To build long-term investment success, it's vital to manage ourselves, not just our portfolios. Nobody has greater insight on how to manage our cognitive biases, emotions, mindset & physiology than Emily Haisley, my latest guest on the #RicherWiserHappier podcast. She heads the Behavioral Psychology team at @BlackRock, the world's largest asset manager. This conversation offers a fresh, unique & practical perspective on the psychology of investing.

Listen: https://t.co/Q1gDGD8hma

Watch: https://t.co/9UuwRBPEwQ

@that_stocks_guy Loved this! Excellent write-up and a great chat with Ben - I especially liked his last answer where he outlined the huge potential for scalability that the team and its partners are currently working on 🔥🔥🔥

Huge thanks for this, Charles 🙏

@asjwebley Excellent update, Andrew.

Thank you, as ever, to you and all the team @smarterwebuk for all your hard work on behalf of shareholders 🙏

And tbh, I'm personally enjoying the price volatility and just keep regularly adding to my #SWC holding!💪

#GEO announces highly positive initial field findings at the Gorge Project, with three priority prospects confirmed:

📍 Gorge Mine Prospect

📍 401 Prospect

📍 Central Zone Prospect

Key findings include:

🔹 Visible gold observed at the Gorge Mine and 401 Prospects

🔹 Coarse gold observed in areas of known historic activity

🔹 Copper-rich gossan identified at Central Zone

🔹 Mapping highlights favourable structures for gold mineralisation

🔹 Historic hard-rock workings, shafts and costeans confirmed

These findings further support GEO’s view that Gorge has significant exploration potential, with systematic follow-up work now advancing.

Read the full RNS below 👇

https://t.co/kpex0y7uAv

#GorgeProject #Mining #Exploration #Gold #Copper #Australia

📍 Gorge Mine Prospect Spotlight

#GEO has identified the Gorge Mine Prospect as a priority prospect for follow-up work at the Gorge Project.

Key findings include:

🔹 Visible gold observed in quartz vein samples near historic shafts and workings

🔹 Historic records refer to extracted ore reportedly returning more than 450 g/t Au, equivalent to 14 oz/t Au

🔹 Historic records refer to bedrock mineralisation extending for more than 1km of strike

🔹 Historic records also refer to 12 tonnes of ore extracted and processed, yielding gold, silver and lead from a 1.8m-wide quartz vein

🔹 Five open vertical shafts identified, estimated to remain open to depths of at least 20–30m

🔹 No modern exploration or drill testing recorded at the Gorge Mine target area

The combination of visible gold, historic high-grade records, historic workings and no recorded modern drill testing supports GEO’s view that Gorge Mine is a high-priority prospect for systematic follow-up work.

Photos from the field programme below 👇

#GorgeProject #GorgeMineProspect #Mining #Exploration #Gold #Copper #Australia

Great to see #COBR featured in @DiscoveryAlert, exploring the unique heavy rare earths opportunity emerging at Boland.

Good explanation of the value in ISR for production economics.

🔗: https://t.co/aQVxXrrGn9

#SouthAustralia#RareEarths

Our ambition is to become one of the largest companies in the UK. I believe that our strategy gives us a credible path to achieving that goal.

At the centre of our approach is the balance sheet. We are building a balance sheet around what we believe is the best form of capital available: Bitcoin. As that balance sheet grows, it creates opportunities across the business. It can support the growth of our operating activities, enable strategic acquisitions, provide flexibility to pursue new opportunities as they emerge, and allow us to further strengthen and expand the balance sheet itself.

These are often viewed as separate strategies, but we do not see them that way. They are all connected. We have one strategy, and it revolves around building and intelligently deploying a strong balance sheet. Everything else flows from that foundation.

Because of this we think that it is important for investors and potential investors to understand this balance sheet at any moment in time and increasingly these investors include institutional investors who are used to specific metrics.

