Almost every winner I own took years, not months.

Here is how long I actually had to hold to get these gains.

$APLD +1100%, held since 2022 trade few lots at 500% in 2025 still 3+ years

$MU +1000%, over 2+ years

$VSAT about 8x, around 15 months

$CIFR +600%, over 2 years

$NVTS +500%, about 13 months

$RKLB +400%, about a year and a half

$RGTI +400%, over 2+ years

$GOOGL +300% on the oldest lots, since 2022

$AVGO +200%, about 2+ years

$KOPN +200%, under a year

$SMCI +100% on the 2024 lots, about 2+ years

$RR +50%, about a 18 months

$META +40%, over 2 years

$AMZN 2 to 3x, held since 2018. Recently closed last week.

This is not even the full list. I am missing a few names and did not go through the whole portfolio.

Only one or two of these paid off (still it can go negative as I did not capture the gains) in under a year, and even those were never a sure thing.

None of them went straight up. Most put me through drawdowns of 50% or more, and I sat through every one. I did not panic. I added what I could, and each time that was the right call. Nothing stays down forever, and nothing stays up forever.

I do not chase the 10x. I buy names I want to own, let the winners run, and keep adding to what is working.

Real estate taught me how to wait, and that same patience is what pays in the market.

This has been fun to put together. None of it is that difficult. I just read what is public and learned as I went.

It's not a sprint, it's a marathon.

Last 10 years in. Stocks and real estate. Many multibaggers along the way, some 1,2,3,4x, some 5x, some 50x.

The pattern is simple. Do the work. Put a sizable lump sum in, or DCA. Then sit. I went on to Build buildings. Live life. Focus on family. Let the position breathe.

Most names need time. The compression builds quietly while everyone gets bored. Then one day it just breaks and runs. Your job is to hold.

Early names: $AMZN $TSLA $SHOP $MARA $RIOT. More recently $APLD $MU $RGTI $CIFR $NVTS $VSAT $RKLB $QS $SLS $OSS $HURA $KOPN $RDW $AMPG $RR $NVDA $GOOGL $AVGO $AMD $AMKR $ZETA $OSCR. Probably forgetting a few.

90% stocks. 10% options.

Only 9 months into options trading. Most of mine are 1 to 2 year expiries. Rarely 6 months, and only on names I really know. $APLD 40 strike calls bought when it was sub 20 and everyone hated it. 8 to 9x already. Exercising the rest.

I am here to win. Competitive, but only against myself. The market does not care about your feelings. You cannot control macros, market makers, or headlines. You can only control you.

If you are following any of my positions, know my risk appetite runs hotter than most. Size it for you, not for me.

Control your risk. Protect capital. Always do your own research before riding anyone's trade on X. Nobody can see a price target with any certainty. Anyone who claims they can is fooling themselves.

It is not a sprint. It is a marathon.

As someone holding $CIFR for the long term, this CNBC sit-down with Tyler Page mostly reinforced why.

On the pipeline he did not hedge. 'It's extraordinarily robust,' he said. That tracks with a 4.2 GW portfolio across 10 sites, 600 MW of it already under construction for hyperscaler tenants. The market spent two years seeing a bitcoin:native miner. He thinks it is finally seeing the real business.

The core idea is about land. 'We're ahead of the curve,' he said, and the reasoning is contrarian. To make mining work, you chase cheap power where generation is abundant and demand is thin. West Texas, mostly. The AI buildout flipped those same spots from tier three to tier one, and $CIFR was already standing there with a deep land position.

His read on demand was blunt. He called AI adoption 'a completely convex adoption curve,' with tenants now wanting 200 to 500 MW at a single campus. His question as a non incumbent was simple. Where do you find that in Northern Virginia? There is not enough power there, so the demand has to move to where the power already sits.

On the old latency objection, he pointed to a fiber line built 25 years ago running east to west under I-20, where they found unused capacity. For training and inference he claims 'sub 10 milliseconds' to the major Texas metros. Not low enough for traditional cloud, but fine for AI work.

