We thought we were getting a TACO

"Trump Always Chickens Out"

But so far we are getting a NACHO

"Not A Chance Hormuz Opens"

(With appreciation to the trader who told me)

Over the last 48 hours:

1. Iran has closed the Strait of Hormuz

2. The US claimed peace talks would resume with Iran tomorrow

3. Iran has backed out of peace talks with the US

4. Iran has accused the US of plotting a “surprise attack”

5. The US has struck and seized an Iranian vessel in the Strait of Hormuz

6. Iran has denied Trump’s claims of giving up uranium enrichment

There appears to be severe distrust on both sides of the table in this conflict.

Trump says “no deal” this week would be detrimental for Iran.

Futures open in 2 hours.

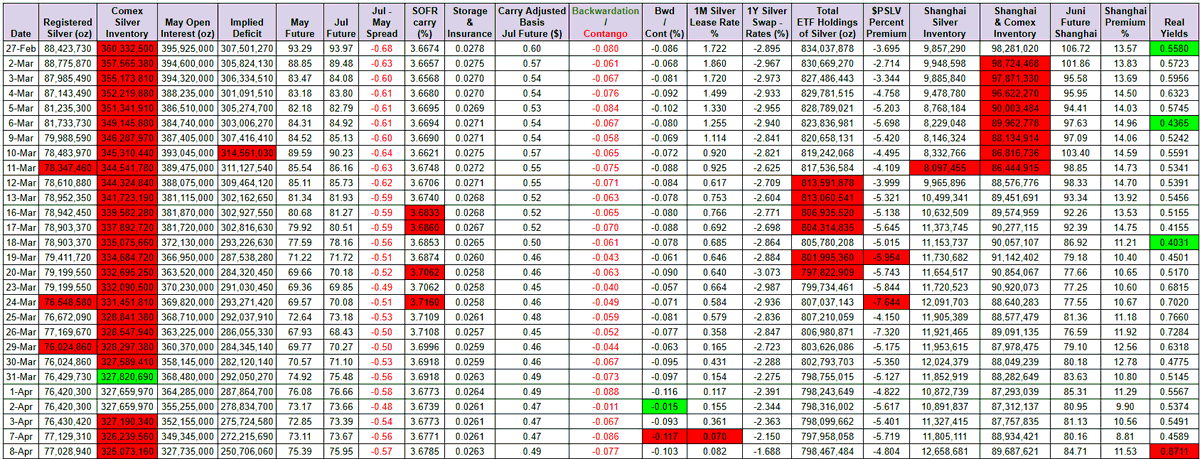

Oil, silver and gold are all at the high of the day.

The negative correlation between oil and silver/gold looks broken for good.

If silver breaks $80, ETF inflows return, lease rates rise, the 1-year swap goes more negative, and phase two of the silver bull market begins.

Morning all!

- US President Trump threatened massive military escalation if Iran deal terms are not met, vowed no nuclear weapons and to secure the Strait of Hormuz.

- Iran’s Parliament Speaker Ghalibaf said three clauses of the 10-point plan have been violated so far, and as such, a bilateral ceasefire or negotiations is unreasonable.

- IRGC claimed on Thursday that shipping through the Strait of Hormuz slowed sharply and then stopped following what it said was an Israeli ceasefire violation in Lebanon, according to CNN.

- FOMC Minutes stated that many said persistently higher oil prices could keep inflation elevated long enough to justify rate rises.

- APAC stocks were lower in a mild pullback from yesterday's ceasefire-fuelled extremes; European equity futures indicate a marginally lower open with Euro Stoxx 50 futures down 0.1%.

- Looking ahead, highlights include German Trade Balance (Feb), Industrial Production (Feb), US Initial Jobless Claims (Apr/04), PCE Final (Feb), GDP Final (Q4), Atlanta Fed GDP, NBP Policy Announcement, Banxico Minutes. Comments from SNB's Schlegel. Supply from Spain, UK & US.

You hit the nail on the head. Iraq doesn’t even have a national shipping line like Bahri; they sell most of their oil on an FOB basis.

It’s non-Iraqi tankers that actually move the oil, so literally nothing is going to change. Even at this very moment, drones are being launched at Iraqi oil fields.

No captain or shipowner who’s terrified of a physical attack is suddenly going to jump at the chance to carry Iraqi barrels.

You have to read between the lines here—it’s pure political propaganda. Iran has been constantly pushing the GCC countries to ditch the US and Israel.

Their message is: "See? If you abandon the US like we said, your oil can flow." It’s a performance for the GCC public and the international community.

Iran knows full well the UAE, Qatar, Saudi, and Bahrain can’t just flip like that. But for them it’s all about the narrative and the optics.

Plus considering Iraq has the largest Shia population in the GCC and many militias under the PMF are tightly aligned with Iran, Tehran needs to send a conciliatory message to them as well.

I don’t think we should read too much into it, but the market might think otherwise—it’s a place full of wishful thinking just bc a few ships passed through a strait that used to move ~20mb/d.

Of course they never mention the vessel types, whether it’s bulk or liquid, or the absolute volume. That’s just how they play the game.

