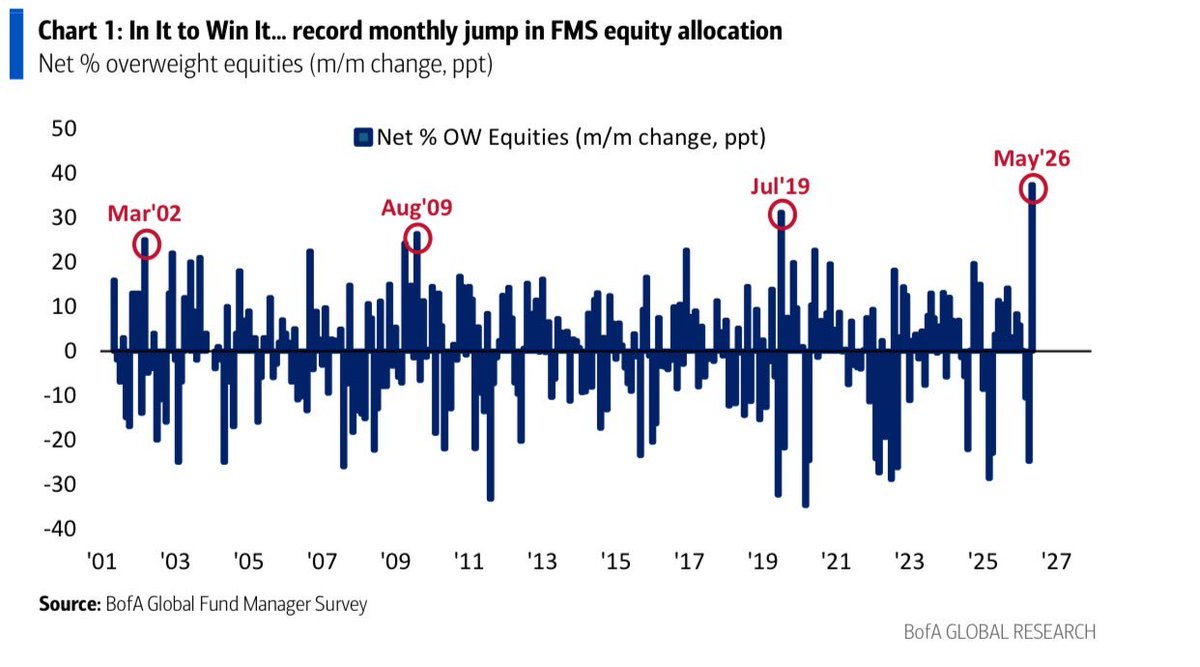

Lo que mata un mercado alcista no suele ser la bolsa, son los bonos. El 30 años americano cerró ayer por encima del 5%. Umbrales psicológicos de Hartnett: UK 6%, USA 5%, Japón 4%. A las urnas de medio término con inflación camino del 5%, ojo.

Bullshit. Try measuring sigma for the actual range of the day in points, as grown ups actually do.

Friday’s range in the Nasdaq was almost double the points lost during 2007-2008 all together.

A country becomes prosperous when its brightest people build companies, create jobs, and take risks.

When they shift from entrepreneurship to a government desk, prosperity slowly stops being created.

Germany became rich through builders. It won’t stay rich with bureaucrats.

This is wild. While most countries have enjoyed decent growth in real wages, Italy and Spain have seen none for three decades.

Maybe the introduction of the euro there wasn’t the best idea? Pressure on wages is the only avenue left when one cannot devalue the currency anymore.

be iker jiménez

> te dan un programa de radio para un verano

> en la primera emisión te dice el técnico de sonido que se han borrado todas las grabaciones 30 segundos antes de entrar en directo

> improvisas y salvas el primer programa

> el verano va tan bien que en septiembre te dicen que sigues

> tu programa se convierte en líder absoluto de audiencia en su franja horaria

> decides llevar el formato a la tele

> te dicen que no va a funcionar, que nada que funcione en radio funciona en tele

> estaban equivocados, funciona

> en paralelo sigues con la radio

> un gobierno de derecha te da un toque porque te metes en un tema del que no les interesa que se hable (ébola)

