Tokenization is reshaping regulated finance by moving assets onto programmable ledgers, delivering efficiency gains but requiring strong policy and trust anchors to protect stability. Read our new IMF Note on the issue: https://t.co/JnpWurNJos

In the year 2000 there were nine countries without a

Rothschild owned or controlled Central Bank:

1. Iran

2. Iraq

3. Sudan

4. Libya

5. Cuba

6. North Korea

7. Afghanistan

8. Syria

9. Venezuela

Tucker Carlson said he’s a hard "NO" on Bitcoin, claiming it was created by the CIA and calling himself “a gold person.”

“I fear it’ll become a scam run by financial elites and politicians to tighten control over society… Nobody can tell me who Satoshi is. I grew up in a CIA family.”

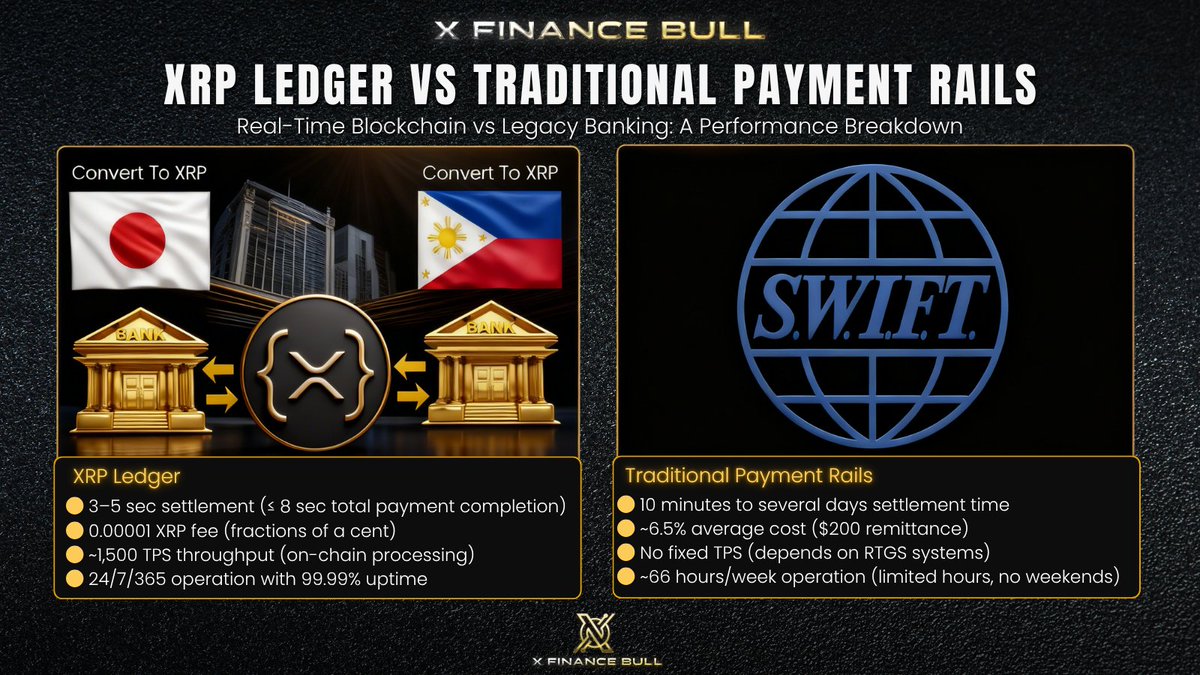

I can't believe people are still bearish on $XRP when you look at this side by side 🤯

XRP Ledger: 3-5 second settlement. Fractions of a cent in fees. 1,500 TPS. Running 24/7/365 with 99.99% uptime.

Traditional rails through SWIFT: 10 minutes to several days. 6.5% average cost on a $200 remittance.

Limited hours. No weekends. Dependent on RTGS systems with no fixed throughput.

One system runs 66 hours a week. The other never stops.

The Japan to Philippines corridor alone represents billions in annual remittance volume. $XRP settles it in 3-5 seconds for almost nothing.

This isn't about replacing traditional finance overnight. It's about the fact that the replacement already exists and is operational.

And Ripple isn't waiting. They're acquiring traditional finance companies to bring $XRP into the system from the inside.

Hidden Road for $1.25 billion. GTreasury for $1 billion. Rail. Palisade. Solvexia. Metaco. Standard Custody. Fortress Trust. BC Payments. And more incoming.

All folded into one stack. Payments, custody, treasury, prime brokerage under one roof.

75+ regulatory licenses globally. VASP applications in Brazil.

Full EU EMI license. OCC banking charter under review. Expanding across Dublin, London, Singapore, Sydney.

The CLARITY Act is around the corner. XRP is already classified as a digital commodity by both the SEC and CFTC.

Ripple isn't building beside traditional finance. They're absorbing it. And $XRP is the settlement layer underneath all of it.