#oott #iran

Oil experts are an interesting breed of people. They are sorta like gold bugs. For long periods they sit in a distant corner of the financial markets. We pass by their desks and they nod at us and occasionally they get our attention and draw us close. We hear their predictions of chaos and global doom. We slowly back away and go about our business and live life.

Episodically once every decade or so these same people are thrust to the center of the stage. They haven't changed. They are the same people. It's us who have decided to pay attention. Their story remains the same. Energy is a physical commodity and real supply shocks will unleash chaos on the global economy for years to come. The thing is they amaze us with their depth and understanding of all things energy. Barrel count, geopolitical alignments of countries, grades, distillates, etc. So many facts. So much depth. So credible. They always had this level of credibility. They have specialized in this topic for their lifetime and we are simply tourists. They are incredibly valuable and always have been.

Maybe this time is different. Certainly market prices of oil and scarce immediate supply is "chaotic" and feeds back into the real economy. Heck I care about the path of oil and its impact on the global economy and various market sectors. At the same time I suggest recognizing that YOU are the one who has changed. If your Oil guru or gurus have been saying the same thing for decades despite being wrong for decades it's your job to find the rare one who is pivoting and see their rationale and then for YOU to back slowly away from the perma oil bulls.

Morning all!

- US President Trump reportedly told aides he's willing to end the war without reopening the Strait of Hormuz, according to the WSJ.

- US Secretary of State Rubio presented a plan at last week's G7 foreign ministers' meeting for the Strait of Hormuz to be run by a multinational coalition, while he stressed there would be “no fees, and free circulation” through the shipping route.

- The Iranian Foreign Ministry said they have not conducted any negotiations with the US during the 31 days of the war.

- The EU will expand its naval operations in the Red Sea and western Indian Ocean, but will for now refrain from taking part in any potential missions to secure oil and gas shipments through the Strait of Hormuz.

- APAC stocks were mixed; European equity futures indicate a flat cash market open with Euro Stoxx 50 futures up 0.1%.

- Looking ahead, highlights include German Retail Sales (Feb), Import Prices (Feb), Unemployment Rate (Mar), UK GDP Final (Q4), French/Italian/EZ Inflation Prelim. (Mar), Canadian GDP Prelim. (Feb), US JOLTS (Feb), Australian Manufacturing PMI Final (Mar). Speakers include Fed's Goolsbee, Barr & Bowman. Supply from Germany. Earnings from Nike.

Markets are starting to reflect the reality of the Middle East situation.

While the $SPX500 is now -7.1% YTD, our portfolio has recovered this week and is outperforming on a relative basis as energy strengthens and gold stabilises.

Full update: https://t.co/wtsVXf9cV1

I’m the most copied Popular Investor on eToro with 250K+ followers, +$300M AUC, and 35% avg. annual returns over 5 years.

Copy Trading is not investment advice | Capital at risk | Past performance does not guarantee future results.

To grasp the extent of how much oil demand will need to decrease to balance out 12 million b/d of supply outage, consider this:

During the peak COVID lockdown, global oil demand fell 15 million b/d.

Note: April 2020 balance +20 million b/d due to Saudi’s surge in production.

BREAKING: An oil tanker operator paid Iran a $2 million fee for safe passage through the Strait of Hormuz on Wednesday, per FT.

Iran is now charging "favored" countries millions per oil tanker for safe passage through Hormuz.

Good morning to our US followers!!

- Iran's armed forces said Iran's retaliation against attacks on its energy infrastructure is not yet complete, SNN reported; any repeat of such attacks will lead to a far stronger retaliation against the enemy, enemy infrastructure and that of their allies.

- US President Trump said Israel violently lashed out at Iran's major facility and that the US did not know about the attack, while he said there will be no more attacks by Israel on South Pars; added that the US will retaliate by massively blowing up the entirety of the South Pars Gas Field if Qatar's LNG is attacked again.

- FX mixed amid the central bank bonanza; SNB, Riksbank and BoJ all left rates unchanged, as expected, while the BoE and ECB await.

- Crude surges as attacks in the Persian Gulf threaten long-term damage to major energy facilities.

- European equities suffer as Energy continues to surge; US equity futures follow suit, Micron slips after increasing capex plans.

- Fixed income weighed on energy upside and hawkish Chair Powell.

- Looking ahead, highlights include US Initial Jobless Claims (Mar/14), Atlanta Fed GDP, New Zealand Trade Balance (Feb), BoE & ECB Policy Announcements. Speakers include ECB's Lagarde. Supply from the US. Earnings from FedEx.

Morning all!

- US President Trump said they had a big day on Tuesday, knocking out targets, and said it will be a couple of weeks regarding Iran, not much longer, and that they are way ahead of schedule.

- Iran confirmed that its security chief Larijani was killed, according to Iranian media.

- Iran's Foreign Minister said Iran will target US forces wherever they assemble, including near urban areas, he understands neighbours' concerns and holds the US responsible for the conflict.