We believe the term "mNAV" is currently being used in ways that can create confusion rather than clarity. Various companies and commentators often calculate the metric differently. Some use Market Capitalisation as the numerator, while others use Enterprise Value. On the denominator side, some use Net Asset Value, while others use the market value of Bitcoin holdings, often referring to this as "BTC NAV" despite it being closer to a gross asset value than a true NAV calculation.

The treatment of outstanding securities is also a further element. We use the fully diluted number of shares which includes all in the money warrants and then factors in cash linked to the warrant proceeds, however if we were creating our analytics from the beginning, understanding everything that we know now, we would treat Smarter Convert as debt rather than an instrument that will convert into equity.

In traditional finance, mNAV generally refers to Market Capitalisation divided by Net Asset Value, producing a premium or discount multiple relative to NAV. However, many of the mNAV metrics currently used in the Bitcoin treasury company sector employ neither of these measures, resulting in a broad range of calculations that share the same label but convey very different information.

We believe this lack of standardisation becomes increasingly problematic as treasury companies introduce debt, preferred equity and other financing instruments. As capital structures become more complex, comparisons between companies become less meaningful if investors are not working from a common framework.

For this reason, we updated our analytics dashboard during the week and are moving away from mNAV as a primary valuation metric. Instead, we now display "Fully Diluted EV vs BTC Value", calculated as Fully Diluted Enterprise Value divided by the current market value of total Bitcoin holdings. We have also added charts that show “Net Bitcoin Value Per Fully Diluted Share” and “Net Sats Per Fully Diluted Share”. For all calculations on our analytics page, you can hover over the question marks and view the formulas.

In our view, this provides a completer and more transparent picture of the value of a Bitcoin treasury company. We believe investors should also consider several important measures, including leverage or amplification, Bitcoin per share growth over time ("Bitcoin Yield"), and the sustainability of that growth going forward. The last being harder to statistically analyse.

This naturally leads to another question we were asked this week: what is the single most important metric for evaluating a Bitcoin treasury company?

Our view is that there is no single number.

Our treasury objective is straightforward: to increase the amount of Bitcoin attributable to each share over time. However, we would encourage investors to assess performance over quarters and years rather than days or weeks. The key question is whether management decisions are increasing Bitcoin per share on a sustainable basis.

For a simple, ungeared treasury company, the analysis can appear relatively straightforward. One could argue that issuing shares is accretive whenever the value received exceeds the Bitcoin value attributable to the shares issued. However, the reality becomes considerably more nuanced once debt financing, debt repayment, warrant repurchases, share buybacks and other capital allocation decisions enter the equation.

A transaction that appears dilutive when viewed through one metric may in fact be accretive when viewed through another. This is precisely why we believe the industry requires better and more transparent analytics. As treasury strategies become more sophisticated, and treasury companies become much larger, investors need to consider multiple variables rather than relying on a single ratio or headline figure.

For public companies, such as The Smarter Web Company, there is an additional dimension. Investors should not only consider the Bitcoin treasury itself, but also operating revenues, corporate costs, cash generation and the broader business activities that sit alongside the treasury strategy. These elements can have a meaningful impact on the company's ability to grow Bitcoin per share over the long term.

If Bitcoin treasury companies are to mature into a recognised institutional asset class, the industry will benefit from greater consistency in reporting standards, valuation methodologies and performance metrics. Investors should be able to compare companies using measures that are transparent, widely understood and economically meaningful.

Over the coming months, we intend to continue refining our analytics framework and working with others across the sector to help improve consistency and comparability throughout the industry.

On Monday this week we announced an update to our ATM-style facility. We raised £145,670 (before expenses), equivalent to approximately £0.29 per share. The ATM-style facility continues to be an important part of our capital markets toolkit and provides us with valuable flexibility as we execute our strategy.

Throughout the week we continued sharing the remaining videos filmed at the Bitcoin Treasuries Unconference UK. As a reminder, early bird tickets for the 2027 event are available on our website.

