Hidden Credit Lines Scandal:

From Irish customers’ files research.

A Q&A

What disclosures were made?

Key risks, mark-to-market liabilities, or credit implications were not explained at all - let alone adequately explained. Some mention of “break costs” when asked but staff said minimal if asked.

@labourlewis Too many victims of RBS GRG, fixed mediations and failed compensation schemes were also left without proper justice or full recovery of their losses.

Many lost businesses, homes, pensions and years of their lives, while banks moved on untouched.Accountability should apply to all

There are three types of people in the world.

The first group does what the authority tells them without questioning it. Often because they strangely believe that the authority knows best and is benevolent.

The second group doesn't actually want to do what the authority commands, but they're afraid of the consequences if they don't obey.

These two groups have been behind every tyranny in history—every single one—because without them, tyrants couldn't rule; they're simply not strong enough.

The third group is growing and says: 'I see what you're doing, but I'm not going along with it.' This group has ended every tyranny in history.

Today I read a judgement emanating from our Court of Appeal.

As a legal professional, it truly sickened me.

🔹Supernatural and derisive imagery was applied to the defendants’ arguments. It was and is unnecessary.

🔹Unnecessarily pejorative characterisation of pleadings

🔹Several passages imputing bad faith on the part of lay litigants

🔹Colloquial pejoratives

🔹One paragraph is the most concentrated and the most striking

🔹Within the same paragraph the judge expressly acknowledges “the first defendant’s entitlement to be treated with respect and courtesy” and, in the same breath, deploys

“daft”,

“anyone with a titter of wit”, and

“ridiculous”.

The juxtaposition is itself as revealing as it is cringeworthy.

🔹Characterisation of non-parties associated with the defendants - described as “a mob”.

Why?

🔹The word is repeated and is not qualified by reference to evidence of any mob-like conduct whatsoever.

🔹A more neutral formulation (“a group”, “the persons who re‑entered”) was available to the judge.

🔹Many editorial asides that are completely unnecessary to the legal reasoning more fitting to a judge of such seniority;

🔹The rhetorical disposal of the appeal in three words prior to any analysis.

🔹Embarrassing and not for the lay litigants

🔹The cumulative footprint is substantial.

🔹Rhetorical or pejorative material appears in at least eighteen numbered paragraphs.

🔹The appellants’ arguments were approached with a settled view, in a manner inconsistent with the appearance of impartial appellate adjudication.

🔹Having been at the receiving end of this when indeed underlying fraudulent activities were being conducted, I’m extremely concerned.

🔹Robust reasoning is one thing. Courts are no doubt entitled to be firm but litigants are entitled to be heard without being mocked.

🔹Is this the register we want from our appellate courts?

Yesterday’s refereeing was one of the best I’ve seen in a long time.

For the first 15 minutes, the ref fell for Arsenal’s shenanigans: blowing a foul for every slight fall and every little touch. Then, all of a sudden, he clocked their dirty antics and took complete control of the game.

He stopped buying their silly theatrics: Mosquera time wasting, Havertz falling at every slight touch, Saka wasting time for the corner, Arteta touchline tantrums, Madueke diving. I can go on and on

Arsenal have become so used to getting away with this cunning stuff from Premier League refs that they seemed genuinely shocked when it didn’t work.

I’m glad the referee refused to be intimidated and stood his ground. That’s how you referee a final.

You might con your way to a Premier League title, but you can’t do it in the UCL. Either you play like real men or go home

Prison for role in pension fraud scheme. No clear difference between this fraud scheme and the orchestrated fraudulent sale of derivative / swap transactions by Ulster Bank and Bank of Scotland Ireland…

https://t.co/7XYMFXrO6h

HE WROTE "0800-F***-YOU" TO AN NHS WHISTLEBLOWER. THE TRUST GAVE HIM AN AWARD.

A few weeks ago I posted Sharmila Chowdhury's @sharmilaxx story. That posts reached nearly 800,000 views. Thank you. That number tells me people understand exactly how serious this is. So let me give you one more detail from this case. Because it deserves its own post.

Quick recap for anyone new here. Sharmila gave 30 years of spotless service to the @NHS. She caught two consultant radiologists at Ealing Hospital billing the NHS while working privately down the road. She reported it.

They sacked her on fabricated allegations and blacklisted her across the NHS. She won at tribunal. They ignored it. She developed cancer. They carried on.

Now here's the detail.

The man who made those fabricated allegations against her was Mike McWha, the PACS/RIS manager at Ealing Hospital NHS Trust. The same Mike McWha who had already failed to upload nuclear medicine reports for approximately 100 patients over six months. Patients with potentially life-threatening conditions. Sharmila had formally raised that against him in writing before he turned on her.

