I just minted DEATH TOUCH ALPHA SEASON 1 PASS from @Deadfellaz

You can still get in on this OG Bluechip project from circa '21. the founders keep grinding and keep building value for the holders AND they believe that airdrops should just be "dropped" not any other way.

</alpha>

LFG!

This team keeps building, inspiring and the mojo up for the class of '21

Looking forward to celebrating the summer and much more @betty_nft@psych_nft 🚀

People have asked me how I feel about Udemy’s sale to Coursera. Honestly, I’m kinda pissed about it.

I want to be clear - I’m grateful for the opportunity to start and benefit from Udemy’s success. It changed my life.

But there’s another side to Udemy. A story of what could have been.

After our Series B, founders owned less than 30% of the company. Our investors took over and installed their own CEO to run it. We all liked this new CEO and honestly, for years it looked like a brilliant move. The company kept growing and growing. They launched B2B and built a $500M ARR business. Eventually, the company IPO’ed for $3B.

Yet all along there were clear cracks under the surface. Over Udemy’s history, there have been 7 CEO’s. The board replaced the second CEO with dud after dud. I’d often try to meet with the board or the new CEO, and was completely ignored. Eren had influence as Chairman of the Board but Oktay and I were so ignored they didn’t even invite us to the IPO. LOL WTF. There are like 50+ people invited to these things and nobody thought: “oh maybe we should invite the people who fucking invented the thing we’re all celebrating.” It shows how little respect they had for founders and for product innovation as a discipline.

I think they wanted a CEO they could control, a buttoned-up suit instead of a brash founder/CEO that is risk-taking, visionary, but a bit of a pain. For awhile, it looked like it didn’t even matter who was CEO - the company was run by the incredibly talented team that reported to them anyways.

Well, it worked until it didn’t.

The company made no major product innovations for 15 years. Instead, they took the original idea (video-based courses) and sold it in every place imaginable. It got us to $800M run-rate. That’s no joke; that takes serious execution and a great team that hustled hard to win the market.

But eventually the consumer business stopped growing. The B2B business has now flattened out as well. Meanwhile, Coursera was catching up.

Original Coursera was a far worse product than Udemy, but it got a ton of press. Learning ivory tower bullshit from academics doesn’t get you a real education, but it does create prestige. They raised from better investors on better terms, and had better leadership.

Udemy to this day has more revenue than Coursera, but Coursera won the court of investor opinion. They got higher multiples from both private and public markets.

Coursera innovated heavily. They added corporate courses to their university catalog, built fully-online degree programs, and offered a B2B competitor that kept Udemy on its toes. Still, the Udemy B2B business (and team) out-performed and so the two companies were deadlocked. Coursera was better at B2C, Udemy at B2B.

A merger was inevitable.

But WHY IN GODS NAME did we sell to Coursera instead of the other way around? Why are the combined companies under $3B in market cap?

Three reasons:

First, edtech didn’t live up to its promise. While these two companies had solid revenue and cash positions, their growth slowed, and public markets balked. This meant compressed multiples and significantly lower valuations.

Second, the companies stopped innovating. They are selling a product to businesses that their customers don’t love. They were category leaders, but they lead the category into mediocrity. They captured a significant share of learning and development (L&D) spending, but L&D as a whole actually lost budget within their organizations. That’s Udemy’s fault, and it doesn’t even realize it.

That brings me to my final point: I personally believe Udemy traded upside opportunity for downside risk. Us founders were unproven and young. We made lots of mistakes, including fighting amongst ourselves. A good investor would have supported us through it because they believe founders drive the highest long-term returns. Instead, they brought in outside CEOs to replace us. I sometimes wonder if they recognize this error; everyone makes mistakes and maybe they learned from it.

Either way - the consequences are real. By ignoring the founders, Udemy failed to innovate, which led to slowing growth which led to mediocre public market results. Furthermore, they don’t have a good evangelist and public markets don’t like a headless horse.

I sold my Udemy stock awhile ago. I think the merger was critical for both companies’ survival. Now, though, the new combined entity needs to innovate again.

On B2B, Coursera needs to help L&D become the heroes of the AI era so the entire market starts growing again. On B2C, they need to build the most educational AI product on the planet. (I’d focus on the former, since the latter is a lot harder and riskier).

Coursera can still achieve our original vision and likely build a $10B+ company in the meantime. Even though I’ve got no stake in its future, I’m mission-driven and I REALLY hope they figure it out.

The current education system sucks and the world deserves something better.

The Colourful Truth of Sugary Soft Drinks in India. Love the way this bro explains to kids.

Infact No Human deserves to Consume this.

FSSAI team - For your kind information.

This video needs to go Viral.

#FI

Founders who don’t fold, fade.

For every founder that raises capital, for every business that hits a major liquidity event, there are many more founders and businesses that don’t get to a logical end.