Looking ahead, we have decided to rename the event series from Bitcoin Treasuries Unconference UK to Bitcoin Treasuries Conference UK. As we scale both the event and help scale the wider industry in the UK, we believe this name will be more familiar to a broader audience. The core spirit and format of the event will remain largely unchanged, but we believe this evolution will help us reach and engage a larger community.

I would also like to remind shareholders that we have an important vote at our General Meeting on 17 June. Shortly afterwards, we will announce the results via RNS. Thank you to everyone who has already taken the time to vote. Depending on your platform, there may still be an opportunity to submit your vote if you have not yet done so. Voting is an important part of share ownership, regardless of whether you vote for or against a resolution.

Finally, I would like to acknowledge that our share price is not currently performing as well as I would like. I cannot control the market, but I can control what we are building and the two certainly seem a little disconnected from where I am sitting.

While short-term market performance can be frustrating, my conviction in the direction of the business has never been stronger. I believe we are executing the right strategy, and I am excited about where we are heading. As our progress becomes more widely understood and the opportunity ahead of Smarter Web becomes clearer, I believe the market will recognise the value of what we are building.

Thank you for your support.

LSE: #SWC | OTCQB: $TSWCF | FRA: $3M8

There's only 4.6% of #Bitcoin left to be mined.

In 2 years, it will be just 3.1%.

At this point, new supply issuance will be cut in half permanently.

People are currently focused on when the bear market is over (is it now? in 3 months?)...

but the supply shortage that will fuel the next bull market is already loading.

This is the heart of Bitcoin's game theoretic inevitability.

Bitcoin has increasing scarcity of new supply issuance... terminating in absolute scarcity.

Both of these properties are a first in the world of store-of-value assets (because a set-in-stone supply schedule is not possible in the physical world - only in the digital world).

And yet, 99.9% of the world does not realize these simple truths, and as a result has not yet adopted Bitcoin as their primary savings technology / treasury asset.

They will have to bid for the meager 4.6% of new supply left, or try to buy existing coins from the 0.1% who already understand what Bitcoin is.

All you have to do is remember what you're holding, accumulate if you can, and wait for economic reality to continue to play out.

When the 99.9% come bidding for your coins, at what price will you sell them some?

#PRD

🔑 "TO DETER PREMATURE PROJECT DILUTION."

Six words in today's #PRD RNS that rewrite the Guercif endgame.

In February, PRD asked for a full carry. Today they publicly withdrew the ask. Pre-drill dilution of MOU-6? "Commercially no longer attractive."

Why would a £33M company refuse free drilling capital?

Because the ITR told them what they'd be giving away:

1️⃣ NPV10 of $96M NET — on the pilot CNG case alone

2️⃣ 79% IRR off just $37.8M total CAPEX

3️⃣ A 10-year Moroccan tax holiday a partner would consume

4️⃣ 498 BCF net 2U that a carry-partner would capture for the price of a $4M well

5️⃣ A self-funding route now in place: placings done, long-leads bought, Trinidad cash flow building, and — for the first time ever in a PRD RNS — reserves-based lending on the table

"This window of opportunity must be exploited before the cycle of positive sentiment might yet turn again." — Paul Griffiths, this morning.

The asset-level door didn't close today. The price went up. And anyone who wants Guercif at pre-drill numbers now has one route left — and a window that shuts at spud.

⚠️ Independent research only. The transaction inference is thesis, not disclosure. Not investment advice. DYOR.

#PRD @PredatorOilGas #Morocco #Guercif #LSE #MandA #smallcaps

@Blowster85@AM231982@GrahamHengland

#PRD

🔬 MOU-6 IS NOT ONE TEST. IT IS TWO. AND THE SECOND ONE IS THE COMPANY-MAKER.

Everyone will watch the flow rate. Fine. The DSTs across the TGB-6 fan answer the question that has haunted Guercif since MOU-1: can these sands deliver gas at commercial rates once you stop destroying them with the wrong mud?

