Nobody should care about TA charts since people just made up squiggly lines trying to convince others to sell.

$SIVE just raised an emergency $70M for mass production likely for allocation from fabs.

With $JBL, $POET, $AEVA, and others volume ramping near term.

Then $GFS, Ayar, and many other players are volume ramping later in 2027.

Sivers also confirmed intent to complete NASDAQ Listing in the next few quarters.

It's probably my highest conviction photonics long, everything seems to be coming into place.

Photonics is backed by actual revenue numbers and it's an architectural shift championed by $NVDA.

Quantum barely has any revenue.

$LITE is completely sold out for the next 2 years (per $POET AGM) likely starting into 2029. Lumentum is so strained that they buy CW lasers off competitors (earnings transcript)

$COHR is bottlenecked, so they buy EML off Lumentum.

Then, $AAOI is coming in with Made-in-America independent CW capacity, are projecting $1.4B/quarterly revenue ending H1 2027 of a stupid $9.3B MC today.

So all the CW capacity from independent players who have it now like $AAOI or $SIVE are likely to become scarce resources.

Many other hyperscalers have already started LTA discussions (per Trendforce). And players like $AMD are currently talking with players such as $AAOI (Rosenblatt channel checks).

Thematically, next 2 years is 9x TAM to US$154B per GS reports, especially with 16x/45x dollar content increase in scale out/scale up.

Then there's the overall thematic AI drop from $META, which is widely misunderstood because people conflate what "excess capacity" means. And as UBS mentioned, Meta planning a cloud offering is NOT NEW NEWS.

Bloomberg just has a tendency to publish information that causes doom drops across the semi sector like Nvidia export controls a few months back.

But I'm familiar with what I'm holding so I'm confident in these numbers playing out.

Especially when all the major players are sold out, the fundamentals catch up eventually.

$PLTR CEO Alex Karp says customers want control over their “compute, models, data stack & alpha” instead of handing their edge to frontier labs.

Enterprises don't just want token access but want ownership, security & AI systems that don't give away the value of their business.

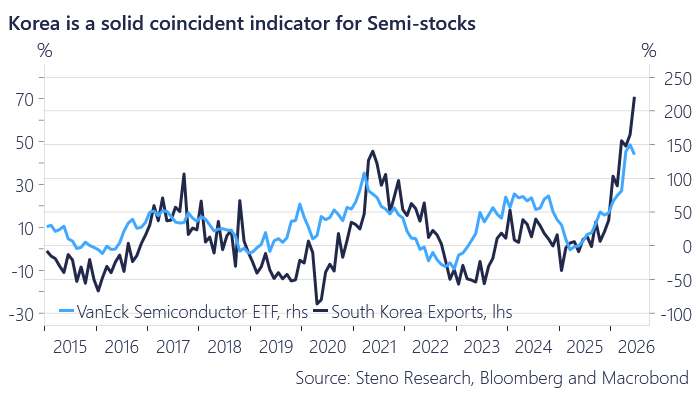

I get why there is a bit of "angst" whether the semiconductor cycle is overbought..

I just cannot find a single measure that is not accelerating live. Not one. Korean exports through the roof and BLEW past all expectations again today

The Next Phase of Artificial Intelligence, the Physical AI Universe and Stocks

Pure physical AI / perception:

$OUST: the 3D lidar eye of the physical world

$AMBA: the camera based AI vision brain

$LSCC: the low power edge FPGA brain

$CGNX: the eye of industrial machine vision and quality control

$ZBRA: logistics, warehouse, and industrial machine vision automation

$AEVA: FMCW based 4D lidar and velocity sensing layer

$ARBE: radar perception of autonomous systems with 4D imaging radar

$MVIS: lidar, perception, and sensor fusion player

Robotics application / embodied AI:

$SYM: AI driven warehouse robotics automation

$TER: cobot and autonomous mobile robot platform

$PDYN: embodied AI / edge autonomy software for robots and drones

$RR: service robotics application for restaurants, hotels, and commercial spaces

$ISRG: leader in robotic surgery and precision physical automation

$AUR: autonomous trucking and autonomous driving software platform

$MBLY: ADAS, autonomous driving, and camera based perception brain

Infrastructure and pick and shovel:

$PENG: AI factory / HPC infrastructure provider

$ADI: sensor, motion control, and analog physical AI infrastructure

$NXPI: industrial edge AI and embedded processor infrastructure

$QCOM: robotics, edge AI compute, and connectivity brain

$ROK: factory automation, industrial control, and physical AI integration platform

@alGix0 I’m not concerned with short term volatility, which is expected with high-beta photonics and current macro.

I’m long on $SIVE to see my thesis play out with laser volume ramp.

Dilution could be a short term factor, but I see the development as positive long term

$SIVE: "Intent to complete the [NASDAQ] listing process over the next few quarters"

This statement was largely missed by many screeners.

Very material improvement from evaluation, to formal confirmation of timelines.

