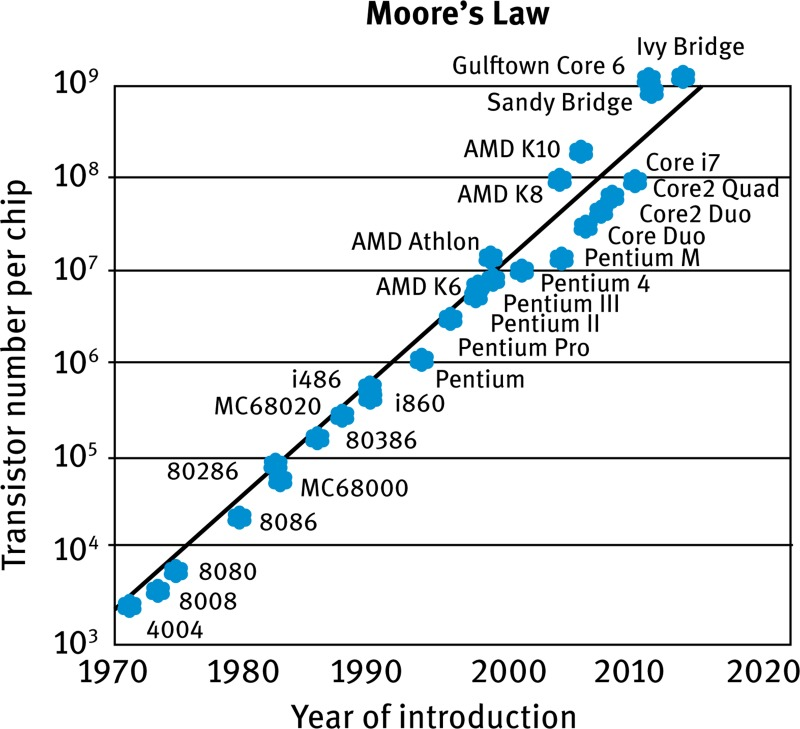

What 30 good years in tech looks like:

Moore’s law stipulate that the number of transistors on an integrated circuit doubles every two years, implying a high exponential growth rate of compute power over the long term. This has been significant in driving down the cost to make processors and chips over time.

Meanwhile, Metcalfe’s law says that the value of a network is the square if its number of users, which in a interesting way illustrate the incredible value that the buildout of the internet over the past thirty years has had, and been instrumental in the wide corporate and consumer adoption of information technology as the internet has evolved.

These forces, coupled with the attractive business model characteristics that software companies possess, including very low capital needs, cost efficient distribution (over the cloud), contracted revenue paid upfront (in the case of SaaS), ability to swiftly and cheaply iterate and improve the products, etc. has created a fantastic time for this space.

Many factors have played into making the ’90s and onwards a fantastic time for tech. Is AI going to be the new fuel to the fire for the coming decade of growth?

Some thoughts on how the investment horizon interacts with returns:

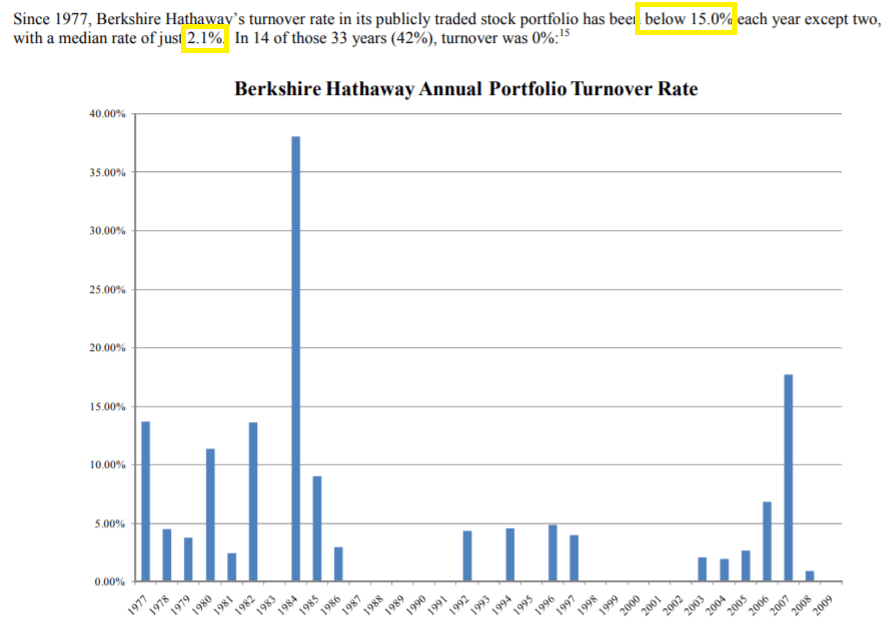

Buffett is famous for his permanent capital approach to the businesses he buy, whether they be listed or private companies; majority or minority stakes.

