@RStallyns@PeachSabi@TheBMA@wesstreeting@BMAResidents To quote Wes Streeting when in opposition: "the power to stop these strikes lies squarely at the feet of the government".

I'll be sad to leave next year but I can't be a martyr for a system that detests us, leaves us saddled with 100k+ debt and offers a relative pittance

@DatchetTrainMan@TheBMA@wesstreeting@BMAResidents I'm not sure if tongue in cheek but that's literally what whole cohorts are doing. The pay is 100-400%+ higher, with lower workloads and better weather. Sign me up Sunny

Nuclear Fuels’ Friday Feedstock:

1. Like clockwork, we got the annual macro-driven market sell off for the BMO mining conference which took place in FLA this week, and uranium equities were not spared, falling by 7.4% on average w/w and down 19% for the month. While it isn’t much solace to investors, the uranium spot price appears to have avoided its traditional month end sell off/gamesmanship in Feb, holding relatively stable around the $65/lb mark over the past week. Hopefully this is a signal that we’ve found the bottom in the spot market. Buried in her $DML $DNN note on the CNSC hearing dates (see below), Canaccord’s Katie Lachapelle had some (more) great uranium spot market commentary, noting that the unwinding of ANU’s (a privately-owned physical uranium investment fund) 2.5Mlbs U3O8 position is now complete, as is selling in the spot market by a producer who recently re-started prod’n (also highlighted in $CCO $CCJ CFO Grant Isaac’s recent interview with Triangle Investor @capnek123).

2. The last Monday of the month also saw UxC’s Ux Long-Term U3O8 price hold steady at $80/lb, with their commentary noting that while no utilities are currently reported as active with formal public term uranium requests (likely due to ongoing geopolitical uncertainty as discussed below), several are expected to enter the market in the coming months. At some point, the contracting cycle has to pick up!

3. It was hard to keep up with the market-moving macro headlines this week. Elections outcomes in both Germany and Ontario were positive for the nuclear industry, but the positive impact of these was drowned out, first by a (now refuted) broker report that $MSFT was cancelling data centre leases in the US and scaling back plans for international spending, supposedly because of an overestimation of the demand for AI capacity. This was followed by $NVDA Q4 results on Wed, with the modest beat-and-raise and positive data centre demand commentary not being enough to stem the recent NASDAQ sell off (down 7.5% since the start of Presidents’/Family Day long weekend) to which the nuclear sector seems to have now been tied. Throw on top of this more tariff-related turbulence (whether or not they’ll start on March 4 for Canada and Mexico seems to change on an hourly basis…and will likely continue to do so until the 11th hour), and US-Ukraine minerals deal for good measure (while not uranium-related, the @JavierBlas Bloomberg article on the topic is definitely worth a read: https://t.co/GPjBDm6dbn). All the macro headlines definitely has the broader market in a risk off mode for the time being.

4. In more normal times, a flooding uranium mine would have been taken as a massively bullish data point for the uranium price and equities…but not today! Dramatic video, supposedly from ARMZ’s Priargunsky uranium mine complex in Krasnokamensk, Russia, shows large volumes of water falling down a shaft, with an article noting that 9th horizon of the mine is currently completely flooded, and workers have been evacuated from the flooded area, but with officials being quoted as “Efforts to eliminate this incident are ongoing, the situation is under control. There are no casualties. Work at underground mine No. 8 continues as usual. At the moment, the water inflow has been localized. There is no threat of flooding the mine”: https://t.co/mZUFueXdu2. I don’t have recent prod’n data handy for this operation but WNA shows it as being one of the larger ones in Russia with a capacity of 3000tU (~7.8Mlbs U3O8) per year: https://t.co/lWXRM4xajQ. We’ll stay tuned here but this could have Russia looking for even more uranium from Kazakhstan….

