paradigm shift in DeFi, enabling a market driven mechanism where interest rates are no longer dictated by the few, but chosen by the many. The interest rates set by users’ also influence how BOLD's peg mechanics work ↓

When BOLD trades above $1, borrowers will tend to reduce their rates due to the lower redemption risk. This makes borrowing and leveraging on ETH (and LSTs) more attractive, while holding BOLD becomes less attractive.

Conversely, when BOLD is below $1, borrowers are exposed to a higher redemption risk and are likely to increase their interest rates. Borrowing thus becomes less attractive, while demand for BOLD increases as the interest payments result in higher yield for the stablecoin, pushing its price upward.

Instead of driving collateral ratios to unreasonable levels, user-set interest rates should enable a capital efficient equilibrium between borrowers and stablecoin holders in a fully market-driven manner.

Borrowers will be able to actually benefit from Liquity v2’s attractive loan to value ratios, and get as much funds against the chosen collateral as their liquidation risk tolerance permits.

What does this mean? 🤔 👇

As a borrower, you will be able to choose any interest rate you like, to pay whatever you want. You can also delegate your interest rate to:

1) A manager - a 3rd party which actively and continuously adjusts the rate for a group of users, with a clear goal / rate percentile.

2) A smart contract - an Ethereum contract address autonomously managing the borrow rate for its users following a preset logic.

3) Any EOA - this can be a hot wallet or a friend doing this for you.

In all cases, the only permission this delegate will have is to adjust the interest rate in a predetermined range. Nothing else. 🔷

With this advancement, we expect v2 to offer very competitive borrowing and stablecoin holding rates.

What else are you cooking? 👨🍳 🍚

User-chosen interest rates will be a big leap forward - but this is by no means the only innovation Liquity v2 will ship with.

Stay tuned for our upcoming article which emphasizes the other borrowing enhancements in greater detail, and join our Discord for discussions ✨

Liquity v2 will change the fabric of CDPs in DeFi 🔵🔹

At @EthereumDenver and keen to contribute in any way to the next big DeFi primitive? 🔹

DM, and let's hang ☕️

🚨 another one

And this time on Mainnet 🔵

@blueprintfi_eth are a novel gas-efficient ve (3,3)+ DEX that have integrated both LUSD and bLUSD as assets!

Liquidity providers of either asset can earn LP rewards for 4 different pairs including the LUSD / bLUSD pair 👀

Check it out here:

https://t.co/i2Zyb8NEBe

Why are user-set interest rates a game changer?

Until now, collateralized debt positions had 3 rate-primitives:

- Fixed rate, e.g. Liquity

- Governance set rates, e.g. Maker

- Algorithmic rate, e.g. crvUSD

Now we'll be pioneering another, the 4th primitive: user-set interest rates.

And we think it's the best one to date.

With it, a market driven policy rate is introduced.

And as you know, the market is always right 😉

The protocol taps into the wisdom of the crowd to create a rate which is:

- Adaptive

- Macro-driven

- Reflects individual needs

Additionally, we are bringing Liquity's capital efficiency to full bloom.

👇

How?

By splitting liquidation and redemption risks into separate parameters!

- Liquidations happen when you loan to value exceeds a certain level (eg. 91%)

- Redemptions happen when your interest rate set is too low

What's better, your interest rate can be delegated to 3rd party smart contract, service provider, or protocol as well.

This way, your loan can be very capital-efficient while at the same time have zero redemption risk.

Here's a cheat-sheet which illustrates our point - shoutout to @bjnpck for the nifty artwork.

