honestly been sitting on this for a while before posting but here it goes

the robotics space is at an inflection point that most people are completely missing. everyone's talking about AI, everyone's talking about SpaceX, and yeah those are real - but both are essentially priced in at this point. you're not getting in early on anthropic. that ship sailed.

what's NOT priced in is humanoid robotics. figure and apptronik are the two serious US players and their combined valuation was sitting below cardano six months ago. cardano. a chain that has been a ghost town since 2020. let that sink in for a second.

now i'm not here to tell anyone what to buy but $BOT (robostrategy) has been on my radar for a while and the thesis is actually pretty clean. it's essentially a vehicle that gives you pre-IPO exposure to these companies with actual liquidity - no 7 year lockup, no being stuck at a 60% discount if you need to exit. that alone separates it from most VC-adjacent plays retail ever gets access to.

the NAV premium people complain about is based on last year's funding rounds. figure and apptronik are raising again, probably sooner than most expect, and those rounds are not coming in lower. when that happens the math on $BOT flips pretty fast.

robotics hasn't had its ChatGPT moment yet. that's the whole point. when it does, and it will, the window you had to position beforehand is gone. every major bull run has that one sector where people look back and say "it was so obvious." i think this is it for the next cycle.

not financial advice, do your own research, all that. just think more people should be paying attention

$SPCX shares are priced at $135 for its $2 trillion IPO.

Its return is 100x-200x by 2035.

These 20 companies will benefit the most:

1. $BKSY ~$34

AI-ready Earth observation satellites feed SpaceX orbital intelligence layer.

2. $SPIR ~$20

Space data analytics monetizing SpaceX's growing orbital constellation.

3. $ACHR ~$5

Air mobility networks integrate with Starlink's low-latency infrastructure.

5. $SATL ~$7

High-resolution imaging complements SpaceX orbital AI compute constellation data.

6. $VIAV ~$50

Optical networking components critical for Starlink ground station upgrades.

7. $OUST ~$40

Sensor fusion tech supports SpaceX booster catch reusability automation.

8. $GILT ~$15

Satellite ground infrastructure scales alongside Starlink enterprise deployments.

9. $POET ~$11

Optical interposer chips slash data center power costs inside COLOSSUS AI cluster.

10. $ARQQ ~$12

Quantum encryption securing Starshield government classified orbital networks.

11. $TWST ~$74

Synthetic biology tools accelerate SpaceX long-term Mars life support research.

12. $LUNR ~$30

NASA lunar lander tech directly supports SpaceX Moon base buildout.

13. $AEVA ~$24

LiDAR sensors enable autonomous Starship landing and booster catch precision.

14. $KTOS ~$60

Defense tech partner powering Starshield national security satellite contracts.

15. $IONQ ~$58

Quantum compute layer powering next-gen orbital AI satellites.

16. $RDDT ~$178

Real-time social data feeds Grok's truth-seeking AI via X integration.

17. $RKLB ~$115

Small payload launch fills exact gaps Falcon can't efficiently serve.

18. $ASTS ~$97

Direct-to-phone satellite broadband. Starlink's closest competitor and partner.

19. $MTSI ~$375

RF semiconductors power Starlink phased-array antenna signal processing.

20. $BWXT ~$200

Nuclear propulsion R&D aligns with SpaceX Mars mission power requirements.

I'm definetly a buyer of $SPCX IPO and want to get it super cheap.

♻️ RESHARE this post and write 1 comment, I'll DM you the PRICE I want to buy $SPCX at this month.

I’ve wanted to tell this story for years. Never had the courage. Here it is.

I turned a presale allocation into $80 million on $OHM. Today I have $500k left.

In 2021, I got a presale allocation in OlympusDAO, then aped heavily myself on top of it. The allocation got me in the door. My own conviction made me go all in. Staked everything. Watched it compound daily. By the peak I was sitting on $80 million.

Then I started spending like the money printed itself.

Private jets to Dubai because commercial felt beneath me. $40k weekends in Monaco. A garage full of cars I drove twice. Watches I never wore. I tipped $5k at dinners just to feel something. Every purchase was a flex for an audience that didn’t care.

