Director of Indexing & Derivatives at Benchmark | ex-S&P, ex-ICIS | talks about lithium, cobalt and rare earths prices | (assume opinions are mine and not BMIs)

What can lithium or rare earths learn from Bretton Woods?

I spend a lot of time (some would say "too much" time) talking to policy makers and advisors about critical minerals policy - specifically on price support mechanisms like floors and contracts for difference. In my spare time I'm interested in jursiprudence so this think-piece is trying to weave together the lessons from the past, the legislative reality for most Western govs, and criticality of cross-border partnerships. I wrote it with #rareearths in mind but its just as pertinent to #batterymetals like #lithium.

#criticalminerals

https://t.co/LBSXJSiMRP

All three instruments (lithium carbonate CIF Asia, lithium hydroxide CIF Asia, Spod FOB Aus) are technically in contango through to June 2027 still. However, the hype in sentiment in May has come off - market participants are planning for higher prices through to the end of Q3 and softening in Q4.

We survey the largest Chinese exporters, Japanese and Korean buyers and traders, as well as spodumene participants to aggregate their forward positions. This is the latest data.

Candidly, I think they're wrong (we all suffer from analyst bias - me included!). I suspect that the weak inventory dynamic will prevail through Q3 and increased cell demand in Q4 (ahead of the knock down in Chinese battery VAT rebates to 0%) on 31 Dec will keep lithium prices elevated.

Q1 2027 is likely to see price correction but I would be suprised if we see it in Q4 2026.

My view - could be wrong - is that operational capacity is 100kt, nameplate is closer to 150kt. My understanding from the market is it can turn out 8-10,000 tonnes LCE per month so 45kt isn't actually impossible. My guess is between 30-40kt if it really wants to: July very little, August-September ramp up (4.5kt, 7kt), Oct-Dec 10kt per month.

Honestly (imo), whether its 25kt or 40kt - its not going to move the needle for pricing in H2. It puts a cap on the price rally (which was always there, above $25/kg we start to see ESS demand cool) but it doesn't drag the price down meaningfully.

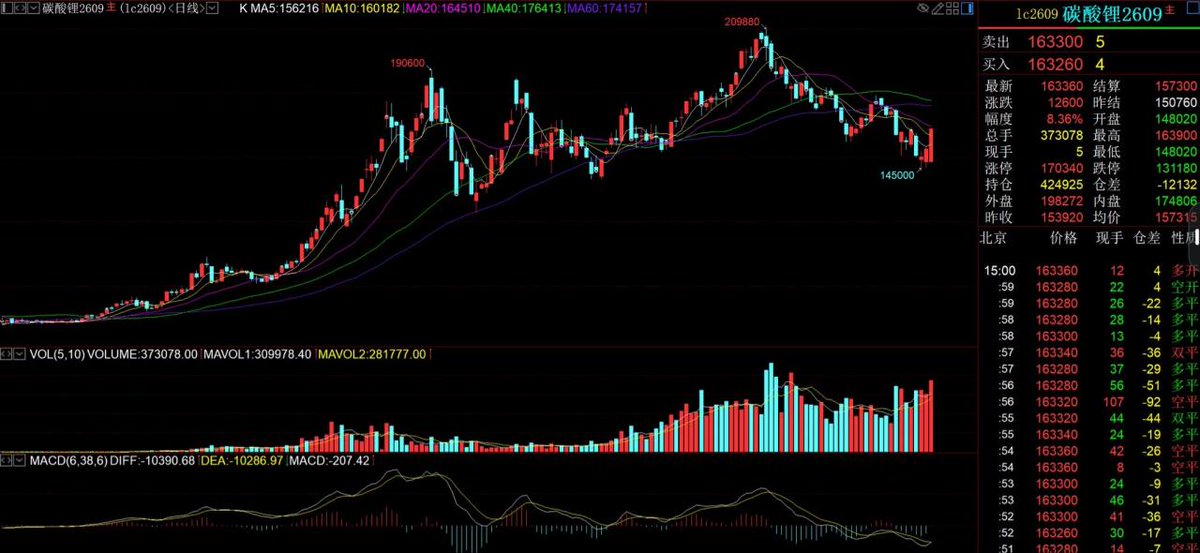

@jczuleta We’re at $22.6/kg EXW China and $21.1/kg CIF Asia (the Japanese and Korean import benchmark) in the physical spot market as of market close on 1 July - so I would suspect there’s a fair bit of upside still.

By the end of June, lithium carbonate and hydroxide inventory had fallen 1,400 tonnes LCE month on month, according to Benchmark’s independent survey of Chinese converters and cathode manufacturers. Modest decline but in keeping with the trend of inventories remaining under pressure.

Jiangxi Sinomine Lithium’s statement yesterday that it will curtail lithium chemical production in July, taking about 5,000 tonnes out of the market, potentially points to further inventory tightening this month.

Solid pricing analysis by @adam_benchmark. Physical spot prices in China closed at $22.6/kg on 1 July (#lithium carbonate, battery grade, spot).

CIF Asia (the price to Japanese and Korean cathode manufacturers) closed at $21.1/kg.

My unofficial bet with a banker in London that we would hit $30/kg by 1 July weighs heavy on my bank balance (well, one bottle of champagne worth).

In the US we're currently tracking over 60GWh of announced data centre #BESS projects, a figure that is growing fast. We've just released a free whitepaper - Gigawatt Ambitions: Data Centres, BESS, and the Race to Power - request a copy here: https://t.co/YH0VZhMNYI

#battery

Yesterday (29th June) was an interesting day for Jianxiawo rumours (🥱) but an even more interesting day for reading the tea leaves on trader sentiment about Jianxiawo. GFEX futures prices suggest the restart is priced in. https://t.co/xW3tbaKYqJ

It was announced on 19 September that authorities in Qinghai launched a full investigation into Xinghua #Lithium Salt, after media reports and video footage alleged the company had illegally dumped thousands of tonnes of hazardous waste in Dachaidan

https://t.co/nbkmoXNAzc

The world is in the midst of a global battery arms race and the US is no longer a bystander…

But domestic mining remains the great challenge ahead.

@Benchmarkmin is in Washington DC for our #GigaUSA 2023 event.

A real joy to sit down with @Sen_JoeManchin to kick off today.

Exclusive preview of Benchmark's upcoming Rare Earths Forecast ⬇

Join our webinar on Thursday 25 May - Beyond the Battery: Rare Earths in the Energy Transition.

In this webinar, Benchmark’s Project Manager @Dejonge_Daan will present analysis of the market fundamentals for #rareearths as well as Benchmark’s comprehensive outlook to 2040 for supply, demand and prices.

Register for the 08:00 (GMT+1) session: ➡ https://t.co/BCh9sfOFup

Register for the 15:00 (GMT+1) session: ➡ https://t.co/102Ya0Ga7X

#permanentmagnet #rareearthelements #energytransition #electricvehicles

The DRC government has lifted its export ban on China’s CMOC ending the ten-month dispute over royalty payments between CMOC and Gécamines.

The resolution allows this #cobalt to enter the market, which is already expected to be in surplus until 2026. ⬇️

https://t.co/NXxgy8y5Ui