What happens when Bitcoin stops depending on traders… and starts depending on paychecks?

A single policy change just linked BTC to a $9T retirement machine.👇🧵

---------------------------

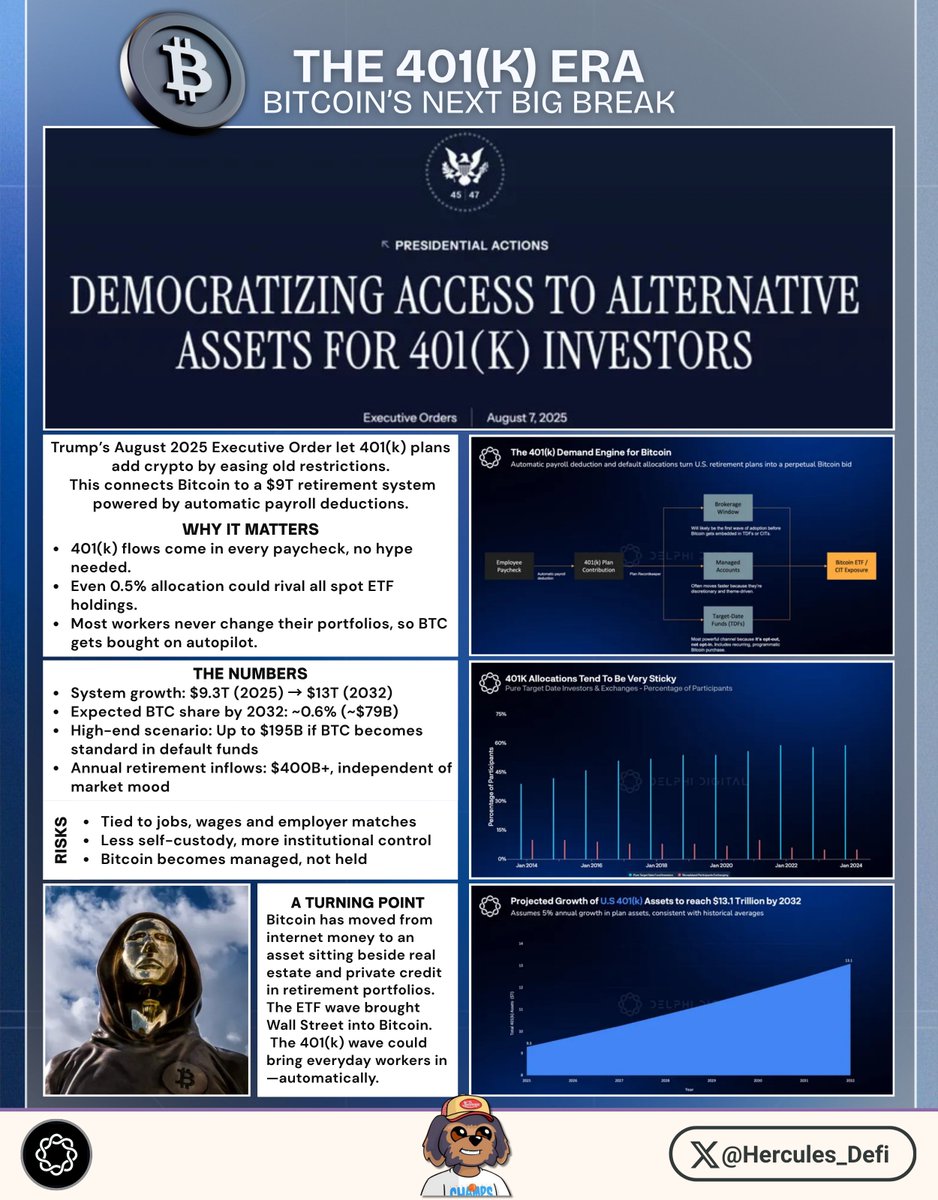

𝘛𝘳𝘶𝘮𝘱’𝘴 𝘈𝘶𝘨𝘶𝘴𝘵 2025 𝘌𝘹𝘦𝘤𝘶𝘵𝘪𝘷𝘦 𝘖𝘳𝘥𝘦𝘳 𝘮𝘪𝘨𝘩𝘵 𝘦𝘯𝘥 𝘶𝘱 𝘣𝘦𝘪𝘯𝘨 𝘢 𝘣𝘪𝘨𝘨𝘦𝘳 𝘣𝘳𝘦𝘢𝘬𝘵𝘩𝘳𝘰𝘶𝘨𝘩 𝘧𝘰𝘳 𝘉𝘪𝘵𝘤𝘰𝘪𝘯 𝘵𝘩𝘢𝘯 𝘌𝘛𝘍𝘴.

