Assets in motion, stay in motion.

INERTIA is the interwoven lending protocol for LSTs, LRTs, and more within the modular ecosystem.

As an interwoven rollup on @initiaFDN 🪢, with @celestiaorg underneath ✨, we’re building the platform for high-performance DeFi.

🧵

🚀 Lano is joining the Initia testnet as a validator! Stay tuned for updates on our journey and for more exciting tech threads related to Initia! 📡🔓 #Initia#Testnet#Blockchain#Crypto#LanoTechnology

I'm ecstatic to announce that @FourPillarsFP has been awarded a 'Research Grant' by @dydxfoundation. This is a significant acknowledgment for us, as it underscores the recognition of our research quality by global entities like @dYdX. Despite being just six months into our journey, this grant is a testament to our rapid growth and dedication.

However, our research journey is far from over. We remain eagerly open to exploring new possibilities :)

Part 2 of the Frax article explains how Frax Finance grew FRAX in the stablecoin market. It covers the stablecoin market conditions at the time and how Curve AMO played a pivotal role in its growth. Additionally, it discusses the strategies Frax employed on the Onchain platform.

TL;DR

- Frax Finance defined, through the concept of AMO, the extent to which they could issue more FRAX against their collateral assets.

- Through this leverage, they actively controlled the price of FRAX in the market while managing liquidity in the form of protocol-owned liquidity on the Curve pool.

The Stablecoin Market Conditions in 2021

In 2021, the competition among stablecoins was fierce. Major stablecoins had already established themselves in various sectors (centralized - USDC/USDT, algorithmic - UST, leverage farming - MIM). Frax did not have a clear advantage over existing players in terms of being a store of value, a means of payment, or a lending instrument.

Limitations Faced by Frax

Frax aimed to combine the price stability of collateral-based stablecoins with the flexibility of algorithmic stablecoins through its partial algorithmic structure. However, in reality, there was a lack of demand for FRAX in the market, which hindered the increase in FRAX issuance in the market.

Challenges Frax Needed to Address

To grow its stablecoin, Frax needed to maintain price stability while creating utility that would encourage users to continuously mint FRAX. Furthermore, it had to mint as much FRAX as possible using the limited USDC reserves held by the protocol.

Interpretation of AMO and Collateral Ratio

Frax Finance introduced a system called AMO during this period, and they set different methods for calculating collateral ratios for each AMO based on how they utilized collateral assets.

Rather than considering the absolute quantity of collateral assets held by an AMO, they used the collateral ratio calculation based on how the assets were utilized. This allowed Frax to create a foundation for issuing more FRAX compared to USDC collateral, as each AMO determined the minimum price support they could offer for the FRAX they issued based on their asset utilization.

