@happytrader69@preston_holland I’ve been on here for years saying SL was a problem for gogo. Your opinion is definitely the majority but size matters. FDX is 195 mbps. What if you want LEO and GEO. Mil/gov… will have better data tmr. Believe it or not the equity has treated me pretty well lol…

Given recent positive developments re: Clarity Act, let’s review the economics of BeelineEqutiy $BLNE

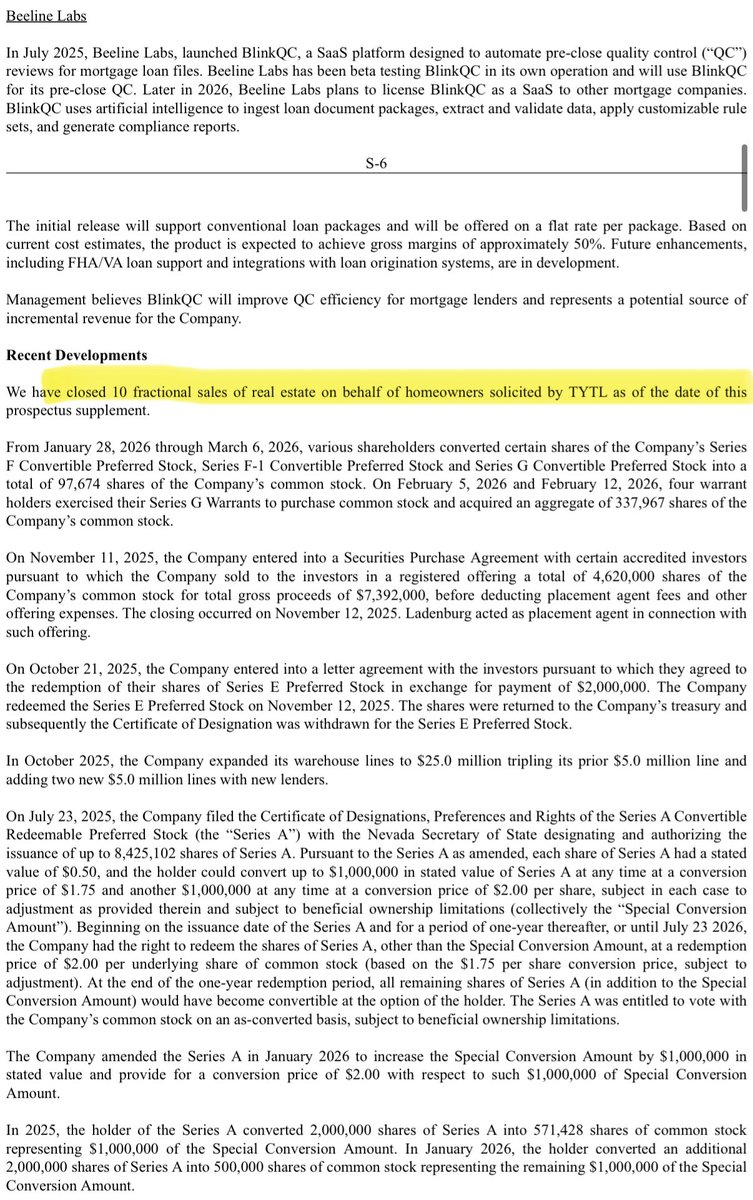

Beeline will facilitate a fractional sale of your home equity from $50-200K for an 8.5% transaction fee. Of the 8.5% fee, 3.5% goes to $BLNE and 5.0% goes to the stablecoin partner TYTL (https://t.co/6YwaEBPwYJ).

TYTL is backed by @strobefund, which was the VC arm of @BlockTower that spun-off following BlockTower’s merger with @arca, keeping the original team in tact. Also, TYTL has a strategic partnership with @Anchorage for custody and distribution of its stablecoin. Anchorage Digital is the first and only federally chartered crypto bank in the U.S., and it is the custodian for BlackRock’s crypto products, and @tether made a $100M investment in the bank. Point is that TYTL appears to be pretty legit given these relationships.

Anyways, the bottleneck to scaling this business in my view is the demand for a stablecoin backed 1:1 by U.S. residential real estate, and I believe that the Clarity Act would unlock a lot of institutional demand for these assets, particularly from overseas investors.

I also think that TYTL’s partnership with $BLNE position it well to be the first-mover in this space, as $BLNE founder and CEO Nick Liuzza is an expert in title services, having previously built the largest privately held title company in NA. Title, in my opinion, would be the most challenging operational part of scaling this product, but Nick and his team have the expertise to get it done. Nick is also a co-founder of TYTL.

Back to the economics. If $BLNE is able to facilitate 100 fractional home equity sales per month with an average transaction value of $150K, that would be $15M of monthly volume, with $525K of transaction fees to $BLNE at 3.5%. Tack on an extra 50 bps for title services and you get $600K of total fees, which are expected to have ~80% pre-tax margins. So 100 transactions per month could support $5.8M of annual pre-tax income. The TAM is in the trillions, so it’s not unreasonable to think the business could scale to 500-1000 monthly transactions, which would be $29M-$58M of annual pre-tax income. Assign a 10-15x multiple and BeelineEquity could be worth $290-870M on a standalone basis, or ~$8-25 per share on fully converted shares of 35M.

I won’t drag you through the math on the mortgage business, but I think that’s likely worth $7-10/share in a more normalized environment.

Put it all together and I could see $BLNE being worth $15-35 per share, versus $1.93 today. And this doesn’t even contemplate potential buybacks with all of the capital it would be generating, with minimal capex needs. 🐝