He also sent an email signed off "0800-F***-YOU-B****."

That same year, Ealing Hospital NHS Trust put Mike McWha in their Annual Report and gave him the "Top Mentor" award.

Not a disciplinary hearing. Not a formal investigation. A published award. In the Annual Report.

Sharmila was escorted out of the building in front of her staff. Her colleagues were warned they would face the same treatment if they contacted her. Her name was removed from her office door within two weeks. Her post was advertised while she was still suspended.

Twelve staff members submitted written statements in her support. The Trust ignored all of them.

She won. He got a plaque.

Nearly 800,000 people looked at this case and said this matters. It does. Share this one too please.

Full case: sharmilachowdhury com

Sources: Health Select Committee written evidence | @guardian | @BBCNews | @Channel4 | @DailyMail | @Independent | @thetimes | @DailyMirror

It is clear now that

🔹the Irish Banking Inquiry and indeed the Dutch de Wit Commissions were permitted to say

🔹”the banks ran a customer funding gap”

but

🔹they were NOT permitted to say

🔹”and here are the specific instruments by which they hid the consequences from their own customers and from the public.”

🔹The instrument-level story is omitted:

⚜️the securitisations,

⚜️the swaps,

⚜️the all-monies clause,

⚜️the GRG-equivalent workouts (or Dutch equivalent)

🔹precisely the missing layer, between the Inquiry or Commission’s deliberately crafted macro narrative and the lived experience of the Irish / Dutch SME.

Explaining why numerous individuals simply could not be permitted to give oral, written or any testimony at all.

Explains also the visible levels of stress ingrained on the faces of some of “the actors” brought in to run a rigged show.

Some from @AskAIB - some who even went to @AskAIB mid or post Banking Inquiry.

Ironic to post this just after the CFO of @AskAIB steps down for what we are to believe are new business opportunities.

@Wftproof@stevemiddi1@BankConfidenti1@WhistleIRL

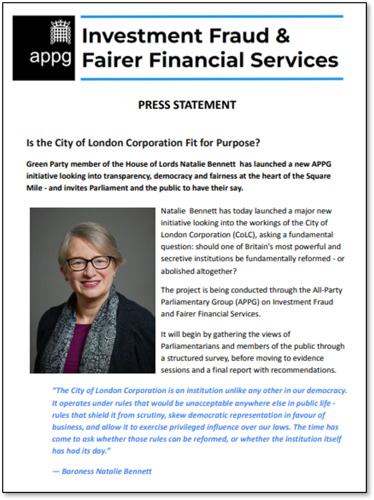

📢 We are pleased to share a press statement regarding an important new project that the APPG on Investment Fraud and Fairer Financial Services has embarked on.

It’s about looking into the City of London Corporation; and very importantly it’s about inviting you to have your say, via a short and simple survey.

The project examines whether the City of London Corporation should be drastically reformed or even abolished altogether. Perhaps reform or abolition could lead to a significant reshaping of our financial services landscape, for all the good reasons given in the statement.

This initiative is being led by Green Party member of the House of Lords Natalie Bennett @natalieben .

And if you do want to take the opportunity to have your voice heard please complete the online survey, which is available for you here; 👇

https://t.co/iGJe7zQIyL

we won’t be publishing respondents; email addresses or names, so please do take this opportunity to share what you think.

Why is this issue so relevant to TTF members?

Because the project is all about exploring whether the City of London Corporation is as fair, democratic and transparent as it should be; and as you may already know the City of London Corporation has a significant degree of influence over how the financial industry is run - the press statement explains the ‘interesting’ role of the City Remembrancer, whose job is to influence financial services legislation.

The full statement is available for you here 👇

https://t.co/EdNH72kzPu

So many ask me about false & misleading pleadings and affidavits that go further, and positively assert there was no swap, no derivative, no ISDA-referable product - just a “fixing of the interest rate”.

🧵

1/ In Promontoria/Cerberus-style enforcement, I have seen pleadings characterising the sum as a “loan”, a “facility break cost”, or a “contractual early repayment fee” - with no mention of a derivative, of a hedging product at all.

2/Where the originating bank’s own records describe the product as a swap and the customer simply signed an advisory note unsigned by the bank - having been told it was “for protection”, a pleading that denies a swap or derivative is not a drafting choice. It is a representation to the court.

3/ Under the Solicitors Guide to Professional Conduct, a solicitor must not make, or permit, a statement they know - or ought to know - to be false or misleading. That duty runs to pleadings, affidavits and open correspondence. It is not discharged by client instructions alone.

4/ The deeper exposure: an affidavit grounding summary judgment that swears the sum is due on foot of the loan, when the break-cost component is in truth a close-out of a derivative the bank never validly contracted - risks crossing from misleading into misstatement on oath.

