Citadel fired their best quant. He rebuilt their entire algo with Claude Fable 5 in 48 hours - and he's up $430,000 trading it against them.

He didn't take a single file. He didn't need to - ten years of that logic lived in his head, and you can't raid a memory.

Wallet proof: https://t.co/JSA6VkmGuX

Here's the engine MiroFish runs - and it's rigged in his favor. Picture a Galton board: a ball dropping through eight rows of pegs, bouncing left or right at random.

One ball is chaos. Thousands of balls always fall into the same bell curve. That's the law he weaponized.

Every ball is one trade. Each row is a volatility gate - news, liquidations, order-book flow, things nobody controls.

On a fair board every gate is a 50/50 coin flip. His model tilts each one to 0.54 - four cents of edge that only shows up when fair value splits from the book.

Four cents sounds like nothing.

Compound it through eight gates, thirty-two thousand times, and the whole bell shifts right of breakeven: 71% of trades land green.

$93 of edge per trade. $430k across the distance.

Watch the win rate converge in real time - it swings between 50 and 85% for the first few dozen trades, then locks on 0.71 and never leaves.

He doesn't predict a single trade. One trade is a coin flip. Eighteen thousand is mathematics.

They thought firing him protected the edge. They just handed it a grudge.

Copy the wallet quietly out-trading a $60B fund before they connect the dots: https://t.co/vbDZyVcfT3

Here's a bunch of random 30 US-available random stocks I like today and why:

1. $INTC - America's hope for foundry, national security

2. $MRVL - scales rev from future maia asics and add ons like cpo, they do everything lost count

3. $TSM - backbone of semis/ai

4. $COHR - They do everything vertically integrated + captures optical cycle

5. $RKLB - the final frontier of space will be around 5 years from now and 20 years from now.

6. $DRAM - memory exposure for samsung/sk hynix

7. $AVGO - hyperscalers dont like nvidia gpu tax

8. $AMZN - nobody can compete against the overnight shipping of toilet paper. robotics will lower opex over time

9. $ARM - AGI CPUs scale revenue quite a bit over the next decade

10. $TSEM - you're going to need a foundry for light based stuff

11. $IBIT - bitcoin, we all know by now

12. $NBIS - i think it's the next AWS. Also they do self-driving cars with uber, own scaling DB companies, data labeling. It's almost like a mini Google.

13. $GOOGL - youtube is not going away, gemini is great. they're vertically integrated with TPUs and fund buildout with operating income so i like it.

14. $AMKR - super facilities coming online in late 2027-2028. benefits from made in america

15. $HOOD - i dont like short term, but long term i'm a fan of Robinhood since they captured retail + have more products like banking, etc that they're scaling up. product innovation is wild.

16. $CRCL - I happen to really like stablecoins and see them as the future for both payments/holding (depends on clarity act)

17. $META - people aren't going to stop using instagram or whatsapp, or others anytime soon.

18. $LITE - $GOOGL TPU exposure decently high part of BOM. As long as Google's AI program keeps running I think $LITE will do well.

19. $LPTH - Germanium and China export controls will always be an issue so US made engineered alternatives will always be important

20. $FN - Someone needs to assemble optical stuff

21. $JBL - same as above, but added with ip from Intel's SiPh acqusition so might end up like innolight?

22. $MP - American rare earths program is extremely important, similar to $INTC national security risks

23. $HIMS - Okay here me out they just acquired a ton of companies, and at $19 they have global DTC channel. short sellers really hate this company, but I think it's actually promising as a contrarian long

24. $SMTC - LRO/LPO transition

25. $POWL - US alternative to hammond for switchgear DC type bottleneck

26. $VPG - Humanoids will be a thing down the road maybe 2027-2028, this makes the sensors.

27. $MOG.A - Feels like i see them everywhere in robotics, to spacex supply chains

28. $MSFT - At $375, one day we'll look back and see this as a buying opportunity.

29. $CVX - oil might crash after war but these oil companies are going to be extremely important, especially when Venezulea is a goldmine.

30. $XLU - i think rate cuts might be back online, we need power/grid for AI so these names will always be improtant from $CEG to $NEE

Just throwing out other thoughts aside from $AAOI and $AEHR.