> sientes que tu cadena te deja vendido y les dices que ahí se quedan

> te vas de la radio teniendo unas cifras de audiencia salvajes y te centras solo en la tele

> tu programa se convierte en uno de los más longevos de la historia de la televisión en españa sin cambiar de presentador (solo superado por jordi hurtado)

> llega una pandemia y la cadena paraliza la grabación de tu programa

> no te quedas quieto y te montas un programa en youtube desde tu casa

> lo revientas tanto en internet que la cadena te llama de urgencia para hacer un programa en prime time en directo

> ese programa también tira y decides cambiarle el nombre por si acaso decides seguir con él para hablar de otros temas cuando pase la pandemia

> te dicen que tú solo puedes hablar de ovnis y de fantasmas pero decides que el programa se centre en política

> aplastas sistemáticamente a la competencia directa en tu misma franja

> la cadena te propone pasar de hacer un programa a la semana a hacer cuatro a la semana

> dudas pero aceptas probar durante unas semanas a ver qué tal va

> va bien

> el presidente del gobierno (de izquierda esta vez) te llama bulero en el congreso de los diputados

> efecto streisand

> tu programa supera en audiencia a la gran apuesta de la televisión pública para esa misma franja

> tu mujer ha hecho cada uno de los programas contigo desde el día 1 de radio

> como no tienes suficiente con 5 emisiones a la semana, te da por componer música y te haces tú mismo la sintonía del programa

os caerá mejor o peor, pero es la cabra absoluta

The disconnect between oil prices and oil Twitter / oil experts is maybe the greatest disconnect I’ve ever seen in markets.

Inventories plunging towards functional bottoms, price plunging with it.

Incredible to watch everyone on #OOTT losing their sanity this week.

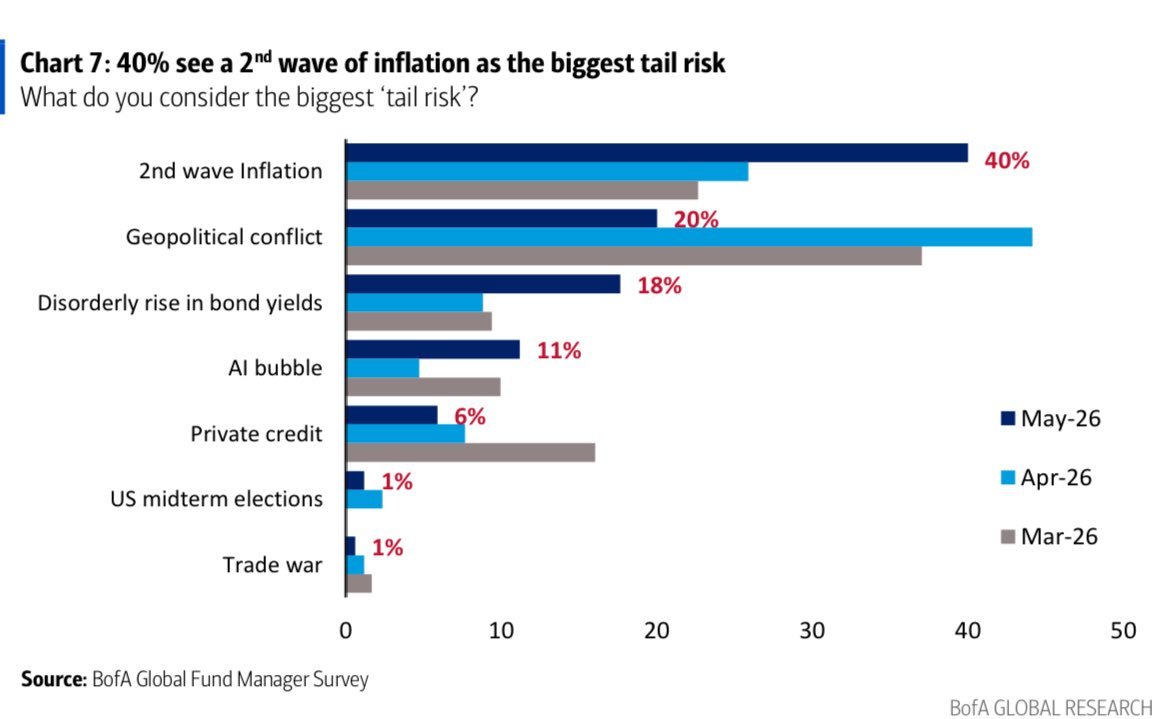

Nuestros amigos de Bianco Research lo dicen claro 👇

Los gestores de fondos están comprando bolsa como cobertura contra la inflación.

