watching for something like this on $BTC

Alts rallying is giving me more confidence we'll continue higher, right now we're consolidating before the next push imo.

I know weekend scam pumps bla bla but this just feels different (famous last words)

Payments company Stripe and private equity firm Advent International have made a joint offer to acquire PayPal Holdings, $PYPL, for $60.50 per share, per Reuters

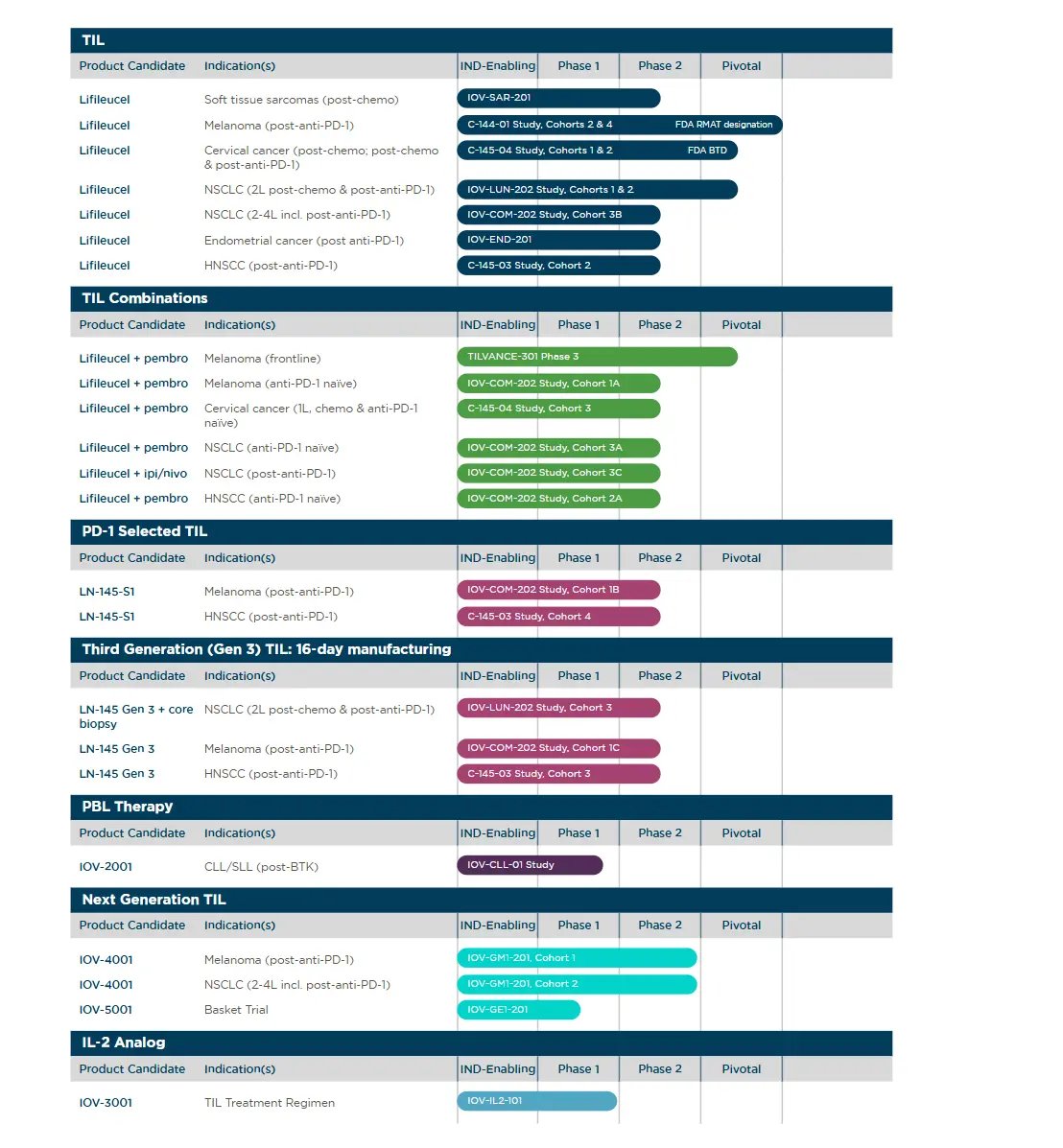

$IOVA Re-summarising the investment thesis of @IovanceBio! 🕊️

1. Iovance is the only company with an FDA-approved TIL therapy.

2. Strong backing from Dr. Steven Rosenberg (father of cancer immunotherapy) and Wayne Rothbaum, whose biotech investments often lead to successful buyouts and largest position is IOVA.