What Trump did was simple but powerful: he allowed 401(k) retirement plans to add cryptocurrency by telling the Department of Labor to relax the rules that were holding institutions back.

---------------------------

𝐈𝐦𝐩𝐚𝐜𝐭 𝐨𝐧 𝐁𝐢𝐭𝐜𝐨𝐢𝐧

That change connects Bitcoin to a massive pool of slow, steady, nonstop savings, around $9T in the U.S. retirement system.

And unlike ETFs, which rise and fall with hype, sentiment and news, 401(k) money flows in automatically through payroll deductions, no matter what is happening in the market.

Before this order, most employers and retirement platforms were hesitant to offer Bitcoin even if they wanted to, because the regulatory framework was unclear and the risk of non-compliance was too high.

But this move gives giants like Fidelity, Schwab and Vanguard room to finally include Bitcoin exposure in 401(k) options.

The scale is what changes everything. Even the smallest percentage allocation, let’s say 0.5% of retirement assets, would almost double the total amount currently held in spot Bitcoin ETFs.

And the impact goes beyond the numbers. It creates a consistent buyer that keeps accumulating regardless of market noise, price dips or the fear-greed mood swings that usually dominate Bitcoin investing.

---------------------------

𝐋𝐞𝐭’𝐬 𝐜𝐡𝐞𝐜𝐤 𝐨𝐮𝐭 𝐭𝐡𝐞 𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞 𝐨𝐟 401(𝐤)

Most employees contribute automatically every month, and most of them never change their allocations once it’s set.

Studies suggest that around 95% of retirement participants don’t adjust their portfolios in a given year. That is, the minute Bitcoin appears in any fund used inside a 401(k), the system drip-buys it with every paycheck.

It’s a different kind of demand that keeps flowing even when retail panic is selling at the bottom.

---------------------------

𝐖𝐚𝐲𝐬 𝐢𝐧 𝐰𝐡𝐢𝐜𝐡 𝐁𝐢𝐭𝐜𝐨𝐢𝐧 𝐜𝐚𝐧 𝐦𝐚𝐤𝐞 𝐰𝐚𝐲 𝐢𝐧𝐭𝐨 401(𝐤) 𝐩𝐥𝐚𝐧𝐬

➢ Brokerage windows, where individuals who want Bitcoin can buy it manually, much like they pick specific stocks or ETFs.

➢ The next layer would be managed accounts, where professional portfolio managers allocate a slice of the portfolio on behalf of workers.

➢ But the deepest and most transformative change would be if Bitcoin becomes part of the default products inside these plans like target-date funds or collective trusts that people get enrolled into automatically when they start their jobs.

𝘐𝘧 𝘉𝘪𝘵𝘤𝘰𝘪𝘯 𝘨𝘦𝘵𝘴 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘢𝘵 𝘵𝘩𝘢𝘵 𝘭𝘦𝘷𝘦𝘭, 𝘮𝘪𝘭𝘭𝘪𝘰𝘯𝘴 𝘰𝘧 𝘈𝘮𝘦𝘳𝘪𝘤𝘢𝘯𝘴 𝘤𝘰𝘶𝘭𝘥 𝘴𝘵𝘢𝘳𝘵 𝘥𝘰𝘭𝘭𝘢𝘳-𝘤𝘰𝘴𝘵 𝘢𝘷𝘦𝘳𝘢𝘨𝘪𝘯𝘨 𝘪𝘯𝘵𝘰 𝘉𝘛𝘊 𝘸𝘪𝘵𝘩𝘰𝘶𝘵 𝘦𝘷𝘦𝘯 𝘬𝘯𝘰𝘸𝘪𝘯𝘨 𝘪𝘵. 𝘛𝘩𝘦𝘺 𝘫𝘶𝘴𝘵 𝘸𝘰𝘳𝘬, 𝘦𝘢𝘳𝘯, 𝘤𝘰𝘯𝘵𝘳𝘪𝘣𝘶𝘵𝘪𝘰𝘯𝘴 𝘨𝘦𝘵 𝘥𝘦𝘥𝘶𝘤𝘵𝘦𝘥 𝘢𝘯𝘥 𝘉𝘪𝘵𝘤𝘰𝘪𝘯 𝘨𝘦𝘵𝘴 𝘣𝘰𝘶𝘨𝘩𝘵.