5. And while we’re talking about Russia, press reports out earlier this week note that Tenex, part of Russian’s state-owned nuclear corporation Rosatom, resumed the export of low-enriched uranium to the United States earlier this month. The articles note that according to the ImportGenius procurement tracking service, the Atlantic Navigator II delivered two cargoes of 15 and 85 tons of uranium to Baltimore on Feb. 12 for U.S. companies, Westinghouse and Global Nuclear Fuel Americas, respectively. To deliver the shipments, Tenex had to obtain three special licenses from the Russian authorities. U.S. company Centrus Energy confirmed the report, noting that it uses most of the raw material received in order to fulfill orders from one of its customers. https://t.co/OITl80hbWs. Why is this significant? Check out this great article from the G&M this week “As tensions rise, Canada to lean on U.S. for uranium enrichment” which does a really good job explaining reactor technology, uranium enrichment requirements, and the current state of play as it relates to export restrictions and potential tariffs. https://t.co/WcGkZFWhee(behind a paywall so let me know if you need the full text).

6. So while tariffs and mineral deals steal a lot of the headlines, the Trump administration continues to beat the drum on its pro-domestic energy and nuclear policy. At his first cabinet meeting, President Trump stated “We’re leading right now with AI…We’re leading with everything right now. But…we need resources…We have to double our electric capacity. We have to do many things…..We have to really triple, if you think of it, the electric capacity from what we have right now, if you can believe it.” Also this week, @DOE Secretary Chris Wright made his inaugural visit to the Los Alamos National Laboratory in New Mexico. At a press conference, he noted “AI is the next Manhattan Project. This is an incredibly fast-moving science and pace, and it’s critical that we win this race as well” and that “growing commercial nuclear and geothermal production could help meet increasing energy demands.” And with respect to (de-)regulation, he noted “They’re such high bars that we’ve just seen almost nothing happen in next-generation nuclear. Our goal is to get that out of the way, bring private businesses together and figure out what kind of nudge we might need to get shovels in the ground and next-generation small modular reactors happening.” Finally, thanks to @SheriffJanet for highlighting @Interior Secretary Doug Burgum’s speech at CPAC which outlined the path forward for domestic, clean energy, a made-in-the-USA nuclear fuel supply chain, and unleashing the power of American energy (the 11 minute mark is where it gets really good): https://t.co/C20sjs0QHu

7. And in terms of walking the walk, great to see news this week that Constellation Energy’s $CEG Three Mile Island Unit 1 restart is progressing ahead of schedule, with the main office building fully restored and enhancements to the training centre and control room simulator are nearly complete, as well as inspections of the plant’s steam generator, main generator, rotor, turbines, feedwater heaters and condensers and equipment upgrades progressing on schedule. Constellation is also on track to file all the required licensing and regulatory documents with the NRC @NRCgov who held a second public meeting on Feb 19. Constellation is looking to extend operations to at least 2054 and expects the plant to be ready for service by 2028. Also on the positive permitting front, the DOE @Energy has completed a final environmental assessment for preliminary activities at TerraPower’s Natrium reactor system demonstration project in Kemmerer, Wyoming, having found no significant impact from planned activities for what will be Unit 1 at the advanced nuclear plant. The DOE is proposing an authorization of federal funding for TerraPower to carry out the next stage of activities under a seven year, $2B agreement to fund TerraPower’s project under its Advanced Reactor Demonstration Program. The first unit of the Kemmerer Natrium plant is expected to be online around 2029-2030. Won’t it be great when the uranium for this NPP is produced right in Wyoming as well!

8. Sticking with the permitting theme, $DML $DNN announced that the Canadian Nuclear Safety Commission @CNSC_CCSN has scheduled the final hearing dates (Part 1 on October 8 and Part 2 on December 8-12, 2025) for the Wheeler River Uranium Project in Saskatchewan's Athabasca Basin. Canaccord’s Katie Lachapelle notes that the CNSC has up to 60 business days (12 weeks) after the Part 2 Hearing to render a final a decision (i.e. final decision in late Q4 or Q1 2025), and if approved, $DML would be in a position to commence construction activities in early 2026 (in line with Katie’s model). She notes that Wheeler River is the first project in over 20 years (Cigar Lake being the last in 2004) to reach a public hearing to consider an application for a License to Construct a uranium mine, although she also acknowledges that the dates may be further out than some investors may have expected…her understanding is that the CNSC is backed up, leading to delays on a number of approvals. We agree that having a concrete timeline is positive but this is more evidence that bringing new Canadian uranium prod’n to market certainly doesn’t happen overnight, and that’s why we see a great opportunity in the US, especially with the current administration.

