Rates Spark: The damage has been done

https://t.co/2aWgYfPwmG

A slide lower in oil prices has helped rates dip, but we're not returning to pre-war yield levels. The US 10yr real yield is likely to remain elevated, and US inflation breakevens have little room to fall further. The ECB has already hiked once, and at least another hike is discounted. We anticipate more oil price volatility as a big reserve rebuild kicks off

Market rates have been remarkably steady of late. Long end rates are holding to elevated tendencies that built in recent months, while shorter tenor rates are being bolstered by ongoing rate hike threats. Trying not to mention the war, but… Iran remains a factor. Yet, as a 'steady-state tolerable negative', it's proving less impactful. Payrolls next

https://t.co/67kaGYdLZt

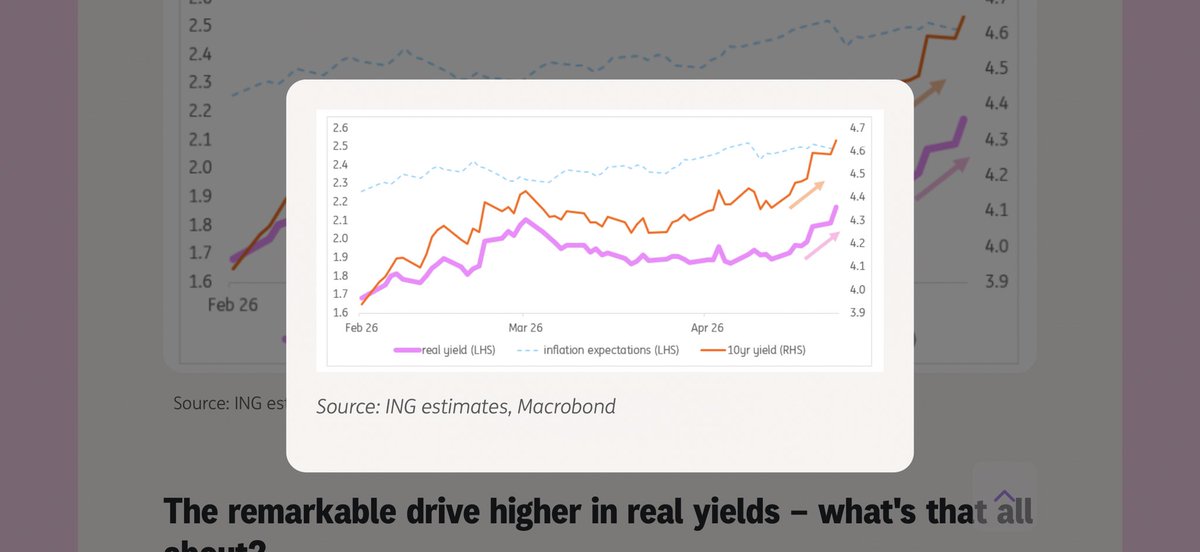

Rates Spark: The real deal

On a longer view, real rates highlight a backdrop, where better growth hopes and record bond supply keep long-end pressure intact. Recession fears are the clear risk to that. But in the absence of recession, inflation expectations are arguably benign and real rates have little need to fall

https://t.co/qfQMq6FVts

Rates Spark: Sticky circumstances

US long rates set to remain sticky to the upside, as a material downside impulse is far from straightforward

https://t.co/lGFZ6iHCuP

The recent spike in US yields has come from higher real yields. Inflation expectations in fact are okay (2.5%). The risk is real yields remain relatively elevated, even if the Strait were to re-open. Fits with belated de-rating / selling pressure on Treasuries, and in fact with the tech boom (granted tenuous, but still a thing)

PADHRAIC GARVEY

US Treasuries losing the control they had

https://t.co/tvXRlYewzf

We’ve marked 4.75% as our next staging post. We hold to that, but we still worry that an overshoot risk beyond that to 5% cannot be ruled out (the new uncomfortably high probability risk case). The mood music rhymes with this.