---------------------------

How fast this happens depends on the Department of Labor’s timeline.

If new guidance comes out in early 2026, adoption will likely roll out in two stages.

➢ The early stage will be brokerage windows and more experimental retirement plans that already offer alternative assets.

➢ After that, once the platforms are confident, we’d see Bitcoin show up inside managed portfolios and eventually in the default funds that most workers never touch or modify.

Historically, new asset classes take one to two years to spread through the 401(k) ecosystem. Bitcoin will probably follow the same pattern.

𝐓𝐡𝐞 S𝐩𝐞𝐜𝐮𝐥𝐚𝐭𝐞𝐝 N𝐮𝐦𝐛𝐞𝐫𝐬

If we try to model how much money could realistically flow into Bitcoin over time, the numbers get interesting even with conservative assumptions.

The 401(k) system is projected to grow from roughly $9.3 trillion in 2025 to around $13 trillion by 2032. If Bitcoin manages to earn even a sliver of that allocation, retirement plans could hold around 0.6% of assets in BTC by 2032 ( roughly $79 billion).

Even conservative scenarios, where adoption is slow and limited mostly to brokerage windows, still funnel several billion dollars into Bitcoin over time. On the high end, if Bitcoin becomes a standard line item in default retirement funds, exposure could reach close to $195 billion.

The point is that small percentages matter when you’re dealing with a system that channels over $400 billion a year into retirement accounts through worker contributions and employer matches.

This demand doesn’t sleep. People don’t look at their paycheck deduction every two weeks and ask themselves whether the Bitcoin market sentiment looks bullish. They just keep contributing.

Retirement flows happen even during fear, sideways trading, corrections and headlines about market doom. This is a new kind of structural buying force for Bitcoin designed to accumulate for decades.

---------------------------

𝐏𝐨𝐭𝐞𝐧𝐭𝐢𝐚𝐥 𝐑𝐢𝐬𝐤𝐬

Once Bitcoin is plugged into the payroll-funded retirement system, it becomes tied to the wage economy in a way it has never been before. If unemployment spikes, contributions slow.

If companies cut matching programs in a recession, the automatic buying pressure reduces. Bitcoin starts depending not just on investors but on job markets, wage growth and economic cycles. Inflation, layoffs and hiring freezes suddenly matter to Bitcoin in a new way.

There’s also the institutional aspect. The deeper Bitcoin integrates with TradFi, the more it risks losing some of the decentralized identity that defined it in the early days.

If most retirement exposure sits inside funds run by large custodians, then millions of holders won’t have self-custody. Their Bitcoin will live inside managed accounts governed by compliance rules, benchmarks, quarterly reporting and risk committees.

𝘐𝘯 𝘵𝘩𝘢𝘵 𝘸𝘰𝘳𝘭𝘥, 𝘉𝘪𝘵𝘤𝘰𝘪𝘯 𝘣𝘦𝘤𝘰𝘮𝘦𝘴 𝘢𝘯 𝘢𝘴𝘴𝘦𝘵 𝘵𝘩𝘢𝘵 𝘪𝘴 𝘮𝘢𝘯𝘢𝘨𝘦𝘥, 𝘯𝘰𝘵 𝘩𝘦𝘭𝘥. 𝘋𝘦𝘤𝘪𝘴𝘪𝘰𝘯𝘴 𝘨𝘦𝘵 𝘧𝘪𝘭𝘵𝘦𝘳𝘦𝘥 𝘵𝘩𝘳𝘰𝘶𝘨𝘩 𝘵𝘩𝘦 𝘴𝘢𝘮𝘦 𝘤𝘰𝘳𝘱𝘰𝘳𝘢𝘵𝘦 𝘴𝘺𝘴𝘵𝘦𝘮𝘴 𝘉𝘪𝘵𝘤𝘰𝘪𝘯 𝘸𝘢𝘴 𝘰𝘳𝘪𝘨𝘪𝘯𝘢𝘭𝘭𝘺 𝘥𝘦𝘴𝘪𝘨𝘯𝘦𝘥 𝘵𝘰 𝘳𝘰𝘶𝘵𝘦 𝘢𝘳𝘰𝘶𝘯𝘥.