El problema: eso no ha funcionado en más de 100 años.

BofA lo cuantifica: cuando el CPI supera el 4%, el SPX cae de media un -4% en los siguientes 3 meses y un -7% en los siguientes 6 meses. El CPI interanual de abril está en 3.8%. Ya casi estamos ahí.

Buffett lo advirtió hace casi 50 años — en 1977 — y el mercado lo volvió a ignorar.

Los tres grandes riesgos que más preocupan a los gestores ahora mismo:

— Segunda ola de inflación (40%)

— Conflicto geopolítico (20%)

— Subida desordenada de yields (18%)

El 78% en tres riesgos que en realidad son el mismo: la guerra sigue empujando el crudo, el crudo empuja la inflación, la inflación empuja los yields.

Y los que no recuerdan la historia están condenados a repetirla.

— George Santayana, 1905 🎯

#Inflation #SPX #Macro #BofA #SpreadGreg

This dynamic holds true everywhere.

Everyone in Mr. Beast’s YouTube pod ended up w over 1M followers.

Many traders in Lukas’s pod went on to become elite.

The standards and environment you set for yourself matter. As do the people self-selecting to be in these groups.

I see it on the prop side all the time. For every 25 people you hire, 1 or 2 of them works their ass off and does whatever it takes to be on the best team.

Soybeans are entering a historically favorable seasonal window. From TDY #66 to 90, returns have tended to skew higher, reflecting a consistent cyclical tailwind during this period. Seasonality alone is not a guarantee, but it does highlight a window where the odds have often leaned positive.

Read Full Analysis: https://t.co/b5EidO7ZgA

For a ceasefire, the fire does not seem to be ceasing. The UAE and Kuwait are under attack, and Iran says it is under attack too. Beyond the ceasefire itself, the bigger question is that the plan still looks unclear when it comes to what follows, assuming the ceasefire actually holds.

BREAKING: Iran says it has "forced" the US to accept its "10-point plan" which includes the following terms:

1. Commitment to non-aggression

2. Iran’s control over the Strait of Hormuz

3. Acceptance of Iran's uranium enrichment

4. Lifting of all primary sanctions

5. Lifting of all secondary sanctions

6. Termination of all UN Security Council resolutions

7. Termination of all Board of Governors resolutions

8. Paying compensation to Iran

9. Withdrawal of US combat forces from the region

10. Cessation of war on all fronts, including in Lebanon

Trump says this plan is "a workable basis."

".... The only long-term solution is new infrastructure—making a massive, internationally coordinated investment in energy corridors that bypass the Strait of Hormuz entirely... " -- @amoshochstein

https://t.co/hvu4ACTwok

It is a very hard situation to handle for Bessent.

1. The manufacturing push by Trump needs exports to be competitive, meaning a weaker dollar to given for manufacturing in US to be competitive on the world stage.

-> Weaker dollar = Stronger incentives to sell.

2. The disregard for allies in this war led to collocations to be weakened and the Us threatening leaving NATO is leading partners to reconsider the US-debt as something they want on the balance sheet.

-> Weaker alliances = Treasuries being sold

3. As the US needs to refinance 30% of $30 trillion USD over the next 2 years, they are caught.

As allies and Asia sell USD and Treasuries, yields spike higher, making it very expensive to refinance the debt.

-> Higher refinance rate = Inflate USD to repay debt.

4. Add to it a potentially weakening of the petro-dollar, credit stress and a potential recession...

This war will cost way way more than almost everyone sees, the Oil is the tip of the iceberg.