UBS REPORT ON INDIA’S GROWTH SLOWDOWN: A SIMPLIFIED EXPLAINER

1. For the first time in decades, a leading global investment bank has used the words “There are structural aspects to India’s growth slowdown.” These “structural aspects” cannot be termed temporary or cyclical, UBS says in its recent report on the Indian economy.

2. UBS has not issued a “general” market report. It has specifically advised its global clients to short the rupee (buy bearish rupee options) + buy interest rate swaps (betting on interest rate cuts in the future to stimulate the economy) providing them with a precise investing strategy, which is bearish on India.

3. Global investment banks, such as UBS, enforce “Chinese Walls” (information barriers) between different divisions of the bank to eliminate conflict of interest. So, different divisions can have different views and strategies.

4. The Research Division of UBS has issued a deeply bearish report on India (which is the subject of this post.) Other divisions, such as Trading Desk, Advisory, or Asset Management can issue different reports or provide different advice to their clients, depending on individual client risk profiles and goals.

5. The research division for Emerging Markets Strategy at UBS is headed by Manik Narain, who is a top Emerging Markets specialist with UBS in London for many years. His department operates independently from all other divisions.

WHAT DOES THE UBS NARAIN REPORT SAY

1. Structural Aspects: There are “structural aspects to India’s growth slowdown.” It means, certain problems are embedded in the economic policy framework of India, which may require deep reforms and long-term corrective measures. These are not cyclical, and you cannot wish them away with a “chalta hai” attitude.

2. Earnings Moderation is Spreading: Narain says that corporate earnings moderation is spreading to the “defensive sectors” of the economy, such as consumer staples (dal-roti).

Note: Remember, nearly one year ago, the economist Dr. Arvind Subramanian had publicly stated: “It is absolutely mystifying to me that India’s GDP is growing at 7.5%, while household consumption is at 3%. I simply cannot understand this. The numbers don’t add up.”

3. Highest Interest-to-Revenue Ratio: Narain says that India’s Debt Service-to-Revenue ratio is one of the highest among Emerging Markets. Debt Servicing Cost = Interest + Principal repayments on your debt.

India has a high national debt. The Indian government borrows from banks and financial institutions within our own country when its tax revenue collection is not enough to pay for all government expenditures. There is no urgent obligation to repay the principal amount, but the “interest” on that debt must be paid every year (as per global accounting norms.)

India’s highest cost component in the annual government expenditure is “Interest” on the national debt – over 25% at present. This is higher than what the Indian government spends on defence or public infrastructure etc. in the annual budget.

4. Higher-for-Longer US Yield Environment: Narain says that if the yields (interest rates) on US Treasuries remain higher for a longer period, while the RBI is forced to cut interest rates in India (to stimulate demand), the foreign investors will further lose the incentive to keep their money in India.

Foreign investors look at “risk-adjusted returns”. It means, if they invest in bonds in an Emerging Market like India, they want a risk premium because of rupee volatility and other risks. On the other hand, US Treasuries are considered the safest investment in the world because they are backed by the US government.

Even as we speak, the foreign investors have been withdrawing from Indian bonds at a pace not seen since Covid 2020.

5. Net FDI Inflows Have Nosedived: Narain says that while investors are worried about India’s “Balance of Payments” position – at UBS the bigger concern is slowing FDI inflows. According to the RBI data:

Net FDI Inflows (Inflows minus Outflows)

FY23 (Apr ‘22 to Mar ‘23)

@ $28 Billion

FY24 (Apr ‘23 to Mar ‘24)

@ $10.6 Billion

(62% Decline Y-o-Y)

Jan ‘24 to Dec ‘24

@ $3 Billion (this data point is provided by Narain)

6. Credit Growth is Moderating: Economic growth improves when the country's banks are able to provide credit (loans) to entrepreneurs to start new businesses, expand existing businesses, and generate employment and national income.

