"Isn't $LMND just another insurtech?"

This chart can lay that argument to rest.

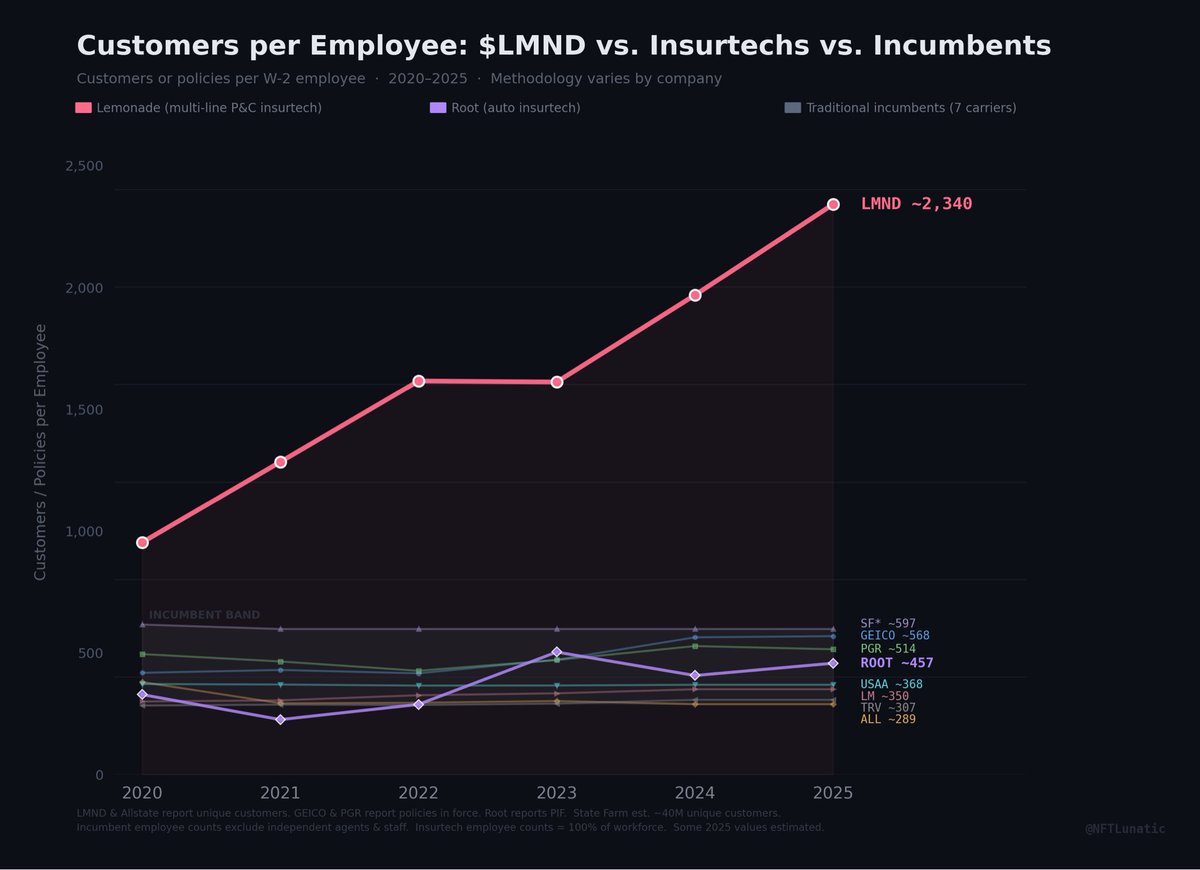

Customers per employee, 2020–2025:

$LMND vs. $ROOT vs. 7 major incumbents.

$ROOT is the perfect test case. Same era. Same "insurtech" label. Same direct-to-consumer P&C model. Public company with clean data.

$ROOT at 457 customers per employee.

GEICO at 568.

Progressive at 514.

Root IS the incumbent band.

Why? $ROOT innovation was telematics — better pricing through driving data. That helped them reach profitability. But it didn't change how many humans they need to operate.

Root hired 341 people last year to add 73K policies. $LMND hired 47 to add 570K.

That's not a difference of degree. It's a difference of kind.

$LMND didn't just digitize the front end. AI Maya underwrites. AI Jim handles claims. The marginal customer costs almost nothing to serve.

$ROOT used tech to price better. $LMND used AI to run the company.

That's why one curve compounds and the other flatlines.

This also kills the bear argument that competitors will "just copy $LMND playbook."

$ROOT has been trying for 9 years. Backed by $1.2B+ in funding. Public since 2020. Building technology from scratch with no legacy constraints.

And they still ended up in the incumbent band.

If a well-funded, tech-native insurtech with zero legacy baggage can't replicate this efficiency curve, what makes anyone think State Farm or Allstate will?

$LMND AI-first architecture isn't a feature. It's a compound advantage that gets harder to replicate every quarter — because every new customer, claim, and interaction feeds the models that make the next one cheaper to serve.

The moat isn’t JUST the AI operating system running the company. It’s 3 million customers (and growing) training the AI.

$IOT vs $PLTR

Could Samsara be Palantir 2.0?

$PLTR deserves every bit of its reputation. 70% revenue growth. 51% FCF margins. Rule of 40 of 127. AIP bootcamps converting prospects in days instead of months. This is generational execution.