So here’s the big question:

𝐃𝐨𝐞𝐬 𝐦𝐚𝐢𝐧𝐬𝐭𝐫𝐞𝐚𝐦 𝐚𝐝𝐨𝐩𝐭𝐢𝐨𝐧 𝐬𝐭𝐫𝐞𝐧𝐠𝐭𝐡𝐞𝐧 𝐁𝐢𝐭𝐜𝐨𝐢𝐧 𝐨𝐫 𝐝𝐢𝐥𝐮𝐭𝐞 𝐢𝐭𝐬 𝐜𝐨𝐫𝐞 𝐢𝐝𝐞𝐧𝐭𝐢𝐭𝐲?

➢ ETFs made Bitcoin accessible.

➢ 401(k)s could make it ubiquitous.

But ubiquity also means integration into the structures Bitcoin was meant to exist outside of. The truth is that adoption changes the asset. As Bitcoin is pulled deeper into the financial system, it becomes subject to the conventions of that system allocation models, regulatory guidance, institutional incentives, and asset managers who now control billions on behalf of workers.

---------------------------

𝐇𝐨𝐰 𝐅𝐚𝐫 𝐁𝐢𝐭𝐜𝐨𝐢𝐧 𝐇𝐚𝐬 𝐂𝐨𝐦𝐞

Still, it’s hard to deny how far Bitcoin has come.

From an internet currency to an asset recognized alongside real estate and private credit inside the world’s largest retirement system is a massive shift. And this change brings something Bitcoin has never had before: a steady wave of automatic buyers who don’t care about charts, bull markets, bear markets, crypto Twitter or macro narratives.

They just contribute to retirement every month like they always have. That quiet accumulation is incredibly powerful in an asset with fixed supply.

The move also marks a turning point for the narrative. Bitcoin is becoming part of the financial system.

The ETF era brought Wall Street into Bitcoin. The 401(k) era could bring millions of workers into Bitcoin without them even lifting a finger. Whether that future strengthens Bitcoin or reshapes it is a question the industry will wrestle with for years.

𝘐𝘯 𝘤𝘰𝘯𝘤𝘭𝘶𝘴𝘪𝘰𝘯, 𝘵𝘩𝘦 𝘌𝘹𝘦𝘤𝘶𝘵𝘪𝘷𝘦 𝘖𝘳𝘥𝘦𝘳 𝘤𝘰𝘶𝘭𝘥 𝘦𝘯𝘥 𝘶𝘱 𝘣𝘦𝘪𝘯𝘨 𝘰𝘯𝘦 𝘰𝘧 𝘵𝘩𝘦 𝘮𝘰𝘴𝘵 𝘴𝘪𝘨𝘯𝘪𝘧𝘪𝘤𝘢𝘯𝘵 𝘮𝘰𝘮𝘦𝘯𝘵𝘴 𝘪𝘯 𝘉𝘪𝘵𝘤𝘰𝘪𝘯’𝘴 𝘩𝘪𝘴𝘵𝘰𝘳𝘺 𝘣𝘦𝘤𝘢𝘶𝘴𝘦 𝘪𝘵 𝘶𝘯𝘭𝘰𝘤𝘬𝘴 𝘢 𝘵𝘺𝘱𝘦 𝘰𝘧 𝘥𝘦𝘮𝘢𝘯𝘥 𝘵𝘩𝘦 𝘮𝘢𝘳𝘬𝘦𝘵 𝘩𝘢𝘴 𝘯𝘦𝘷𝘦𝘳 𝘴𝘦𝘦𝘯, 𝘢𝘶𝘵𝘰𝘮𝘢𝘵𝘪𝘤, 𝘤𝘰𝘯𝘵𝘪𝘯𝘶𝘰𝘶𝘴 𝘢𝘯𝘥 𝘣𝘶𝘪𝘭𝘵 𝘪𝘯𝘵𝘰 𝘵𝘩𝘦 𝘱𝘢𝘺𝘤𝘩𝘦𝘤𝘬𝘴 𝘰𝘧 𝘦𝘷𝘦𝘳𝘺𝘥𝘢𝘺 𝘱𝘦𝘰𝘱𝘭𝘦.

---------------------------

Disclaimer: This post is based on the @Delphi_Digital's report written by

@that1618guy. Link to the report in the second tweet.

Why is it so hard for people to understand that this is all political stunts between these two titans... Trump and Powell probably having breakfast and laughing over who's having the best shots. Trump needs to blame Powell for f...ing up the economy so he can rebuild it in the next 3 years. Why? look at the housing market, it's unsustainable