Narain says that “equilibrium credit growth rate in India will go down from 16% per year to 10% per year.” The reason, he says, is that the Loan-to-Deposit Ratio (LDR) is stretched to the highest on record at 80%.

An LDR of 80% means that if a bank has Rs. 100 in deposits, it lends out Rs. 80 from it. This is already the upper limit of safe lending practices, according to Narain.

Unless the banks in India are able to generate more deposits from the public, they will have to cut back on lending growth to avoid the risk of bad loans to risky borrowers.

7. Stock Market Participation is High: The Indian stock market can no longer be called an “under-penetrated” (under-utilized) market. According to UBS calculations, public investments in the Indian stock market are already equivalent to 60% of bank deposits. It means for every Rs. 100 in bank deposits, Indian investors have Rs. 60 invested in equities.

If you consider all the financial assets of Indian investors (including bank deposits, gold, and real estate), 23% of the entire Indian household wealth is already invested in the stock market, according to Narain. So, the scope for further penetration is diminishing, unless economic growth revives.

8. Stock Market Valuations are High: Based on UBS internal valuation methods (P/E ratio and P/B ratio etc.), India’s stocks are trading at 72% premium to the rest of the Emerging Markets in the world. This kind of premium was unheard of even 12 months ago, he says.

Taken together, points # 7 and # 8 further explain why the foreign investors have been exiting from Indian stocks.

THE BOTTOM LINE

In the current Indian stock market scenario, the bulls definitely have a valid argument, and the bears too have a valid argument.

Examine both sides of the argument based on data and facts. Then position your investments based on your own unemotional judgment.

Charlie Munger said: "I never allow myself to have an opinion unless I know the other side's argument better than they themselves do."

@arvindsubraman@arabicatrader@dugalira

UBS Says Structural Slowdown UBS Group AG is recommending investors should short India’s rupee and go underweight on the country’s stocks amid slowing economic growth, Bloomberg is reporting. The bank’s research group said India’s $4 trillion economy has entered a structural slowdown that can’t be explained by cyclical factors like oil-price hikes or declining government spending. A structural slowdown in India is a call no other institutional investor appears to have taken and of course no resident economist has said something like this. The deceleration is underpinned by a long-term moderation in credit growth, foreign direct investment, export competitiveness and earnings potential, UBS said. The “conventional wisdom that India is ‘far removed’ from Trump risk compared to other emerging markets is debatable,” said Manik Narain, head of EM strategy research at UBS. “A potentially higher-for-longer US yield environment poses challenges to India’s growth, with one of the highest debt service-to-revenue ratios in the major EM space.” Apart from the losses in equities UBS says India’s bonds are recording the fastest outflows since 2020 as euphoria over their inclusion in global bond indexes wanes. Market losses follow a slowing in real GDP growth over successive quarters, showing the Indian economy slipping below the 7% average generated before the Covid-19 pandemic. Disappointing business updates following a decade in which companies in the Sensex index failed to meet analyst expectations have underscored the bearish turn. UBS says that the moderation in India’s earnings growth is spreading to defensive parts of the economy — such as consumer-staples — showing that temporary factors such as government capital expenditure are not the only reasons behind the slowdown. Elsewhere, UBS says there is credit moderation, china deflation which will lead to tougher competition, slowing FDI which is a big concern as India saw only around $3 billion in the past 12 months. Equities are now 23% of the financial assets of Indian households and 60% of bank deposits. That means the market can no longer be termed “underpenetrated,” UBS said, adding that as per their valuation methodology, the country’s stocks trade at a 72% premium to the rest of emerging markets, a premium “unheard of even 12 months ago.”

