@FuzzyPandaShort Jack was one of a kind. Typically first $ into former students’ funds too, just to give you that initial boost.

Still flip through my notes from time to time.

Will be missed

@dalibali2 $WEAV still cheap if that AI receptionist works. Henry Schein guys say the phone based exchange is 1 of only 2 in that world.

$NCNO still cheap on FY28 FCF (consensus not showing the lift as billing model hits) & upside if the agent sandbox for banking takes hold

A few quick Sohn pitches.

Longs:

$IFX on AI rev from 5% to 25% of total by '29. Thinks 25x p/e on '28 revs = 94 EUR/sh by end '27, 58% upside.

$PRM sees 30+% EBITDA cagr from here, mostly from value creating M&A. In-house talent for M&A underappreciated, e.g. ex-Extant guys re-running the Extant playbook. >10% operating margin improvement at each unit. Thinks 2x 3-4y.

$AXON ex Coatue guy argues "AI agents for officers." AI plan charges $559/officer/mo vs old $99/officer/mo. $750m '25 AI plan bookings. Think revenue 2.5x in 3y, EBITDA nearly 3x in 3y.

$APP 3y 25% revenue cagr as ecom vertical takes off & improved models drive improved ROAS. 20x '30e $50 EPS = $1,000 stock. Fastest L36M revenue growth and highest EBIT/employee in the S&P.

$CVNA getting to MSD/HSD used auto share means north of 30% revenue growth for a long time.

$VTRS rescheduling sleeping drug from EU to the US for wakefulness + another drug in SPV = 6x-8x upside. (Missed part of this one, sorry)

Korean holdcos at discount to the parts, eg Samsung Life.

Korean consumer exposure as SK Hynix & Samsung bonuses of 10% of operating profit spill over into consumption.

$TTMI printed circuit board unit growth + increased complexity means topline growth at very high incremental margins. And defense segments in budget epicycle.

$CPT sun belt multifamily REIT with improving supply picture driving pricing power. More of a low beta, MSD downside, 40% upside frame.

Shorts:

$OSIS Sedona contract recognized 80%, collected mid 30s % of cash. May need to revise recognized revenue down materially.

$RZLV 4x revs for a promotional stock looter buying declining software assets. Significant related party cashouts.

Online classifieds like $REA.AU if MSD pricing power breaks.

(Didn't catch every pitch, but should give a sense)

@Noicewon11 It was the AI classifieds short thesis. Will eg Zillow lose incremental property searches to ChatGPT, and if so does that reduce advertising pricing power?

Tough debate bc likely won’t hit the numbers for a few years

@Process_Cap 100%.

Off of memory, I think they FOIA'd the 2024 $PRM contracts to get a sense of price ∆s by line.

There was also an interesting comment: "Many of the board are talented short sellers. When smart short sellers go long, it's worth paying attention."

@astridwilde1@vineelyalamarth Yeah I think that makes a ton of sense.

Buddy of mine runs a top 10 gaming app in the Middle East. What's interesting is that game player demographics keep expanding.

(And not to sound awful but if hantavirus becomes a thing...)

@astridwilde1@vineelyalamarth Late to reading this, but sure looks like a long runway to me: https://t.co/Eokem4fHcd

I haven't seen public disclosures on AppLovin's model vs Meta's. Think the longer runway function of newly unlocked ecommerce / self-serve / mediation views / smaller size / something else?

@astridwilde1@vineelyalamarth Been thinking a bit about this.

Any strong thoughts on APP vs META as the bigger beneficiary of new models improving ad conversions?

@hump_bear@DannyDayan5 Latest chigirl note is excellent on this.

Just thinking this market might be primed to look through PCE if Warsh messages this way. Thinking something like 'core PCE excl Hormuz is fine longer term, we still want to sell MBS and cut short-term rates'

@DannyDayan5@hump_bear Do you think the damage is already embedded or can a Hormuz re-opening be looked-through for 3-6 months?

Interesting to me that CL1 is still $95, Dec '26 is $80, Dec '27 is $72. Those forward prices don't look *too* terrible to me?

@matt_slotnick@midwit_capital Think it's just a mix of (1) FY revenue guide up a bit but EBIT guide down more w Statsig team + (2) a lot of fear that LLMs kill the business = few buyers

If today's SaaS investors need to see FCF-SBC margins or serious revenue acceleration, AMPL just in a tough spot (for now)

$RELY Q1 Rev 25% YoY @ 22.4% EBITDA margin

Sandbagging the FY EBITDA margin guide, again.

Q4 '25 guided 12%, hit 20%

Q1 '26 guided 18.9%, hit 22.4%

Headcount down -4% YTD, SS modeling >10% cash opex growth, and the CEO commenting how "Remitly has all the headcount we need"...