The key argument for this approach is that transaction costs and taxes will eat into your returns if you flip the portfolio too frequently, which over long periods of time becomes a significant drag on dollar returns due to the effects of compounding. Moreover, it forces you to set a sufficiently high bar for you to be comfortable with owning the business on a perpetual basis.

However, in order to take this permanent capital approach and be successful, I believe you are in some ways constrained to the areas that are Buffett’s specialty, namely (i) established industries that change infrequently and are stable over time, (ii) companies with a proven track record, and (iii) a large margin of safety in order to be comfortable with owning the company over long periods of time.

Of course, you can in certain cases be successful in emerging and/or changing industries with a long term horizon, but the lack of predictability becomes a limiting factor in your ability to control the investment horizon. The situation can simply change too quickly and lead you to a new reality in just a year or two.

In essence, emerging or changing industries / companies, as a strategic investment focus, should exhibit more of a power law dynamic in the distribution of returns (a few big winner making up the bulk of returns) coupled with a shorter average investment horizon. On the other hand, the approach taken by Buffett and peers allows for longer hold periods (decreasing transaction costs) and requires a strong focus on downside protection and loss mitigation, resulting in a more evenly distributed return profile of the portfolio.

To summarize, I think the investment horizon must be tailored to the strategy and expertise of the investor. Personally I think flexibility is important and hard rules should be avoided. As my focus primarily is on profilable companies on the cheaper side of the spectrum (not to say that they are very mature yet - a common feature of investing in microcaps), I find a longer investment horizon to suit me, with an average hold of 3-7 years.

How do you think about this as you build your portfolio? 🤔

#investing #microcaps

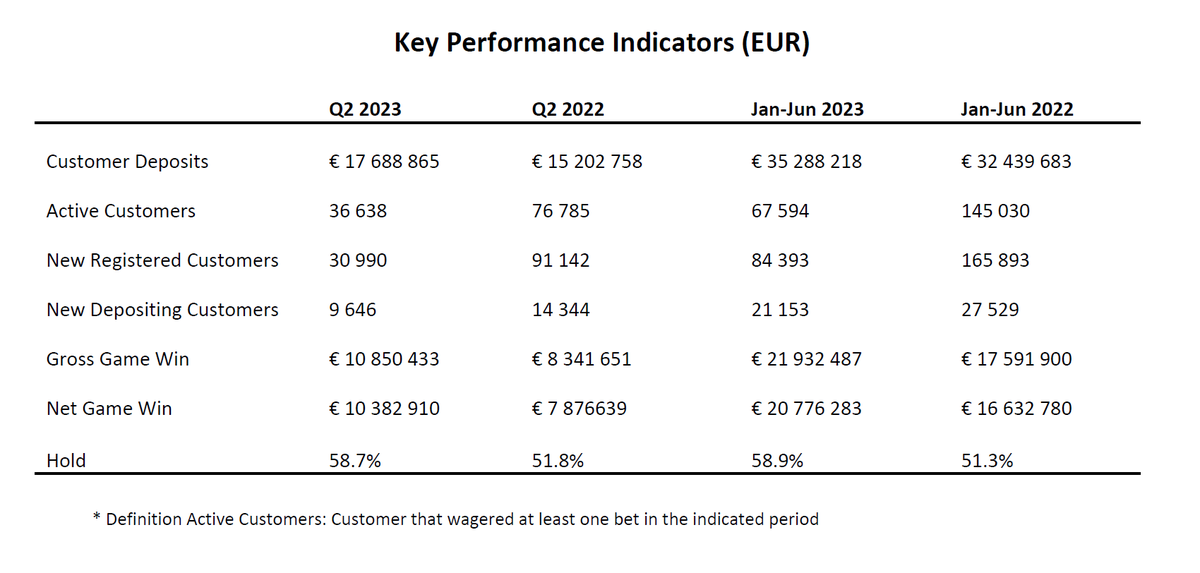

My take on Angler Gaming’s Q2 2023 report:

While 2020 and 2021 were breakout years due to Covid-19, as people had more money to spend and more time at home to spend it, 2022 was a really tough setback for Angler Gaming, posting contracting customer deposits and revenue throughout the year. In Q1 2023, we saw early indications of a turnaround, which was now further strengthened to a positive momentum in Q2.