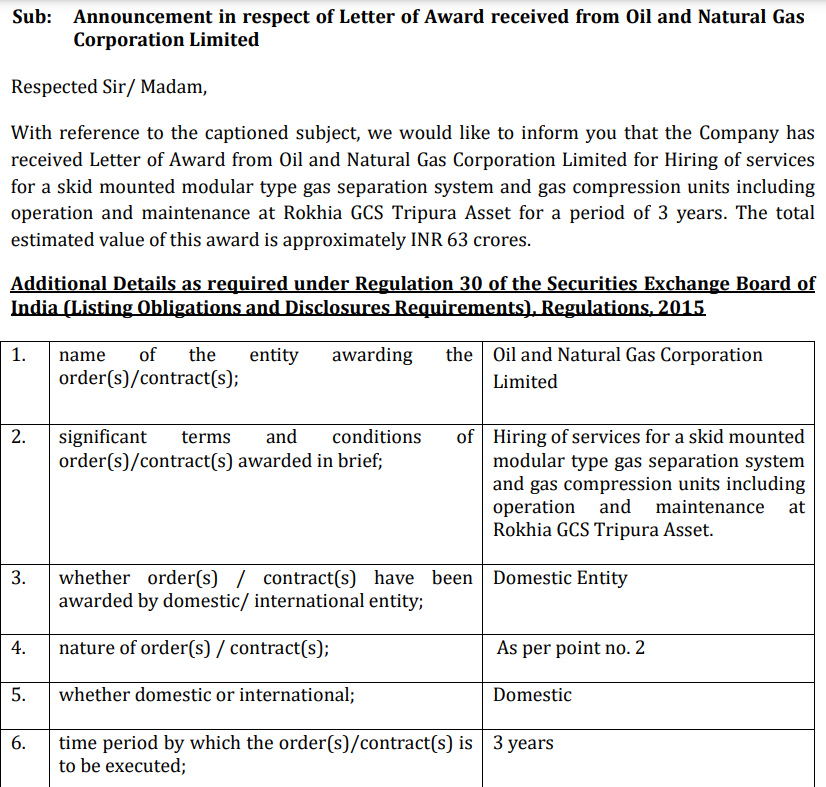

Deep Industries Ltd has been awarded a Letter of Award from Oil & Natural Gas Corporation Ltd for the hiring of services for a skid-mounted modular gas separation system