$SIVE is my favorite CPO / photonics stock after AAOI.

Partly because it's Swedish and you have entertainment from comedians over there.

Today a new non-technical hedge fund called Protean Funds (likely shorting), went on air.

To said $SIVE CPO applications are imaginary.

Right after $GFS just made $SIVE their reference laser.

(Just for some context to newer readers: Lot of people in Sweden can only look at past 12 month revenue, and don't understand concepts of forward growth)

Also because they don't understand that no CPO application has scaled up yet at all.

So Swedish hedge funds keep going short (with many of their hedge funds like Colosseum / Origo heavily underwater).

But... for the technical readers... from H2 2026 to 2028, it goes from near $0 to $91B TAM in 1 1/2 years. (we're entering H2 now).

Overall TAM hits $141B (which is also 10x+ or so in 1 1/2 years)... and $SIVE has scaled into pluggable market with $JBL + other unnamed pluggable players with that too.

Probably not going to end well for the local Swedish firms, shorting right before the largest inflection points ever hits for $SIVE.

Just a matter of time before volume ramps.

Just very helpful timelines reiterated around glass substrate (source: Trendforce):

- SKC Absolics (011790) H2 2026 (first mover x $AMAT) - $AMD customers

- Samsung electromechanics h2 2027 (009150) x Sumitomo Chem (4005) - Apple / $AVGO / hyperscalers

Idk about $INTC 2030 reports, we’ll see.

$TSM CoPoS was 2-3Y was correct though from recent TSM chairman comments. Innolux was interesting beneficiary. $SHMD should be too off TSM but financials were pretty toxic.

Same players should appear multiple times, eg innolux + SKC.

Also applies to $LPK and upstream equipment seller around these ramps.

I think my personal style of investing is a bit different, just some reflection:

It's inherently discretionary, based on stuff markets don't know yet. And a culmination of life experiences?

If you look at $AXTI, $RPI, $SIVE, $IQE and others.

Lot of it is guessing on unstructured relationships then seeing if it's right or not down the line.

$RPI is the perfect example:

1. Nobody really thought of Raspberry Pis for AI growth. Mainly people bought one or two just for class + education + hobbyist.

2. After OpenClaw, just noticed all my friends and people just buying Apple Mac Minis / RPIs for AI applications.

3. Found validation of that trend online with lot of people sharing video tutorials on AI orchestration with RPI.

4. AI was their ideal perfect growth vector, did some modeling, and thought it was compelling.

Earnings comes out and I was right.

Everyone in media was calling it a meme stock because there's nothing online that shows revenue growth from AI (was 14% forecasted revenue growth, turned out to be 58%, my projection was around 55%).

So it was a mix of guessing next industry trend (AI using lightweight hardware instead of GPU clusters), real life trends, then revenue forecasting off my guess.

For stuff like $AXTI:

1. Everyone called it a joke when I bought at ~$12. LLMs would hallucinate and say "hyperscalers/govs would have known about this by now and fixed this vulnerability with InP substrates"

2. Or would conflate very nuanced parts of InP substrate stack, where there's multiple different chokepoints in upstream processing.

3. So part of this was just discretionary based on what I've seen over InP substrate breakdowns, industry trends, etc.

4. Then also guessing the major supercycle was photonics (this was before everyone caught onto $LITE, and others). Or before you saw the $141B TAM projections from GS.

5. AXT owned 40% of InP supply chain, without them the supply chain just gets cripped).

6. All the "analysts" were forecasting steady InP substrate growth, few hundred million TAM, etc. or export controls.

7. Everyone kept trying to say $AXTI was overvalued based on TAM estimates. But if it's a few hundred million TAM you just think that's a joke and go into game theory over allocations.

8. Then I just had to guess, how much would this be worth if it were a NAND style bottleneck, what MC could it reach based on control, how much would hyperscalers price it as, etc.

A lot of the current research outputs from Goldman Sachs, or earnings reports from the Epiwafer companies, were confirmed after I published my piece on AXT. If you did research back then, lot of the same material /framing wouldn't have come up.

With stuff like $XFAB as you're seeing now, a lot of it is just pure guessing:

1. Not really any CPO materials, how much their MTP process makes in revenue, etc. Everyone online keeps saying they're not a photonics player.