The casino was worse. High limit rooms in Vegas and Macau. I’d lose $2 million in a night and laugh it off because the portfolio would make it back by morning. Until it didn’t.

When $OHM unwound, I didn’t sell. I doubled down. Then I leveraged. 5x, then 10x, trying to trade my way back to the peak. Every liquidation felt like a personal insult, so I’d open a bigger position. I wasn’t trading anymore. I was gambling with a different interface.

$80 million became $20 million. $20 million became $4 million. I told myself $4 million was still life changing money. Then I levered that too.

$500k. That’s what’s left.

Here’s what I learned the expensive way:

Unrealized gains are not money. I never had $80 million. I had a number on a screen and the arrogance to believe it was permanent.

Getting in early is a gift. I treated it like a skill. The allocation didn’t make me a genius. It made me lucky. I confused the two for three years.

Lifestyle inflation is a leak you don’t notice until the ship is underwater. The jets and cars didn’t kill me. The identity did. I became someone who needed to spend to feel like a winner.

Leverage doesn’t get you back to even. It gets you to zero faster. Revenge trading is just grief with a chart open.

Nobody at the table in Monaco remembers my name.

I’ve carried this story alone for years. Too embarrassed to say it out loud. But $500k is more than most people will ever hold at once, and I’m done pretending the past didn’t happen. The next decade is about building slow and keeping what I make.

If you’re up big right now, screenshot this. You’ll need it.