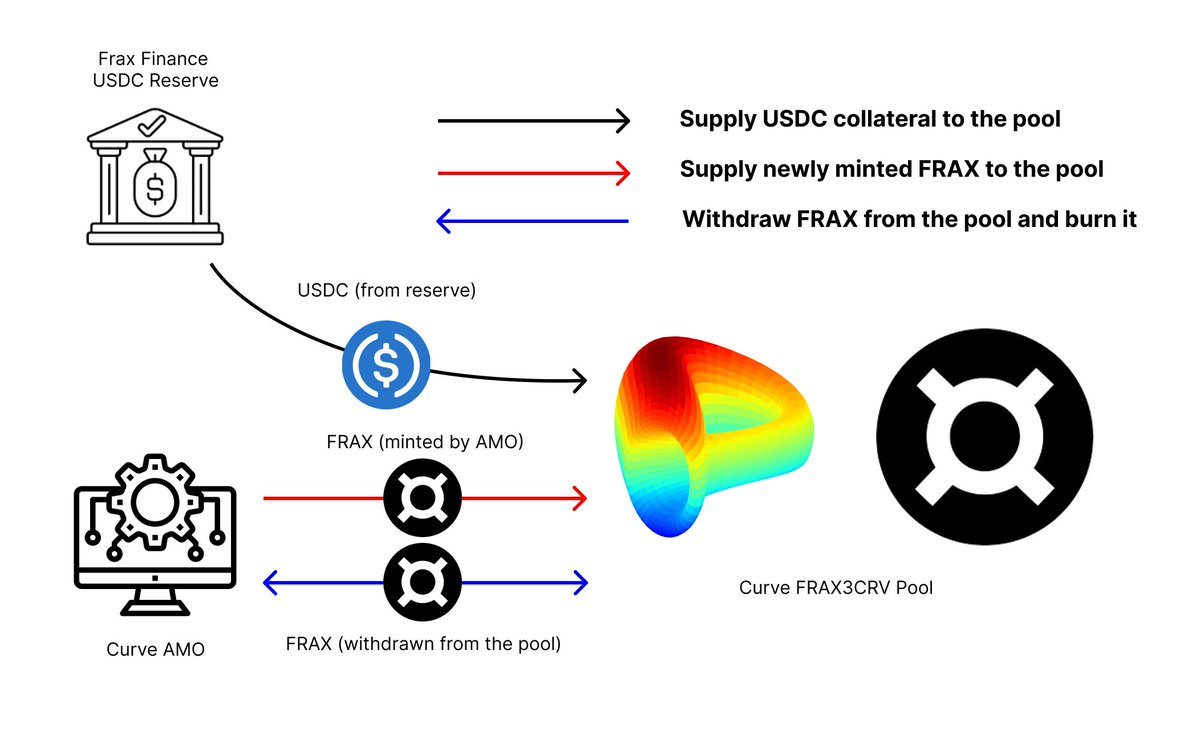

Concept of Curve AMO

Curve AMO was introduced to create protocol-owned liquidity on the stable swap pool, which is considered the optimal DEX pool for stablecoins. Its purpose was to manage liquidity in the FRAX3CRV pool, primarily held by Frax, by adding or withdrawing liquidity according to market conditions in order to maintain the price.

Curve AMO utilized the unique trading ratio calculation method of stable swaps, interpreting the quantity of collateral assets held by Curve AMO in a way that could be expanded (this aspect can be complex and is recommended to be read in the article). This allowed for the issuance of more FRAX into the market.

FRAX issued through AMO was used to maintain the price of FRAX at $1 in the FRAX3CRV pool. For example, when the price of FRAX was too high, more FRAX was issued and added to the pool to lower the price. Conversely, when the price of FRAX was too low, FRAX was withdrawn from the pool and burned.

Impact of Curve AMO

With the introduction of Curve AMO, the issuance of FRAX increased rapidly, and a significant portion of FRAX was minted in the FRAX3CRV pool through Curve AMO. Thanks to the involvement of Curve AMO, the ratio of FRAX to 3CRV tokens in the FRAX3CRV pool remained stable, allowing the pool to grow.

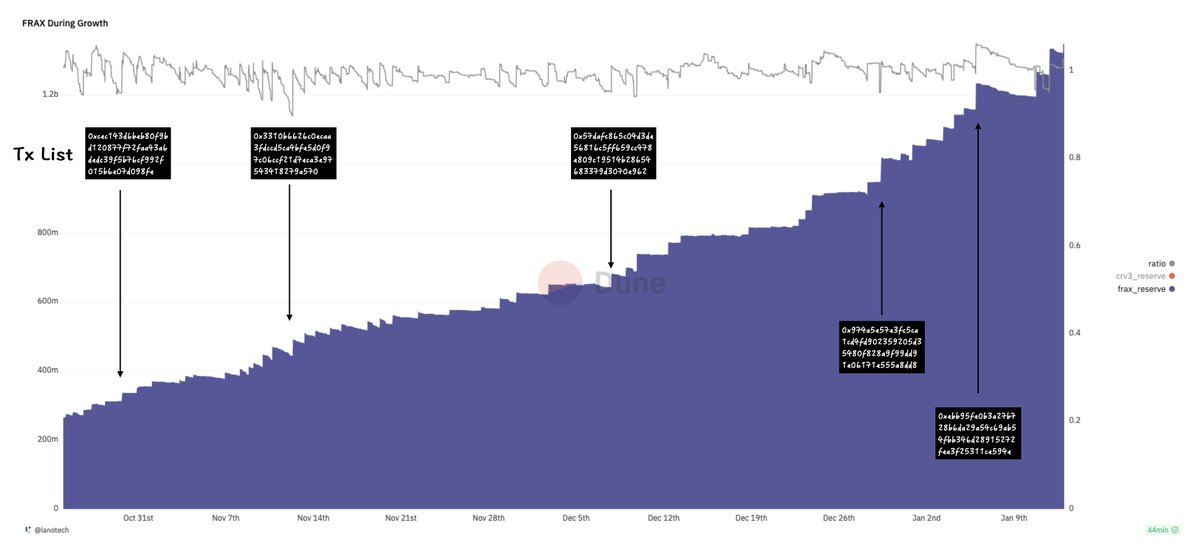

Impact of Curve AMO - Bull Market

Looking at the data from the growth period of the FRAX3CRV pool, we can see that the proportion of FRAX within the pool decreased continuously due to market buying of FRAX. At each instance, Curve AMO issued FRAX to supply the pool, thereby maintaining the price of FRAX at $1 while increasing the size of the FRAX3CRV pool.