Wow, Liquity V2 is shipping some new fire features in Q3 with V2:

- user-set interest rates

- minimum collateral ratio of 110%

- supporting LST/LRT collateral

- built-in mechanisms to improve peg

- better redemption protection

Read the full post... 👀

Introducing the next evolution of CDPs 🏦

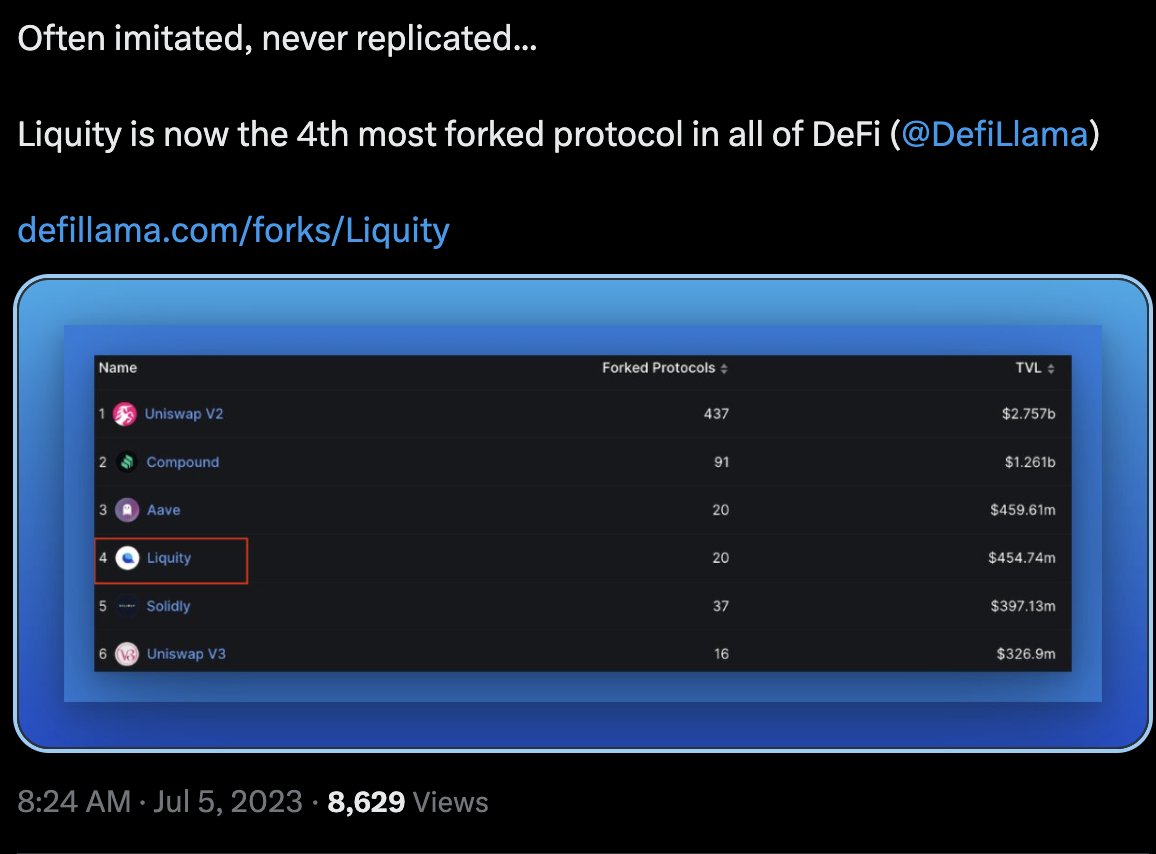

For nearly three years, Liquity has stood as a cornerstone within DeFi. With over $4.5 billion in loans issued, and its status as the most forked stablecoin protocol, its impact is undeniable.

We share a steadfast commitment to the principle of decentralization, resulting in a protocol that stands immutable and autonomous in the face of fluctuating market conditions. While this journey has been marked by success, it has also brought to light some challenges like addressing evolving user needs (demand for liquid staking tokens), and future-proofing against macroeconomic dynamics (interest rates).

This introspection, combined with recent market trends, has highlighted several key areas for improvement. With the insights gained from the last few years, we're embarking on a fresh journey of innovation.

As we open this new chapter, we’re proud to introduce one of our most significant innovations to date: user-set interest rates.

This feature represents a significant leap forward with CDPs, empowering users with unparalleled control, while also addressing current challenges and future dynamics.

👇

Crafting a superior CDP model

Initially, we explored the idea of a novel Reserve-backed stablecoin. However, after extensive research and repeated modeling over several iterations, we realized that the final product would face a difficult product-market fit due to economic uncertainties and lack of market maturity.