9. Big week for quarterly reports in the uranium sector, with $UUUU, $BOE.A and $PDN.A all out with their numbers, as well as $EU filing a batch of new technical reports:

$PDN.A (who rang the bell to open trading on the TSX this week) had mostly pre-reported Langer Heinrich’s operational data but did maintain FY25 guidance (3-3.6Mlbs) and highlighted the potential to bring forward the mining of fresh ore (vs. processing low grade stockpiles which has been the source of some ramp up issues in Namibia).

$BOE.A looked good operationally with the Honeymoon ISR ramping up well in South Australia, with IX prod’n of ~215klbs during the DecQ and making a first shipment of 57klbs to Honeywell in Illinois, having achieved nameplate capacity at NIMCIX columns 1 & 2, with commissioning of column 3 and kiln 2 underway, as well as commencing ISR extraction from Wellfield 2. Commercial prod’n was declared on January 1, 2025 and the remaining NIMCIX columns 4, 5 and 6 will be commissioned during CY2025 as part of Boss’ strategy to ramp-up to Feasibility Study forecasts of 2.45Mlbs per year. At the Alta Mesa ISR in Texas (30% $BOE.A and 70% $EU), the first of three IX circuits was commissioned in June 2024 with the circuit nearing flow capacity in October. Alta Mesa also recorded increased wellfield recoveries as the ramp-up continues, with wellfield solution head grades having peaked at approximately 140 mg/l U3O8 and averaged approximately 65 mg/l U3O8. $BOE.A received its first pro-rata shipment of 35,181 lbs U3O8 and the second IX circuit is to be commissioned this quarter, and the third by the end of 2025.

$UUUU $EFR.C reported full year prod’n of 158klbs, at the low end of the revised FY guidance (150-500klbs) as prod’n was limited to ore from La Sal and Pandora mines due to delays in transporting ore from the Pinyon Plain mine in Arizona until an agreement was signed with the Navajo Nation in January. For the year, $UUUU sold a total 450klbs at a weighted average sales price of $84.23/lb, with 200klbs sold into a LT contract (in Q1) and the remainder sold into the spot market. However, on the conf call, the company noted that it is exercising discipline and wont sell into the spot market at current prices, as it has four long term contracts with 2025 deliveries of 200-300klbs and 393klbs in finished U3O8 inventory at the end of 2024. Of note, the Whirlwind mine in Colorado and the Nichols Ranch ISR project in Wyoming, located immediately adjacent to $NF ‘s very own priority Kaycee Uranium Project. are being prepared for prod’n within one year of a “go” decision.

Finally, on the topic of ISR projects, $EU ($NF 's largest shareholder) filed tech reports for four of its key uranium projects: Alta Mesa Uranium Project, the Mesteña Grande Uranium Project and the South Texas Integrated Uranium Projects (all located in, you guessed it, Texas), as well as for the Gas Hills Uranium Project in Wyoming. These reports provide updated mineral resource estimates, as well as preliminary economic assessments (PEA) and are great reading for those interested in ISR projects in the US. Details here https://t.co/Hifi6z4KYH let us know if you’d like a copy of the 43-101 versions (also avail on SEDAR).