It's worth noting that Frax Finance (Curve AMO) held the majority of liquidity in the FRAX3CRV pool. This allowed the Frax team to incorporate the 3CRV tokens sold by FRAX buyers into the protocol's assets. As a result, the Frax team was able to increase collateral assets in line with the increased FRAX supply.

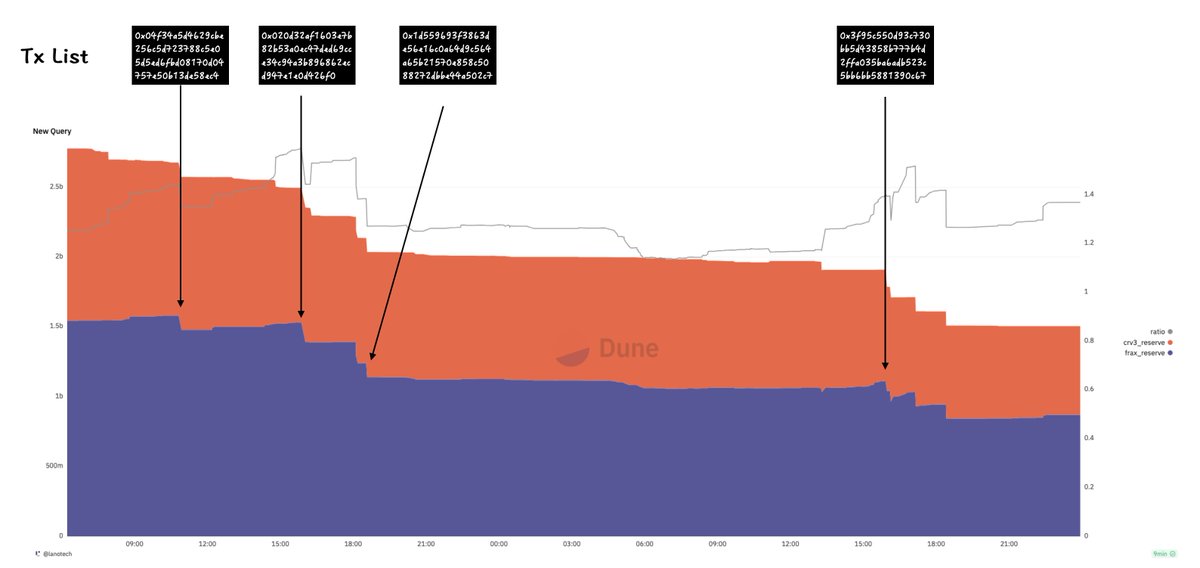

Impact of Curve AMO - Bear Market

During the bear market (the time of Terra's collapse), continuous selling pressure on FRAX persisted due to uncertainty. This resulted in an ongoing increase in the proportion of FRAX within the FRAX3CRV pool. Whenever the proportion of FRAX exceeded a certain threshold, Curve AMO would withdraw FRAX from the pool.

Through these actions, Frax Finance was able to directly maintain the price of FRAX at $1 on-chain and prevent an excessive depletion of USDC collateral assets by arbitrageurs. Thanks to the proactive role of Curve AMO, FRAX has been able to maintain a stable value of $1, except during USDC de-pegging events.

For more detailed explanation, please read our article!

@fraxfinance@samkazemian

https://t.co/0tBlMEZq1t

Frax Finance는 이러한 함정을 피하기 위해 자신들만의 토큰을 계속 발행하는 대신 다른 프로토콜의 보상 체계를 적절히 활용하여 높은 보상을 제공했습니다. FRAX의 경우 Curve 보상을 적극적으로 활용하였고, frxETH의 경우 ETH 스테이킹 보상과 Curve 보상을 활용하였습니다.

Frax 아티클 3편은 Frax Finance가 ETH LSD 시장에서 성장한 방법에 대해 설명합니다. 당시 LSD 시장 상황부터 초기 성장의 발판이 되었던 Curve AMO와 다른 LSD에 비해 높은 이율을 제공한 방법에 대해서 다루겠습니다.

https://t.co/HzGsda72eL

Lesson Learned - 4 지속 가능한 보상 설계의 중요성

높은 보상을 주는 가장 쉬운 방법은 자신의 토큰을 계속 발행해서 지급하는 것입니다. 하지만 이러한 방법은 지속 가능하지 않으며, 발행하는 토큰을 받아줄 시장 유동성이 결국 부족하게 되어 토큰 가치가 급락하게 됩니다.