The ITR's formation-damage post-mortem is forensic: 250–600 psi of overbalance, water-based mud shredding potassium-rich clays, kaolinite plugging the perforations, resistivity logs reading low because of invasion. The fix: vertical well, intermediate casing, on-balance drilling, oil-based mud preference, big imported guns, nitrogen lift standing by.

And here's the detail that made me sit up — the ITR cites ONHYM's own Meskala field, where a well written off for the identical clay-plugging problem was worked over years later and put on production. PRD's state partner's own field history is now Exhibit A for the MOU-3 narrative.

But the second test is the one to watch:

🧪 The MDT programme. Specialist pressure tools, closely-spaced sample points down the entire TGB-6 column. Purpose, in the ITR's words: to demonstrate "a continuous vertically connected gas column which exceeds the vertical extent of the currently mapped structural closure."

Translation: if the pressure gradients connect — the 11 km² structure becomes an 81 km² trap.

96.5 BCF becomes a pathway to 665 BCF gross.

And it doesn't even need a spectacular flow rate to do it. The gauges decide.

One well. Two verdicts. August.

The market is pricing neither.

⚠️ Independent research only. Not investment advice. DYOR.

#PRD @PredatorOilGas #Morocco #Guercif #naturalgas #LSE #geology #smallcaps

@GrahamHengland@AM231982@Blowster85@Share_Talk@ONHYM_Official

#PRD

🧵 #PRD THREAD PART 2 — THE DEAL ARCHITECTURE THE MARKET HAS COMPLETELY MISSED

Going deeper. Because the surface barely scratches it.

🔬 LET'S TALK ABOUT WHAT A "DEAL" ACTUALLY LOOKS LIKE HERE

- The market thinks PRD needs to flow gas before anything happens.

- The HOA terms already disclosed tell a completely different story.

- From the October 2025 investor presentation — publicly recorded, publicly available — Griffiths laid out the deal architecture in plain English:

💬 "Initial cash payment... past cost repayment... royalty tied to production milestones... wellhead gas purchase commitment."

Break that down:

💡 Past cost repayment — PRD has capitalised £18.7 million in Moroccan expenditure. That comes back as upfront cash at signing. Before a single molecule of gas flows.

💡 100% appraisal well funding — the acquirer drills and pays for MOU-6. PRD contributes zero capex. The "flow test" is on the buyer's balance sheet, not PRD's.

💡 Royalty tied to production milestones — PRD participates in the upside after the deal closes. The initial consideration is not contingent on flow rates.

This is not a farm-out. This is a structured exit. The wells don't need to flow for PRD to get paid. The deal structure was engineered specifically so they don't have to.

🧬 THE ASSET THE MARKET HAS NEVER PROPERLY VALUED

Most retail investors think PRD is a single biogenic gas play. It is five distinct hydrocarbon systems stacked on top of each other:

🔴 Biogenic gas — 441 BCF 2C certified. Established. Derisked. The floor.

🟠 Thermogenic gas — GRF-1 well (1972) confirmed C2/C3 thermogenic shows at depth. The Jurassic system is real, charged, and entirely undrilled within the Guercif licence.

🟡 Helium — confirmed at MOU-3 (0.3%) and MOU-5. MOU-2 helium interval described by Griffiths as 4-5x thicker than MOU-3 with a ~60km² closure. Independent risked estimate: 1.86 BCF net PRD. Never in a single RNS.

🟢 Oil — geo-microbial survey (GMT, 2006) confirmed oil signatures at MSD-1 and the SE seepage anomaly. Boudraa and Tselfat oil fields sit directly on trend. PRD cited them once — in May 2022 — and never mentioned them again.

🔵 Hydrogen — detected at MOU-3. Never disclosed in any RNS filing. Confirmed by Griffiths in the October 2025 presentation only.

The market is pricing in the biogenic gas floor — and nothing else. The acquirer will be buying all five systems.

🏔️ THE ASSET THAT WAS DELIBERATELY LEFT FOR THE BUYER

💬 "There is a Triassic structure at approximately 700 metres below MOU-5... approximately 100km² in size... analogous to Hassi R'Mel."