The part I keep coming back to is the deal method. The 4.2 GW he frames as grid connections. The faster lever is bring your own power. Tap the natural gas pipeline next door with a lateral, build your own generation, and skip the grid queue. He says that path can deliver power in about '18 months' instead of years. His line on the land says all of it: 'an endless ocean of natural gas.' Sites sitting on cheap gas, next to existing fiber, able to self generate while grid interconnects catch up. Speed to power is the moat right now, and he is selling speed.

Execution backs the talk. A $5.5B, 15 year AWS lease for 300 MW with phase one due this July. The earlier Fluidstack and $GOOG deal. A 1 GW JV called Colchis. A new Ohio site that opens the PJM market. A third hyperscaler lease and a $200M revolver. $MS just lifted its target to $53.50.

The stock now trades on future leases instead of mining cash flow, which is why a soft bitcoin:native tape still pulls it around. It faded from $28.56 to about $26 today.

None of that changes the long term picture for me. Rent starts landing in August, the land is real, and the power strategy is the difference.

It's not a sprint, it's a marathon.

$CIFR sum of parts:

$18 signed leases

$8 Reveille 70 MW + Ulysses 200 MW (near-term, priced in)

$56 McLennan 500 MW + Mikeska 500 MW + Colchis 1,000 MW (medium-term, not priced in)

Total bull case: $82/share

Stock near $25 today. The market is paying for the floor and the near-term layer. The $56 medium-term layer is the gap.

Catalyst: ERCOT batch study clarity in June. If McLennan, Mikeska, and Colchis all land in Batch Zero, that layer starts getting marked up.

Still long $CIFR.