Furthermore, the past three years have provided us with invaluable insights: the primary challenge has transitioned from scaling borrowing demand, which was at the heart of our reserve-backed approach, to scaling stablecoin demand in an environment with rising interest rates.

This shift, along with the understanding gained from Liquity’s original product, has illuminated areas where our current system can improve, and highlighted opportunities for innovation within our codebase.

While numerous forks have emerged, most have barely improved on our original design. They have primarily focused on adding new collateral types and governance complications aimed at short-term gains rather than long-term resilience.

However, we do recognize that governance, if limited to peripheral or non-critical aspects of the system, can actually be advantageous, especially in areas like managing external liquidity.

So what improvements does the new protocol bring?

👇

The new protocol will offer the best borrowing experience, a highly resilient Ethereum-native stablecoin, and sustainable on-chain yield. It will be adaptive to any market environment, while also having minimal centralized exposure.

Let’s take a quick look at some of the key enhancements it introduces 👇

- User-set interest rates 💡

Unlike other CDPs and money markets where interest rates are typically set algorithmically or by governance, the new stablecoin gives users the power to choose their interest rate. However, this freedom comes with strategic considerations as borrow rates affect the loan position’s redemption order (more on this below). This flexibility allows users to tailor their borrowing experience based on their risk profile, providing them with full control over their open positions.

- Better redemption protection ⛓️

User-set borrowing rates also largely alleviate the redemption concerns seen in Liquity; as redemptions will now be based on an ascending order of interest paid. Users can avoid getting redeemed by paying higher interest rates (rather than keeping a high collateral ratio). This new borrow-rate model will also make redemptions less likely in general, as interest payments determine the yield paid out to stablecoin depositors within the Stability Pool.

- Adaptive to all economic conditions ⚡️

Unlike Liquity’s fixed one-time borrowing fee, the introduction of user-set interest rates makes the system dynamic and responsive to a changing economic environment. Users will be able to adjust their interest rate at any time throughout the lifecycle of their loan, or delegate it to a third party manager or smart contract.

- Improved peg dynamics ☀️

The new protocol’s introduction of dynamic borrowing rates and a market-responsive monetary policy will provide an additional lever to manage the stablecoin’s peg. Instead of having a fixed one-time rate that does not actively counteract over-pegging, there will now be in-built mechanisms in place to help the peg below and above $1.

- Multiple LSTs and ETH as collateral 🔷

The new stablecoin can be borrowed against various LSTs and ETH, while allowing borrowers to keep the generated yield. This means that the new stablecoin will be completely Ethereum-native with no ties to fiat or TradFi assets.

- Built-in liquidity incentives ✨

Maintaining liquidity is costly and time consuming. While a liquid market for LUSD developed over time, the new protocol aims to get there quicker. It will funnel a portion of the borrowing fees to select pools, thereby providing built-in, sustainable and continuous liquidity incentives.

- Sustainable real yield 👨🌾

In the new protocol, stablecoin holders will be able to earn real and sustainable yield coming from borrowing fees and liquidation gains. This will offer a sustainable and fully on-chain yield-venue for depositors. The Stability Pool yield in the new protocol will be reactive to changing market conditions ensuring enhanced sustainability of stablecoin demand and a reduced likelihood of strong sell events, like what happened to LUSD in Q2-Q3 2023.

- Capital efficiency 💫

Liquity was designed to push the boundaries of capital efficiency by introducing the minimum collateral ratio of 110% and improved liquidation mechanisms. However, due to the redemption pressure, it's not been able to live up to its goals consistently. Our new product aims to change that.

- Ecosystem for builders to build on top of

We are strongly convinced that the introduction of this new DeFi primitive, centered on user-driven interest rates, not only enhances its direct appeal to users but also opens doors for developers and protocols.

A key feature of the product is the ability for user-set interest rates to be delegated, enabling interest rates to be managed by third party managers or smart contracts. This functionality encourages developers and protocols to build novel integrations (eg. a tool to manage interest rates) on top of our infrastructure, fostering innovation.