Hassi R'Mel is Algeria's largest gas field. One of the largest in Africa.

Griffiths didn't drill it. He didn't even try. He left it — deliberately — as undiscovered upside for an acquirer to find after the deal closes.

Why? Because a certified TCF-scale Jurassic/Triassic resource would transform the valuation conversation. Leaving it undrilled keeps the entry price lower and gives the buyer a reason to pay a premium for control.

This is not exploration incompetence. This is deal strategy.

💎 THE HELIUM NOBODY IS TALKING ABOUT

Let's put the helium in context:

🔹 Global helium demand is in structural deficit

🔹 The US, Qatar and Algeria control ~85% of supply 🔹 Morocco has zero existing helium production

🔹 A Gulf NOC acquiring Guercif gets a strategic helium optionality layer that no Moroccan asset currently offers

Griffiths on MOU-2 helium (October 2025 presentation):

💬 "An incoming party... with huge resources... will be very attracted by that as an add-on."

He is explicitly marketing the helium to the acquirer in a recorded public presentation. This is not speculation. He said it out loud.

📅 THE CLOCK NOBODY IS WATCHING

5 November 2026.

That is the expiry date of PRD's First Extension Period on the Guercif Petroleum Agreement.

If no deal and no drill by that date, PRD must apply for a Second Extension. Under Moroccan petroleum law, extension applications require demonstrated work programme commitments.

This is not a soft deadline. It is a hard regulatory forcing event.

The divestment agent was appointed on a 6-month mandate in October 2025. Six months from October 2025 is April 2026. We are now past that initial mandate window.

The silence suggests the clock is ticking on announcements soon.

🌍 WHY A GULF NOC — AND WHY NOW

The fingerprints were on the wall from 2021:

✅ UAE Confidentiality and Disclosure Agreement — signed and disclosed in the 2021 Annual Report, before MOU-2 was drilled

✅ HOA terms — 100% full carry, wellhead gas purchase, past cost repayment — these are Gulf NOC deal mechanics, not European major deal mechanics ✅ Jersey structure — zero UK assets, designed for foreign acquisition, maximum tax efficiency for a Gulf sovereign entity

✅ ADNOC Gas — $13–15 billion international growth capex mandate 2024–2029, explicitly targeting gas value chain acquisitions

✅ Morocco context — the Nigeria-Morocco Gas Pipeline, Atlantic LNG infrastructure, EU energy security pivot — Morocco is becoming the most strategically important gas corridor in Africa

A Gulf NOC buying PRD doesn't just get 441 BCF. They get:

🟢A Morocco sovereign partner relationship (ONHYM SA post-dahir)

🟢Atlantic-facing LNG export optionality

🟢Hormuz diversification

🟢Helium strategic layer

🟢A Triassic exploration package with Hassi R'Mel analogue upside

🟢A Jersey shell with zero UK regulatory friction

🟢At £31 million market cap. Against a $692 million floor valuation on biogenic gas alone.

🔇 AND THEN THERE'S THE SILENCE

Since the May 2026 placing:

❌ No CEO interview

❌ No detailed operational update on Trinidad oil sales

❌ No SC-3 rig contract announcement

❌ No MOU-6 rig confirmation

❌ No voluntary Morocco update of any kind

Under UK Takeover Code Rule 2.2 — once a potential offeror approaches a listed board, the company enters a confidentiality obligation. Operational RNSs don't stop automatically. But voluntary disclosure does.

Five operational threads. All silent. Simultaneously.

Make of that what you will.

⚡ THE NEXT 8 WEEKS COULD DEFINE THIS COMPANY

🔵 SC-3 Trinidad spud — end June

🔵 ONHYM Royal Dahir — imminent, could drop any day

🔵 MOU-6 rig contract — third-party funded, announcement pending - spud end July

🔵 Divestment process — past the initial 6-month mandate window

🔵 Licence clock — 5 November 2026 forcing event approaching

This is not a story about what might happen someday. This is a story about what is happening right now — and a market that has absolutely no idea.