2. But if you go through ASE docs or Gov websites, they all kinda cite XFAB as a major emerging player here.

3. $NVDA also evaluating them right now (maybe it's successful who knows).

4. No clear revenue around this area because their main silicon photonics process is still precommercial, but if you guess it's trying to create a EU supply chain to compete with $TSEM, once pre-commercial shifts to commercial, maybe similar but less volume contracts?

5. Then just seeing updates over the next few months to see if anything confirms this thesis guess.

_

I think a lot of information discovery still can be done with LLMs I'm seeing online. But it's also really hard to make a bunch of unstructured inferences based on unrelated material or even just trends you're seeing in real life.

So probably better to just do what's standard, eg. do valuation forecasting based on current numbers

Stuff like $AAOI, if they're projecting $471m/M h1 2027 and you see MC at $12B, probably undervalued might be a good idea to go long for next years.

Stuff like Samsung Electronics is easier, see what people are modeling for operating profits for 2027, 2028 then just seeing if it's undervalued or not at current levels.

Maybe something harder is $JBL. I haven't really seen any great volume numbers around 1.6T LRO, but you can just make a guess on how popular that might be then project how that might impact current MCs.

Or picking just good names everyone kinda agrees like $TSM, $INTC, $MRVL is also solid.

So a lot of things is just building up your life skills then applying that to markets. I don't think it's that can be taught with courses and stuff.

Of course, much of what I'm doing is just high conviction inference based on unconnected parts. Could always be wrong.

Just some mobile shower thoughts around $XFAB and train of thought:

1. 800vdc $NVDA push look for GaN/SiC players / power semis.

2. $NVTS and other fabless/fab-lite beneficiaries of $NVDA push probably use foundry models

3. care more about Western supply chains over Asia, want to build up Western capabilities + Western premiums.

4 China has a lot of capacity, maybe risk into 2028, but again it’s building up Western supply chains

5. XFAB only high volume SiC foundry in America (others like $ON or Infineon are vertically integrated)

6. advanced 6in SiC, 8in GaN on Si, building out 8in GaN

7. Maybe likely they’re developing 8in SiC from CHIPS backing, just not public material

8. check SiC revenue -> 152% Y/Y growth okay. Probably something markets missed, since blended looks worse from automotive slump, that should come out recovery

9. $NVTS and others turns out to use $XFAB. $POWI cites $XFAB in filings, among others.

10. both are $NVDA power semi explicit partners, great exposure indicator to 800vdc power semi players.

11. US Dpt. of commerce cites $XFAB as only high volume SiC foundry in the US, $50M PMT

12. validation from US Gov about critical component in supply chains is amazing

13. EU CHIPS Act gives $XFAB $128M EU, for foundry (MEMS, AI, etc), okay turns out they’re critical MEMS player

14. So that’s validation from EU gov about critical component in supply chains, dual continent subsidies

15. So now we know $XFAB is a critical MEMS foundry so you get SiC capabilities, GaN development, and MEMS upside

16. they also got $47.6M EU funding for leading Silicon Photonics supply chain in EU. So that’s EU funding on multiple angles.

17. Turns out, I know all the players there from smartphotonics from $GFS deck.

18. $NVDA and $NOK are qualifying them for silicon photonics HVM. I think this is just a government backing angle for success in EU photonics so likely to succeed… kinda like how Us gov encourages everyone to use $INTC.

19. Okay chips act 2 is coming out next week… so they’ll probably get funding there or more revenue commitments

20. 1.28 p/b, now that’s probably just book cost? Likely coming out of $SOI type legacy drag cycle.

21. Did some modeling around actually replacement values, true replacement p/b cost likely ~.5/.7.

22. Getting business for free, while having upside from SiC near term into Silicon Photonics / GaN as main growth past H2 2027.

Thoughts: derisked by p/b values + replacement value. maybe like 20% downside from macro.

However, critical dual continent importance. So downside risk seems low, but upside is compelling.

Lot of capex likely backstopped by upcoming chips act catalyst + national security concerns.

Maybe 2.5-4x rerating seems possible/likely.

Not a 10-20x, but recovery from depressed valuations from silicon photonics upside with SiC / GaN bridge.