The good:

- Strong trading in Q2 as well as good first half of Q3 on revenue, implying continued momentum in Q3. This alleviates any speculations around the need for a capital injection following the negative results during 2022. A positive dynamic for Angler is that the company is extremely asset light, requiring minimal CAPEX to grow the business

- Management has for the past year executed on a comprehensive operational improvement plan, which has started yielding results. Moreover, the inflow of new active customers seen this year is a good foundation for future growth and profitability.

The bad:

- Continued volatile COGS, which includes (i) payment processing fees to payment suppliers, (ii) affiliate expenses, (iii) gaming license fees for products, (iv) software license fees and (v) affiliate costs. The volatility in COGS are primarily a mix effect, as different games, geographic markets and source of the customer impacts the gross margin. As such, COGS are expected to remain volatile. However, with that said, such swings are expected to even out over time when looking at longer time periods, according to CEO Thomas Kalita.

- No news, but the quarterly reporting by Angler Gaming is very limited in scope, lacking both quarterly conference calls and context to current trading in quarterly reports. This continues to be a source of uncertainty, as visibility on trends and underlying drivers of the business are limited

Angler traded up 0.6% on the day of the report, with top line of 9.5 MEUR beating analyst expectations but EBIT of 0.7 MEUR below expectations. As of close of the reporting day (17/8), the company was valued at neg. P/E LTM and 9.8x EV/adj. EBIT LTM, based on the closing price of (5.09 SEK).

What were your impressions of the report of $ANGL?

Håller med, multiplarna på denna nivå var länge sedan man såg för Hexatronic. Förvisso grumlig kortsiktig utsikt med konjunkturoro, högre räntekostnader på skulden och svårberäknerliga blankare. Men fundamentalt inget som jag ser tyda på något avsteg från den långsiktiga tillväxtpotentialen.

@b1lch Håller med, I Hexatronics fall tror jag att blankare som Viceroy har en rätt stor psykologisk inverkar på investerarkollektivet, som hellre avvaktar och plockar upp bolaget när blankarna blivit motbevisade snarare än sticka ut hakan och riskera att ha fel...

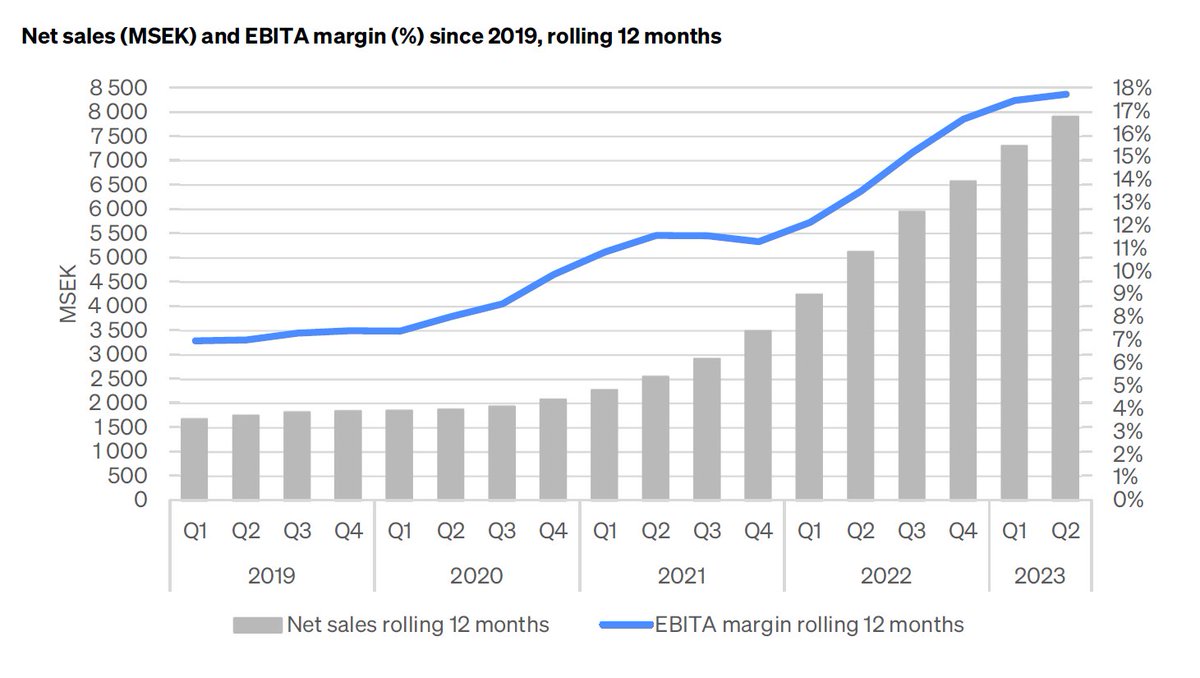

Some notes on Hexatronic’s Q2 2023 report:

The stock has had a tough first half of 2023, trading down -53% YTD. The company has for some time been targeted by short sellers, most notably Viceroy, which blame Hexatronic for opaque reporting (especially regarding organic growth), lack of investor communication and a questionable M&A track record.