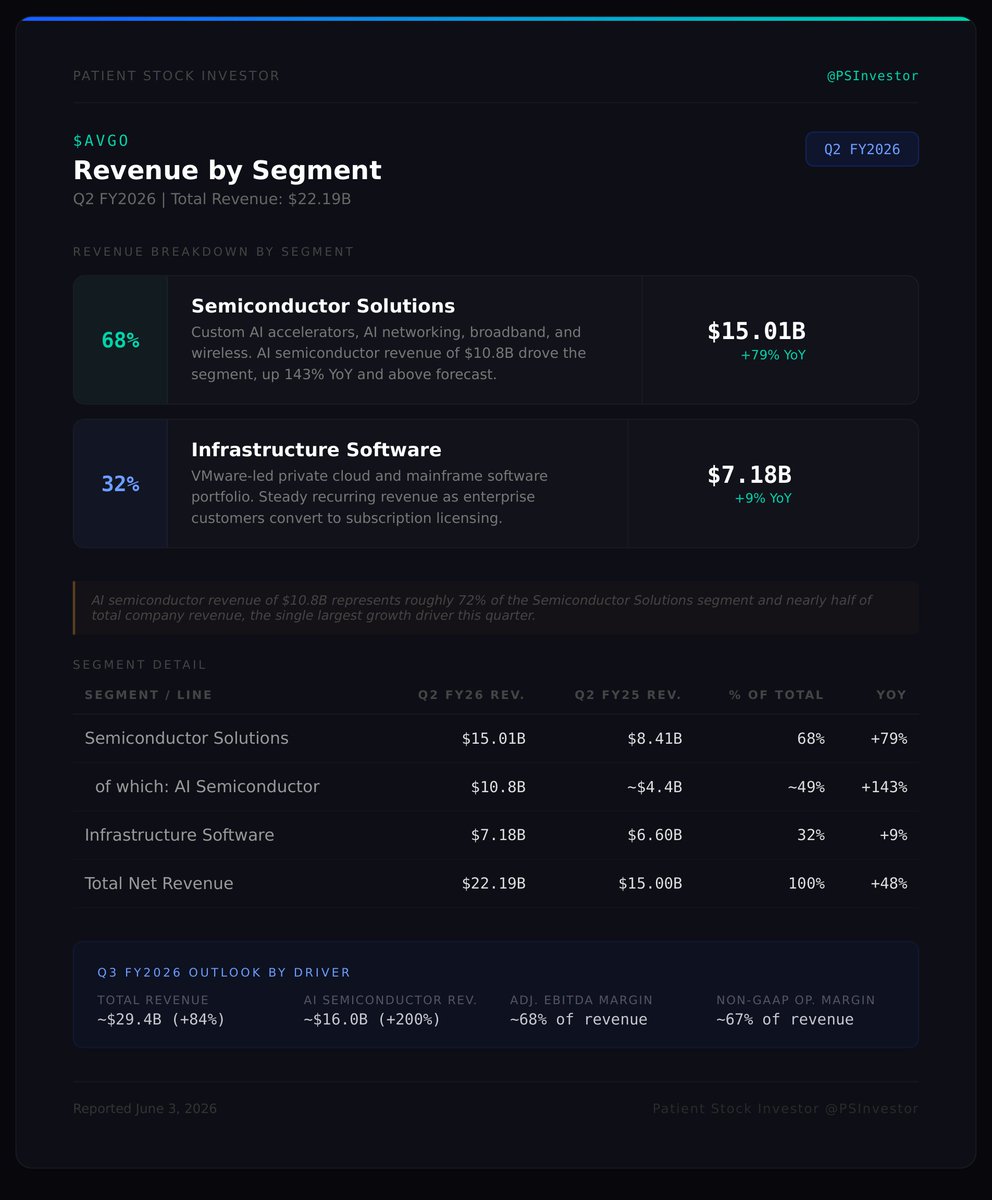

$AVGO Hock Tan, President and Chief Executive Officer: 'Broadcom achieved record revenue, operating profit and free cash flow in Q2 driven by accelerating growth in AI semiconductor revenue and strong operating leverage. Q2 semiconductor revenue from AI of $10.8 billion grew 143% year-over-year, above our forecast, driven by increasing demand for custom AI accelerators and AI networking. The momentum continues and in Q3 we expect semiconductor revenue from AI to grow over 200 percent year-over-year to $16.0 billion.'

Bullish commentary on $QS from the Time Holme and Shahar Noi conversation:

The big shift is $QS opening a second front. EV was always the long game. Now they have a credible play into AI data centers, and the framing is sharp. Power is the bottleneck, not silicon. Energy density and safety per square millimeter is what data center architects will pay for.

The Shahar Noi hire matters. 30 years in tech, 25 in semiconductors, 10 building data center systems at $AVGO , $SNDK , and $MRVL . That is not a marketing hire. That is someone who knows how a rack is built, how hyperscalers buy, and where the pain lives. $QS bringing him in says they are serious about commercializing this beyond a slide.

The math he walked through is hard to ignore. 3x more power per GPU vs CPU, 3x denser racks, then cluster scaling. 50x more power demand in the AI era versus cloud compute. Within 5 years GPUs up 5x, racks up 8x. Hundreds of megawatts to gigawatts per site. Supply catches up slowly. The pipe between the grid and the GPU is where the gap sits, and almost no one is talking about it.

$QS sits in that gap in three ways. Delivery at 800V, already proven through the PowerCo and Ducati work. Storage with higher Wh per liter, which gives architects more room to cram GPUs in the same footprint. Buffer use as a fast discharge layer that smooths spiky AI workloads so GPU utilization stays near peak. All three lean on real attributes of the cell, not promises.

Safety is the quiet bull case. Solid state with a non-combustible ceramic separator inside a 24/7 hyperscale environment is a different risk conversation than lithium ion. As voltage moves up to 800V, the risk profile moves further inside the building. That favors cells that do not go thermal.

What I like about this pivot is that it expands the TAM without abandoning EV. Same cell, same chemistry, different end market, faster procurement cycle, and customers writing close to $1T in AI capex this year. If even a sliver of that capex routes into advanced battery buffers and BBUs, the optionality is real.

What still needs to be earned: actual data center contracts, named hyperscaler partners, and volume. The PowerCo ramp remains the anchor for commercial credibility. But the strategic positioning is sharper than it has been in a long time, and the hire backs it up.

Net read: bullish. The story is no longer single-track EV. It is now solid state into two of the largest capex cycles of this decade. One of my biggest conviction stock since 2024. This is going to run the same way $NVTS did soon.

$AVGO Hock Tan, President and Chief Executive Officer: 'Broadcom achieved record revenue, operating profit and free cash flow in Q2 driven by accelerating growth in AI semiconductor revenue and strong operating leverage. Q2 semiconductor revenue from AI of $10.8 billion grew 143% year-over-year, above our forecast, driven by increasing demand for custom AI accelerators and AI networking. The momentum continues and in Q3 we expect semiconductor revenue from AI to grow over 200 percent year-over-year to $16.0 billion.'