TLDR: likely trading lower than replacement value, dual continent subsidies likely subsidize capex.

Gov grants shows importance to Western supply chains, photonics longer term upside, SiC/GaN demand likely near term upside and bridge.

Don’t control any recent volatility, should shake out anyone not really confident in the thesis though.

CHIPS act 2 from EU is coming up, $XFAB was listed in earlier blueprints for optical ecosystem, so should get a boost after that comes out as near term event catalysts.

So now is the risk reward seems compelling, we’ll see if this is right or not

Just in case people are wondering about my track record with European equities:

$RPI: $280 -> $800 (agentic AI hardware demand thesis).

$LPK: ~$6, thesis at $13 -> $24.2 (glass cores substrates close monopoly)

$SOI: $44 -> $181 (silicon photonics, monopoly over substrates)

$SIVE: $4 -> $71 (CPO, critical chokepoints over lasers).

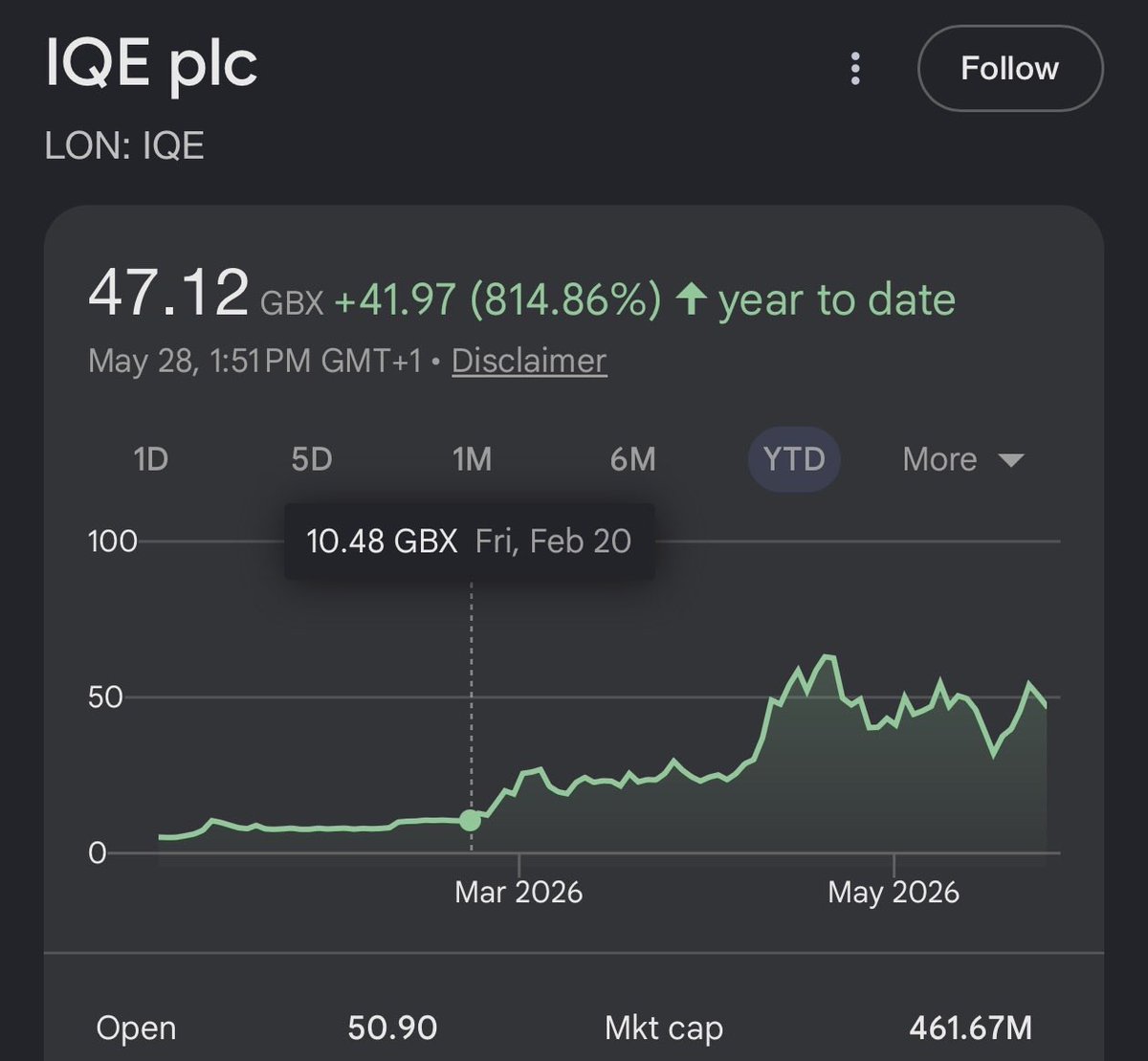

$IQE: $12 -> $47 (latent epiwafer capacity, information discovery around downstream photonics companies).

$ALRIB: $5 -> $15 (duopoly, synthesis around quantum buyers with photonics growth verticals).

And now $XFAB at $9.

I’m not always right.

But every single one of my European longs thesis have been validated so far by either earnings, investments (eg. $MTSI in IQE) or market returns.

A week ago, I gave you:

- $TE from $6 to $10 (66.67%)

- $IREN from $46 to $61.47 (33.63%)

- $CLSK from $13 to $17 (30.77%)

- $WYFI from $23 to $33 (43.48%)

- $APLD from $36 to $48 (33.33%)

- $HIVE from $3.1 to $4.3 (38.71%)

- $KEEL from $4 to $5.3 (32.50%)

Next alert dropping soon!

If you are not following us with notifications turned on, you might miss our next alerts.

Leopold Aschenbrenner is literally telling you what stocks to buy before they squeeze.

He turned $225M into $5.5B in just 12 months.

In 2025 he called out:

$SNDK at $42 & is now up 3,200%

$BE at $18 & is now up 1,500%

$LITE at $59 & is now up 1,400%

This time around for 2026 he’s bullish on:

1. $TE ~ T1 Energy

2. $IREN ~ Iren Limited

3. $HIVE ~ Hive Digital

4. $CRWV ~ CoreWeave

5. $RIOT ~ Riot Platforms