The world's financial system is being modernized. The asset powering it is sitting at $1.45.

You are still early 🫵

🚨 MASTERCARD PRAISES RIPPLE 🚨

🇺🇸 The $10T payments giant Mastercard says Ripple is “fueling the future of the digital payment world.”

Traditional finance is paying attention.

And $XRP is right at the center of it. 🚀

🇩🇪 Meanwhile this evening over Germany

Yet another bizarre action meteorite is caught on camera, except it probably most definitely isn’t a meteorite, look at it appear to accelerate‼️

There is something happening out in ‘Space’ right now.

Jeżeli spojrzymy na to szerzej, Japonia nie jest odosobnionym przypadkiem.

To, co dzieje się wokół Bank of Japan i SBI Holdings, zaczyna przypominać element większej, globalnej układanki.

Bank Japonii testuje rozliczenia pieniądza banku centralnego on-chain czyli bada możliwość przeniesienia warstwy rezerw międzybankowych do środowiska rozproszonego rejestru.

To fundament systemu finansowego. Równolegle SBI od lat jest strategicznie powiązane z Ripple, rozwija rozwiązania oparte na XRP Ledger, wdraża emisje instrumentów on-chain i rozwija infrastrukturę płatności transgranicznych.

Teraz przenieśmy się do Stanów Zjednoczonych.

Cross River Bank już w 2014 roku był jednym z pierwszych banków w USA, które zintegrowały protokół Ripple do rozliczeń międzynarodowych.

To nie była teoria to była operacyjna integracja technologii DLT z realnym bankiem działającym w systemie regulowanym przez amerykańskie instytucje nadzorcze.

Cross River to nie niszowy fintech. To bank infrastrukturalny, który obsługuje wiele platform płatniczych i fintechów w USA.

Jeżeli taki podmiot już dekadę temu testował i wdrażał rozwiązania Ripple w obszarze cross-border, oznacza to, że technologia ta przeszła przez rygor compliance, audytów i wymogów regulacyjnych jednego z najbardziej restrykcyjnych systemów finansowych świata.

I tutaj zaczyna się ciekawa część analizy.

W Japonii mamy:

– bank centralny testujący settlement on-chain,

– największą grupę finansową silnie powiązaną z Ripple,

– rozwiniętą infrastrukturę operacyjną XRPL.

W USA mamy:

– bank regulowany federalnie, który wcześnie integrował Ripple w obszarze płatności międzynarodowych,

– rozwijający się rynek tokenizacji i stablecoinów,

– rosnącą presję na modernizację rozliczeń międzybankowych.

To nie są odizolowane eksperymenty. To równoległe budowanie kompatybilnych warstw infrastrukturalnych w dwóch największych gospodarkach świata.

Jeżeli banki komercyjne integrują rozwiązania DLT do płatności transgranicznych, a banki centralne zaczynają badać rozliczenia rezerw on-chain, to pojawia się naturalne pytanie: czy w przyszłości te warstwy mogą zostać połączone?

Nie chodzi o „jedną światową walutę”.

Bardziej prawdopodobny scenariusz to interoperacyjna sieć:

– banki centralne emitujące lub rozliczające cyfrowe rezerwy,

– banki komercyjne korzystające z tej samej lub kompatybilnej infrastruktury do rozrachunku międzynarodowego,

– stablecoiny i tokenizowane aktywa funkcjonujące jako warstwa pośrednia.

Cross River pokazuje, że integracja Ripple z regulowanym bankiem w USA jest możliwa i funkcjonalna. SBI pokazuje, że można wokół tej technologii budować całe ekosystemy finansowe. A Bank Japonii testuje, czy najważniejsza warstwa systemu — pieniądz banku centralnego — może działać w podobnym modelu technologicznym.

To nie jest dowód na istnienie globalnego planu.

To jest dowód na to, że infrastruktura finansowa świata jest stopniowo przebudowywana w kierunku rozproszonych, programowalnych systemów rozliczeniowych.

A kiedy kilka kluczowych jurysdykcji zaczyna budować kompatybilne rozwiązania w tym samym czasie analityk przestaje patrzeć na to jak na zbieg okoliczności i zaczyna patrzeć jak na zmianę architektury systemu.

BREAKING: The UN’s nuclear watchdog chief, Rafael Grossi, says inspectors have not found evidence of a coordinated Iranian programme to build nuclear weapons despite Israeli and US claims.

🔴 LIVE updates: https://t.co/Pp5PMsskiW

Die Deutsche Bank schlägt ein neues Kapitel in der Modernisierung des globalen Finanzwesens auf. Durch die verstärkte Integration von Technologien aus dem Ripple-Ökosystem zielt das Frankfurter Geldhaus darauf ab, die oft als veraltet kritisierten Strukturen des weltweiten Geldtransfers grundlegend zu reformieren. Im Fokus stehen dabei nicht nur grenzüberschreitende Zahlungen, sondern auch das komplexe Devisengeschäft sowie die sichere Verwahrung digitaler Vermögenswerte.

