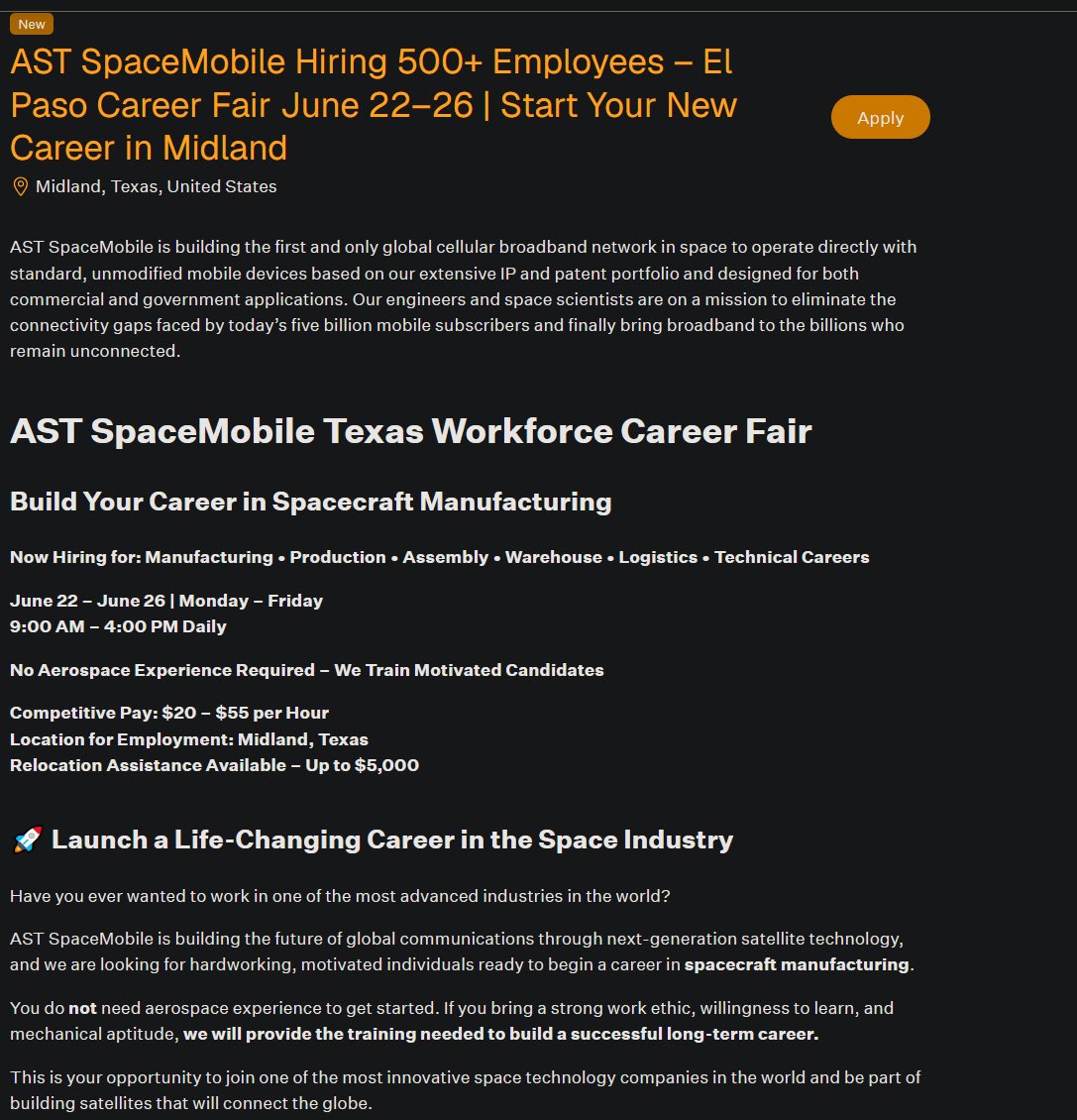

1/7 $ASTS is hiring 500 plus people in Midland. Sounds normal until you remember they only have around 1,200 employees total. Fill those roles and that is basically a 40% jump in headcount. You do not hire like that unless you are trying to build at volume.