So what came out of the report? The good:

- The company still exhibit organic growth of 7% in Q2, although down significantly vs. levels seen during the pandemic

- Strong free cash flow generation (ex. M&A) in the quarter of 338 MSEK, corresponding to an FCF margin of 14.8%

- Biden’s recently announced Broadband Equity, Access and Deployment program is expected to act as a tailwind for duct demand in the U.S. over the coming 7-8 years. The assessment by Hexatronic is that these subsidies will begin to show effect in 2024

The bad:

- The CEO confirmed that the organic growth will be very low or none in H2 2023, which could possibly extend into 2024

- The orderbook is normalizing back from 5 months of orders secured to pre-pandemic levels of 2-3 months. This is a natural effect of normalization in supply chains, but adds some insecurity with regards to where we will end up in 2-3 quarters if the market slows down

- The net debt of 2,519 MSEK represent 1.8x LTM EBITA, which is moderate, but like for many other businesses becomes taxing on earnings and cash flow as interest rates keep rising and remain at elevated levels. This could limit the company’s ability to keep looking for M&A targets

- While the company continues delivering a strong EBITA margin of 17.9% in the quarter and 17.7% LTM, a market slowdown might temporarily harm margins as well due to changing supply-demand dynamics

The company traded down 12% on the day of the report and is after close the 15/8 valued at 13.7x LTM P/E and 11.2x EV/LTM EBITA.

@KobeissiLetter We’re seeing similar patterns in Europe, with many anecdotal data points pointing towards decreasing industrial demand and a surge in bankruptcies…

Time for an intro! 👋

I’m Swedish, working for a Nordic LMM PE firm, with a deep interest for the hidden opportunities of the microcap world - listed as well as private.

What I’m about: sharing investment ideas and insights on the Nordic microcap scene, with the addition of the occational mid-/largecap idea to mix it up (I see the largest opportunities in microcap, but good ideas can emerge anywhere and I won’t discriminate on size).

Look out for stock analyses, portfolio updates, and anything else related.

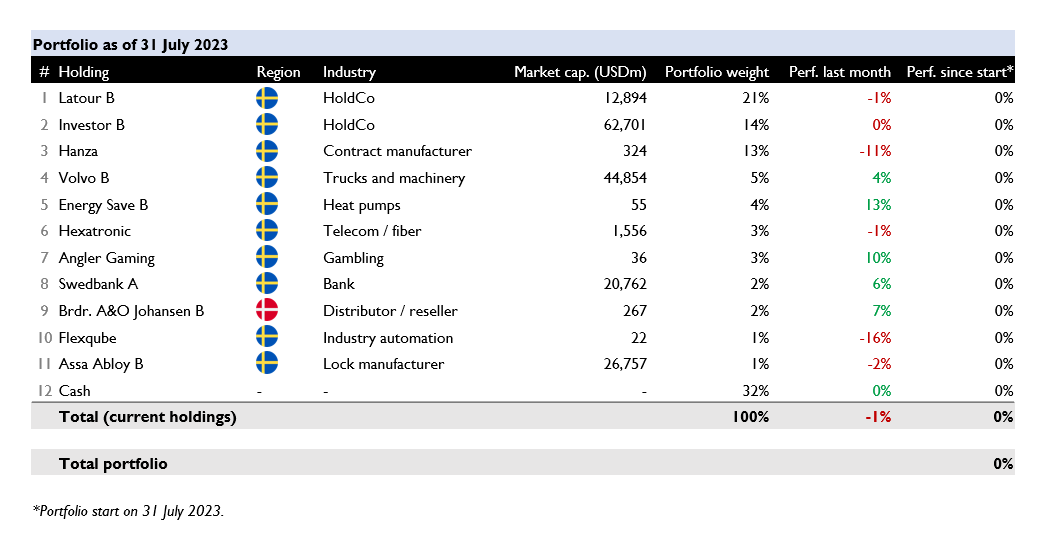

Plugging in my portfolio as of today below and will update continously. More to come!

@unusual_whales Yes, In the short term I think this acts as a sort of stabalizing force, as sellers won’t sell under certain prices and deals won’t get done, rather than being made at the market clearing price. But only until it gets really bad…