Broadcom $AVGO Q2 FY2026 earnings are out.

The AI story is no longer a side narrative, it is the whole engine. Custom AI accelerators and AI networking pushed AI semiconductor revenue past every internal forecast, and management is now guiding to a level of growth next quarter that reframes what this company is.

Key catalysts from the report:

- AI semiconductor revenue reached a new record and grew triple digits as custom accelerator demand from hyperscalers accelerated

- Q3 guidance calls for total revenue to step up sharply with AI semis expected to more than double year-over-year

- Operating leverage is widening, with adjusted EBITDA margin near 70% and free cash flow approaching half of revenue

Hock Tan $AVGO, President and Chief Executive Officer:

'𝘉𝘳𝘰𝘢𝘥𝘤𝘰𝘮 𝘢𝘤𝘩𝘪𝘦𝘷𝘦𝘥 𝘳𝘦𝘤𝘰𝘳𝘥 𝘳𝘦𝘷𝘦𝘯𝘶𝘦, 𝘰𝘱𝘦𝘳𝘢𝘵𝘪𝘯𝘨 𝘱𝘳𝘰𝘧𝘪𝘵 𝘢𝘯𝘥 𝘧𝘳𝘦𝘦 𝘤𝘢𝘴𝘩 𝘧𝘭𝘰𝘸 𝘪𝘯 𝘘2 𝘥𝘳𝘪𝘷𝘦𝘯 𝘣𝘺 𝘢𝘤𝘤𝘦𝘭𝘦𝘳𝘢𝘵𝘪𝘯𝘨 𝘨𝘳𝘰𝘸𝘵𝘩 𝘪𝘯 𝘈𝘐 𝘴𝘦𝘮𝘪𝘤𝘰𝘯𝘥𝘶𝘤𝘵𝘰𝘳 𝘳𝘦𝘷𝘦𝘯𝘶𝘦 𝘢𝘯𝘥 𝘴𝘵𝘳𝘰𝘯𝘨 𝘰𝘱𝘦𝘳𝘢𝘵𝘪𝘯𝘨 𝘭𝘦𝘷𝘦𝘳𝘢𝘨𝘦. 𝘛𝘩𝘦 𝘮𝘰𝘮𝘦𝘯𝘵𝘶𝘮 𝘤𝘰𝘯𝘵𝘪𝘯𝘶𝘦𝘴 𝘢𝘯𝘥 𝘪𝘯 𝘘3 𝘸𝘦 𝘦𝘹𝘱𝘦𝘤𝘵 𝘴𝘦𝘮𝘪𝘤𝘰𝘯𝘥𝘶𝘤𝘵𝘰𝘳 𝘳𝘦𝘷𝘦𝘯𝘶𝘦 𝘧𝘳𝘰𝘮 𝘈𝘐 𝘵𝘰 𝘨𝘳𝘰𝘸 𝘰𝘷𝘦𝘳 200 𝘱𝘦𝘳𝘤𝘦𝘯𝘵 𝘺𝘦𝘢𝘳-𝘰𝘷𝘦𝘳-𝘺𝘦𝘢𝘳 𝘵𝘰 16.0 𝘣𝘪𝘭𝘭𝘪𝘰𝘯 𝘥𝘰𝘭𝘭𝘢𝘳𝘴.'

Kirsten Spears $AVGO, Chief Financial Officer:

'𝘐𝘯 𝘘3 𝘸𝘦 𝘦𝘹𝘱𝘦𝘤𝘵 𝘤𝘰𝘯𝘴𝘰𝘭𝘪𝘥𝘢𝘵𝘦𝘥 𝘳𝘦𝘷𝘦𝘯𝘶𝘦 𝘨𝘳𝘰𝘸𝘵𝘩 𝘵𝘰 𝘪𝘯𝘤𝘳𝘦𝘢𝘴𝘦 84% 𝘺𝘦𝘢𝘳-𝘰𝘷𝘦𝘳-𝘺𝘦𝘢𝘳 𝘵𝘰 29.4 𝘣𝘪𝘭𝘭𝘪𝘰𝘯 𝘥𝘰𝘭𝘭𝘢𝘳𝘴, 𝘸𝘪𝘵𝘩 𝘯𝘰𝘯-𝘎𝘈𝘈𝘗 𝘰𝘱𝘦𝘳𝘢𝘵𝘪𝘯𝘨 𝘮𝘢𝘳𝘨𝘪𝘯 𝘴𝘵𝘢𝘣𝘭𝘦 𝘢𝘵 67% 𝘳𝘦𝘧𝘭𝘦𝘤𝘵𝘪𝘯𝘨 𝘰𝘶𝘳 𝘴𝘵𝘳𝘰𝘯𝘨 𝘰𝘱𝘦𝘳𝘢𝘵𝘪𝘯𝘨 𝘭𝘦𝘷𝘦𝘳𝘢𝘨𝘦.'

Revenue mix is tilting hard toward semiconductors, which now make up roughly two thirds of the business, while the VMware-led infrastructure software segment keeps compounding steadily in the background. The custom silicon franchise is doing the heavy lifting and the software base is funding it.

Inflection point: AI semiconductors are crossing from a fast-growing line item into the dominant revenue driver, and the Q3 guide implies that shift is accelerating rather than maturing.

My take: when a company this size guides to 84% revenue growth and still talks about stable margins, the market stops debating whether the AI cycle is real and starts arguing about how long it lasts. I am watching the durability of custom accelerator demand more than any single quarter.

Broadcom $AVGO Q2 FY2026 earnings are out.

The AI story is no longer a side narrative, it is the whole engine. Custom AI accelerators and AI networking pushed AI semiconductor revenue past every internal forecast, and management is now guiding to a level of growth next quarter that reframes what this company is.

Key catalysts from the report:

- AI semiconductor revenue reached a new record and grew triple digits as custom accelerator demand from hyperscalers accelerated

- Q3 guidance calls for total revenue to step up sharply with AI semis expected to more than double year-over-year

- Operating leverage is widening, with adjusted EBITDA margin near 70% and free cash flow approaching half of revenue

Hock Tan $AVGO, President and Chief Executive Officer:

'𝘉𝘳𝘰𝘢𝘥𝘤𝘰𝘮 𝘢𝘤𝘩𝘪𝘦𝘷𝘦𝘥 𝘳𝘦𝘤𝘰𝘳𝘥 𝘳𝘦𝘷𝘦𝘯𝘶𝘦, 𝘰𝘱𝘦𝘳𝘢𝘵𝘪𝘯𝘨 𝘱𝘳𝘰𝘧𝘪𝘵 𝘢𝘯𝘥 𝘧𝘳𝘦𝘦 𝘤𝘢𝘴𝘩 𝘧𝘭𝘰𝘸 𝘪𝘯 𝘘2 𝘥𝘳𝘪𝘷𝘦𝘯 𝘣𝘺 𝘢𝘤𝘤𝘦𝘭𝘦𝘳𝘢𝘵𝘪𝘯𝘨 𝘨𝘳𝘰𝘸𝘵𝘩 𝘪𝘯 𝘈𝘐 𝘴𝘦𝘮𝘪𝘤𝘰𝘯𝘥𝘶𝘤𝘵𝘰𝘳 𝘳𝘦𝘷𝘦𝘯𝘶𝘦 𝘢𝘯𝘥 𝘴𝘵𝘳𝘰𝘯𝘨 𝘰𝘱𝘦𝘳𝘢𝘵𝘪𝘯𝘨 𝘭𝘦𝘷𝘦𝘳𝘢𝘨𝘦. 𝘛𝘩𝘦 𝘮𝘰𝘮𝘦𝘯𝘵𝘶𝘮 𝘤𝘰𝘯𝘵𝘪𝘯𝘶𝘦𝘴 𝘢𝘯𝘥 𝘪𝘯 𝘘3 𝘸𝘦 𝘦𝘹𝘱𝘦𝘤𝘵 𝘴𝘦𝘮𝘪𝘤𝘰𝘯𝘥𝘶𝘤𝘵𝘰𝘳 𝘳𝘦𝘷𝘦𝘯𝘶𝘦 𝘧𝘳𝘰𝘮 𝘈𝘐 𝘵𝘰 𝘨𝘳𝘰𝘸 𝘰𝘷𝘦𝘳 200 𝘱𝘦𝘳𝘤𝘦𝘯𝘵 𝘺𝘦𝘢𝘳-𝘰𝘷𝘦𝘳-𝘺𝘦𝘢𝘳 𝘵𝘰 16.0 𝘣𝘪𝘭𝘭𝘪𝘰𝘯 𝘥𝘰𝘭𝘭𝘢𝘳𝘴.'

