Bitcoin cayó de $0.17 a $0.01

Luego de $32 a $2

Luego de $266 a $63

Luego de $1,166 a $170

Luego de $19,783 a $3,122

Luego de $68,891 a $15,479

Luego de $126,272 a 57,734

Un día caerá de $21M a $9M

Preferiría simplemente mantener USD porque es estable

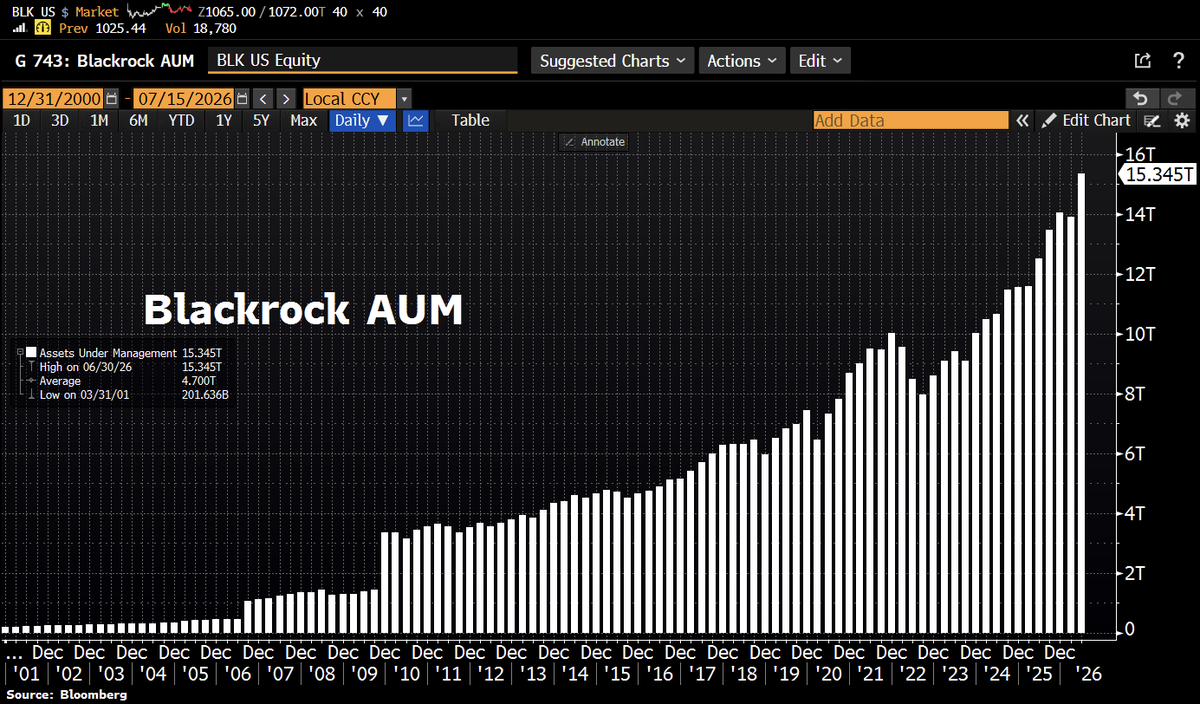

BlackRock is eating the world. The asset manager just crossed $15tn in AUM for the first time, powered by $192bn in Q2 inflows and a record $321bn in H1. ETFs alone pulled in $178bn, revenue jumped 31%, EPS beat. Scale is becoming the ultimate moat.

Largest inflation decline in over six years. Core inflation comes in at 2.6%. Four years ago with Biden inflation was at 9.1%.

Watch the consensus crowd on Wall St execute a familiar pivot. Only weeks ago, the dominant narrative pointed to imminent rate hikes, driven by the so-called “Iran shock” and reinforced by the ECB’s tightening. The argument was framed in terms of central bank credibility: if the ECB hikes, the Federal Reserve, under Chairman Warsh, must follow.

That logic is flawed.

It rests on a narrow, demand-centric view of inflation that has long dominated Wall Street thinking, the growth is bad. The Keynesian reflex is to treat inflation as a function of excess demand, with higher rates serving as the primary corrective tool. Yet this framework struggles when inflation is rooted in supply constraints rather than overheating demand.

The second- and third-order effects so often invoked, wage spirals, tariffs , embedded expectations, are not immutable laws. They are contingent outcomes. But when supply is impaired, tighter monetary policy can exacerbate the problem rather than solve it. Basic supply side theory.

Housing offers a clear example. Elevated rates have constrained new construction, tightened inventory, and reinforced price pressures in shelter, a major component of inflation indices. In such cases, policy is not restraining inflation; it is helping to sustain it. CPI ex shelter was -0.7% MoM.

This raises an uncomfortable possibility for policymakers. If inflation is being driven, even partially, by supply-side bottlenecks, then rate cuts, not hikes, may be the more effective tool. Lower financing costs can stimulate construction, unlock capacity, and expand supply, easing price pressures over time.

That perspective has been largely absent from the policy debate for decades. But as the limits of demand management become clearer, it may be due for reconsideration.

For Chairman Warsh, the implication is straightforward but politically fraught: credibility is not established by reflexively tightening in the face of inflation. It is established by correctly diagnosing its cause. If the source lies on the supply side, particularly in interest-sensitive sectors such as real estate, then easing policy, yes Rate Cuts, may be the more credible response.

Como les he dicho muchas veces la IA no es deflacionaria como fácilmente se compra, sino inflacionaria. Los costes están aumentando más rápido que la productividad, y el auge de la tecnología está absorbiendo recursos a un ritmo bastante mayor del que genera beneficios.

