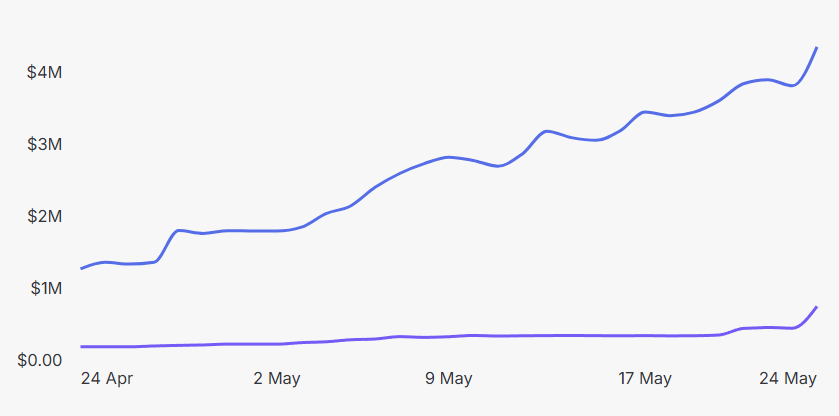

May was the month Flying Tulip’s margin-based Lend expanded across Sonic and Ethereum.

Without token incentives or points, Lend TVL grew from $1.76M on April 30 to $6.44M on May 25.

▸ Lend lets users supply assets and earn yield, gives borrowers access to liquidity, enables delta-neutral strategies for ftUSD, and establishes the infrastructure for Spot, Leverage Trading, and TRS.

▸ Lend yield comes from two sources: borrower interest on used capital, and strategy yield on idle, not-borrowed capital.

▸ Spot will also be integrated with Lend. Limit orders are signed intents with a minimum price and expiry; while waiting to be filled, assets can remain deposited in Lend and continue earning yield in bought-back and distributed ethereum:0x5dd1a7a369e8273371d2dbf9d83356057088082c.

Still personally most exited about Total Return Swaps coming out, but so incredibly happy and proud of the team for shipping all this in under 60 days.

The PUT system is working even in these stressed environments, exactly what it was built for, great to see it align long term supporters and provide easy exit for short term flippers without impacting the secondary.

Secondary NAV system managed to absorb all exits as well, making sure there isn't a dragging tail, already bought and burned $1.22m worth of tokens.

PUT marketplace trading has generated over $1m in trade volume with over 200 active sales, all without impacting the secondary market while trading PUTs at premium.

Flying Tulip USD I believe is the only pure activity based stablecoin yield system, and even in these markets has outperformed base lending and even "managed vaults", and that's with only 14.5% allocation to the delta neutral staking yield positions.

Our Lending is the first onchain margin based (not LTV) system, and has already shown higher capital efficiency (we needed to build it to facilitate onchain delta neutral staking trade [not possible elsewhere]).

All this in 71 days, for only $475.77k spent to date. Still an exciting road ahead with spot, leverage, TRS, perps, options, binary options, and insurance, but already massive milestones accomplished.

ftUSD limits increased.

Ethereum & Sonic caps increased from 1,000,000 to 5,000,000.

Earn 8.38% on USDT & USDC depositing into ftUSD;

Earn: https://t.co/V3rNljYt03

Stats: https://t.co/ogvxnlVhBK

Disrupting Tokenomics (Combination of 4 Unique Mechanisms)

Most DeFi

projects use well-known tokenomic models, however, @flyingtulip_ system combines 4 unique mechanisms that do not exist anywhere else.

Fixed supply without inflation 1:1 to real deposits

No upfront distributions for the team

Continuous buyback with revenue

and an on-chain reserve to guarantee the redemption of the original asset.

These four pillars are mutually exclusive in traditional models AC combines them to create a completely new class of tokenomics.

This is the only tokenomic that makes losing impossible.