Kirsten Spears $AVGO, Chief Financial Officer:

'𝘐𝘯 𝘘3 𝘸𝘦 𝘦𝘹𝘱𝘦𝘤𝘵 𝘤𝘰𝘯𝘴𝘰𝘭𝘪𝘥𝘢𝘵𝘦𝘥 𝘳𝘦𝘷𝘦𝘯𝘶𝘦 𝘨𝘳𝘰𝘸𝘵𝘩 𝘵𝘰 𝘪𝘯𝘤𝘳𝘦𝘢𝘴𝘦 84% 𝘺𝘦𝘢𝘳-𝘰𝘷𝘦𝘳-𝘺𝘦𝘢𝘳 𝘵𝘰 29.4 𝘣𝘪𝘭𝘭𝘪𝘰𝘯 𝘥𝘰𝘭𝘭𝘢𝘳𝘴, 𝘸𝘪𝘵𝘩 𝘯𝘰𝘯-𝘎𝘈𝘈𝘗 𝘰𝘱𝘦𝘳𝘢𝘵𝘪𝘯𝘨 𝘮𝘢𝘳𝘨𝘪𝘯 𝘴𝘵𝘢𝘣𝘭𝘦 𝘢𝘵 67% 𝘳𝘦𝘧𝘭𝘦𝘤𝘵𝘪𝘯𝘨 𝘰𝘶𝘳 𝘴𝘵𝘳𝘰𝘯𝘨 𝘰𝘱𝘦𝘳𝘢𝘵𝘪𝘯𝘨 𝘭𝘦𝘷𝘦𝘳𝘢𝘨𝘦.'

Revenue mix is tilting hard toward semiconductors, which now make up roughly two thirds of the business, while the VMware-led infrastructure software segment keeps compounding steadily in the background. The custom silicon franchise is doing the heavy lifting and the software base is funding it.

Inflection point: AI semiconductors are crossing from a fast-growing line item into the dominant revenue driver, and the Q3 guide implies that shift is accelerating rather than maturing.

My take: when a company this size guides to 84% revenue growth and still talks about stable margins, the market stops debating whether the AI cycle is real and starts arguing about how long it lasts. I am watching the durability of custom accelerator demand more than any single quarter.

$AVGO reports Q2 FY26 tomorrow after the close . Options are pricing a ~10.6% move.

$AVGO beats every quarter, but by low single digits. The stock trades on the guide and the margins, not the beat.

Last 3 prints:

Q3 FY25 | EPS +1.8%, Rev +0.8% → +9% next day, +20% in a week

Q4 FY25 | EPS +3.2%, Rev +3.1% → -11% next day, worst day since 2020

Q1 FY26 | EPS +1.5%, Rev +0.6% → +5% next day, +8% in a week

Why they moved:

Q3: a $10B custom AI chip order revealed on the call. The catalyst, not the beat.

Q4: gross margins guided down ~100bps at 57x forward earnings. The beat was not enough.

Q1: multiple reset to ~32x, solid beat, plus a big Q2 guide.

Watch tomorrow:

Gross margin commentary, this is what sank Q4

The Q3 revenue guide

Q2 is already guided to $22B rev (+47% YoY), AI semis ~$10.7B

Beat is the base case. The reaction lives in the margins and the guide.

ChargePoint $CHPT Q1 FY27 earnings are out.

A third straight quarter of year-over-year growth, and the story underneath is the mix. The high-margin subscription software business keeps compounding while the company keeps cutting cost, so the losses are narrowing even though hardware demand is still soft.