⚠️ Independent research only. Not investment advice. DYOR.

#PRD #Morocco #Trinidad #ONHYM #LSE #oilandgas #helium

@PredatorOilGas@Blowster85@AM231982@GrahamHengland@Share_Talk@OilVoice

"The battle for hearts and minds is actually going to be won by the Bitcoin network. As long as that continues as it has the last 17 years, we will get there."

Institutional investors share their perspectives - hosted by @Croesus_BTC at the Bitcoin Treasuries Unconference UK.

Featuring:

Alan Howard, Analyst, Tennyson Securities

Axel Cabrol, Managing Director, Tobam

Tyler Evans, UTXO Management, Metaplanet, The Smarter Web Company & Nakamoto

Alex Norris, Head of Investments, Silver 8 Capital

Hosted by Jesse Myers, Head of Bitcoin Strategy, The Smarter Web Company

@tylev

LSE: #SWC | OTCQB: $TSWCF | FRA: $3M8

#PRD

🧵 PREDATOR OIL & GAS #PRD — ONE OF THE MOST UNDERVALUED COMPANIES ON THE MAIN MARKET?

A forensic thread for anyone who hasn't done the work yet.

🎙️ THE CEO SAID WHAT?

Here are real quotes from Paul Griffiths — CEO & Executive Chairman — that almost nobody on the market seems to have processed:

💬 "We are in Jersey for a very good reason... it would have huge implications to our ability to attract foreign entities into a divestment process for Morocco." "We never have an asset in the UK and never will... the whole structure revolves around never having a presence in the UK."

The company was structurally engineered from day one for foreign acquisition. This isn't a pivot. It was always the plan.

💬 "Maybe next year... £1 a share." (That's a 2025 quote for realisation in 2026)

The current share price is ~3.5p. £1 would be a ~2,757% return from here. This is the CEO's own words. Not a broker note. Not a bulletin board post.

💬 "We will not fund MOU-6 ourselves... news sooner than expected."

A third party is paying for the next Morocco well. PRD doesn't drill it with its own cash. Someone else wants to own this acreage badly enough to carry all the cost.

💬 "Apparently we are giving up on Morocco. That rumour was spread on the morning of our AGM — could only have done so on the basis of trying to undermine our position."

A deliberate rumour. AGM morning. Shares dropped 25% on 8 million shares out of 681 million. Someone distributed stock into manufactured weakness. Draw your own conclusions.

💬 "We have appointed the same agent who structured the $7 billion Ireland transaction."

A $7 billion deal adviser. On a company with a £31 million market cap. This is not how you hire advisers if you're planning to stay small.

🔑 THE 16 DISCLOSURES NOBODY NOTICED

From the October 2025 investor presentation — spoken word, recorded, publicly available — but buried, unread, and certainly not in any RNS:

🟠 Hydrogen detected at MOU-3 — never disclosed in a single RNS filing

🟠 441 BCF total 2C certified resource — 20-25 MMcf/d per well deliverability (CEO's own estimate)

🟠 MOU-2 helium interval is 4-5x thicker than MOU-3, ~60km² closure

🟠 Triassic structure 100km² at 700m below MOU-5 — a Hassi R'Mel scale analogue — deliberately left for the acquirer to discover

🟠 Gas storage + salt caverns + Nador FSRU strategic layer — never discussed publicly

🟠 Jersey structure explicitly designed for foreign acquisition with no UK assets — ever

🟠 "Initial cash payment + royalty tied to production milestones" — deal architecture already publicly disclosed

🟠 UAE Confidentiality Agreement signed 2021 — before MOU-2 was even drilled

📐 THE VALUATION GAP IS OBSCENE

Sound Energy sold its Tendrara licence (Morocco, similar geology) to Moroccan state utility ONEE for $57M in 2022 — at $1.57/MCF on 36 BCF 2C.