Order size ~₹63 Cr

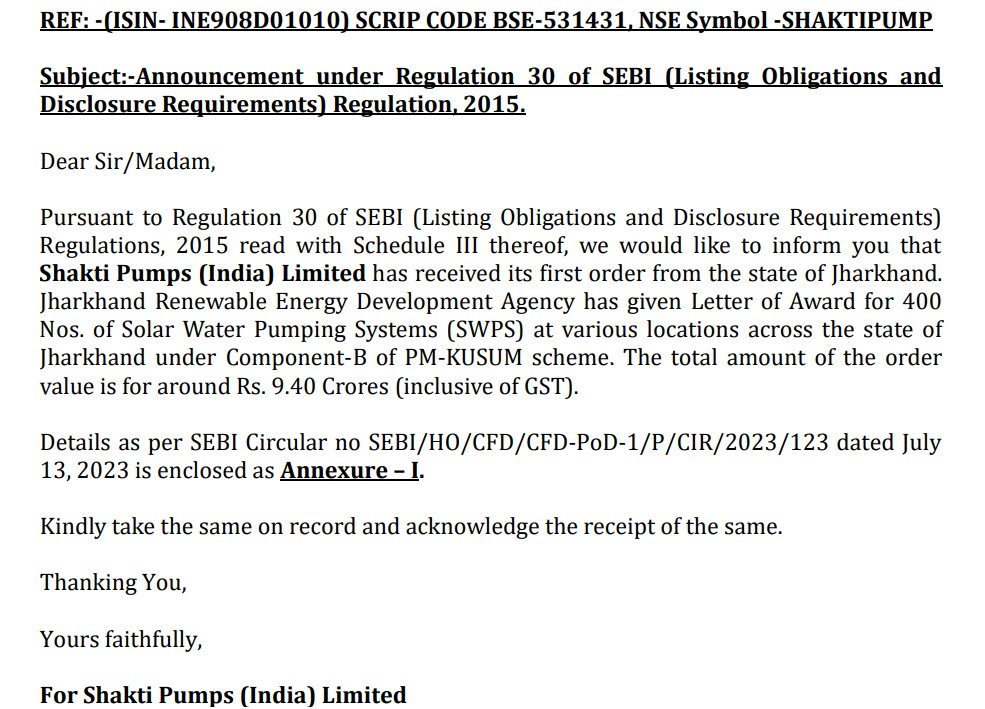

Shakti Pumps (India) Ltd has received an order from Jharkhand Renewable Energy Development Agency for 400 SWPS under the PM-KUSUM scheme

Order size ~₹9.4 Cr

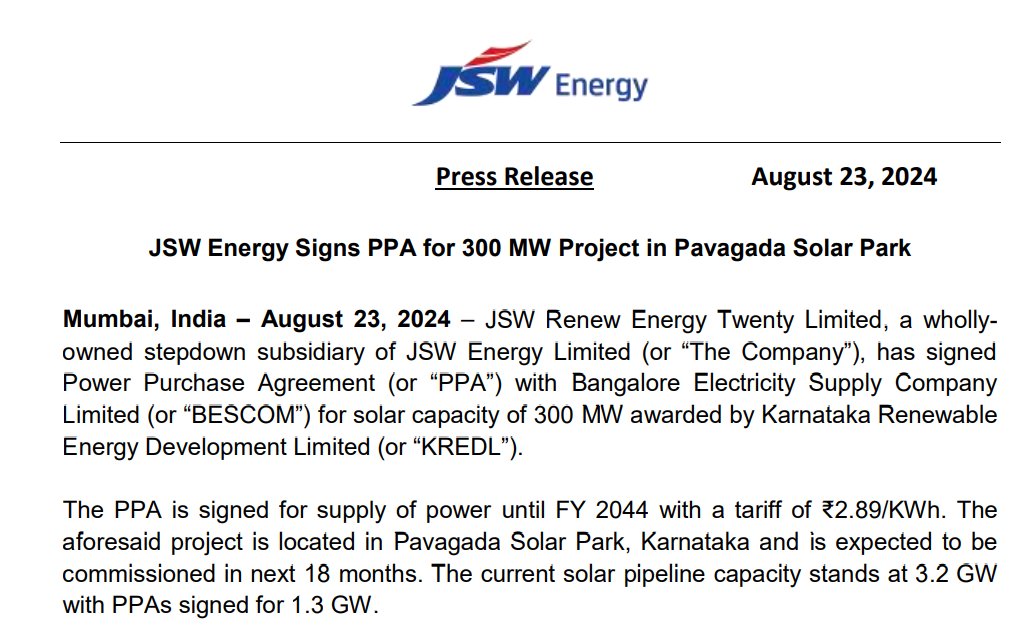

JSW Energy Ltd

JSW Renew Energy Twenty Ltd (subsidiary) has signed a Power Purchase Agreement with Bangalore Electricity Supply Company Ltd for a 300 MW solar project in Karnataka, awarded by KREDL