10. PDAC kicks off on Sunday, taking place at the Metro Toronto Convention Centre. $NF will be at booth 3030 (adjacent to $EU who is at booth 3028) inside the Investors Exchange exhibit hall, featuring a 55-gallon Uranium Drum and chances to win some great Wyoming-themed prizes (think the OTHER yellow metal!). We'll also be participating in 1x1 meetings at PDAC as well as a number of other events...contact us if you'd like to schedule an update. Finally, we’re a sponsor for the annual “Uranium Night” on Monday…if you’re attending, please “vote” for $NF and our chosen charity, the Kaycee Wyoming Chapter of FFA (Future Farmers of America)…we like to remember the first part of our favourite saying: “If it can’t be grown, it has to be mined (or pumped!)” and this is a very active organization for young people doing great work in our local community.

As a consultant I can protest against the associate scheme until the cows come home but some will always accuse me of elitism and pearl clutching

Sometimes it’s just better to let an associate call up a national radio show and let them do the talking for me

$GLO 🇳🇪 My 16-page analysis covering Niger’s geopolitical risks, management decisions, the implications of potential DFC and JV financing strategies, and the effects on DASA’s valuation.

The link to the PDF is in the post below. You can view it online; no download required.

1/2

Constellation Energy CEO on demand for energy: "The fact of the matter is demand for our products is, it is expected to grow at levels we haven't seen in a lifetime...These charts show you revisions in their demand forecast over the last few years."

