Offshore Drilling Notes

(1) Noble's 7G Viking is reportedly nearing a $465k, ~300 day award from Petronas in 2028, according to SB1M and S&P Global. This is likely for the Kelidang gas project in Brunei. Strong number from recent low-$400k levels on rising regional utilization.

Eldorado's sale of drillships Dorado and Draco to Turkey last summer was a positive signal for deepwater dayrates — vessels that would otherwise have competed for SE Asian and global tenders are now absorbed into Turkey's domestic energy security program and effectively removed from marketed supply. Also, the Eni/Petronas JV (Searah) will use 2 rigs on multiyear terms in Indonesia, along with Eldorado's Platinum Explorer moving to India leads to rising utilization in the region pushing dayrates higher.

(2) Transocean Norge was awarded a $497k dayrate in Norway on a 300-day term. Given market strength, short duration contracting is the right posture for Tier 1 Semisubs here — Norway runs heavy on shorter-cycle brownfield demand, drilling intensity is rising, and exploration activity remains active (see dayrate chart). Norge at $497k is positive readthrough for Odfjell Drilling, whose semisubs are comparable.

(3) Odfjell Drilling is a pure-play NCS with a >9% div yield and visible growth potential. Alongside Transocean Norge, their 5-rig fleet is the best in Norway. Its Deepsea Atlantic dropped its BOP to the seabed in April, though it's since been secured and is trending toward a return to work.

The strength in NCS Semisubs is also applicable to the valuation of Northern Ocean's Deepsea Mira, although Mira has been mostly working Namibia's Orange Basin drilling and appraising key discoveries, waiting for Namibia to mature into a development drilling market. TotalEnergies' Venus is the nearest FID, with more likely to follow in coming years. A return to Norway is possible for Mira, though mobilization carries costs and Namibia has promising long-term return potential.

(4) SED Energy Holdings tender barges T-15, T-16 and Vencedor were once collateral on a distressed $2.7B Seadrill Partners LevLoan issued a dozen years ago (eventually bankruptcy due to other asset troubles), but have proven resilient assets with good utilization since. Tender rigs compete against jackups as lower cost options in SE Asia and are exposed to jackup dayrate and utilization trends.

Somewhat reminiscent to me of the Shelf Drilling old 1st lien HY bonds w/ mid-teen YTM before ADES bought them, but ENH is only 0.3x leveraged so free cash flow is instead paid to equity investors. Downside: these aren't expensive to build in Chinese yards, limiting asset valuation upside. ENH currently trades at a low-to-mid teens yield on 2009–2014 vintage assets.

Middle East Conflict Readthrough: US land services, Canadian oil sands E&P and Brazil, Guyana deepwater E&P are early beneficiaries, with shallow water jackups most impacted (Middle East 35-40% demand) and a short-term negative, but long-term positive read on deepwater rigs #oott

(1) The Middle East accounts for 35–40% of global jackup demand, making shallow water the offshore segment most exposed to the current conflict. Saudi Arabia alone represents 13–17% of jackup demand, with the UAE, Qatar, and Kuwait adding materially to that figure. The Middle East is a low-cost production region that has historically supported jackup market stability, though subject to geopolitcal risk. Borr carries limited direct exposure with only three rigs in the region, but a prolonged conflict (not base case) that drives rig relocations could pressure dayrates across the jackup market, which appears unlikely thus far.

(2) Borr’s 10% 2028s (B3/B-) are still well-bid at 103 but down 1 ¾ pts. Borr enters 2H26 with 48% of its fleet open at a $139k average dayrate. Diversification across the GoM, West Africa, SE Asia and Europe should support utilization at current oil prices, though dayrates may depend on conflict duration and whether Mid East rigs are ultimately relocated (not expected)

Watch Item: Saudi Aramco has more influence over the jackup rig market than any other operator. It’s MSC-13 capacity expansion tightened the market in 2022–2023, only for Aramco to shed over 10% of global supply as prices weakened in 2024–2025. The program targeting ~700k bpd growth via Berri, Marjan, Zuluf and Safaniya was put on hold in Jan ‘24.