Tariff - ₹2.89/KWh until FY 2044

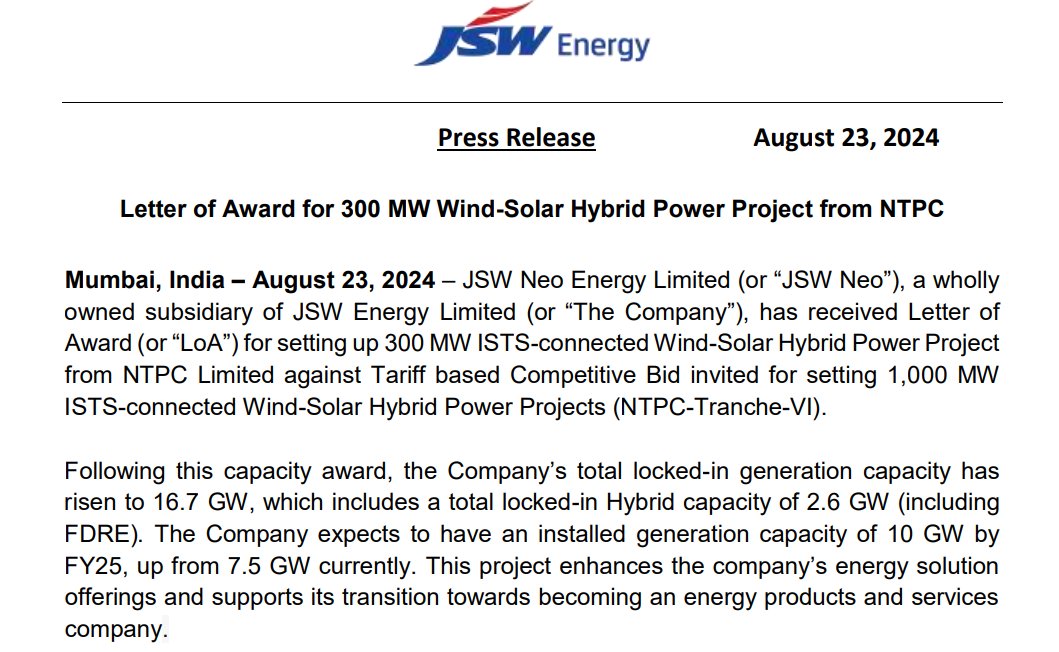

JSW Neo Energy Ltd, a subsidiary of JSW Energy, has received a Letter of Award for a 300 MW ISTS-connected Wind-Solar Hybrid Power Project from NTPC Ltd

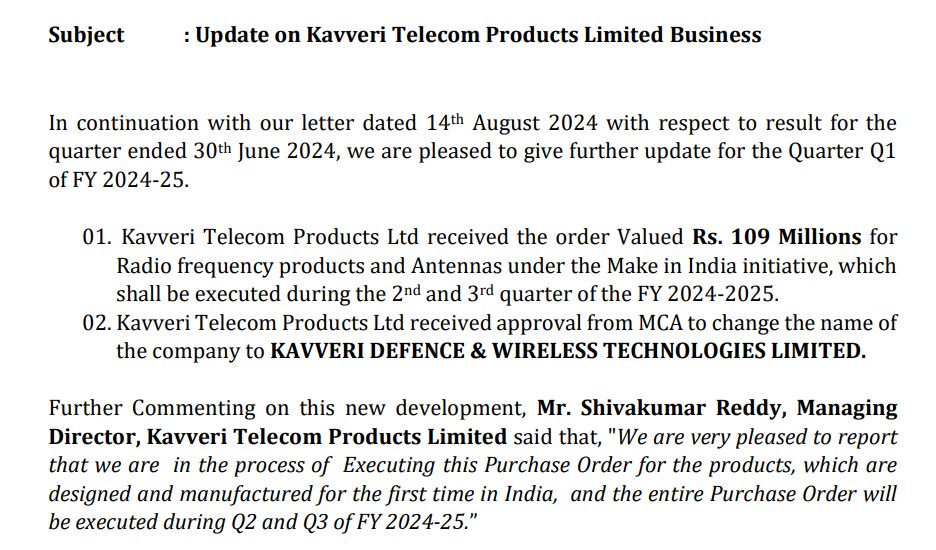

Kavveri Telecom Products Ltd has received an order for radio frequency products & antennas under the 'Make in India' initiative.