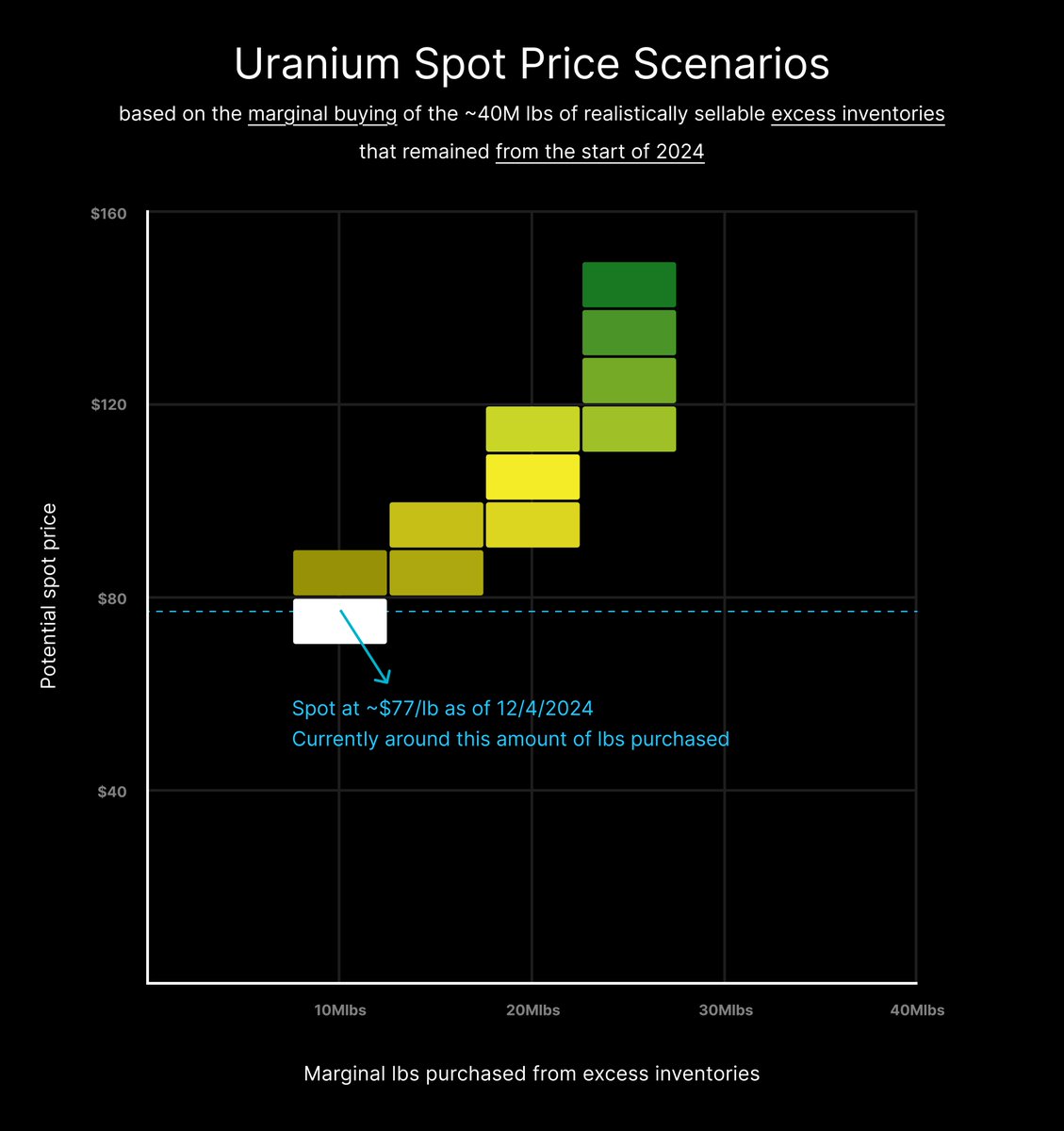

#Uranium Spot Market & Excess Inventories

- - - - - - - - - - - - - - - - - - - - - -

Spot Price: Why has it been down?

Marginal Sellers: Who has lbs to sell?

Marginal Buyers: Who needs to buy?

Volume: How much has been sold this year?

Model: What are price discovery scenarios?

Catalysts: Which are relevant to spot in ‘25?

The TL;DR: From the start of 2024, there were ~40M lbs of realistically sellable excess inventories. Low marginal spot buying in 2024 was due to a combination of (1) lbs drawn down from the operational inventories of producers, (2) lbs sold from those with excess inventories, (3) lbs loaned from those with excess inventories, (4) a temporary conversion bottleneck and (5) some recent bearish events that reduced demand. However there is (i) a declining amount of these lbs that remain, (ii) the temporary conversion bottleneck should start easing in 2025 and (iii) most of the bearish events are in the rearview mirror.