Las revoluciones tecnológicas anteriores, como la electrificación y la Revolución Industrial, requirieron años, e incluso décadas, antes de que se reflejaran mejoras significativas en la productividad.

Durante la fase de inversión, las presiones inflacionarias solían aumentar antes de que se materializaran las mejoras en la eficiencia.

Y a eso añadan que los estados aprovecharán cualquier mejora en la producción para ponerse las botas a imprimir papel, regular, intervenir, etc.

THIS IS HOW THE S&P 500 HAS PERFORMED EVERY YEAR SINCE 1928

The market finishes positive roughly 73% of all years.

Here is the full breakdown by return bucket:

More than +40%: 5 years

+30% to +40%: 17 years

+20% to +30%: 14 years

+10% to +20%: The biggest bucket. Most years land here.

0% to +10%: 14 years (2026 is currently here)

-10% to 0%: 12 years

-20% to -10%: 9 years

-30% to -20%: 6 years

-40% to -30%: 2 years (2008 and 1937)

More than -40%: 1 year (1931 only)

Out of 98 years, the market has been positive in roughly 72 of them.

Which of these would you choose to hold for the next 5 years?

A)

Nvidia $NVDA

Apple $AAPL

Google $GOOGL

Microsoft $MSFT

B)

SpaceX $SPCX

Anthropic

OpenAI

Databricks

C)

Amazon $AMZN

Eli Lilly $LLY

Walmart $WMT

Berkshire Hathaway $BRK.B

D)

Micron $MU

Nebius $NBIS

CoreWeave $CRWV

Iren Limited $IREN

NVIDIA presentó resultados... Y demostró por qué sigue siendo la compañía más importante del mercado.

- Ingresos: 81.620M$ vs 79.190M$ esperados

- BPA ajustado: 1,87$ vs 1,76$ esperados

- Margen bruto: 75% vs 74,5% esperado

¡La demanda de IA sigue acelerándose!

BREAKING: SpaceX has selected Goldman Sachs to lead its record-setting IPO, per CNBC.

Also working on the IPO will be Morgan Stanley, Bank of America, Citigroup, and JPMorgan.

SpaceX could publicly disclose its prospectus as soon as Wednesday.

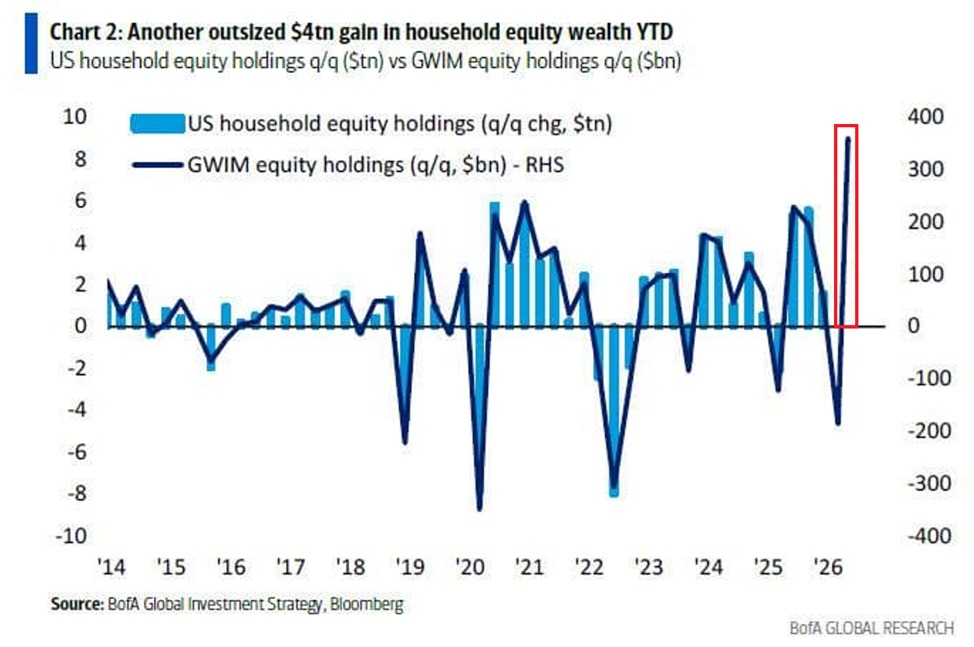

BREAKING: US household equity holdings are up +$4 trillion year-to-date.

This follows +$10 trillion, +$9 trillion, and +$8 trillion for in 2025, 2024, and 2023, respectively.

Since 2023, US equity holdings have surged a massive +$31 trillion in total.

Households now own ~40% of the entire US equity market, the highest percentage in at least 20 years.

This is followed by foreign investors at 18%, active mutual funds at 10%, ETFs at 10%, and pension and government retirement funds at 9%.

Asset owners are winning.

China deja de comprar el petróleo de Irán, y ha en su lugar compra petróleo estadounidense. en su lugar.

Trump cerró el Estrecho y redirigió la demanda china de petróleo EEUU.

Esto es ajedrez y Trump gana.

Bill Ackman started a 15% position Microsoft.

Meanwhile, co-founder Bill Gates has fully exited his position.

One sees risk.

One sees opportunity.

Microsoft remains near 10-year low valuations.

$MSFT

BREAKING: President Trump says "the great" Jensen Huang of Nvidia, $NVDA, is currently on the Air Force One with him on the way to China.

Trump says Elon Musk, Tim Cook, Larry Fink, Stephen Schwarzman, David Solomon, and many other CEOs are joining him on the trip.