(3) US land services benefit from shale's short-cycle E&P capex, with natural exposure to the front end of the futures curve with >$30/bbl above 2028-2030 levels and geopolitical stability. Canadian oil sands E&P’s combine a low-decline production profile with minimal incremental capex requirements, generating strong free cash flow with low geopolitical risk.

(4) Deepwater's long-cycle nature limits its direct exposure to elevated spot oil prices. A small share of floater demand — roughly 2–3% — is tied to East Med projects in Israel and Cyprus, with some work expected for 2H26. Deferral into 2027 is a risk, though outright cancellation is unlikely given the geopolitical importance of the region’s gas supply (Egypt).

Longer-term, deepwater stands to benefit as energy security becomes a higher-order priority following the supply shocks of recent years. Large, import-dependent economies have strong incentives to develop domestic offshore resources with Turkey's successful Black Sea program, and India's deepwater ambitions having early-stage potential.

(5) SPR Releases are a Curve-Flattener: The futures curve is in steep backwardation, reflecting near-term supply disruption premiums. While the front end has risen sharply, coordinated SPR releases are designed to cap the move which likely results in a modest curve flattening. Longer-dated prices may find support, however, from future SPR refill demand.

Long-term futures in the low $70s for 2028–2030 remain sufficient to generate returns on greenfield deepwater developments, supporting FID potential.

Mr. Market continues to hit $MELI for spending a couple years making sure they rapidly & profitably compound for several more years.

They’re being punished for focusing on long-term e-commerce market share & growth vectors instead of optimizing near-term margins to meet a sell-side EPS estimate.

Their markets are gigantic & relatively untapped. They should be staying aggressive right now.

I think they’re absolutely making the right decision for shareholders.

Time will tell.

$NE 4Q25 “Adj EBITDA” of $232mm just tad light by ~$10mm to some estimates. 2026 EBITDA guide w/in range

2026 Capex guide of $590-$640mm is a bit elevated. Going to have to justify the GreatWhite upgrade decision, but I think is reasonable because it’s a unique opportunity 🇳🇴

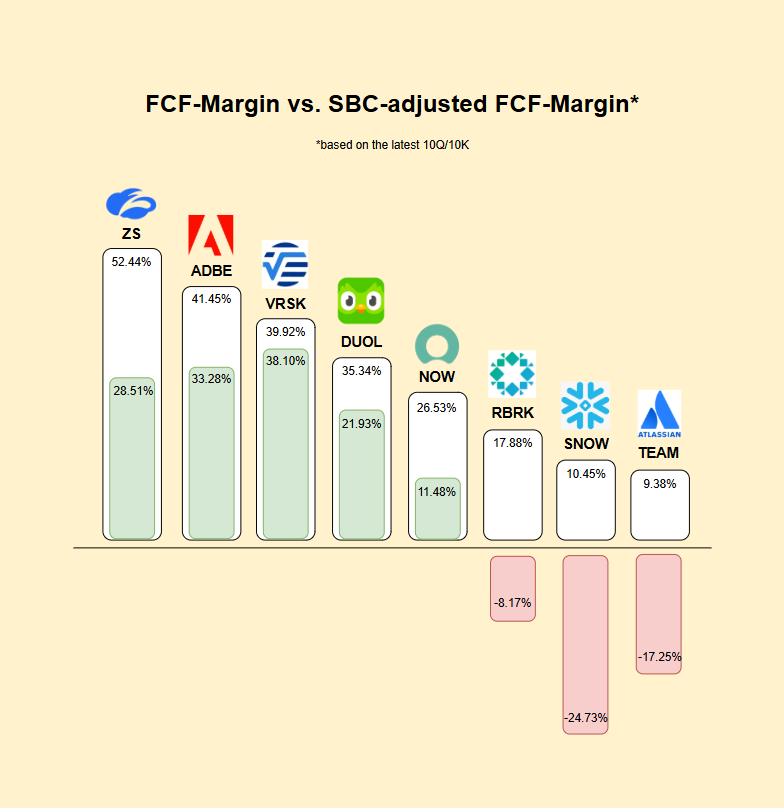

Some companies make real money, others just pretend to!