Bisher galten Auslandsüberweisungen als das Sorgenkind der Finanzbranche: Sie sind meist langsam, intransparent und mit hohen Gebühren verbunden. Die Deutsche Bank nutzt nun Blockchain-Lösungen, die durch die Technologie von Ripple angetrieben werden, um diese Reibungsverluste zu eliminieren. Anstatt Werte über mühsame Ketten von Korrespondenzbanken zu bewegen, ermöglichen diese Infrastrukturen einen direkten Transfer.

Während klassische Überweisungen oft mehrere Tage in Anspruch nehmen, verkürzt die neue Infrastruktur diesen Prozess auf wenige Sekunden. Dies bietet enorme Vorteile für Multi-Währungs-Konten und den globalen Devisenhandel, da Liquidität nun in Echtzeit bereitgestellt werden kann. Zudem erhöht die Blockchain-Dokumentation die Sicherheit, da jede Transaktion manipulationssicher und sofort nachvollziehbar ist.

Die wirtschaftlichen Auswirkungen dieses technologischen Schwenks sind gewaltig. Schätzungen gehen davon aus, dass der Einsatz von Distributed-Ledger-Technologie (DLT) die operativen Kosten im globalen Zahlungsverkehr um bis zu 30 Prozent senken kann. Angesichts von Transaktionsvolumina, die weltweit in die Billionen gehen, ergeben sich hieraus enorme Einsparpotenziale für das Institut und seine Kunden.

Neben dem Zahlungsverkehr forciert die Deutsche Bank das Feld der "Digital Asset Custody". Ziel ist es, Kunden die Verwahrung digitaler Vermögenswerte mit derselben Sicherheit anzubieten, die sie von klassischen Wertpapieren gewohnt sind. Die Skalierbarkeit der Ripple-Infrastruktur bildet hierfür das technologische Fundament.

BREAKING: Polish Prime Minister Donald Tusk says Polish citizens in Iran should leave immediately.

'In a few hours, there may be no more possibility to evacuate,' he says.

https://t.co/PAiZ4D1jU3

📺 Sky 501, Virgin 602, Freeview 233 and YouTube

BREAKING:

🇮🇱 An Israeli spyware firm co-founded by Jeffrey Epstein’s longtime close friend Ehud Barak just made a catastrophic blunder.

A live screenshot of Graphite’s control panel was accidentally exposed - showing real victim phone numbers and active toggles to instantly hijack WhatsApp, Signal, Telegram and take full control over anyone’s digital life.

This was the moment a company revealed exactly how its weapon spies on the world.

This tool hacks journalists, activists, human rights defenders, but above all politicians, ministers, opposition leaders, and anyone who might threaten the power or interests of those who pay.

Paragon isn’t a tech company. It’s a surveillance factory with political cover.

@KhaledElawadi@VinceLaBido@saradwinter@bramk Not really. I think bitcoin is largely a technological dead end for the same reason the dollar is. The technology just doesn't seem to matter all that much to its success, at least not at the blockchain layer.

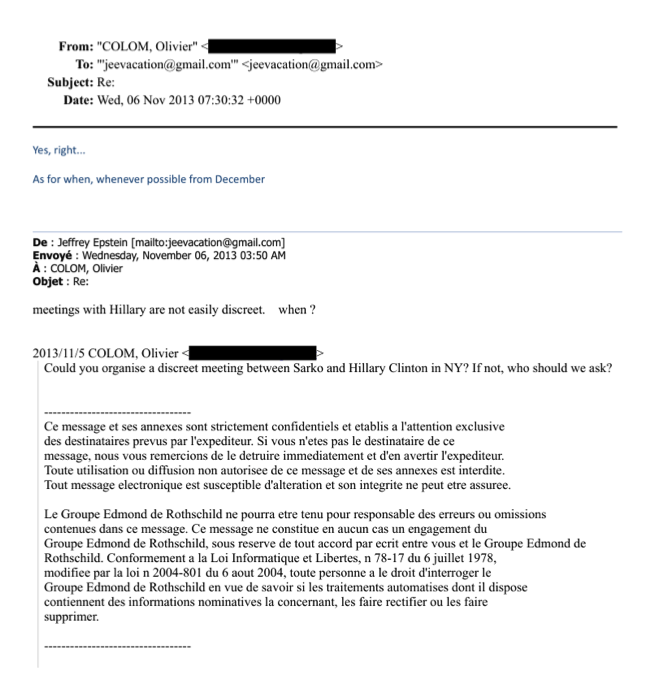

In 2013, France's Nicolas Sarkozy -- currently imprisoned for corruption -- wanted to "discreetly" meet @HillaryClinton during an upcoming NYC trip. Who does his team contact to arrange it? Jeffrey Epstein of course.