Apply the same metric to PRD's 441 BCF 2C certified resource:

💰 Implied floor value: ~$692 million

💰 Current market cap: ~£31 million (~$39M)

That's an 18x gap on a like-for-like Moroccan gas asset comparison. Before you price in the helium, the Jurassic upside, the undrilled thermogenic system, or Trinidad.

⚡ RIGHT NOW — THE CATALYSTS ARE STACKING

🔵 SC-3 (Trinidad) — drill spud imminent, end-June/early-July window, 100% PRD-owned through T-Rex Resources, zero revenue share

🔵 MOU-6 (Morocco) — third-party funded, rig being secured, Exploitation Concession application precursor 🔵 ONHYM Bill 56.24 — both chambers of Moroccan parliament approved ✅. Royal Dahir awaited — could drop any day now. Once promulgated, ONHYM converts to société anonyme and the structural precondition for a Gulf NOC acquisition is legally in place

🔵 Divestment process live — agent appointed Oct 2025, CPR commissioned to support deal terms, 6-month mandate targeting Middle East / Asia / Africa NOCs

🔵 Post-placing silence — no CEO interview, no operational updates, no voluntary RNS since the May 2026 placing. Under UK Takeover Code Rule 2.2, a board in active offer discussions cannot disclose the approach. Draw your own conclusions.

🏗️ THE STRUCTURE TELLS THE STORY

✅ Jersey incorporation — maximum foreign acquisition flexibility

✅ UAE CDA signed 2021 — Gulf NOC relationship pre-dates the resource definition

✅ $7B deal adviser engaged

✅ CPR timed to "support divestment terms" not for internal planning

✅ AGM resolution to acquire assets "to achieve materiality for divestment"

✅ CEO openly states £1/share ambition

✅ Licence clock: First Extension Period expires 5 November 2026 — time pressure is real

This is not a small company hoping for the best. This is a structured exit vehicle being walked toward a transaction.

⚠️ Independent research only. Not investment advice. DYOR.

#PRD @PredatorOilandGas #Morocco #Trinidad #Ireland #smallcaps #oilandgas

@Blowster85@AM231982@Share_Talk@OilVoice@GrahamHengland

Removing Capital Gains Tax from Bitcoin is the single most important thing we can do for Bitcoin adoption.

It will allow Bitcoin to be used as money and incentivise people to save in Bitcoin over assets such as Real Estate.

I will keep repeating this.

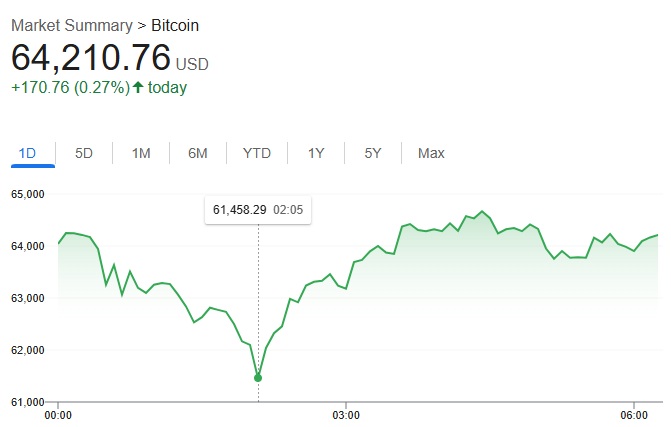

A bit of a flush in Bitcoin overnight, but importantly (for those looking shorter term) it held above the early-February lows. If today's candle can finish green, it could create a very compelling setup and get the technical traders extremely excited.

More importantly, none of this changes the long-term trajectory. The day-to-day volatility is just noise when viewed against the bigger picture. Across the world, institutions, companies, governments, and investors continue to move toward a Bitcoin standard and rebuild financial infrastructure around it.

We stay focused on the mission, ignore the short-term distractions, and keep building. The long-term direction of travel remains the same.

My presentation from the Bitcoin Treasuries Unconference UK last week.

How big is the UK asset landscape?

What's the TAM for a Bitcoin treasury company like @smarterwebuk ?