@flyingtulip_ #FlyingTulip #Tokenomics #DeFi

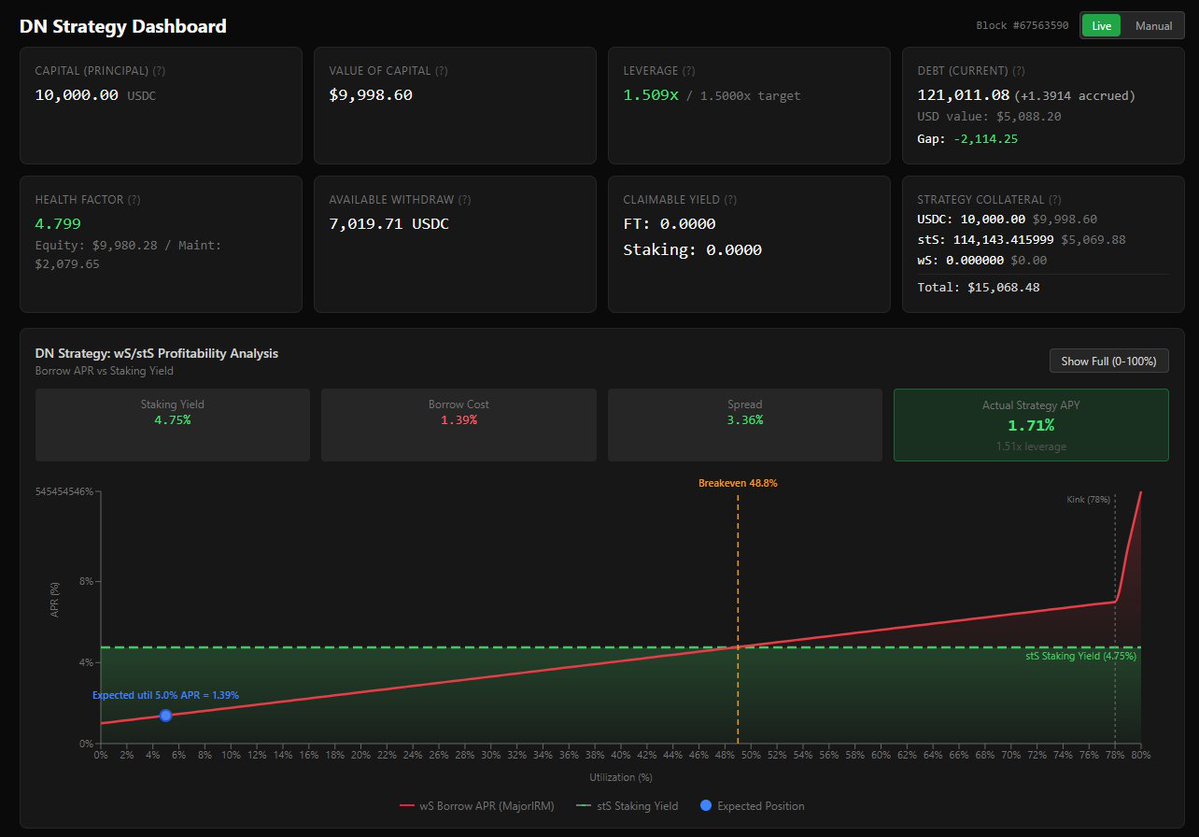

So many new building blocks required to get here onchain. You can do this strategy with active management (in a limited fashion onchain), but no passive options, so we had to first rebuild an issuance / settlement layer (ftUSD), that can then feed into a margin based lending system (LTV based doesn't work here), with onchain RFQ for fillers, all just to enable a passive way to scale this trade. Bit more hardening and we can scale up leverage and caps. At scale this does ~8%-12% on USDC/USDT.

$ftUSD's Delta Neutral Staking Yield strategy has been enabled on Sonic, currently earning 5.39% APY on USDC deposits. Capped at $10,000. Once infra is hardened will scale up to full deposits.

This year, @flyingtulip_ introduced a revolutionary DeFi model in which investors provide the yield that funds the system, while retaining the option to exit their full position without loss, without creating sell pressure, and without negatively impacting the remaining holders.

- Revenue up, even when PUT backing down.

- ftUSD growing steadily with 7.54% APY without additional token incentives being active yet.

- Almost $1m bought back and burned

- Good operational buffer.

- $50m safely exited that would otherwise have sold on secondary.

- Onchain liquidity steadily growing, already ~$400k in protocol generated passive orders.

Understanding @flyingtulip_ new raise model;

TLDR;

Market Cap: $2k

FDV: $175m

Volume: $33.5m

2 weeks in (and brutal markets) and yet the token looks boring (by design). Volume is tiny (by design).

Comparative projects that raised and TGE'd in the same time-frame are on average significantly down, and the reasoning is simple, bad markets cause people to exit/liquidate what they can, repay loans, and often move to cash in hand vs risk on strategies. If during these markets your only choice is "sell the token" that's the rational actor step. This new model on the other hand gives the holder choices; refund original investment (no loss), sell the Option instrument on the secondary market, withdraw the token and sell the token.