6. $CLSK ~ CleanSpark

These stocks can easily be the next to 5-10x within months.

Don’t miss out again…

I'm going to borrow this image because I think it looks spectacular

Just so you can see my position in this photonics sector:

Layer 1 - $IQE

Layer 2 - $SIVE

Layer 3 - $AAOI

Layer 4 - $LPKF

Layer 5 - $AEHR

I don't hold this last one anymore, but I used to

I'm looking forward to a good entry price to have all layers covered again with my winning horse out of all of them

This is my current portfolio

As I said, I wouldn't sell any positions

And I’ve kept my word, the money for the new position in $PENG does not come from my existing investments

At the moment, I don’t see better opportunities in the market than what is already in my portfolio

At least not at these prices

I have on my radar things like $KOPN $DGXX $SOI etc

A few of you guessed correctly that company #2 that I started a position in was Ensilica ( $ENSI)

Up 11.13% today.

I'll do a proper thesis post this week, but at just £135M MC, they own genuinely scarce RF/mmWave/satcom IP.

And are at a sovereign-supply chokepoint in the UK & EU industrial policy stack.

Still kinda early in converting a multi-yr stack of NRE design wins into recurring royalty/supply revenue.

Notably: $ASTS's AST5000 payload ASIC + a multi-chip win from a European satellite operator.

Balance sheet has always been the factor preventing me in taking positions. But they did a raise in March (dilution) so are now sitting on some cash finally.

As with any microcap, please conduct your own research.

Global Foundries photonics/CPO ecosystem list:

1. $GFS - $30.5B

2. $CDNS - $85.9B

3. $SEIGY - $217.2B

4. $SNPS - $84B

5. $KEYS - $57.3B

6. $ATEYY - $130.4B

7. RoboTechnik (ficonTEC) - $11.4B

8. $GLW - $141.2B

9. $LITE - $63.8B

10. $SIVE - $950m

11. $FN - $24.7B

12. $ASX - $63.3B

For publicly traded names.

Equal weighted long on the ecosystem from their presentation might not be a bad idea?

I still find it funny how everything publicly listed is trading in the tens of billions.

Then there's some small Swedish laser company there next to $LITE.