🇺🇸 Anduril: The Company Rewriting The Entire Defense Industry

While everyone's distracted by SpaceX, the real disruption in defense is happening at Anduril Industries. The company just closed a $5B Series H round at a $61B valuation, doubling from $30.5B in just 9 months. Revenue went from $1B in 2024 to $2.1B in 2025 (+110% YoY), and they're projecting $4.3B in 2026.

In March 2026, the US Army awarded them a 10 year enterprise contract with a $20B ceiling, consolidating over 120 separate procurement actions into one framework. That kind of contract structure was historically reserved for Lockheed and Raytheon. Anduril just took a seat at the table the legacy primes have controlled for decades.

⚠️ Key Drivers

- Anduril's moat is software native architecture. Their Lattice OS platform fuses sensor data, AI targeting, and autonomous coordination across all domains. Legacy contractors built hardware first, software second. Anduril flipped the model,

- The Pentagon is pivoting to "intelligent mass": thousands of cheap autonomous systems instead of a few expensive platforms. Anduril's product stack maps perfectly to this doctrine. Lockheed's F-35 doesn't,

- Arsenal-1 in Ohio is a $1B, 5 million sq ft autonomous weapons factory designed to produce tens of thousands of drones per year. The Fury combat drone is already in production with Roadrunner, Barracuda, and classified programs to follow,

- International expansion is accelerating fast. Edge Group partnership (UAE), Rheinmetall (Europe), Dutch Ministry of Defence contracts, plus participation in the US "Golden Dome" missile defense system,

📈 TLDR: Anduril is doing to defense what Tesla did to automotive and SpaceX did to space launch. The legacy primes are 60 year old contractors trying to compete with a software first, AI native, vertically integrated machine. When this company goes public, it's going to be the most anticipated defense IPO in modern history.

$NBIS:

Retire your generation is not just a phrase here, it is the implication of what a $61B to $1.5T re-rating would actually mean

That is a ~24.6x move upside, translating a $240 entry point into something closer to $5,900 if the thesis fully compounds into that end-state valuation

At that scale, we are no longer talking about incremental upside, but a structural re-pricing of what $NBIS represents in the market, where early conviction gets rewarded asymmetrically and late positioning pays the premium for hesitation

Today's price might one day be considered as one of the early entry on Nebius

DYOR

SpaceX went public and then traded poorly, and it's a good reminder that even the most hyped names have to grow into their valuations eventually.

I'm not touching it yet. I'd rather watch how it trades for a couple of quarters before I form a real opinion on it.

Nebius is still growing revenue at a pace most companies would kill for, and it comes down to one thing: they rent out the GPUs every AI lab is desperate to get their hands on.

Demand isn't slowing and they keep adding capacity to match it. As long as compute stays this scarce, I think the runway is long. I'm adding on the dips.

I'm long $NBIS

Nebius is the only company I'll put all my money behind. Every drop is a gift, and this week has been full of gifts.

I've doubled down on my position and averaged up after a long time.

Nebius is one of the only NeoClouds with a clear path to becoming a hyperscaler in its own right. The AWS of AI inference.

~7x revenue growth YoY. 45% AI cloud EBITDA margins. ARR scaling to $7-9B. Power buildout pushing into GW territory.

@Funmentalist just dropped a 2030 valuation model that maps exactly where this goes. One of the sharpest pieces on the name out there.

This weekend I'll work on my own deep dive for Nebius and share it for free, both here and on Substack.

If you're selling this name, it's because you don't like money.

I'm a simple Pikachu.

I don't like debating which NeoCloud is better.

I just like printing money.⚡

Micron's next chapter is HBM4, the memory that goes inside Nvidia's upcoming Vera Rubin chips.