ING THINK: Rates face risk of instability https://t.co/qBJknDbl21 Market rates have risen because of the Iran war, but have been controlled (apart from UK gilts). An extrapolation of the shutdown of the Strait points to higher market rates still

ING THINK: Rates Spark: Flip the gaze from China back to Iran https://t.co/uh0LlbzxJW President Trump's China visit is ongoing and offering a welcome break from Iran war angst. But that is what we are going right back to. The implications of the Iran war for US inflation have been clear in the past few days of releases for April, and while it's not the best barometer of the war effect, export price inflation of 8.8% year-on-year is a scary enough number to at least ponder the implications of

ING THINK: Rates Spark: The evaporation of real yields https://t.co/xcFfCuUXMo Apart from excess supply, the biggest enemy for bonds is inflation. Well, we've got some of that to worry about, on both sides of the Atlantic, and the Pacific. The ratchet higher seen in bond yields has been measured and steady. But it risks becoming less measured, if the Strait remains closed and higher economy-wide prices are just allowed to become a thing

ING THINK: Rates Spark: Hard to see a ceiling for gilt yields https://t.co/U5PQYRpBp1 Meanwhile, US Treasuries continue to feel pain from the never-ending shuttering of the Strait, with April CPI data already high, and set to rise further in the coming months. Not great for core bonds generally

ING THINK: Rates Spark: A lot not to like for bonds https://t.co/kcmhnDN56S Tough to see much progress on the US-Iran “talks” this side of the Trump-Xi summit. As we wait, Treasuries feel pain

ING THINK: Rates Spark: Feels quite digital this time https://t.co/Tw07XibtFc There's a lot of optimism about a deal to be struck between the US and Iran. We're fine with that. But we are also cognisant that there is a polar opposite outcome that could still see us dipping back into a troubling direction, mostly as we've been down this route a few times now. Market rates took a breather lower on Wednesday. Expect an edge higher ahead

ING THINK: Rates Spark: Triple-whammy for gilts https://t.co/WfOKp1d5w7 US yields backdrop has come off extremes, but the problems that drove us there remain

ING THINK: Rates Spark: 10yr SOFR hits the 4% handle https://t.co/7tw7lylbvI The 4% handle is where the fixed rate receiver conversation begins in earnest. We've been here before. In fact, we saw peaks at 4.6%, 4.4% and 4.3% in 2023, 2024 and 2025 respectively. We're likely heading back in that direction, but note that the peaks have been less pronounced each time we've hit one. Greedy?

ING THINK: Rates Spark: A cacophony of mad stuff https://t.co/W5wJ3xYjyN Thursday was a mad day, with many markets just doing their own thing. The war 'over there' seemed like a sideshow, of little importance for risk assets at least. And bond yields fell even as inflation breakevens continued to rise. The price of oil even fell, on zero war progress. All a bit disorderly, as central banks talk risks but hold pat

ING THINK: Rates Spark: Big rate decisions as oil tests highs https://t.co/ncffsDgaTN Earlier Wednesday, the US 10yr yield had gapped higher, and hit 4.4%. Actually, the whole curve gapped up. The hold-out in the Strait of Hormuz was the catalyst. Some duration selling makes a lot of sense here, where we are in “nowhere land” on a resolution to the war. Extrapolate this, and we could sail back up to the 4.5% area that we hit a few weeks ago.

ING THINK: Rates Spark: It’s Jay’s day https://t.co/BuofQleoRW It's Fed day. Given the challenging war-impacted inflation environment, it won't cost much for the Fed to adopt a hawkish tilt; while remaining in a wait-and-see mode. There will also be questions on the incoming Kevin Warsh and Powell's intention to stay-or-go. But likely to be swatted away. As it's really Jay's big day, his last as Chair

ING THINK: Rates Spark: Snail’s pace, but getting there https://t.co/4VeeLVg7XO Discomfort from closure of the Strait is slowly amplifying. The US 10yr break-even inflation rate is edging towards 2.5%. Far from catastrophic, but if it were to break above, it would be a growing problem, for both Treasuries and the Federal Reserve

ING THINK: Rates Spark: Something must give https://t.co/92ouu2PSI7 President Trump's barometer of approval – the stock market – has been flashing 'nothing negative to see here' for the past few weeks. We can't say for sure, but it is quite likely that it has been a factor supporting the US stance to play hard ball. The US may have done that anyway, but risk asset comfort together with a mostly sub-$100/bbl oil price has absolutely helped

ING THINK: Rates Spark: Swap lines imply some pressure https://t.co/ag3MsORVFj The market discount through to the end of March centred on the freezing of the Strait of Hormuz as critical. Fast-forward to this week, and equity markets impliedly think it's not that critical after all. But there is stress brewing