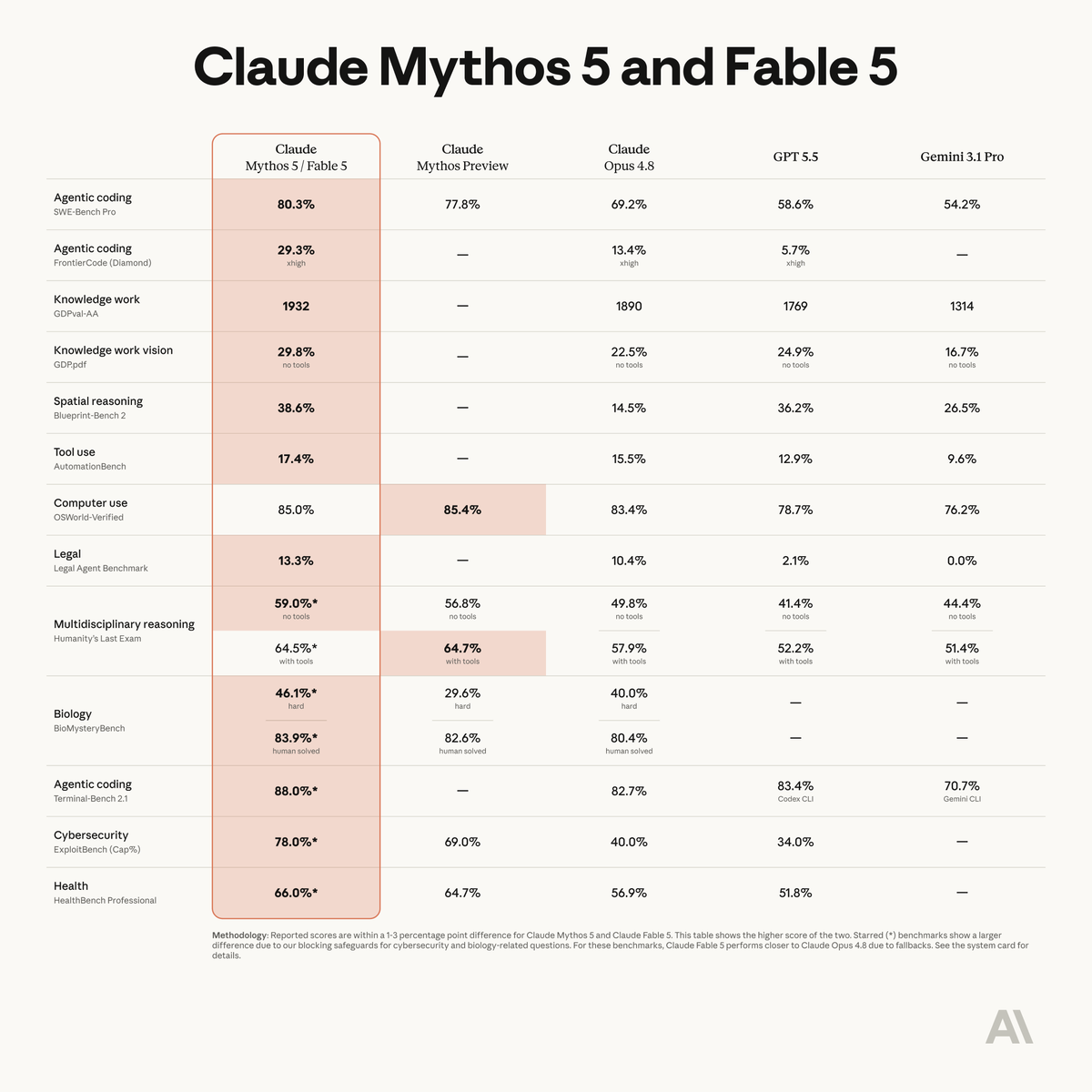

Fable 5 is state-of-the-art on nearly all tested benchmarks, with exceptional performance in software engineering, knowledge work, scientific research, and vision.

The longer and more complex the task, the larger Fable 5’s lead over our other models.

a few words on the HBM/DRAM story, memory makers, how far current inference optimizations can go, who’s positioned well, and what changes once new capacity starts coming online in 2027

BREAKING: Claude can now run Stock Market research like a top consulting firm (for free).

Here are 10 Claude prompts that replace $100K/year stock analysts (Save for later)

Howard Marks has been writing investment memos for 30 years that Warren Buffett says he reads first thing every time.

In 36 minutes he explains why every bull market ends the same way - and where he thinks we are right now.

36-min. Oaktree. TBPN.

Bookmark & watch - the clearest market cycle read you'll find in 2026

Businesses moved billions of stablecoins through onchain payment rails for the speed, settlement, and programmability they needed.

Tokenized assets are going to want the same thing.

Sounds pretty Mantle.

Goldman Sachs just dropped the most precise map of where $7.6 trillion is going over the next five years and it tells you exactly which companies are standing in the middle of an unavoidable flood of capital (Save this).

The numbers are worth understanding precisely before talking about who benefits.

Goldman's baseline projects $765 billion in AI capital expenditure in 2026 alone, growing to $1.6 trillion annually by 2031.

Over the full 2026 to 2031 period, cumulative spend breaks down to $5.1 trillion in compute, $2.1 trillion in data centers, and $358 billion in power.

Nvidia is assumed to command 75% of all compute spend throughout the period, using the Rubin VR200 chip at $80,500 per GPU as the baseline.

The data center specification charts reveal how dramatically physical requirements are escalating.

A standard cloud data center runs 5–15 kW per rack while a transitional Blackwell era AI data center runs 130–200 kW per rack.

The AI factory of the future, running Rubin and Feynman silicon operates at 500+ kW per rack, at greater than 1 gigawatt scale, with liquid cooling only.

Traditional hyperscale data centers cost roughly $10 million per megawatt to build while the next generation AI data centers are being discussed at $15 to $20 million per megawatt.

Goldman identifies silicon useful life as the single biggest swing factor in the entire model.

At a 3-year replacement cycle, cumulative compute depreciation hits $3.99 trillion and at 7 years, it drops to $2.23 trillion, a $1.76 trillion difference on one assumption alone.

Power is only $358 billion of the total, but Goldman is explicit, it is the only component that can prevent the other 95% of the stack from deploying.

Amazon's Andy Jassy put it, "Our single biggest constraint is power." Connecting large data centers to the grid takes years.

Now here are the companies standing directly in the path of each layer of this capital.

Nvidia is still the most concentrated bet on the compute layer.

At 75% of $5.1 trillion in compute spend over six years, that is $3.8 trillion in cumulative revenue flowing through one company's products.

