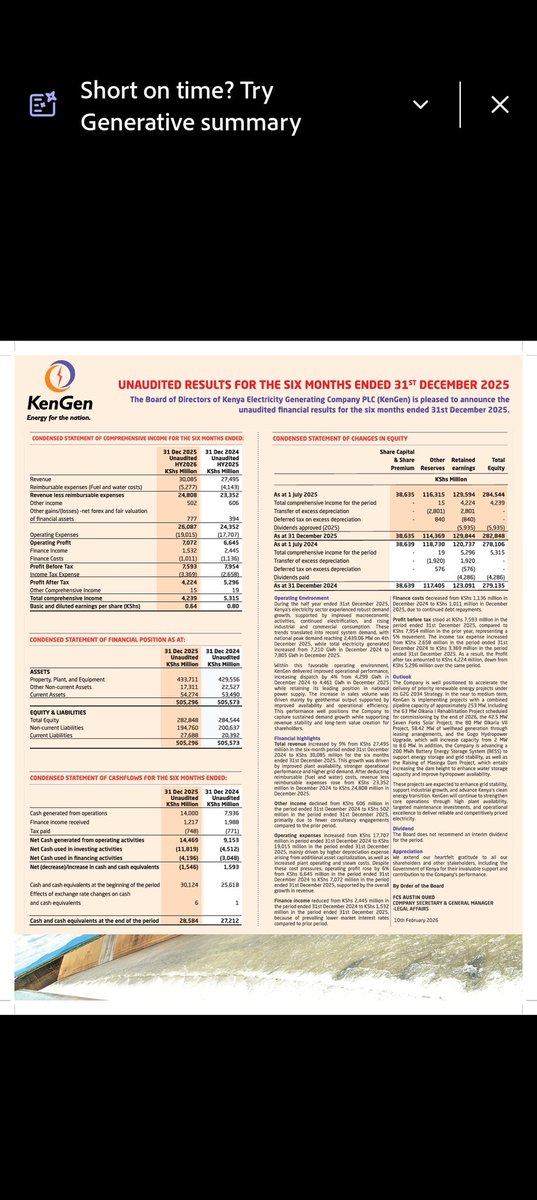

The NSE is set for another banking sector addition. Family Bank is set to join the market on 23 June 2026 through a listing by introduction.

Learn How to Invest in Financial Markets

CBK projects that inflation will remain below its upper target of 7.5%, based on the assumption of a de-escalation of tensions in the Middle East.

Learn How to Invest in Financial Markets

The issuance of a Kenyan identity card to a foreigner who vows that never requested it shines a spotlight on the rot in the office that bestowed this important responsibility. Bosnian national Zlatko Gegic told the High Court that he was given a Kenyan ID card after he requested a residence permit.

https://t.co/Gxmew53qkM

Banks in general need to increase their lending to the private sector, otherwise their growth and profit margins will stagnate or decline.

Learn How to Invest in Financial Markets

In 2026, banks should be approached as value or income plays, rather than growth investments.

In other words, buy Equity, KCB or any other undervalued bank with a strong ROE, for its undervaluation, not on expectations of higher income.

Learn How to Invest in Financial Markets

In FY 2025, banks' net income growth was primarily driven by lower interest expenses and in some cases lower loan loss provisions.

Since interest rates are already low, the scope for further reductions in interest expense is limited.

Learn How to Invest in Financial Markets

Tanzania are not in a position to supply us with 1000MW at the moment.

However by the end of 2026, the 2135MW Julius Nyerere Hydropower plant with be connected to Dodoma. This effectively means Kenya (Isinya substation) is connected to Dodoma through the existing Tanzania 400kV backbone.

Further, JNHPP has Automatic Generation Control system.

https://t.co/KKPvVEABrI

@WaruhiuFranklin@NSE_Investors is right. KCB has not included non-controlling interest in its computation of shareholders' equity.

It would only require subtraction if it was included in the computation of shareholders' equity except that it's not.

Learn How to Invest in Financial Markets

The Finance Bill, 2026 was published on 30th April and is now before Parliament and every Kenyan deserves to know what is in it.

The government targets Ksh3.63 trillion in revenue for 2026/27 and a wider budget deficit of 5.3% of GDP in the 2026/27 fiscal year (July-June) up from 4.7% in 2025/26. These are not unreasonable fiscal objectives but the manner in which the burden of achieving them is distributed is a cause for serious concern.

On tax filing timelines, the Bill moves the income tax return deadline to April 30th which is two months earlier than the current June 30th and compresses nil return filing to January 31st. This reduces the time available for audit completion, cash flow planning and compliance. For small businesses and individual traders, this is not administrative reform. It is an additional compliance cost they can ill afford.

On mitumba, the Bill inserts a new Section 12H into the Income Tax Act which deems profit at 5% of customs value payable upfront before goods are released by KRA as a final tax. A trader importing a bale worth Ksh1 million pays Ksh50,000 regardless of whether they make a profit or a loss. I cannot in good conscience describe this as equitable.

The Bill increases residential rental income tax from 7.5% to 10%. Absent a serious enforcement framework, this will drive non-compliance rather than revenue. The government must fix the enforcement gap before it increases the rate. One without the other is burden-shifting.

On digital financial services, the Bill removes existing VAT exemptions on money transfers and payment processing. These are the tools of financial inclusion that millions of Kenyans including the very people this government says it wants to reach rely on daily. Making them more expensive will not serve the objective of a broader tax base.

By including interchange and merchant service fees within the definition of management or professional fees for withholding tax purposes, the Bill introduces a compliance burden into automated banking processes. That burden will be passed on to businesses and ultimately to consumers.

The amendment to Section 24 of the Income Tax Act empowers KRA to deem at least 60% of a company's undistributed income as dividends for tax purposes. This fails to account for legitimate decisions on reinvestment, working capital and business growth. It is a retrogressive measure that sends the wrong signal to the investors Kenya needs.

A 25% excise duty on telephones for cellular and wireless networks is proposed. A phone is not a luxury. It is how Kenyans bank, communicate, conduct business and access government services. Parliament must interrogate this carefully.

On PAYE, Kenyans were led to expect relief and a restructuring of the tax bands to ease the burden on salaried workers. That proposal does not appear in this Bill. That is not a minor omission. An explanation is owed to every employed Kenyan who was waiting for it.

To be fair, the Bill is not without merit. The reduction of corporate tax for non-resident companies from 37.5% to 30% improves our investment climate. The extension of the tax amnesty to cover liabilities up to 31st December 2025 provides a genuine and welcome pathway to compliance. VAT exemptions on electric buses, bicycles, dialysers, animal feed raw materials and PPP infrastructure are sensible measures. The clarity introduced on trust taxation ensuring beneficiaries are not taxed on income already taxed at the trust level and the recognition of gratuity contributions as exempt income are also steps in the right direction.

Be that as it may, we cannot afford a repeat of June 2024. Parliament must discharge its oversight role with the seriousness this moment demands. They should not merely rubber-stamp what the Treasury has placed before it. Every clause must be scrutinised. Every punitive or ambiguous provision must be rejected or amended.

#FinanceBill2026 #PublicParticipation

@lemanxq The 1st schedule to the income tax act exempts bonds, notes & other securities issued to raise funds for infrastructure & other social services.

KMRC did not apply for tax exemption. It sought confirmation of tax status as per the law.

Learn How to Invest in Financial Markets

Both I&M and KMRC have priced their MTNs at 12.20%. However, I&M's MTNs are taxable with an after tax yield of 10.37% while KMRC's MTNs are tax exempt with an after tax yield of 12.20%.

Learn How to Invest in Financial Markets