That supply is already spoken for through 2026 and they've started selling 2027 capacity.

When a product is sold out that far in advance, the company gets to set its own prices. That's the main reason I'm comfortable holding MU through weeks like this.

What just happened?

In just 27 minutes, the Nasdaq 100 just fell -1,000 points and the S&P 500 erased -$1 TRILLION without any major headlines.

The Nasdaq opened +1% higher then fell -3% between 9:30 AM and 9:57 AM ET.

What does it all mean? Let us explain.

(a thread)

AMD had a rough Friday and fell with the rest of the chip names after Apple raised prices and funds sold to lock in quarter-end gains.

None of that has much to do with how the actual business is doing, which is still growing fast. The dips that come from rebalancing are usually the ones I end up glad I bought.

Per Morgan Stanley, $AMD 2nm Venice CPU could rise from 1.25mn units in 2026 to 6.75mn units in 2027

A 5x jump, and notably running ahead of Nvidia's 3nm Vera CPU at 5.75mn units over the same year

Michael Burry just bought long-dated Microsoft calls running out to 2028.

This is the guy who made his name betting against things, and now he's making a bullish bet on a mega-cap, right as it bounced 5% on Friday.

I'm not buying just because he did, but it got my attention.

Microsoft is down 25% this year, and on Friday it jumped almost 5% while the rest of tech kept bleeding.

Buyers stepped in because the stock is the cheapest it's been against its earnings in years.

I've been waiting for a setup like this on MSFT, so I'm watching it closely now.

Korea down, futures down, fear index at 26, recession chatter everywhere. Weeks like this are the whole reason long-term investors get paid.

I've never once been rewarded for panicking. I have been rewarded, again and again, for staying. Holding.

Everyone's asking if a recession is coming. The actual data says probably not yet.

The Sahm rule sits at 0.10 against a 0.50 trigger, and markets price 2026 recession odds near 12%.

The fear is real. The recession, so far, isn't. I trade what's measured, not what's felt.

BREAKING: US inflation just came in at 3-year high, and the Fed has almost no room left to cut rates.

The PCE Price Index, the Fed's main inflation gauge, rose 4.1% year over year in May, up from 3.8% the month before.

That's the wrong direction, and still more than double the Fed's 2% target.

At the same time, the economy is not slowing down.

Q1 GDP grew 2.1%, well above the 1.6% forecast.

The labor market backs this up. Initial jobless claims came in at 215,000, better than the 225,000 expected, meaning companies are still not cutting workers in large numbers.

Consumers are spending too.

Personal spending rose 0.7% in May, above the 0.6% forecast. Core durable goods orders, which strip out volatile transport numbers, rose 1.3%.

There is one weak spot.

Headline durable goods orders fell 4.5% in May, a sharp reversal from an 8.5% gain the month before. Since the core number stayed positive, this looks more like a one month swing than a trend.

Put it together and you get strong growth, strong spending, a tight job market, and inflation still rising.

That combination gives the Fed almost no justification to cut rates anytime soon.

This data lands right as Kevin Warsh, the new Fed Chair, has already signaled he is open to more rate hikes instead of cuts.

Numbers like these only strengthen that case heading into the next FOMC meeting.

The fear index is sitting at 26 today, 25 yesterday, buried in "Fear."

Here's the uncomfortable part: that zone is historically closer to where money gets made than lost. I do my best buying when the screen is red and my hands are a little shaky.

🚨 BLOODBATH in Asian Markets

Over $1 TRILLION wiped out from Asian stocks in just a few hours.

Asian stocks crashing after Apple's price hikes to offset surging chip costs reignited concerns over elevated AI and Tech valuations.

South Korea's KOSPI down -8.2%, wiping out over ₩500,200,000,000,000 ($340 billion).

Japan's NIKKEI down -4.5%, wiping out over ¥52,500,000,000,000 ($355 BILLION).