But here's the structural risk nobody talks about:

$PLTR analyzes data it doesn't own. $IOT generates 25+ trillion proprietary data points per year from hardware physically bolted to customer assets — 90B+ miles of driving data, 180B+ minutes of video.

Analytics layers face commoditization. Anthropic, Snowflake, AWS, Databricks, etc. are all building AI orchestration platforms. Every improvement in LLMs makes the analytics layer more competitive.

Nobody is commoditizing the physical data collection layer. Deploying millions of IoT devices across the real world takes years, capital, and trust. That data compounds and feeds AI models no competitor can replicate.

$IOT is moving UP the stack: AI agents, autonomous safety coaching (73% crash reduction), predictive maintenance.

$PLTR is NOT moving DOWN into hardware.

The company that owns the data source wins. Google with search. Bloomberg with terminals. Tesla with driving miles. $IOT with physical operations.

$PLTR's moat is institutional trust and switching costs. That's powerful.

$IOT's moat is owning something no one else can access. That's structural.

$IOT: approximately 12x EV/Rev, 30% growth, 77% gross margins, GAAP profitable.

$PLTR: approximately 67x EV/Rev.

The market prices $IOT like a fleet tracker. It's becoming the operating system for physical work sitting at an 80% discount to the analytics layer above it while moving deeper into the analytics layer as well.

May closed with a bang. 🔥

Burns dipped mid-month, then snapped back hard - near $170K in the final week alone as $GEOD continues to grow momentum. 20,000+ miners. 80% of revenue burned. Every week.

Why does it matter? The burn isn't speculation. It's real infrastructure, where each miner is doing real work to expand the foundation for drones, robots, and an autonomous future.

Want in? Follow us.

Ironically $GEOD may be one of the most fairly/ undervalued robotics/ drones investment out there.

$60–70M market cap.

Revenue run-rate/ARR has gone from roughly $2–3M a year ago to about $10M annualized today — roughly 3–5x growth, depending on the starting point used.

So you’re paying around 6–7x current ARR for the largest decentralized RTK network in the world, selling centimeter-level positioning data into drones, robotics, autonomy, agriculture, and mapping.

I am in the camp that biotech must be a massive beneficiary of AI.

What other industry could humans value more?

$TWST is the pics and shovels play for biotech.

They are leaders in manufacturing synthetic biology at scale.

This $LMND Community is being shut down by X on May 30th. As far as I understand, I believe all of our tweets in here will be deleted. It's very sad, but we have no say in this matter.

Two solutions I'm proposing:

Join my Patreon Discord for free. I'm changing my Discord so it's free to join. There are 203 members there currently and the discussion has gradually increased as the members have grown. The link to join is here. If the discord grows too large or is full of spammers, then I may need to rethink it's requirements and go back to paid members only and/or have more moderators, etc. But it's a good place to continue this direct back and forth discussion with other investors who look in depth into their investments.

https://t.co/8QE27OLQME

Continue posting on X. Without a community stream, it may be harder to curate all $LMND related posts the same way we can now. That said, I think if we continue to use the ticker symbol $LMND in posts and possibly other hash tags (maybe #Lemonapes, or #LMNDcommunity) then we could curate things around those. If you have an idea for a clean and simple hashtag, please comment it below. What I like about X is it's a completely open discourse full of bulls and bears. Where else can you debate with hedge fund managers, world leaders and CEO's? There's nothing quite like it. So if we continue to post here, the algorithm will connect most of us. If you want my attention, feel free to tag me or others more frequently on posts and we can respond.

It's very sad to see this community go, but I think the same spirit of it will live on in various forms.

$LMND

“We surpassed $1 million of IFP per employee, representing a nearly 3x improvement over the past four years.”

— Daniel Schreiber

This is what a company successfully leveraging AI looks like.

A customer told $PATH CEO Daniel Dines this on stage, and he repeated it twice on the Q1 call:

"Models are easy. Orchestration is not."

The whole bull case in 4 words.

✅ First-ever GAAP profitable quarter

✅ NRR inflected UP to 109% (+2pts QoQ)

✅ 16 of top 20 deals included AI

✅ AI expansion deals 6x larger than non-AI

$HIMS labs will be obvious in hindsite.

When you become a customer you feel the impact of the product instantly.

AI will unlock even more value from this life changing product.

$DUOL and $LMND bounce back is just beginning.

$DUOL already dominates its industry of consumer education apps.

$LMND will ultimately dominate its industry as its competitors are dinosaurs.

$NAUT is one of the stranger small-cap biotech / life-science tools setups I’ve seen.

Pre-revenue. Still high risk. Commercialization not proven.

But insiders own 40%+ of the company, the co-founders each own massive stakes, and the CEO has even been buying shares.

That level of economic alignment is rare in a tiny public science platform company.

It doesn’t prove Voyager will commercialize successfully.

But it does suggest the people closest to the platform still believe the upside is worth staying heavily exposed to.

At a $200M EV, that makes $NAUT a very interesting bet.

Not safe. But unusually aligned.

Kraken Robotics Reports Q1 2026 Financial Results with 35% Year-Over-Year Revenue Growth and Reiterates 2026 Guidance.

For the full announcement, read our news release: https://t.co/U7e3E68L6y

I like how the $XMR / $BTC chart looks.

$XMR is the gold standard for privacy which I believe will become increasingly more valuable as AI advances and governments increase surveillance.