So you can either always exit at investment $0.10, or sell Option (which trade at 4-6% premium on the Options marketplace), or sell in the secondary market (at $0.09844c as per below). The rational action is to try to sell the Option, and if you need liquidity sooner to simply refund. We can see this in the numbers. On the secondary market total volume has been what we have bought back (7.9m tokens [~$790k] almost exclusively), the only real sells here have either been users who were in profit from ETH price decrease, or users who were trying to influence outcomes in Polymarket. Now the next point to understand is "but why is secondary price $0.9844 instead of $0.10", the Options give the $0.10 refund, the secondary market has 2 primary influences, 1. NAV buyback (which creates a floor [limit order] at NAV price of collateral backing withdrawn tokens, NOT full system NAV. Full system NAV would be ~$0.101c, withdrawn collateral backing puts are ~$0.098c. So when a user withdraws FT, their Option refund turns into a buy limit order at NAV price), and 2. yield/revenue/fees buys which are market buys at SPOT. This function is also why the spread is quite high since #2 keeps filling limit sell orders, and #1 keeps eating market sells.

Now if we look at the 2nd image, it shows a current investment value of ~$175m and at peak ~$207m. That's $32m in "volume" that would have otherwise sold on the secondary market, easy to see what would have happened to the token price. However now instead, they can simply exit not impacting ongoing holders (in fact to ongoing holders benefit, given now there is less circ supply). Lastly if we look at the Options market, then we have another additional ~$500k in sales at premium.

So that explains volume, but then let's have a quick look at marketcap and FDV and why both are wrong. FT has no minting ability, so it has a fixed totalsupply of 10bn that can only burn. However, the only way tokens can actually be part of this calculation is via Option sales (which were available during the public sale), so that means only 1.758bn is actually supply and the FDV would be $175m, but then what is circulating supply? Circulating supply is "liquid FT", aka, FT withdrawn from the Option (forfeiting the refund), so current tradable FT is 4.8m or $480k market cap, but now again, this is technically not accurate, because for every outstanding FT there is a NAV bid offsetting it. So in really marketcap is; circulating tokens (4.8m) * price ($0.09844) - exited_nav_price ($0.098c) = $2,134.18 ($2k mcap).

Holders who continue to wish to support the project are rewarded for longer participation with decreasing mcap and fdv, over and beyond price protection.

This is very cool.

Flying Tulip Lend is almost here

More than a lending market, it adds a core collateral and risk layer to the @flyingtulip_ stack.

Key innovations:

🔹Productive collateral

🔹Market-aware borrowing limits

🔹Snapshot LTV

🔹Softer liquidations

It also lays the groundwork for future products and unlocks ftUSD's delta-neutral design.

Most DeFi tokens expand supply through emissions or unlock schedules.

@FlyingTulip_ ($FT) preserves capital, deploys it into yield, embeds redemption rights, and routes real revenue into buybacks.

Here’s where and how $FT is actually used 🧵

![AndreCronjeTech's tweet photo. Understanding @flyingtulip_ new raise model;

TLDR;

Market Cap: $2k

FDV: $175m

Volume: $33.5m

2 weeks in (and brutal markets) and yet the token looks boring (by design). Volume is tiny (by design).

Comparative projects that raised and TGE'd in the same time-frame are on average significantly down, and the reasoning is simple, bad markets cause people to exit/liquidate what they can, repay loans, and often move to cash in hand vs risk on strategies. If during these markets your only choice is "sell the token" that's the rational actor step. This new model on the other hand gives the holder choices; refund original investment (no loss), sell the Option instrument on the secondary market, withdraw the token and sell the token.

So you can either always exit at investment $0.10, or sell Option (which trade at 4-6% premium on the Options marketplace), or sell in the secondary market (at $0.09844c as per below). The rational action is to try to sell the Option, and if you need liquidity sooner to simply refund. We can see this in the numbers. On the secondary market total volume has been what we have bought back (7.9m tokens [~$790k] almost exclusively), the only real sells here have either been users who were in profit from ETH price decrease, or users who were trying to influence outcomes in Polymarket. Now the next point to understand is "but why is secondary price $0.9844 instead of $0.10", the Options give the $0.10 refund, the secondary market has 2 primary influences, 1. NAV buyback (which creates a floor [limit order] at NAV price of collateral backing withdrawn tokens, NOT full system NAV. Full system NAV would be ~$0.101c, withdrawn collateral backing puts are ~$0.098c. So when a user withdraws FT, their Option refund turns into a buy limit order at NAV price), and 2. yield/revenue/fees buys which are market buys at SPOT. This function is also why the spread is quite high since #2 keeps filling limit sell orders, and #1 keeps eating market sells.