$BE and $BN expanded their AI infrastructure power partnership from $5B to $25B (a 5X increase since October 2025).

The deal helps finance Bloom’s onsite fuel-cell power projects as AI data centers increasingly need fast, reliable power outside the traditional grid timeline.

The Robotics Rotation is HERE 🤖👀

Jensen Huang has said, “Physcial AI is the next wave of AI”

In just the last 3 days: 👇

$OUST +57%🟢

$AEVA +47%🟢

$AVAV +20%🟢

$MBLY +19%🟢

$TER +12.5%🟢

$TSLA +12%🟢

$CGNX +11%🟢

$SYM +10%🟢

$ROK +8%🟢 (5 days)

Is this the beginning of a broader rotation, or is the market getting ahead of itself? What do you own?

We tax cigarettes to reduce smoking.

We tax alcohol to reduce drinking.

We tax fuel to reduce driving.

What do you think happens when you tax employing people and running a business?

$SIVE is raising ~$61M (600M SEK) to expand manufacturing capacity for InP lasers and optical amplifiers.

Sivers operates as a fab-lite model so this is likely hinting at foundry allocation/scaling for CW DFB laser ramp across Jabil, and their other partners.

It could also point to broader foundry allocation/scaling beyond the already announced WIN partnership.

My feedback is that it's very bullish if it's comprised of long-only institutions and there's no heavy discount (30 day VWAP). Otherwise, would need to reaccess if there's arb or short term investors.

This is the perfect time to get ideal strategic investors like $GFS on the cap table. As well as focusing on having more US institutional support.

Especially considering $56M is a small check to a single US institution that want photonics exposure (eg. look at Poet's $400M registered direct offering for sentiment).

A lot of it is "it depends when more info comes out", but this looks like a very positive signal for mass production given Siver's fab-lite models.

Just some notes on $POET AGM and read through on optical markets:

- "The top three laser suppliers control 68% of the market, and they’re completely sold out for the next two years"

$LITE CEO said into 2028, so POET implicitly confirms laser shortage is going into 2029 now.

- NRE with a new customer, building on POET’s interposer for high-power external light source.

This is high confidence $SIVE as laser supplier given the Sept 29, 2025 PR on ELS, and new customer qualification would be material for revenue if it goes into volume ramp.

- Poet expects Lumilens commercial agreement to scale to over $500 million over the next 5 years.

Lumilens claimed a top-3 hyperscaler was their initial customer (Linkedin OSINT)

- $830M cash on hand on balance sheet (this is more for Poet fundamentals).

- "The entire optical components industry today is facing a severe shortage of critical components."

Reaffirming what we know already regarding optical bottlenecks.

- "Production ramp in the second half of 2026 this year."

Just production timelines H2.

In terms of $POET volumes:

- existing capacity around 1 million optical engines per year

- projected demand exiting 2027 around 1 million optical engines per month

- roughly 10x capacity expansion

I don't own Poet, but if management delivers on these projections it directionally looks very positive.

However something to note is that unlike other suppliers that have named hyperscaler customers to to back up capacity revenues like $AAOI: $POET seems more questionable.

But this does look like a very positive outlook for $POET if they match projections.

Here’s why $RKLB just spent ~$8B acquiring $IRDM.

Rocket Lab wants to own the network, spectrum and recurring revenue layer once satellites are in orbit which is why this deal is really about vertical integration as Neutron comes online.

Once Rocket Lab can launch Iridium satellites on Neutron then it internalizes a cost that used to flow to third-party launch providers making the deal way more accretive over time as Neutron comes online.

What I like is that Iridium also brings something Rocket Lab stack has lacked which is recurring, high-margin service revenue tied to global connectivity, direct-to-device and government communications.

The space economy is splitting into companies that can launch and refresh their own networks and companies that have to rent access to orbit. $SPCX already proved which side wins because if you own both launch and the network then you control the cost structure, refresh cycle and margin stack in a way third-party launch customers cannot match.

Launch gets you to orbit but connectivity is what you monetize once you're there and the companies that own both the launch layer and the network become the platforms of the space economy.

$MU is now a top 10 holding in the S&P 500 with a 1.9% weighting.

A memory company becoming one of the largest stocks in the S&P 500 while still trading at a fraction of the market multiple shows the market still doesn't fully believe these AI memory profits will last.

$OUST is up nearly 20% as Agility Robotics prepares to go public through $CCXI giving the U.S. its first pure-play humanoid robotics company.

Agility’s Digit robot uses its LiDAR giving Ouster direct exposure to one of the most commercial-ready humanoid robotics platforms.

![aleabitoreddit's tweet photo. $SIVE: "Intent to complete the [NASDAQ] listing process over the next few quarters"

This statement was largely missed by many screeners.

Very material improvement from evaluation, to formal confirmation of timelines. https://t.co/iOceCgJTG4](https://pbs.twimg.com/media/HMIAe65aYAEpRyA.jpg)