$VRSK FCF-Margin is almost identical with the SBC-adjusted FCF-Margin ✅

$ADBE and $DUOL also look good!

$RBRK, $TEAM and $SNOW are only profitable because of stock based compensation

"A wolf in sheep's clothing"

@CapitalObserver@Globalmess65 From your pov better sell puts on elv or ci down here? I own CI shares. Wouldn’t mind getting some cheap elv either although from the two CI should do better.

@SayNoToTrading Cloudrunner is the more stable one. Cloudsurfer is the faster one. I was so pleased with them that I bought the stock finally as it dropped to 45 😀

@StockMarketNerd $ONON Bought the stock after buying the runners although I must admit I was a little too early. Products are very comfortable, high quality, and looking good. Bought the second pair after just a couple of runs with the first one.

@CapitalObserver@RemindMe_OfThis I have CI, ELV and CROX. I’m thinking a rebound in the consumer discretionary might push CROX up. CFO bought shares mid August. Last time she bought in 2022 at 54 it went x2 in 6 months. A lot of bad news already priced in.

The best investor I know in % terms is a 65 year old woman who’s only made a single trade.

Couple years ago I was in CO for a friends wedding and mingling as one does. An older woman at the bar starts talking about her divorce and how she’s deciding what to do with all the money.

“So what did your husband do?” I ask, out of curiosity.

“Nothing. He’s a deadbeat.” I’m kind of interested / a little tipsy so I continue. “Family Money?”

“No, he’s broke as shit.”

Now I’m really confused. With probably not that much tact, I ask her how she’s got all this new money to spend from a divorce if her husband was a broke deadbeat. I know this story will seem fake, but I swear on everything that’s holy to me this actually happened. She says to me…

“Back in the 80s, I worked as a receptionist for CBS. And one day, this guy comes in with a rep from Chiat Day. I have to tell you, this guy has the most charisma of anyone I’ve ever met. He’s looking to run ads - we had the super bowl that year, and he talked my ear off about what they were planning. Anyway, I spoke to him for all of 10 minutes but it stuck with me. I took my entire last month worth of paycheck’s and put it into his stock.”

So you’ve probably guessed by now, the guy was Steve Jobs and the stock was Apple, but here’s where it got really funny. She explains all of this and I’m thoroughly enjoying hearing it because I already know the story of Apple’s 1984 super bowl ad. She continues…

“So I actually forgot that happened until a couple weeks ago. My husband and I are getting divorced and I called Fidelity, and told them I needed to get some documentation for the account for that. And they said ‘which account?’. I didn’t know I had two accounts, I figured I only had the one for the 401K. And they say ‘well there’s the 401K and then there’s another with about 6 million in it”. That was the stock I bought!”

So, yeah, 252,000% of unrealized pnl not including dividends. But her husband ended up getting half, so who’s the better investor?

@WealthyReadings Not that I own 2 pairs as of June but I switched after 12 years of NB. The launch of wide models for running was decisive for me as I wanted to use them since 2014 but were impossible narrow in the front for my feet. Glad they diversified 😀

$NU had massive FX headwinds this quarter, which led to 1.5% QoQ growth when it would have been 9% growth on a FX-neutral basis.

9% QoQ growth is incredible at this scale. And this is by far the worst FX quarter in the history of the company. the Brazilian Real bottomed right at the end of Q4 and has already rebounded since then. This headwind is already reversing.

$NU is a one-of-a-kind company. They have an incredible moat, have proven their ability to scale their operations across national borders, still have so many verticals to exploit with the existing subscriber base, and have plenty of geographies to continue expansion.

If you want to sell a company with an obvious moat and an obvious growth runway for years to come at a FWD PEG of 0.6 because of currency headwinds, I don't know what to tell you. It's getting a heavier weighting in my weekly DCA at this level. I think they can get to a market penetration of 50%+ of the rest of the big LatAm markets (Mexico, Colombia, and Argentina) as they do in Brazil. That's to say nothing of geographies outside of LatAm. I'm happily adding shares into weakness.