Order size ~₹10.9 Cr, to be executed during Q2/Q3 FY25

Glenmark Pharmaceuticals Ltd

Glenmark Therapeutics Inc, USA has launched Olopatadine Hydrochloride Ophthalmic Solution USP, 0.1% (OTC), a similar ingredient to Pataday Twice Daily Relief

Estimated market size ~$26.4 million

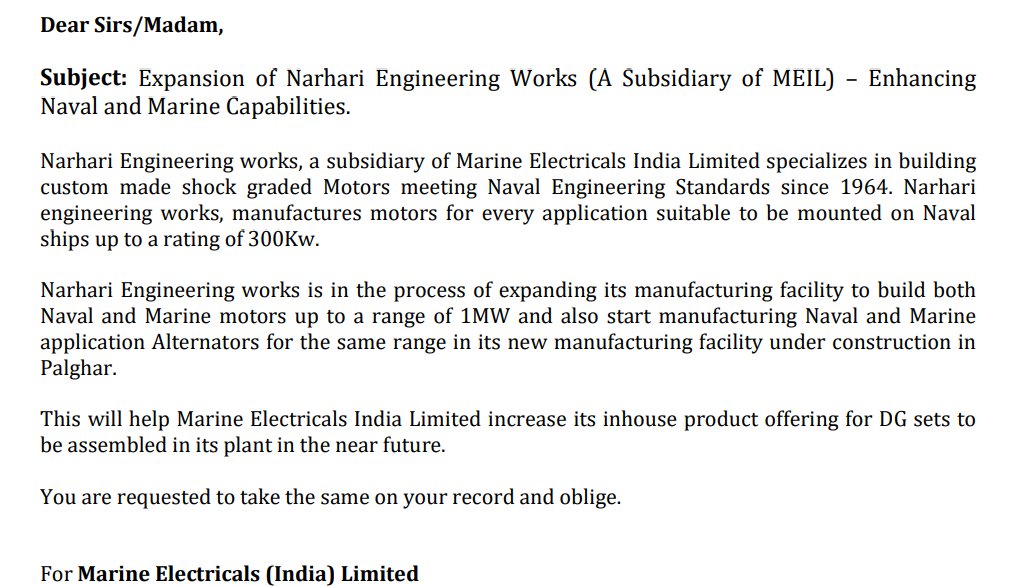

Marine Electricals

Narhari Engineering Works (subsidiary) plans to expand its manufacturing facility to build both Naval & Marine motors up to 1MW & Naval & Marine application alternators in a new facility in Palghar

Narhari specializes in custom shock-graded motors

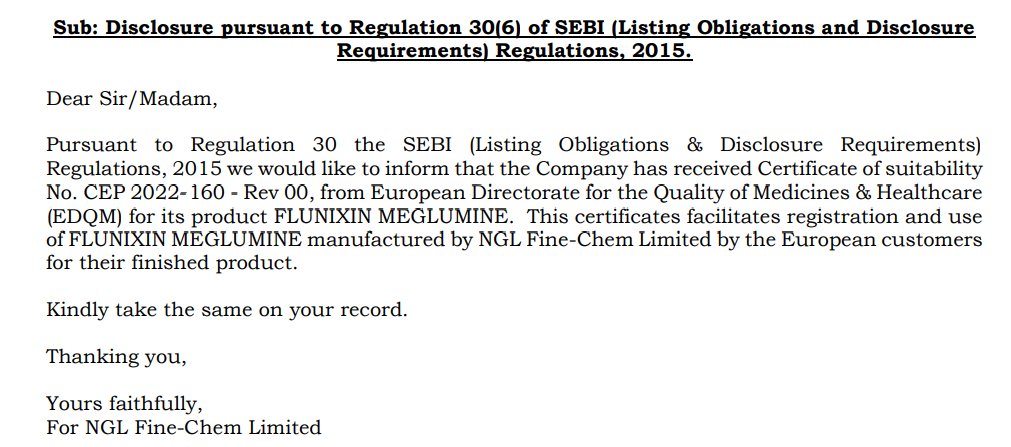

NGL Fine-Chem Ltd has received a Certificate of Suitability from the European Directorate for the Quality of Medicines & Healthcare, enabling European customers to use their FLUNIXIN MEGLUMINE