Now if we look at the 2nd image, it shows a current investment value of ~$175m and at peak ~$207m. That's $32m in "volume" that would have otherwise sold on the secondary market, easy to see what would have happened to the token price. However now instead, they can simply exit not impacting ongoing holders (in fact to ongoing holders benefit, given now there is less circ supply). Lastly if we look at the Options market, then we have another additional ~$500k in sales at premium.

So that explains volume, but then let's have a quick look at marketcap and FDV and why both are wrong. FT has no minting ability, so it has a fixed totalsupply of 10bn that can only burn. However, the only way tokens can actually be part of this calculation is via Option sales (which were available during the public sale), so that means only 1.758bn is actually supply and the FDV would be $175m, but then what is circulating supply? Circulating supply is "liquid FT", aka, FT withdrawn from the Option (forfeiting the refund), so current tradable FT is 4.8m or $480k market cap, but now again, this is technically not accurate, because for every outstanding FT there is a NAV bid offsetting it. So in really marketcap is; circulating tokens (4.8m) * price ($0.09844) - exited_nav_price ($0.098c) = $2,134.18 ($2k mcap).

Holders who continue to wish to support the project are rewarded for longer participation with decreasing mcap and fdv, over and beyond price protection.

This is very cool.](https://pbs.twimg.com/media/HC5ok7YXkAELqyS.jpg)

![AndreCronjeTech's tweet photo. Understanding @flyingtulip_ new raise model;

TLDR;

Market Cap: $2k

FDV: $175m

Volume: $33.5m

2 weeks in (and brutal markets) and yet the token looks boring (by design). Volume is tiny (by design).

Comparative projects that raised and TGE'd in the same time-frame are on average significantly down, and the reasoning is simple, bad markets cause people to exit/liquidate what they can, repay loans, and often move to cash in hand vs risk on strategies. If during these markets your only choice is "sell the token" that's the rational actor step. This new model on the other hand gives the holder choices; refund original investment (no loss), sell the Option instrument on the secondary market, withdraw the token and sell the token.

So you can either always exit at investment $0.10, or sell Option (which trade at 4-6% premium on the Options marketplace), or sell in the secondary market (at $0.09844c as per below). The rational action is to try to sell the Option, and if you need liquidity sooner to simply refund. We can see this in the numbers. On the secondary market total volume has been what we have bought back (7.9m tokens [~$790k] almost exclusively), the only real sells here have either been users who were in profit from ETH price decrease, or users who were trying to influence outcomes in Polymarket. Now the next point to understand is "but why is secondary price $0.9844 instead of $0.10", the Options give the $0.10 refund, the secondary market has 2 primary influences, 1. NAV buyback (which creates a floor [limit order] at NAV price of collateral backing withdrawn tokens, NOT full system NAV. Full system NAV would be ~$0.101c, withdrawn collateral backing puts are ~$0.098c. So when a user withdraws FT, their Option refund turns into a buy limit order at NAV price), and 2. yield/revenue/fees buys which are market buys at SPOT. This function is also why the spread is quite high since #2 keeps filling limit sell orders, and #1 keeps eating market sells.

Now if we look at the 2nd image, it shows a current investment value of ~$175m and at peak ~$207m. That's $32m in "volume" that would have otherwise sold on the secondary market, easy to see what would have happened to the token price. However now instead, they can simply exit not impacting ongoing holders (in fact to ongoing holders benefit, given now there is less circ supply). Lastly if we look at the Options market, then we have another additional ~$500k in sales at premium.

So that explains volume, but then let's have a quick look at marketcap and FDV and why both are wrong. FT has no minting ability, so it has a fixed totalsupply of 10bn that can only burn. However, the only way tokens can actually be part of this calculation is via Option sales (which were available during the public sale), so that means only 1.758bn is actually supply and the FDV would be $175m, but then what is circulating supply? Circulating supply is "liquid FT", aka, FT withdrawn from the Option (forfeiting the refund), so current tradable FT is 4.8m or $480k market cap, but now again, this is technically not accurate, because for every outstanding FT there is a NAV bid offsetting it. So in really marketcap is; circulating tokens (4.8m) * price ($0.09844) - exited_nav_price ($0.098c) = $2,134.18 ($2k mcap).

Holders who continue to wish to support the project are rewarded for longer participation with decreasing mcap and fdv, over and beyond price protection.

This is very cool.](https://pbs.twimg.com/media/HC5owTgXsAAKkQM.jpg)