👇

So how is this new protocol an evolution on CDP models seen to date?

Compared to CDPs of yesteryear, the new product aims to solve the crucial aspect of balance between borrowing and stablecoin demand. This is achieved through the introduction of user-set interest rates.

In contrast to Liquity, borrowers on the new protocol will have the freedom to set their own interest rates, and change them at any time. This autonomy not only caters to diverse borrower preferences, but also impacts their risk levels. By choosing higher interest rates, borrowers can reduce the likelihood of being affected by redemptions, thereby aligning their individual incentives with the stablecoin peg dynamics of the system.

This approach is mutually beneficial: it provides borrowers with the tools to adjust to an ever-changing market, while promptly reflecting those shifts in the monetary policy of the protocol itself.

For example, when there is significant sell pressure on the stablecoin and redemptions pick up, borrowers can protect themselves by increasing their borrowing rates. The resulting higher fee payments serve as direct revenue to the Stability Pool, driving demand for the stablecoin which subsequently helps the stablecoin peg and lowers redemption risk.

Thus, the protocol has built-in incentives to reach an equilibrium between the demand for the stablecoin and the supply created through borrowing. ✨

Furthermore, the protocol achieves this balance while maintaining a decentralized approach, diverging from peers that have “centralized" collateral assets or modules. This is especially interesting for users who value trust minimization; the protocol will not have any counterparty or collateral risk connected to fiat or real world assets as it is only backed by LSTs and ETH. The addition of LST’s will broaden the protocol’s appeal to a more diverse group of borrowers, increasing the addressable market while future-proofing it. ⛓️

Within the Liquity ecosystem, users will now have access to multiple borrowing options tailored to their preferences and risk profile. Liquity offers a robust, battle-tested framework that prioritizes ETH as collateral, ideal for long-term borrowing, while the new protocol introduces user-set interest rates and diverse ETH variants, appealing to those with different borrowing needs.

This means that the Liquity ecosystem ensures that all users, regardless of their risk appetite and goals, find a suitable option for their ETH or LSTs. 💫

👇

Setting the stage for future discussions

By creating this new protocol, we aim to pioneer a more adaptable and capital-efficient CDP protocol without sacrificing resiliency. 🪐

In the coming weeks and months, we will be releasing detailed articles that will delve deeper into each improvement, providing insights and data-driven analyses of how these features will shape the future of CDP-based borrowing protocols. Some of these topics include:

- User-set interest rates and the borrowing enhancements 💡

- The inner workings of the stablecoin 🪙

- The LSTs that will be used as collateral 🔷

- The new best-in-class approach to non-centralized frontends 🕸️

- and more

And lastly, wen ?

Late Q3, 2024

Don’t miss our next articles - ensure that your notifications are turned on for our Twitter 🔵

Your voice matters - be an active participant in our Discord via our v2 channel and contribute your ideas, ask questions, and share insights. 🎙️

Roses are red 🌹

Violets are blue 🪻

Liquity's unveiling

A DeFi breakthrough

Tomorrow, info on a new primitive in DeFi comes to life.