5/ Remedies are not theoretical.

Courts can strike out pleadings, refuse relief, and refer conduct to the LSRA.

SMEs can plead the asymmetry, seek discovery of internal product records, and reserve duty-of-care and misrepresentation claims against the solicitors involved.

If I never had another conversation in my life again with lawyers instructed to “support clients” taking on the banks & their minions it would be too soon.

I believe we should push for a regulation defined by days of the week.

e.g. if you’ve argued black is black on a Monday you can’t argue that black is white on any other Monday.

Let’s build a simple system that makes lawyers consistently give honest opinions & tell the truth by days of the week or simple markers like

GREEN = the Truth.

AMBER = I thought I was telling the truth but f***ed up

RED = I was always incompetent/lying until you caught me out.

At that point those dimwits like me would understand how facts, evidence & criminality by “officers of the court” become judgments.

It’s not a lot to ask.

Please could the SRA & BAR Standards set days on which lawyers have to be honest & advise their clients honestly…?

It would save financial fraud victims years of deception, the courts years of impossible claims & the legal system having to completely falsely promote/ defraud the public that Justice exists in law firms & courts in the UK.

Unless you are protected by the City.

@BankConfidenti1@MLorrM@TransparencyTF@BomberMorgan@CarshaltonArt@mickmor16921994@bleating_lamb@efgbricklayer

Richard I appreciate the work you post, as many people do, I work with @TransparencyTF they have an All Party Parliamentary Group meeting on 15 June.

At the support of @premnsikka they are also running a meeting in the Parliament Committee rooms on how banks & others weaponize insolvency to destroy/control fraud victims, on the 7 July, would you be interested in attending?

@RichardJMurphy We were not a distressed business. We were profitable, employing people and paying taxes — until RBS/GRG intervened. Nearly 20 years later, the damage to businesses, families and livelihoods is still being felt.

@Independent Interesting how BDO became our administrators after the RBS GRG / IRHP collapse, then later resigned citing a “possible conflict of interest” because staff had been seconded to RBS Bank.

Looking back, many SME owners are entitled to ask serious questions.

@UKSFO RBS GRG destroyed countless businesses and lives, yet many victims are still waiting for real accountability while those responsible walked away untouched.

Bank fraud and misconduct should be treated no differently to any other fraud.

HE BLEW THE WHISTLE ON THE FINANCIAL CRISIS

Tom Hayes spent 5.5 years in prison for "rigging" LIBOR. Serious Fraud Office called him the ringleader. The judge gave him 14 years. The media called him greedy and corrupt.

There was just one problem.

The Bank of England and the UK government had secretly been telling banks to lower LIBOR rates during the 2008 financial crisis. The people who actually gave the order never saw a courtroom. The junior traders who carried it out went to jail.

@BBC economics correspondent Andrew Verity @andyverity spent years collecting what the authorities didn't want you to hear.

Secret recordings. Internal documents. Sources who couldn't speak publicly. He turned it into a Panorama film in 2017, a Radio 4 podcast called The Lowball Tapes in 2022, and a book called Rigged serialised in The Times in 2023.

In July 2025, the UK Supreme Court unanimously quashed Tom Hayes's conviction. The jury had been misdirected. The trial had been unfair. The @UKSFO said it would not seek a retrial.

No central banker has been charged. No government official has been charged. The people who gave the instructions are still fine.

This is what whistleblowing infrastructure actually looks like in practice. Not a hotline. Not an HR form. One journalist, a handful of anonymous sources, and eight years of dogged work that the establishment hoped would go nowhere.

It didn't go nowhere.

Sources: @BBCNews Panorama 2017, BBC Radio 4 The Lowball Tapes 2022, The Times serialisation of Rigged 2023, UK Supreme Court ruling July 23 2025

The idea that interest rates are used to slow inflation is a myth, Michael Hudson argues.

'The guiding fiction is the idea that rising interest rates will slow price inflation by reducing bank credit creation and thus investment and employment. The fiction is based on the myth that banks help the industrial economy by creating credit to lend to companies to expand the economy. But that is not what banks do under the finance capitalism. They lend against assets already in place and available to be pledged as collateral, for the purpose of buying more real estate, bonds and stocks. The effect of these loans is to inflate asset prices, not consumer prices.

'Governments and their central banks may pretend to be lowering interest rates to spur the economy, but the basic reason is to re-inflate prices for financial securities and real estate.

'That’s the main aim of today’s finance capitalism, after all. Its aim of increasing fortunes by creating debt-leveraged asset-price gains has turned economies into a great Ponzi scheme.'

Read/Watch the full interview here: https://t.co/nuVzQm2snx

#Economics #InterestRates #Inflation #GlobalEconomy #Finance