They neither fold, nor do they exit with a liquidation event; sometimes it’s a pivot with the same name or they move on but retain the brand name until it slowly sunsets.

What they have built over years with sweat, passion, personal capital and all their heart sticks on to them as an identity; until they discover their next calling. Very often this next calling is the same old wine packaged in a new bottle- even if it had a 400Cr exit, for that became an itch that wasn’t fully scratched.

Unscratched itches and unresolved identities are common traits you will find in such entrepreneurs; if you do come across one and have the intent to support, do give them a hug, some acknowledgment and ignite a conversation to help accept closure. For what they will build next, after being unleashed, is likely to be a blockbuster- and you may feature somewhere in the credits.

Many such concepts are lost in translation. Good to see such educational content being created lest our generation and ones to come are anyway being whitewashed.

Also read up on “Adaan-pradaan” in similar context.

I don't use net banking apps on my phone because the mandatory permissions they ask for make no sense.

Why does a banking app need access to my SMS, phone, contacts, etc., in the name of security, when not seeking invasive device permissions is, in fact, the global benchmark for cybersecurity. This is called the Principle of Least Privilege (PoLP).

“Don't do unto others what you don't want done unto you” has been at the heart of the Zerodha philosophy.

This is exactly why we've built Zerodha the way we have. Kite asks for ZERO permissions on mobile, for instance, and this is one of the big reasons why millions of people trust us. What has enabled us is SEBI's mandatory strong two-factor authentication framework strike the right balance between security and privacy.

Everyone’s missing the real story here.

Meta’s Ray-Ban glasses need human data annotators to train the AI. When you say “Hey Meta” and ask the glasses to analyze something, that video gets sent to Meta’s servers, then routed to Sama, a subcontractor in Nairobi, Kenya. Workers there manually label objects in your footage. They see everything you recorded, intentionally or not.

7 million pairs sold in 2025 alone. Every single pair generates training data that flows through human eyes in Kenya. Workers told Swedish journalists they see people undressing, using bathrooms, having sex, and accidentally filming bank card details. One worker said “we see everything, from living rooms to naked bodies.”

Meta’s automatic face anonymization is supposed to protect people in the footage. Workers say it fails in certain lighting. Faces that should be blurred are sometimes fully visible. The person you recorded without knowing? A stranger in Nairobi can identify them.

Buried in Meta’s terms of service is one sentence doing enormous legal work: the company reserves the right to conduct “manual (human) review” of your AI interactions. That’s the legal cover for routing intimate footage from Western homes to a $2/hour labor force operating under NDAs, office surveillance cameras, and a strict no-questions policy. Workers say if you raise concerns about what you’re seeing, you’re fired.

This is the same company, Sama, that TIME exposed in 2023 for paying Kenyan workers $2/hour to label graphic content for OpenAI while being billed at $12.50/hour per worker. Workers described the experience as torture. Sama ended that contract, then pivoted to labeling Meta’s glasses footage. Same workforce. Same rates.

Meta markets these glasses as “designed with your privacy in mind.” The privacy design is a tiny LED light on the frame that most people don’t notice. The data pipeline behind it routes your bedroom footage to a contractor with a documented history of worker exploitation, failed anonymization, and union-busting lawsuits.

And the next generation of these glasses? Meta is planning to add facial recognition. The same system that can’t reliably blur faces in training data wants to start identifying them on purpose.

The LED light on the frame is doing about as much for your privacy as the terms of service nobody reads.

No complexity. No accident.

10/10 was caused by irresponsible marketing campaigns by certain companies.