Notifications on. 🔔🔵

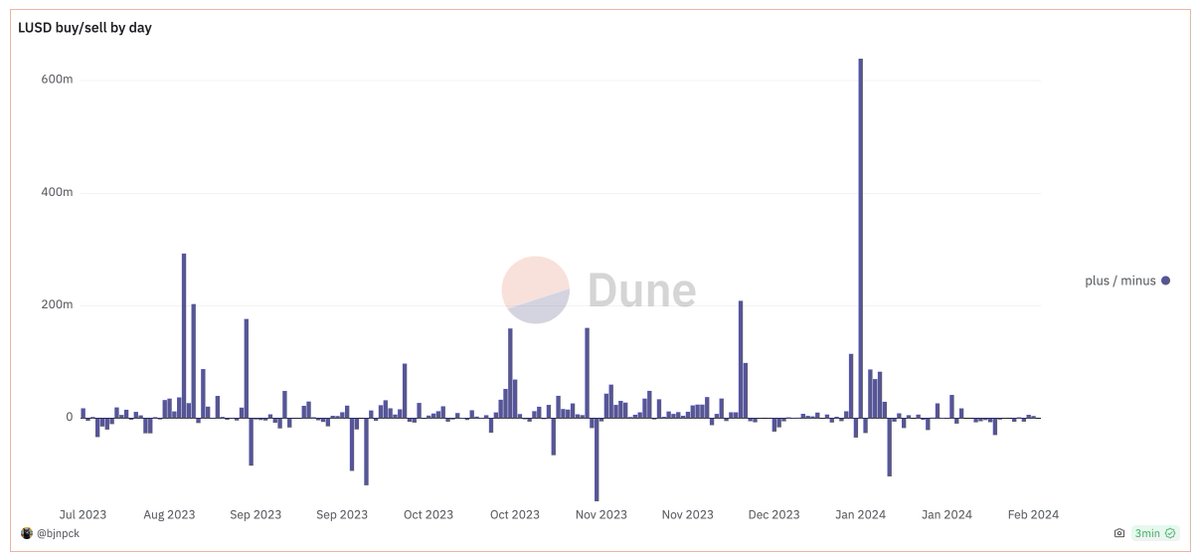

Redemptions, redemptions, redemptions…

As a Liquity user you’ve heard this word way too often lately.

And likely developed a disdain for it.

Understandable. We get it.

But, bear with us for a moment. Let's shed some light on why they are a crucial component of Liquity’s system-design, and how they performed during last year's wave of redemptions.

Between Aug 2023 and Jan 2024, the LUSD supply didn't just dip; it was cut in half!

Plummeting from a robust 298 million to just 148 million - a considerable drop by any measure.

When the market wipes out 50% of a token's supply, logic dictates a significant drop in its price – that's basic supply and demand at play.

However, #stablecoins are designed to be the exception to this rule. They should have mechanisms in place to shield holders from a loss of value.

For LUSD, this is where redemptions come in. They are the key component which helps LUSD repeg from the downside.

Redemptions are the process of exchanging LUSD for ETH at face value, as if 1 LUSD is exactly worth $1.

When the price of LUSD falls below $1.00, users can take advantage of this option.

They can market-buy it, and then redeem it for ETH.

It's essentially a swap, trading LUSD bought at $0.99 for $1.00 worth of ETH, and, in the process, reducing the circulating supply.

Simple, really?

Be mindful though that redemptions are different from liquidations.

Read more here: https://t.co/69eULSLxfU

So, how well did this mechanism perform?

As you can see it worked pretty well.

LUSD remained remarkably stable, seldom dropping more than 0.50%

Notably, over the span of 5 months, it dipped below $0.99 only once!

In simpler terms, there was always enough demand to match the persistent selling pressure.

But why would anyone buy into strong selling pressure?

The answer lies in economics.

Users make instant profits by exploiting the price difference between LUSD's market value and its protocol-set price. Sophisticated players and bots seize any arbitrage opportunity as soon as available.

Consequently, LUSD rarely fell below $0.995.

We can express this also another way, saying that sell pressure was never able to overwhelm demand.

Taking a closer look at the past 5 months, you'll notice that selling volume surpassed buying volume on just a handful of days.

Quite the feat.

Being a LUSD holder is knowing that your asset's value will be protected, no matter what turbulence hits #DeFi or the broader macro environment.

You also know that your funds:

- Are not seizable

- Have 0 exposure to centralized assets

- Cannot be affected by governance decisions

- Are usable across an ever-expanding DeFi ecosystem

No other stablecoin can claim that.

No other stablecoin comes even close.

But, there is a downside to this resilience.

The ETH used in redemptions comes from borrowers.

So, if there's a surge in redemptions, even those with a conservative LTV might be affected.

While the Liquity team cannot change this, we are not sitting idly.

The “v2 product” will offer bullet-proof redemption protection without sacrificing capital-efficiency.

Stay tuned for the article later this week.