- APAC stocks were mostly higher following the positive handover from Wall Street and as oil prices retreated, while markets now await a flurry of upcoming central bank policy decisions, including from the FOMC later today.

- European equity futures indicate a higher cash market open with Euro Stoxx 50 futures up 0.5% after the cash market closed with gains of 0.5% on Tuesday.

- Looking ahead, highlights include EZ CPI Final (Feb), US PPI (Feb), New Zealand GDP (Q4), BoC, Fed & BCB Policy Announcements. Speakers include BoC's Macklem & Rogers, Fed Chair Powell & NVIDIA (NVDA) CEO Huang. Supply from Germany. Earnings from Micron & HelloFresh.

I think it's funny to read some of the oil commentary saying that oil prices aren't that "high" today because it's not going to be that "bad".

No man.

That's because there was a cushion at the beginning of the conflict. We are now eating through that.

Here's what I wrote on March 4 in our report titled, "Why Aren't Oil Prices At $100?"

How much storage do we have before the market starts to panic?

Well, here’s the math:

The Middle East exports ~19 million b/d of crude + condensate + products through the Strait of Hormuz. Saudi’s East-West pipeline has a capacity of ~5 million b/d, but a chunk of that was already in-use. UAE also has the ability to bypass with the Abu Dhabi pipeline (Habshan-Fujairah) with a capacity of ~1.8 million b/d.

Excluding Iranian flows (~2 million b/d), that leaves us with ~10 to ~12 million b/d at risk.

We’ve already had 6 days of disruptions. This amounts to ~60 to ~72 million bbls of crude + condensate + product. Production shut-in so far has been restricted to producers with no real storage capacity (Iraq).

Goldman estimates that there are ~312 million bbls of capacity available. So we are still 2 weeks away from needing to shut in more production.

After storage capacity hits max capacity and if tanker flows remain restricted, that’s when we will see panic. Meanwhile, the global oil market is working through the excess crude on water and the surplus in storage that we have in 2025.

By our estimate, excess crude on water and excess onshore storage will be gone in 2-3 weeks. This is roughly the same timeline as the production shut-in scenario.

In other words, if we don’t see tanker activity pick up after 2 weeks, prepare for the worst-case scenario. For now, the oil market is absorbing the shock via the excess in storage. It won’t have much left after.

This is primarily the reason why we haven’t seen oil shoot past triple digits just yet.

BREAKING: US oil companies are set to make an additional $60+ billion this year if oil prices sustain current levels.

US oil companies are:

1. Expected to be the "biggest beneficiaries" of the Iran war

2. Set to generate an extra $5 billion in free cash flow this month alone

3. Expected to see large gains in the shale business which has little ties to Middle East

Big oil is seeing some of its most profitable conditions ever.

The misunderstanding within the U.S. administration regarding Iran mirrors the Israeli government’s misunderstanding of Hezbollah.

A. Iran and Hezbollah view the current confrontation as a historic opportunity to reshape the strategic end-state of the conflict.

B. They have no intention of surrendering, conceding, or returning to the previous ceasefire arrangements with Israel. On the contrary, both actors appear prepared for a prolonged confrontation essentially a war of attrition — until Israel and the United States agree to new terms that would ensure neither Israel nor the U.S. can surprise them militarily in the future.

C. To achieve this, Iran and Hezbollah are relying on their ability to exhaust Israeli population. In Iran’s case, the strategy also includes putting pressure on Gulf states and the global economy, thereby creating leverage to force more favorable terms in any eventual settlement.

D. Threats alone are unlikely to work — not against Iran and not against Hezbollah. Large-scale ground operations are also unlikely to produce decisive outcomes and may even favor the defending side. Israel and the United States can inflict significant military damage in Lebanon and potentially in Iran, but it is highly doubtful that either actor will simply capitulate.

E. More troubling still, even the end of a military campaign against Iran especially if it is unilateral — is unlikely to bring the confrontation in Lebanon to an end. Hezbollah’s campaign against Israel is not automatically contingent on the immediate course of events inside Iran. In fact, Tehran could continue supporting Hezbollah’s military effort even after a direct confrontation with the United States or Israel subsides.

F. In other words, a military “endgame” with Iran does not necessarily translate into strategic closure in Lebanon. Hezbollah retains its own operational logic and incentives to continue the fight, particularly if Iran sees value in sustaining pressure on Israel through the Lebanese front without Israel accepting Hezbollah terms.

G. Therefore, relying solely on military power without a parallel diplomatic track risks dragging Israel into a prolonged and expanding confrontation with Iran and Hezbollah — two actors that show little sign of backing down.

The alternative is a diplomatic process that includes credible guarantees addressing the strategic concerns that drive Iran and Hezbollah’s current posture.

H. What is already clear, however, is that recent U.S. and Israeli actions have destabilized the fragile ceasefire arrangements that existed in the Iranian and Lebanese arenas. The status quo ante is unlikely to return. The strategic choice now appears to be between expanding the conflict until Iran and Hezbollah "surrender" or pursuing an agreement that, to some degree, incorporates the conditions demanded by Iran and Hezbollah.

#IranWar