The 75% gross margin on data center GPUs is the reason every hyperscaler is trying to build custom silicon to escape it while simultaneously continuing to buy Nvidia because nothing else performs at the same level.

Vertiv is the direct infrastructure play on the data center upgrade cycle.

Every rack going from 40 kW to 500+ kW needs liquid cooling systems, power distribution, and thermal management infrastructure that simply did not exist at prior density levels.

Vertiv just deepened its liquid cooling capabilities through a strategic acquisition and was named a key partner on Hut 8's large AI-focused Texas data center campus.

The liquid cooling market is growing from $5.5 billion today to $15.75 billion by 2030, and Vertiv is the dominant provider in that market.

Vistra is the power thesis in its most direct form.

The $358 billion power segment is the critical path for the entire $7.6 trillion, and Vistra has spent the last 18 months locking up that critical path through long-term nuclear power purchase agreements.

Vistra secured a 20 year agreement with Meta for over 2,600 MW of nuclear energy, plus a separate deal with AWS from its Comanche nuclear facility.

Goldman Sachs and Jefferies both upgraded the stock after the Meta deal was announced.

The architecture of this trade is simple.

Goldman's model is not a prediction of whether AI spending happens but rather a model of the minimum physical capital required to deploy infrastructure that has already been contracted, already been announced, and is already under construction.

The compute layer requires the chips, data center layer requires cooling and power infrastructure and the power layer requires nuclear at scale on multi-decade contracts.

All three layers are being funded simultaneously, and all three have identifiable public companies sitting directly in the path of the capital.

Come join Milk Road Pro and get our full $7.6 trillion infrastructure breakdown which names across compute, data centers, and power we're currently positioned in and our full thesis on the AI trade.

Link below!

In investing, a lot of information you can acquire via the internet and Claude tokenmaxxing.

But there is an entirely different world which you can only tap into through conferences and in-person conversations.

This post is the result of spending a full week in Taipei staring at racks and talking to people! We cover

1. Immersion Cooling

2. Fuel Cells

3. Hiwin (Robotics Supplier)

4. DRAM

5. Kyber Racks

6. Astera Labs

7. Nvidia RTX Spark (Laptops)

8. MediaTek MicroLED

9. Scale-Out CPO

10. Scale-Up CPO

And some implications for CPO players like $LITE.

Japan invented nearly every tool central banks now reach for.

Zero rates → 1999

QE → 2001

Yield curve control → 2016

Its debt is now ~240% of GDP. Double the US.

Japan's reckoning is unfolding right now — and America is walking the same path, a decade behind. Here's my take 👇

Quite a week for open-source AI. Especially American open-source. Nemotron 3 Ultra is the most important release in quite some time. And some really cool RL and fine-tuning work from Harvey.

Everyone says Singapore property is a great investment.

But did it actually beat the stock market over 30 years?

I ran the numbers across condo, landed, HDB 4-room and 5-room — vs the S&P 500.

The answer will surprise you. [1/8]

👉For 4 years, 1 day, and 10 hours, anyone who understood the Orchard circuit could have minted ZEC out of thin air, silently, with no on-chain signature. The bug was disclosed this week. It was found by an AI-driven audit running Opus 4.8, not by an attacker.

1. Call the bug what it is

Two lines in halo2's variable-base scalar multiplication gadget used assign_advice() where copy_advice() was required. As a result, the diversified-address integrity check pk_d = [ivk]·g_d could be satisfied for arbitrary inputs. A malicious prover could spend the same note multiple times with different nullifiers, i.e. counterfeit ZEC inside the Orchard pool, undetectable on-chain because the privacy of the ZK proof hides exactly the inputs that would reveal the attack.

We do not know whether it was exploited. We will probably never know.

2. Four years. Multiple audits. Top-tier reviewers.

Orchard was reviewed by some of the strongest cryptographers in the field before activation. They missed it. Earlier automated audits with Opus 4.7 missed it. Opus 4.8 catches it in roughly 1 in 4 runs when prompted generically. The bug is hard.