Do you know about our Community Reward Program?🤔

It has been running since July '22, rewarding users each month.

🔹 100+ individual recipients

🔹 $60,000+ paid out

What contributions qualify?

✅ Threads / articles covering Liquity, integrations, news, etc. We also value localized content in non-English languages.

✅ Videos / shorts - we would prioritize such content

✅ DAO initiatives - proposing integrations, collaborations, treasury diversification w/ LUSD...

✅ Yield strategy opportunities

✅ Dune dashboards

You can also always ping us on Discord, and ask for feedback and ideas.

We are going to start releasing content around v2 very soon, and contributions around it will be very much appreciated.

Rewards are paid out retroactively. You need to apply via a form which we tweet out each month on the 15th.

👉 Read more here: https://t.co/WuY0raI7mX

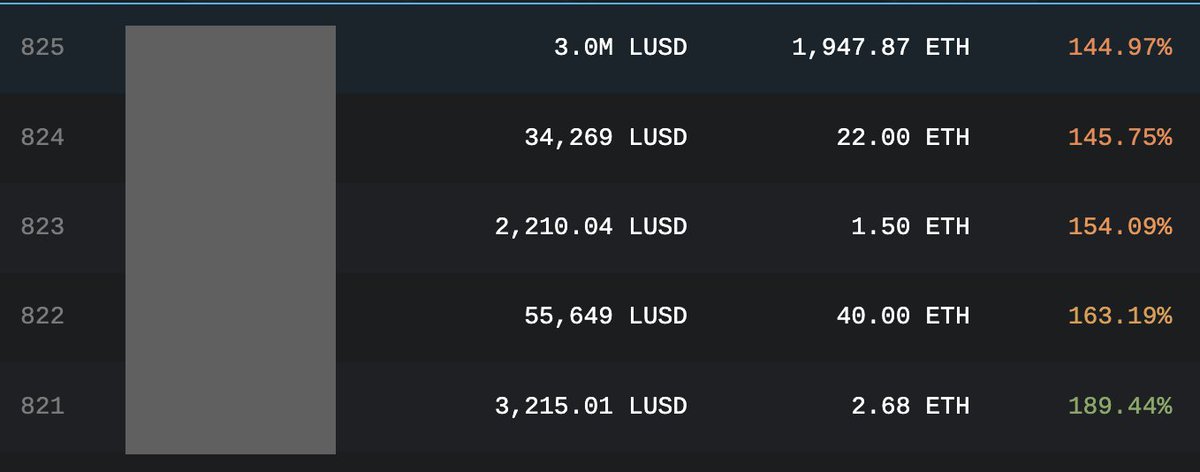

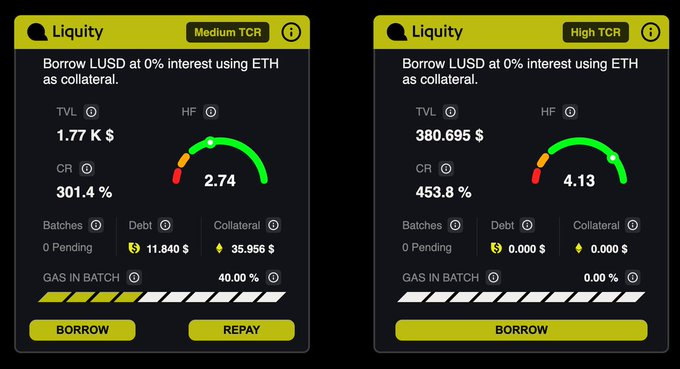

Borrowing on @LiquityProtocol back on the menu?

Recent months has seen the LUSD peg hovering below $1, which has led to a a significant number of redemptions, resulting in a less than optimal borrowing experience for users.

But all things must pass!

With $LUSD now back above $1, redemptions are now no longer profitable.

How did this happen?

Recently we saw a whale 🐋 pay back some of their Liquity debt to the tune of ~ $20m LUSD.

They used aggregators (the likes of @paraswap and @1inch) to market buy LUSD with size ($5m clips) which helped restore the LUSD peg back over $1.