Zen Technologies Ltd has received a patent for 'Mine Detection System'

- uses GPS/GIS technology to plot & record mine coordinates in Lat/Long & Military Grid in Defense Series Maps (DSM)

- comes with handheld devices for safe mine laying & retrieval, even at night

DCM Shriram has commissioned a 52,500 TPA Hydrogen Peroxide plant at its Chemical complex in Jhagadia, Gujarat

Hydrogen Peroxide has various applications, including bleaching, water treatment, chemical synthesis, food processing, mining & environmental

Vishnu Chemicals Ltd has to acquire a 100% equity stake in Jayansree Pharma Pvt Ltd (JPPL) at an enterprise value of ~₹52 Cr

JPPL will become a wholly-owned subsidiary, boosting Vishnu Chemicals' fixed assets by ~₹80 Cr

Sequent Scientific Ltd has received prequalification approval from the World Health Organization (WHO) for its Albendazole API

The approval comes in partnership with Mepro Pharmaceuticals Pvt Ltd, which has developed & commercialized the Albendazole Chewable formulation

The Traffic Lights are flashing Orange.

Covid was a dip in Ganges for Indian lenders. Losses got provided for and capital raised.

The beauty of any problem dealing with money is there is no problem that more money can’t solve.

Post Covid lenders with clean portfolios and Capital built consumer loans pedal to metal.

Meanwhile a few things changed.

1.Households became comfortable living it up today by borrowing from tomorrow.

2.Inflation is a cruel tax on savings .

3.Earnings haven’t kept pace.

4.Families have become nuclear. So either they pay expensive rent or barely affordable home loan EMI.

5.Home Loan EMIs got linked to Repo rates and went up by 2.5%!

https://t.co/CzwNl8C17Y aided economies have reduced need for people- even in manufacturing!

7. Consumption growth has weakened. Life style expenditure is rising sharply.

8.CIBIL data clearly shows downgrades far exceed the upgrades prime and above categories and there is a persistent drop in New to credit customers which means multiple lines of credit is being extended to a proven customer.

9.Household savings is down to a 47 year low of 5.3% of GDP in 2023 from 7.4% in 2021.

10.Just in last 3 years personal loans have doubled.

11.Economist Nikhil Gupta says Household Debt in India is 48% of Personal Disposable Income but Debt Service Ratio at 12% is well past US and China.

12.Households have lost Rs.50,000 crs in FnO. Just Dreams 11 revenue last year was Rs.6300 crores, if you add card games the number goes higher and most of these are from small towns. Anecdotally we see that a lot of personal loans have been taken to make good these losses.

I don’t want to rain in on the parade. I was hoping by now Corporate loans would take some steam off this crowded trade, but that feels like waiting for Godot! The regulator has been well ahead of the curve and blowing the whistle for a while.

Mutal Fund Sahi hein campaign while encouraging investors also informed them about risks.

Banks and NBFCs need to do the same to educate the Indian consumer on the risk of confusing need vs demand. In Mahabharat, Yaksh asks Yudhisthir who is truly happy to which he replies, “The one who has no debt.”

Today Rs.3 trillion is being rolled over in credit cards and the number of loans per customer is piling up. High interest rates add to the woes but you can’t blame the lenders for pricing in the risk.

So far a stock market fall dented the Rupee and Real Estate, the next correction risks hitting Indian lenders given the massive behavioural shift of retail. The average joe now compares FD to MF returns which means at some level has started to believe equity is a risk free asset class.

For the lenders, NPA is just a dent in profits, but my heart goes out to to the indebted household for the trauma it causes.

Caveat Emptor. Caveat Venditor. Let the buyer and seller beware! The lights are flashing orange and both lenders and borrowers need to behave responsibly from here

#banking #sbfc

Brigade Group to partner with abCoffee to establish 6 outlets in its Bengaluru office spaces to improve the tenant experience by offering high-quality, affordable coffee & food