3. Iovance owns the only FDA-approved TIL manufacturing facility (iCTC) and holds 200+ end-to-end patents.

4. Real-world data continues to improve and is outperforming prior clinical trial results. When TIL works, TIL lasts, across solid tumours!

5. Major pharma players face patent expirations (e.g., Merck’s Keytruda). Iovance is partnered with Merck and expects updates from the TILVANCE-301 trial (Amtagvi + Keytruda in 1L).

6. Multiple biotech companies are discontinuing NSCLC trials, while Iovance has shown strong results and received FDA Fast Track designation. Given the progress in the IOV-LUN-202, we could see FDA approval as early as 2027 H1.

7. With a strong and deep pipeline, Iovance is building a platform to address solid tumours; a multi-billion business.

8. Already generating revenue, delivering 45% YoY in 26Q1.

#XBI #LABU #Biotech #FIRE #Cancer #NSCLC #Sarcomas #Melanoma #ClinicalTrials #LungCancer

Seems like a lot of people are up a ton on solana:9cRCn9rGT8V2imeM2BaKs13yhMEais3ruM3rPvTGpump but the exit door is the size of a pinhole.

Almost 300m market cap on paper but 2m in liquidity to actually exit. Right now the game is to advocate it as much as possible to get deeper DEX and CEX listings.👀

$IOVA chart is breaking out after its 2 competitors failed to meet study end points.

Genuinely believe TIL therapy is one of the best chances at a CURE for metastatic solid organ neoplasms with proven efficacy in melanoma and NSCLC data due soon.

High conviction bet with strong ancedoctal evidence & good m&a a candidacy.

Also super bullish on the 10 to 20 year timeframe.

1. AI will replace or augment most knowledge work.

2. AI spend as a proportion of knowledge-work comp is minuscule today, close enough to zero.

3. AI will revolutionize fields beyond software: robotics, biotech, materials science, physics, defense/military, etc. David’s argument is that coding revenue falls off → other revenue doesn’t replace it in time → air pocket. Given (2), even if coding softens, penetration into the broader knowledge-work base is still coming. AI spend should broaden over time.

4. All of this requires tremendous amounts of memory and compute for inference. Falling compute costs (his #2) are also demand-expanding: cheaper inference makes more workloads economic, a Jevons-style effect.

5. Even if you don’t believe any of this, winning the AI race is seen as existential by the US. The government is already turning from regulator into stakeholder: OpenAI is in active equity talks with Washington, and the Intel and IBM stakes are done. Expect more direct state support across the leading labs (Anthropic, DeepMind and peers), whether through equity, contracts, or otherwise.

A key crux of his argument is that 1) app revenue funds the buildout and 2) hyperscalers exercise normal ROI discipline.

1. understates it. The buildout isn’t underwritten by coding revenue specifically; it’s a bet on aggregate compute demand across every use case, made by hyperscalers and labs, not by the app-layer software firms whose code moats could erode. That moat erosion is an app-layer story. It doesn’t subtract from infra compute demand, which is broadening (see 2) and getting cheaper to serve (see 4). A SaaS-multiple shakeout isn’t an infra-capex collapse.

2. may not hold either. Spending here probably won’t be as disciplined as a strict microeconomic context would imply, given the strategic and geopolitical stakes. That may break, or at least delay, the “market realizes → spending stops” step.

For these reasons, I suspect the tailwind remains strong. The 2028 election matters a lot for the buildout, future regulation, taxation/UBI, etc.

So much can still go wrong: safety, high energy costs, rates and credit, employment disruption, liquidity, issuance. Whether we get a boom/bust over the next few years is hard to say. History suggests that’s often what happens, but I don’t think this argument is sufficient to conclude it.

Coding is only the first killer use case. AI spend is tiny relative to the knowledge work wage pool, cheaper inference may expand demand faster than costs fall, and compute is becoming strategic infrastructure.

None of these arguments eliminate the need for eventual returns. It may simply make the cycle longer, less disciplined, and more political.

All in all, I’m very bullish on human (and machine) ingenuity united toward a common goal.

The natural evolution of AI is AI augmented biotech & digital biology. If you lack exposure to this trend, you’re going to regret it. My bets are $ABSI, $ABCL, $IOVA

I have seen 3-4 posts talking about how incredible Hyperliquid is because people are watching price discovery for $SPCX on it after hours…

It is live on Robinhood too, and deeper.

The hyperliquid:native bull case is clear but come on, stop talking about it like it is the next CME lmao