If you screen for labor-intensive public companies likely to transform w LLMs, $GBTG travel agent business likely at the top of your list

Chatted with them last year about this, but they weren't wholly bought in

Hope the next $GBTG is willing to transform in the public market

@thaAdamLittle "Data & Analytics... most bullish on AI impact" is the biggest narrative violation here!

Virtually every investor I chat with worries that the existing analytics companies are dead in the water 2-3 years out...

@InvestingTmr@BrokenMoats I hear you. If you're willing to look out to '28 growth, think not as much of valuation gap -- and I worry that (1) the cash remittance players will continue to churn more and more and (2) it's so hard to maintain compliance across physical locations that it's a political target

Great points - this was actually the chief RELY bear case last year.

Here's how I'm thinking about it.

Stablecoins compress correspondent banking costs but not pay-in, cash-out, FX spreads, or compliance in receiving country.

Defi txn & exchange fees are often >3% all in today, worth noting.

I think it's more likely that the majority of remittance volume paying 5%-7% shifts to the lower cost provider like RELY charging <2.25%.

I agree that pricing compression on constant txn sizes is the #1 thing to track, and I am not seeing or hearing of material moves there from the digital money transfer services.

My opinion is that Stripe Treasury is a death knell, but more for the correspondent bank / SWIFT players that overcharge during the multi-day correspondent settlement process.

If you chat w/ the scaled remittances companies, they'll tell you that stablecoin liquidity pools can only handle a tiny fraction of their current volumes right now. If/when we hear adoption there accelerating, that's probably the time to push the short on those correspondent bank / SWIFT players.

2 bear cases I do worry about for RELY:

1. If we see mass consumer adoption of stablecoin wallets. In that world, the real casualties are probably the card issuing banks & possibly regional banks, as credit cards & debit cards & low yield checking accounts would be replaced by stablecoin wallets. And yes, payment players like RELY would also see margin compression too. If anything, I'm less optimistic about consumer stablecoin wallet adoption in the developed world in the next decade bc of bank lobbying to kill stablecoin yield (which I see as the chief consumer inducement to switch).

2. If WhatsApp decides to push subsidized remittances (i.e. not just offer but advertise aggressively, unlike that recent effort in India). Doing so would open Meta up to a huge amount of legal scrutiny for little incremental gain, but it would be a real concern for me.

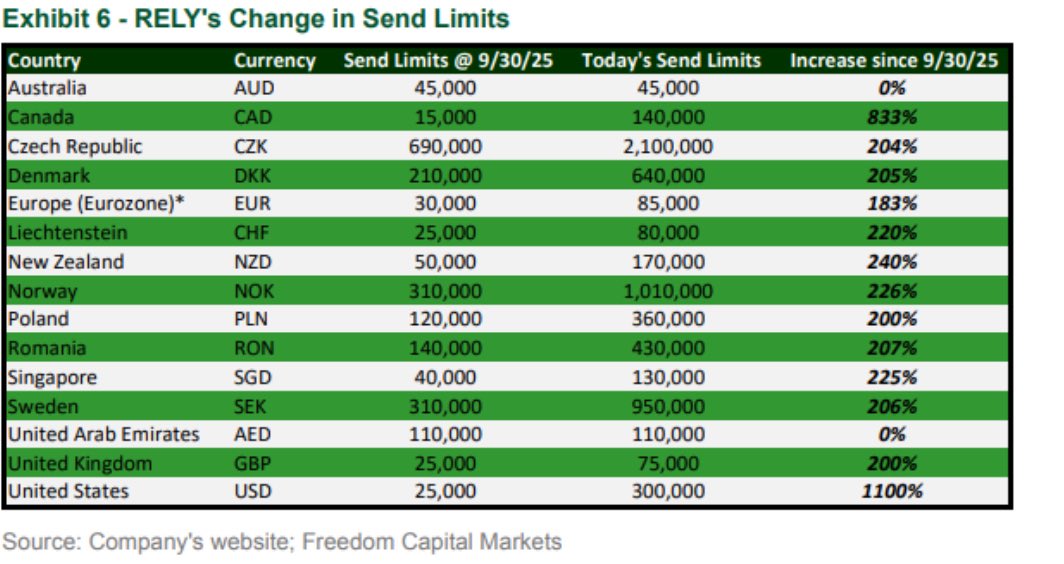

I see the RELY 2026-2027 story as significant send volume growth among very high senders (see attached image) + way tighter opex control than expected by consensus estimates. I actually think Remitly is undercutting Wise on pricing for many >$5k sends, which is a bit of a narrative violation.

Curious to hear if you're seeing/hearing anything opposed to this line of thought (especially anything on like-for-like pricing pressure for the digital remittance players).