Key catalysts from the report:

- Launch of Express Solo, billed as the world's fastest standalone EV charger at up to 600 kW to a single port

- New transit win supplying DC fast charging to Santa Monica's Big Blue Bus e-bus fleet

- OBE Power partnership to deploy roughly 2,500 charging ports at multifamily residences

- Jyothi Swaroop hired as Chief Marketing and Growth Officer to lead global go-to-market

Rick Wilmer $CHPT, President and Chief Executive Officer:

'𝘘1 𝘸𝘢𝘴 𝘢 𝘴𝘵𝘳𝘰𝘯𝘨 𝘴𝘵𝘢𝘳𝘵 𝘵𝘰 𝘵𝘩𝘦 𝘺𝘦𝘢𝘳 𝘧𝘰𝘳 𝘊𝘩𝘢𝘳𝘨𝘦𝘗𝘰𝘪𝘯𝘵, 𝘢𝘴 𝘸𝘦 𝘦𝘹𝘤𝘦𝘦𝘥𝘦𝘥 𝘵𝘩𝘦 𝘩𝘪𝘨𝘩 𝘦𝘯𝘥 𝘰𝘧 𝘰𝘶𝘳 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦, 𝘥𝘦𝘭𝘪𝘷𝘦𝘳𝘦𝘥 𝘢 𝘵𝘩𝘪𝘳𝘥 𝘤𝘰𝘯𝘴𝘦𝘤𝘶𝘵𝘪𝘷𝘦 𝘲𝘶𝘢𝘳𝘵𝘦𝘳 𝘰𝘧 𝘺𝘦𝘢𝘳-𝘰𝘷𝘦𝘳-𝘺𝘦𝘢𝘳 𝘨𝘳𝘰𝘸𝘵𝘩, 𝘢𝘯𝘥 𝘮𝘢𝘪𝘯𝘵𝘢𝘪𝘯𝘦𝘥 𝘴𝘵𝘳𝘰𝘯𝘨 𝘮𝘢𝘳𝘨𝘪𝘯𝘴 𝘸𝘪𝘵𝘩 𝘤𝘰𝘯𝘵𝘪𝘯𝘶𝘦𝘥 𝘤𝘰𝘴𝘵 𝘥𝘪𝘴𝘤𝘪𝘱𝘭𝘪𝘯𝘦.'

'𝘊𝘩𝘢𝘳𝘨𝘦𝘗𝘰𝘪𝘯𝘵 𝘪𝘴 𝘦𝘯𝘵𝘦𝘳𝘪𝘯𝘨 𝘵𝘩𝘦 𝘺𝘦𝘢𝘳 𝘧𝘰𝘤𝘶𝘴𝘦𝘥 𝘰𝘯 𝘢𝘤𝘤𝘦𝘭𝘦𝘳𝘢𝘵𝘪𝘯𝘨 𝘨𝘳𝘰𝘸𝘵𝘩, 𝘥𝘳𝘪𝘷𝘦𝘯 𝘣𝘺 𝘪𝘯𝘯𝘰𝘷𝘢𝘵𝘪𝘰𝘯 𝘭𝘪𝘬𝘦 𝘵𝘩𝘦 𝘯𝘦𝘸 𝘌𝘹𝘱𝘳𝘦𝘴𝘴 𝘚𝘰𝘭𝘰, 𝘵𝘩𝘦 𝘸𝘰𝘳𝘭𝘥'𝘴 𝘧𝘢𝘴𝘵𝘦𝘴𝘵 𝘴𝘵𝘢𝘯𝘥𝘢𝘭𝘰𝘯𝘦 𝘌𝘝 𝘤𝘩𝘢𝘳𝘨𝘦𝘳.'

The revenue mix is doing the heavy lifting. Subscriptions are now roughly 40% of the top line and carry far richer margins than charging hardware, which is why gross margin is holding and adjusted EBITDA loss keeps shrinking even with networked systems sales barely growing.

Inflection point: ChargePoint is quietly turning into a software and recurring-revenue business wrapped around a hardware install base, and the narrowing losses are the first real sign that the cost discipline is sticking.

$AI Q4 FY2026 earnings are out.

The headline is not the numbers, it is the leadership change. Founder Tom Siebel $AI is back as CEO with a restructured org and a singular new focus on revenue growth, cash generation, and non-GAAP profitability after a brutal stretch of declining sales.