And ZK inflation bugs are not new. Zcash itself shipped a counterfeiting vulnerability in Sprout (BCTV14) that survived years before being silently neutralized during Sapling. Similar soundness issues have appeared in circom, halo2, and rollup verifiers since. The pattern is consistent: when the protocol is private, exploitation is undetectable. You patch the bug and hope.

3. What Zcash did right

This was a textbook decentralized incident response:

▶️Audit: a full AI-assisted soundness audit of halo2 + Orchard, scoped end-to-end.

▶️Discover: the agent flagged the missing constraint and worked out the algebra to turn it into an exploit. A working RPC-level PoC in ~6 hours, mostly waiting on tokens.

▶️Coordinate: a soft fork disabling Orchard, prepared and distributed without leaking the bug, activated 2 days and 15 hours after acknowledgement. Coordinating a soft fork across miners, exchanges, and nodes without disclosing why is genuinely hard. They did it.

▶️Disclose: timeline, code lines, math, open questions. No spin.

Worth naming explicitly: Zcash's turnstile invariant caps the value that can ever leave a shielded pool by the value that entered it. Privacy and verifiability inside the same protocol. That is not an accident. That is good engineering, and it is what kept the worst case bounded.

4. The economics of security just changed

AI does not change whether bugs like this exist. It changes the cost of finding them. I wrote about this https://t.co/AeurraJXhB: a missing constraint in a 4-year-old production ZK circuit used to require a top-tier cryptographer with months of context. It now requires a few tokens, an API key, and a well-framed prompt.

The defender benefits. The attacker benefits more, they only need to find it once, and they never disclose.

Orchard is the optimistic version of this story: defense got there first. The pessimistic version is the one we cannot rule out, because the chain is private by design.

5. The only real exit

You do not patch your way out of this asymmetry. You raise the floor.

Formal verification of consensus-critical circuits, every assign_advice audited by SAT solvers and AI for under-constraint, as the reporter himself recommends. Proof-grade engineering that used to be too expensive is now cheap enough to be mandatory.

Hardware roots of trust, secure enclaves, certified secure elements, WYSIWYS. Cryptographic guarantees the user can actually verify, not promises a host can lie about.

Continuous AI-assisted audit of every consensus-critical commit, re-run immediately on the release of any new frontier model.

Zcash didn't just patch a bug. They demonstrated the new defensive playbook: AI-driven audits, decentralized coordination, radical transparency, verifiable invariants. That is the direction the rest of the industry needs to follow.

And those who don't raise the bar for security will be rekt in this new world.

Stay safe. Stay honest about your trust assumptions.

in feb I called $VVV at ~$2-3, today it is at $21 (+740%) and a month ago I called $NEAR at ~$1.30, today it's at ~$3 (+133%)

congrats to everyone who read my articles, understood the narrative & vision + positioned accordingly

and it really is that simple -- even in a bear market -- find good companies, w/ strong tech + team + tokenomics and have conviction + patience

there is opportunity everywhere -- read the article i recently wrote on the current state of crypto if you want to understand where all of this is going

Goldman Sachs on memory:

- DRAM to remain in undersupply until atleast 2028 (undersupply of 5.0%, 5.9% and 3.9% in the years 2026, 2027 and 2028 respectively).

- DRAM global demand revised upwards, now expected to grow by 28%, 20% and 19% y/y in 2026, 2027 and 2028 respectively.

- NAND to also remain in undersupply until atleast 2028 (undersupply of 4.4%, 4.6% and 3.0% in 2026, 2027 and 2028 respectively).

- NAND global demand revised upwards, now expected to grow by 20%, 23% and 19% y/y in 2026, 2027 and 2028 respectively.

- HBM to remain in undersupply until atleast 2028 (undersupply of 5.4%, 6.0% and 4.3% in 2026, 2027 and 2028 respectively).

- HBM TAM expected to be $56 billion, $116 billion and $168 billion in 2026, 2027 and 2028 respectively.

Slowly, the overall consensus is shifting towards memory remaining in shortage until atleast 2028, while it was 2027 previously.

$MU $SNDK $DRAM $EWY

![Chicky_Think's tweet photo. Everyone says Singapore property is a great investment.