China's SSE down -2.15%, wiping out over ¥1,645,000,000,000 ($229 BILLION).

Taiwan's stock market down -3%, erasing NT$132,000,000,000,000 ($127 BILLION).

South Korea's market got hit hard again today, down around 3% with Samsung and SK Hynix leading the fall. When the memory-chip capital of the world sells off this fast, it's worth asking what they're scared of.

The answer is hot inflation and a Fed that might hike. I'm watching from far away.

Rakuten's CEO just called AST's network "critical" for Japan's security.

When a carrier starts describing your tech as national infrastructure, the story stops being about hype and starts being about contracts.

Living in Japan, this one lands a little closer for me.

Vodafone España and Satellite Connect Europe sign commercial agreement to bring satellite-to-mobile broadband connectivity to Spain

https://t.co/xb6Z1yt8HW

Another European market just lit up for AST: Vodafone Spain, normal phone, signal straight from space. Spain now, then the next country, then the next.

I hold ASTS because the map is filling in one flag at a time, and that's how a network quietly turns into a business.

$ASTS: 🚨🇪🇸 VODAFONE SPAIN JOINS SATELLITE CONNECT EUROPE TO OFFER DIRECT SATELLITE-TO-MOBILE COVERAGE

Vodafone and Telefónica advance in direct satellite-to-mobile connectivity to reinforce coverage in remote areas, emergencies, and strategic sectors.

Note: Vodafone Spain is owned by Zegona Communications, a British PE firm

By Agencias

24 JUN, 2026

Vodafone Spain has reached a commercial agreement with Satellite Connect Europe, a Luxembourg-based provider of 'direct-to-device' (D2D) satellite connectivity, with the aim of enabling direct satellite connection to mobile phones and thus ensuring continuous coverage in remote areas, emergency situations, corporate environments, and for individual users.

Vodafone's Director of Technology and Operations, Julia Velasco, announced this during the DigitalES Summit, which is taking place this Wednesday and Thursday in Madrid.

The VodafoneSAT service is designed to provide additional connectivity to companies and isolated areas as an extra layer of resilience, providing a signal where the traditional mobile network does not reach, including rural areas, maritime areas, and emergency or natural disaster scenarios, as well as security crisis responses

Thanks to this technology, a user with a mobile phone in a location without coverage will be able to send messages via applications or consult maps, using the available spectrum very efficiently.

Among the main foreseen uses are emergency response, connectivity in rural areas and at sea, as well as applications in defense, security, agriculture, and business services.

Throughout 2026, use cases will be launched with companies, public administrations, and sectors considered strategic, in order to develop practical applications based on this satellite solution.

The service is expected to be commercialized starting in 2027, subject to the evolution of the regulatory framework. However, in exceptional or emergency circumstances, its early deployment could be authorized, always with the relevant institutional approvals.

Telefónica reinforces its collaboration with Satellite Connect Europe.

On the other hand, Telefónica already announced at the Mobile World Congress (MWC) that it was collaborating with Satellite Connect Europe to explore the application of satellite-enabled services for consumers, businesses, and public services in Spain and Germany, as announced this Monday by the Spanish "telco".

The collaboration will focus on analyzing how "D2D" satellite capabilities could be integrated with Telefónica's existing 4G and 5G networks, with the aim of complementing terrestrial connectivity and improving network resilience in specific scenarios, such as remote areas or exceptional circumstances, maintaining an operator-managed experience.

https://t.co/DpGEwOnV8R

$MSFT says Copilot saved NHS staff an average of 43 minutes a day in a trial, and it's rolling out to 505,000 people.

Multiply 43 minutes by half a million workers and you get the entire AI bull case in one stat. Not magic, just time handed back at scale.

🚨 $MSFT

Just a filthy looking monthly candlestick.

It has not closed below the 50 month moving average in 15 years!!

Threatening this month...

Buy when fearful?