Kenyan businesses cut jobs in May for the first time in 15 months as demand weakens and costs rise.

According to the latest business survey, the score fell below 50 to 46.6 showing the economy is shrinking as sales drop and costs rise.

Na mjue Ebola ikifika Kenya it will not leave soon, Mpaka your minerals in Kenya iishe ndio iishe. It has been in existence for a decade in Congo because minerals haiishi

Kenyan taxpayers will spend Sh2.3 trillion on debt repayment and interest in the next financial year, nearly half of the government's Sh4.8 trillion budget.

Out of this, Sh1.3 trillion will go to interest payments alone.

WHY AFFORDABLE HOUSING SECURITIZATION IS A BAD IDEA FOR WORKERS

Your 1.5% Housing Levy deduction was sold to you as money to build houses. The Government now wants to use it as collateral for Sh100B bond. Your salary deduction is being turned into a borrowing instrument. You are not building houses. You are servicing a loan

Investors will earn Sh57.6B in interest on that bond. So you pay the levy. Government borrows against it. Investors pocket Ksh.57.6B in interest. Workers get what exactly? This is not affordable housing. This is affordable theft.

The bond matures beyond 10 years — longer than Ruto’s maximum constitutional tenure. Meaning even if Kenyans vote him out, the next government CANNOT abolish the Housing Levy without triggering a bond default. Your vote has been neutralised by a financial instrument. Think about that.

This is the same playbook used on the Sports Levy (now funding Talanta Stadium), Tourism Fund (now funding Bomas redevelopment) and Road Maintenance Levy (now funding SGR extension). Every levy eventually stops doing what it was introduced to do. The Housing Levy was always going to be next.

Your housing levy must build houses — not pad investor portfolios. Period. Watch this space. @WahomeHon@KeTreasury@AGOfficeKenya@lawsocietykenya

#HousingLevy #ConsumerRights

If EACC were to raid my home, this is what they will find. I work for every single cent I earn! Beyond taxes, I still contribute in cash + kind to build public institutions. What happened to honest, hard working, principled + altruistic Kenyans? Kshs 63m under the bed? No!

If a junior officer at City Hall kept Kshs 250 million under his mattress, how much money do think members of the executive, judiciary, parliament, governors and other government officials keep under their mattresses? My conservative estimates is Kshs 5.55 TRILLION.

When it comes to your money, the bank is NEVER your friend — you're competitors.

You both want the same shilling, just on opposite sides of the balance sheet.

You want a higher rate on your savings. The bank wants a wider spread: the gap between what it earns lending money out and what it pays you to hold yours. And right now, that gap is winning.

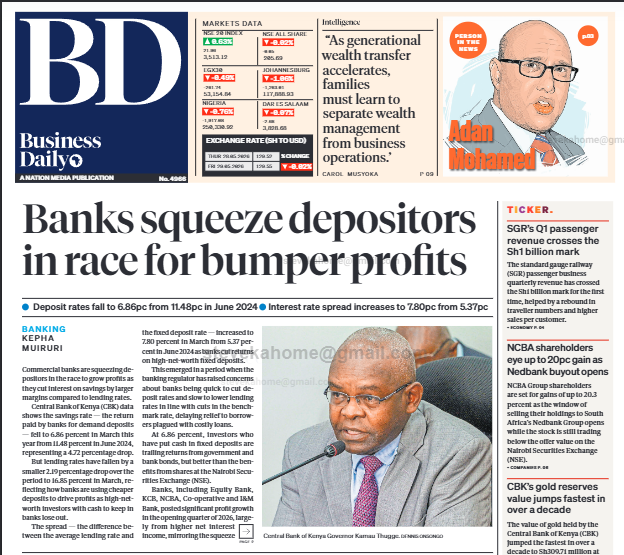

The latest CBK data tells the whole story. Average deposit rates have collapsed to 6.86% from 11.48% a year earlier, while the interest rate spread has widened to 7.80% from 5.37%.

Banks are paying depositors less and keeping more. That isn't an accident — it's the business model. It's also why your savings and fixed deposit accounts pay so little, and why only depositors locking up large sums for long tenors can negotiate anything better.

This is the gap money market funds have stepped into: a) An MMF pools savings into short-term instruments — Treasury bills, bank placements, fixed deposits and high-quality commercial paper — and passes the blended yield back to you. Because it sits at the short end of the curve, that yield typically tracks, and often beats, what a bank offers on savings or fixed deposit accounts.

b) It doesn't discriminate by size or tenor. Whether you invest KES 100 or KES 10 million, you earn the same daily-accruing yield, which moves with prevailing short-term rates. No negotiation required.

c) Liquidity is the clincher. Most funds let you withdraw within one to three working days with no early-exit penalty, and you keep every shilling of interest accrued to the day you exit.

One honest caveat: Unlike bank deposits, MMFs aren't covered by the KES 500,000 KDIC guarantee — your protection is CMA regulation, an independent custodian and diversification, not a state backstop.

For parking short-term cash, that trade-off still favours the MMF for most savers.

The real twist sits with the banks now running asset management arms. Are they steering clients into low-yield deposits, or into their own MMFs and fixed income funds?

The incentives don't point the same way.

As an investor, the maths is simple: if your bank can't beat the prevailing MMF rate net of tax and fees, where you park your money answers itself.

Local banks in Kenya are now cutting savings rates faster than lending rates.

Savings rates fell to 6.8% while lending rates are 16.8%, widening profits for banks.

Hi I'm lynet from Komarock I lost my kids date 13 may 2026 please 🙏 who ever see them please call me on these number 0726096432 name ,precious and Zennel

People MUST resist Freehold Land being turned into Leasehold and oppressive TAXES imposed with the Land being auctioned upon failure to pay the those taxes.Objective is to disposess people of their Lands and turn them into labourers for the new owners.We have a CRIMINAL regime

🚨 Michael Carrick on fielding a strong team vs Brighton:

🗣️ Reporter:

“There’s nothing left to play for. A lot of people were surprised by such a strong lineup.”

🗣️ Carrick:

“And that mentality right there is exactly why some clubs never become elite. What do you mean there’s nothing to play for?

This is Manchester United. Since when did we start celebrating third place like it’s a trophy? If I can score 10 against Brighton, I will. Happily.

Not because I hate them… but because we don’t relax here.

Even at 3-0, you go for the fourth. Then the fifth. Then the sixth. We’ve picked up the most points in the league since I took charge… and I don’t plan on dropping that standard. Next season, people will understand what we’re building.”