As a result of the redemption risk going away, we're beginning to see borrowers borrow at higher LTV ratios as evidenced below 👀

With real world interest rates showing signs of cooling down as well, are we back at an equilibrium point?

Time will tell.

Decentralizing DeFi frontends

Liked our recent content around running local apps?

Check out @edwardmulraney's piece on how local applications work👇

https://t.co/2R1ZnZ41Wx

The Liquity ecosystem tokens as collateral within DeFi 🔷

Did you know that there are 7 different places where you can borrow against:

- LUSD

- bLUSD

- and LQTY

Let's have a quick look at all the different money legos involved 👇

@aave - On Aave, users can get yield on their deposited LUSD, along with being able to use it as collateral to borrow other assets.

All at the same loan-to-value ratio as USDC on Mainnet!

The @optimismfnd & @arbitrum flavors of Aave allow for LUSD to be deposited as an isolated asset.👀

👇

@silofinance - Silo have integrated both LUSD and LQTY as collateral within their money market. Regarding LUSD, there are multiple options for using LUSD as collateral:

a) You can use LUSD as collateral and borrow XAI (Silo's stablecoin) or ETH against it (85% LTV)

b) You can supply the LUSD- 3CRV LP token and borrow XAI (80% LTV)

Silo also supports using LQTY as a collateral asset! You can borrow XAI against LQTY at a 50% LTV ratio.

👇

@AngleProtocol - Angle provides users with the ability to borrow agEUR against LUSD at a LTV ratio of 88% & at an annual interest rate of 2.5%.

Angle also allows users to go leverage long on LUSD if needed as well

👇

@gravitaprotocol - On Gravita, users can use bLUSD as collateral in order to mint their stablecoin, GRAI.

One of the benefits of the bLUSD vault on Gravita is that it cannot get liquidated!

Although mint caps are currently full, keep an eye out on Gravita Twitter/X for when capacity becomes available 👀

👇

@gearbox - Although not necessarily a classic case of borrowing, users on Gearbox can deposit LUSD3CRV LP tokens, loop the LP token on leverage, and get amplified DeFi returns.

👇

@SonneFinance is a money market on @optimismfnd. On Sonne, users can use LUSD as collateral and borrow a plethora of different stablecoins against it. Liquidity providers also get compensated for providing LUSD liquidity to the dApp.

👇

@MysoFinance - Last but not least, there are the new kids on the block, MYSO! It is a P2P borrowing protocol.

MYSO's integration allows LUSD and LQTY holders to lend or borrow against each other, or against every other collateral on the platform.

For example, LQTY holders can use their tokens to borrow LUSD, and do the exact opposite by borrowing LQTY against LUSD collateral.

As the protocol is P2P, the terms are set by you, the user!

Join us again later this month for another dive into the Liquity ecosystem: this time, on DEXes!

The LUSD ecosystem: L2's

Although Liquity's contracts are immutable & on mainnet only, that doesn't stop the stablecoin to foray onto various L2's via bridges 🌉!

Did you know that LUSD is available on all of @optimismFND, @arbitrum, @zksync, @Starknet, and @0xPolygon?

And as of this week, the most decentralized stablecoin is also available on.... 🥁🥁

@BuildOnBase 🔵

LUSD on all these chains can be accessed and 'bridged' through the various official bridges that support them.

However, there is ONE chain where you can do more than just bridge 👀👇

With @Starknet, users can actually access Liquity to borrow, and benefit from:

• 3x-7x less gas cost

• No minimum loans

• Benefit from the various DeFi projects that exist within the @Starknet ecosystem

Check out this guide as to how to get started here:

https://t.co/9qZ9Afiy14

So what other DeFi stuff can you do across all these chains?

Join us tomorrow, and have notifications on 🔔

Looking for a stablecoin that is

- RWA free

- Backed by trustless collateral

- & can be used as a collateral asset?

LUSD is both a borrowable AND a collateral asset on @AaveAave across

- Ethereum

- @arbitrum 💙 , 🧡

- & @optimismFND 🔴

What are some use cases you ask?

👻 👇