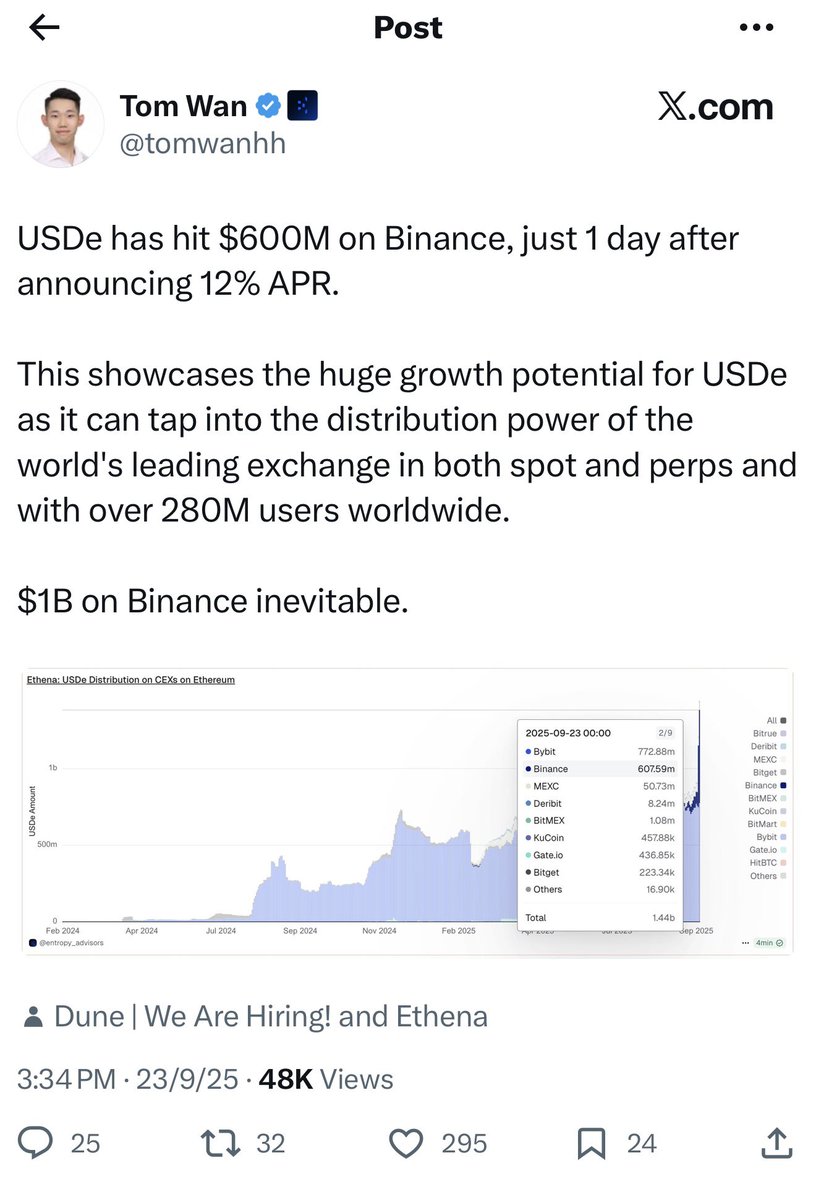

On October 10, tens of billions of dollars were liquidated. As CEO of OKX, we observed clearly that the crypto market’s microstructure fundamentally changed after that day.

Many industry participants believe the damage was more severe than the FTX collapse. Since then, there has been extensive discussion about why it happened and how to prevent a recurrence. The root causes are not difficult to identify.

⸻

What actually happened

1.Binance launched a temporary user-acquisition campaign offering 12% APY on USDe, while allowing USDe to be used as collateral with the same treatment as USDT and USDC, and without effective limits.

2.USDe is a tokenized hedge fund product.

Ethena raises capital via a so-called “stablecoin,” deploys it into index arbitrage and algorithmic trading strategies, and tokenizes the resulting fund. The token can then be deposited on exchanges to earn yield.

3.USDe is fundamentally different from products such as

BlackRock BUIDL and Franklin Templeton BENJI, which are tokenized money market funds with low-risk profiles.

USDe, by contrast, embeds hedge-fund-level risk. This difference is structural, not cosmetic.

4.Binance users were encouraged to convert USDT and USDC into USDe to earn attractive yields, without sufficient emphasis on the underlying risks. From a user’s perspective, trading with USDe appeared no different from trading with traditional stablecoins—while the actual risk profile was materially higher.

5.Risk escalated further as users:

•converted USDT/USDC into USDe,

•used USDe as collateral to borrow USDT,

•converted the borrowed USDT back into USDe,

•and repeated the cycle.

This leverage loop produced artificial APYs of 24%, 36%, and even 70%+, widely perceived as “low risk” simply because they were offered by a major platform. Systemic risk accumulated rapidly across the global crypto market.

https://t.co/IK2gW4xUOP that point, even a small market shock was sufficient to trigger a collapse.

When volatility hit, USDe depegged quickly. Cascading liquidations followed, and weaknesses in risk management around assets such as WETH and BNSOL further amplified the crash. Some tokens briefly traded near zero.

The damage to global users and companies—including OKX customers—was severe, and recovery will take time.

⸻

Why this matters

I am discussing the root cause, not assigning blame or launching an attack on Binance. Speaking openly about systemic risks is sometimes uncomfortable, but it is necessary if the industry is to mature responsibly.

I expect there may be significant misinformation and coordinated FUD directed at OKX in the near future. Even so, speaking honestly about systemic risk is the right thing to do—and we will continue to do so.

As the largest global platform, Binance has outsized influence—and corresponding responsibility—as an industry leader. Long-term trust in crypto cannot be built on short-term yield games, excessive leverage, or marketing practices that obscure risk.

The industry needs leaders who prioritize market stability, transparency, and responsible innovation—not a winner-take-all mentality where criticism is treated as hostility.

Crypto is still early.

What we choose to normalize today will determine whether this industry earns lasting trust—or repeats the same mistakes again.