But did it actually beat the stock market over 30 years?

I ran the numbers across condo, landed, HDB 4-room and 5-room — vs the S&P 500.

The answer will surprise you. [1/8] https://t.co/y6mV94YP67](https://pbs.twimg.com/media/HKMGNvCagAATK_P.png)

![P3b7_'s tweet photo. 👉For 4 years, 1 day, and 10 hours, anyone who understood the Orchard circuit could have minted ZEC out of thin air, silently, with no on-chain signature. The bug was disclosed this week. It was found by an AI-driven audit running Opus 4.8, not by an attacker.

1. Call the bug what it is

Two lines in halo2's variable-base scalar multiplication gadget used assign_advice() where copy_advice() was required. As a result, the diversified-address integrity check pk_d = [ivk]·g_d could be satisfied for arbitrary inputs. A malicious prover could spend the same note multiple times with different nullifiers, i.e. counterfeit ZEC inside the Orchard pool, undetectable on-chain because the privacy of the ZK proof hides exactly the inputs that would reveal the attack.

We do not know whether it was exploited. We will probably never know.

2. Four years. Multiple audits. Top-tier reviewers.

Orchard was reviewed by some of the strongest cryptographers in the field before activation. They missed it. Earlier automated audits with Opus 4.7 missed it. Opus 4.8 catches it in roughly 1 in 4 runs when prompted generically. The bug is hard.

And ZK inflation bugs are not new. Zcash itself shipped a counterfeiting vulnerability in Sprout (BCTV14) that survived years before being silently neutralized during Sapling. Similar soundness issues have appeared in circom, halo2, and rollup verifiers since. The pattern is consistent: when the protocol is private, exploitation is undetectable. You patch the bug and hope.

3. What Zcash did right

This was a textbook decentralized incident response:

▶️Audit: a full AI-assisted soundness audit of halo2 + Orchard, scoped end-to-end.

▶️Discover: the agent flagged the missing constraint and worked out the algebra to turn it into an exploit. A working RPC-level PoC in ~6 hours, mostly waiting on tokens.

▶️Coordinate: a soft fork disabling Orchard, prepared and distributed without leaking the bug, activated 2 days and 15 hours after acknowledgement. Coordinating a soft fork across miners, exchanges, and nodes without disclosing why is genuinely hard. They did it.

▶️Disclose: timeline, code lines, math, open questions. No spin.

Worth naming explicitly: Zcash's turnstile invariant caps the value that can ever leave a shielded pool by the value that entered it. Privacy and verifiability inside the same protocol. That is not an accident. That is good engineering, and it is what kept the worst case bounded.

4. The economics of security just changed

AI does not change whether bugs like this exist. It changes the cost of finding them. I wrote about this https://t.co/AeurraJXhB: a missing constraint in a 4-year-old production ZK circuit used to require a top-tier cryptographer with months of context. It now requires a few tokens, an API key, and a well-framed prompt.

The defender benefits. The attacker benefits more, they only need to find it once, and they never disclose.

Orchard is the optimistic version of this story: defense got there first. The pessimistic version is the one we cannot rule out, because the chain is private by design.

5. The only real exit

You do not patch your way out of this asymmetry. You raise the floor.

Formal verification of consensus-critical circuits, every assign_advice audited by SAT solvers and AI for under-constraint, as the reporter himself recommends. Proof-grade engineering that used to be too expensive is now cheap enough to be mandatory.

Hardware roots of trust, secure enclaves, certified secure elements, WYSIWYS. Cryptographic guarantees the user can actually verify, not promises a host can lie about.

Continuous AI-assisted audit of every consensus-critical commit, re-run immediately on the release of any new frontier model.

Zcash didn't just patch a bug. They demonstrated the new defensive playbook: AI-driven audits, decentralized coordination, radical transparency, verifiable invariants. That is the direction the rest of the industry needs to follow.

And those who don't raise the bar for security will be rekt in this new world.

Stay safe. Stay honest about your trust assumptions.](https://pbs.twimg.com/media/HKCPArbWMAAT2O-.png)