https://t.co/iJlxOaYEH8

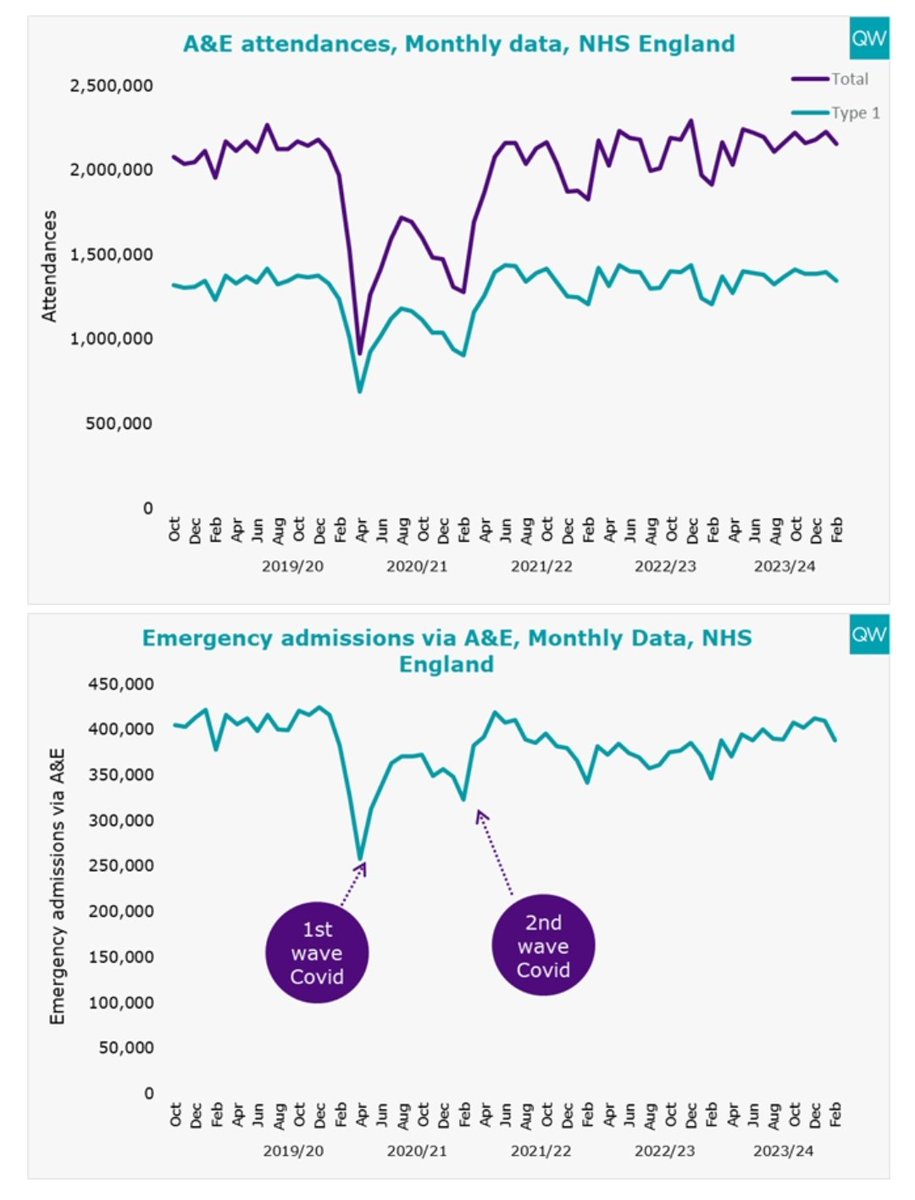

A&E rising demand isn't driving long waits in A&E. Attendance rates are not dramatically up from pre-pandemic levels. The real issue is collapse of social/community care provision & some increased acuity. This is driving longer stays & means fewer open beds for ppl to go into

@RCPhysicians Now no-one is suggesting doctors don't make mistakes (of course we do).

But imagine how many more mistakes you're likely to make if you have no medical degree, no post-graduate training & no defined scope of practice & yet you still see undifferentiated patients. 5/n

@RCPhysicians No-one has ever asked you, the public, if you consent to this radical change to NHS care.

And there are heartbreaking cases in which patients have died after believing they had seen a doctor, yet instead saw a PA who misdiagnosed their condition. 4/n

https://t.co/3zbbkZddwd

Dear 🇬🇧,

Please read - this NHS scandal potentially affects you all.

🧵 Having studied the data, just released, from the @RCPhysicians members' survey on PAs, I couldn't be more disgusted by the lack of probity, honesty & fairness of those who lead my Royal College. 1/n

Yesterday 6pm, the RCPEGM was leaked by an anonymous account onto YouTube. Having watched it, these are some of the most jaw-dropping moments I heard, some not even factually true. Everyone should watch it for themselves though and make up their own mind. Link at the end.

Genuinely baffled by this. 🤔

A BBC journalist has blocked me.

What for you might ask?

Well my only interaction with them is shared below.

I asked a perfectly legitimate journalistic question in relation to a news story they had covered.

🤷🏻♂️

It is the profile of spend over time. For years NHS was on a starvation diet, then a big uplift and the pandemic....what was needed was sustained funding not feats and famine. Its why hospitals are crumbling, we dont have decent computers and deadly staff shortages.

Concerns 🧵

1) patient in Heart Block - which can lead to sudden cardiac death - not identified by PA

2) instead of speaking to supervising GP when seeing pt at 3pm, waited to speak to OOH at 6pm

3) No info re pt whereabouts in this time - sent home? In GP surgery? Not safe.

1/5

12,000 people applying for 4,000 GP spots.

Did I or did I not say this was going to become untenable?

When everybody and their donkey can apply for thirty specialties, those with an actual interest in the specialty are going to get shafted.

Sigh. Such dumb management of a critical national service is frankly embarassing. Plus the dangerous unintended consequences on culture.

Mid Staffs A&E was a warzone precisely because of a culture that demanded hitting targets above care. We've learned nothing.