Key catalysts from the report:

- Tom Siebel resumes the Chief Executive Officer role with a new execution plan

- A restructuring is underway, booking a one-time charge tied to severance and workforce cuts

- Siebel personally bought 6.17 million shares at $11.16, lifting the cash balance to roughly $673 million as of June 3

- Fresh FY2027 guidance frames the turnaround the new team is being measured against

Thomas M. Siebel $AI, Chairman and Chief Executive Officer:

'𝘛𝘩𝘦 𝘴𝘢𝘭𝘦𝘴 𝘱𝘦𝘳𝘧𝘰𝘳𝘮𝘢𝘯𝘤𝘦 𝘰𝘷𝘦𝘳 𝘳𝘦𝘤𝘦𝘯𝘵 𝘲𝘶𝘢𝘳𝘵𝘦𝘳𝘴 𝘩𝘢𝘴 𝘣𝘦𝘦𝘯 𝘦𝘯𝘵𝘪𝘳𝘦𝘭𝘺 𝘶𝘯𝘢𝘤𝘤𝘦𝘱𝘵𝘢𝘣𝘭𝘦, 𝘵𝘰 𝘵𝘩𝘦 𝘱𝘰𝘪𝘯𝘵 𝘰𝘧 𝘴𝘶𝘳𝘳𝘦𝘢𝘭. 𝘞𝘦 𝘢𝘳𝘦 𝘩𝘦𝘳𝘦 𝘵𝘰 𝘧𝘪𝘹 𝘪𝘵.'

Thomas M. Siebel $AI, Chairman and Chief Executive Officer:

'𝘞𝘦 𝘩𝘢𝘷𝘦 𝘢 𝘸𝘦𝘭𝘭-𝘥𝘦𝘧𝘪𝘯𝘦𝘥 𝘴𝘵𝘳𝘢𝘵𝘦𝘨𝘺, 𝘢 𝘳𝘦𝘴𝘵𝘳𝘶𝘤𝘵𝘶𝘳𝘦𝘥 𝘰𝘳𝘨𝘢𝘯𝘪𝘻𝘢𝘵𝘪𝘰𝘯, 𝘯𝘦𝘸 𝘦𝘹𝘦𝘤𝘶𝘵𝘪𝘷𝘦 𝘭𝘦𝘢𝘥𝘦𝘳𝘴𝘩𝘪𝘱, 𝘢𝘯𝘥 𝘢 𝘥𝘦𝘵𝘢𝘪𝘭𝘦𝘥 𝘦𝘹𝘦𝘤𝘶𝘵𝘪𝘰𝘯 𝘱𝘭𝘢𝘯 𝘯𝘰𝘸 𝘪𝘯 𝘱𝘭𝘢𝘤𝘦 𝘸𝘪𝘵𝘩 𝘵𝘩𝘦 𝘴𝘪𝘯𝘨𝘶𝘭𝘢𝘳 𝘧𝘰𝘤𝘶𝘴 𝘰𝘧 𝘪𝘯𝘤𝘳𝘦𝘢𝘴𝘪𝘯𝘨 𝘴𝘩𝘢𝘳𝘦𝘩𝘰𝘭𝘥𝘦𝘳 𝘷𝘢𝘭𝘶𝘦 𝘵𝘩𝘳𝘰𝘶𝘨𝘩 𝘵𝘰𝘱𝘭𝘪𝘯𝘦 𝘳𝘦𝘷𝘦𝘯𝘶𝘦 𝘨𝘳𝘰𝘸𝘵𝘩, 𝘤𝘢𝘴𝘩 𝘨𝘦𝘯𝘦𝘳𝘢𝘵𝘪𝘰𝘯, 𝘢𝘯𝘥 𝘯𝘰𝘯-𝘎𝘈𝘈𝘗 𝘱𝘳𝘰𝘧𝘪𝘵𝘢𝘣𝘪𝘭𝘪𝘵𝘺. 𝘎𝘢𝘮𝘦 𝘰𝘯.'

The revenue mix tells the story of where the damage is. Subscription still carries almost the entire business, but the professional services line, especially customer-funded prioritized engineering, has nearly evaporated year over year as deals dried up.

Inflection point: this is a founder-led reset, with the original CEO returning to a shrinking topline and pledging to fix the sales engine and reach non-GAAP profitability.