Ok guys, mass layoff hv started, now listen carefully what we r going to do next.

In 2023-25 , I need u to :-

- Become obsessed with buying assets

- Have free cashflow.

- Buy real estate (Not now)

- Stay employed for payslip for loans

- Make this tweet as ur wallpaper

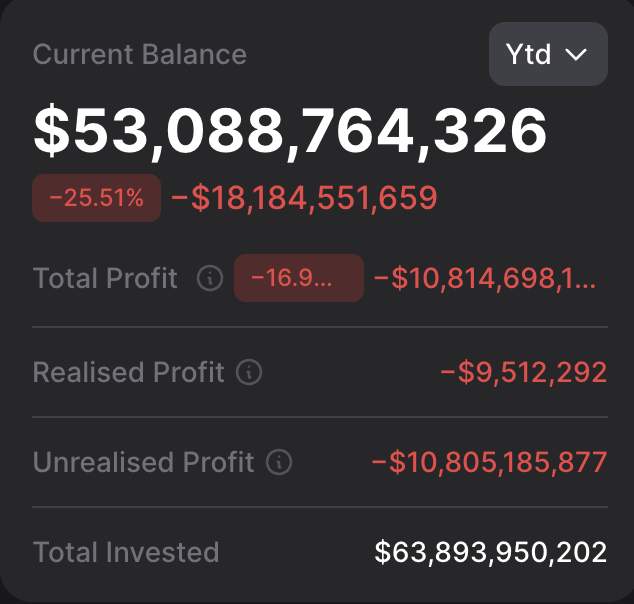

⚠️ MicroStrategy is sitting on its largest unrealized loss in history — -$10.8B down on its Bitcoin position, -17% underwater after six years of accumulation. The stock has fallen -77% from its all-time high. The company recently sold 32 BTC at $77,135 per coin.

𝗛𝘂𝗽𝘇𝘆 𝘁𝗮𝗸𝗲: MSTR's mounting losses matter for $BTC traders because the company has been the single largest institutional bid supporting spot price. A -17% underwater position raises the question of whether MicroStrategy shifts from buyer to seller — or at least pauses accumulation. If MSTR stops buying, a structural demand pillar weakens. The $77K sale price also sets a reference: they're selling into weakness, not strength.

--source: https://t.co/X50qBCDJKb

Track real-time signals & trade → https://t.co/ceYOW7nCNr

dont be a fucking pig

Positioning > predicting.

Long-term accumulation: 30% at $63K, 40% at $58K, 30% at $49K.

Active trading: clear levels + position size that survives being wrong.

beli je la daily cibai. peter thiel nak plant nueralink la cibai . duit bunker

1 thing CT dont realise is

they are being too bearish $btc, and eager to be right . they missed out the real oppurtinity

its in ALT/BTC pair

$hype/btc breakout

$eth/btc breakout

JUST IN:

Tom Lee (@fundstrat)'s #Bitmine is down $8.9B on 5,416,901 $ETH ($10.03B).

Michael Saylor (@saylor)'s #Strategy is down $7.6B on 843,706 $BTC ($56.26B).

refer to Oil beta ratio based on 2 year chart analysis.

selected oil stock exposure

$OXY

$APA

$SM

im still leaning for bullish oil due to migration of money from paper market to hard asset market > commodity supercycle.

oil to $400 2030

kalau oil price naik harga 400$ in next 5 years before 2030

aku sanggup beli kuda , gi solat jemaat nek kude je derr

current oil price 60$

dgan nak war nye, confirm oil pump soon

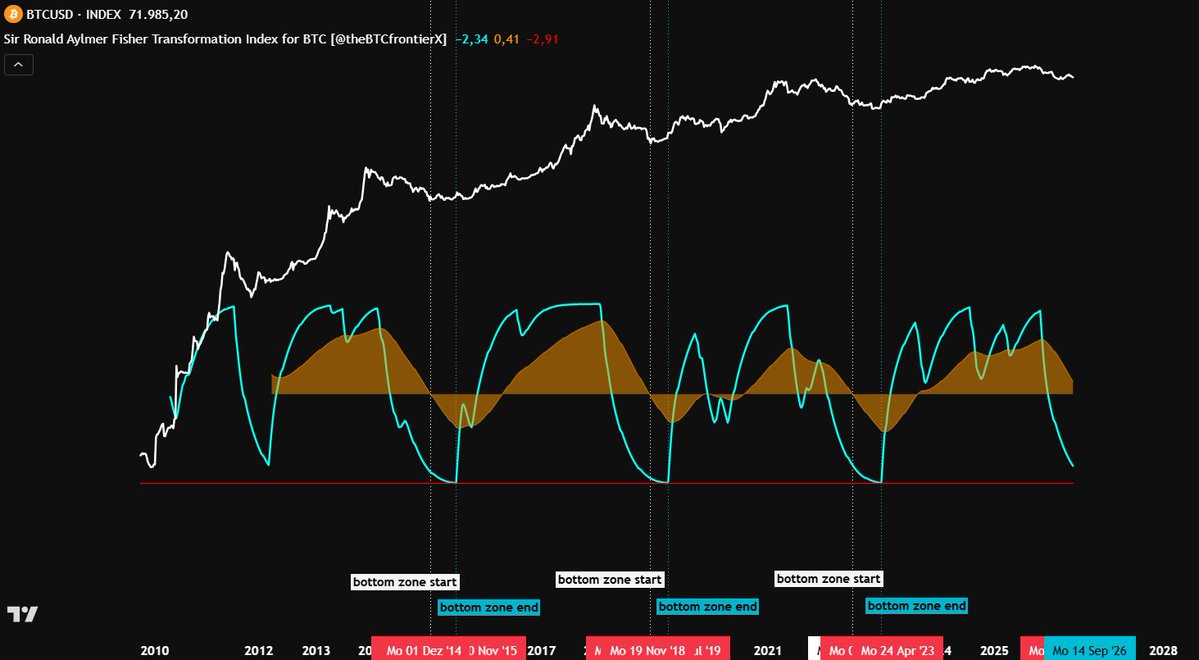

I am personally convinced that MSTR selling BTC is the ultimate bottom signal. It's a form of capitulation from the biggest buyer.

Furthermore we have seen BTC selloff every single time that MSTR buys. Would seem to imply that we will start to rally every time that they sell...

1) ASO (lead) pinching further

2) Weekly RSI (21) on the cusp of breaking down

3) Great Falls Oscillator trailing lower

4) SRAFTI momentum trailing lower (0-level to be hit in 8-10 weeks)

1 thing im surpired by how undervalued these cash generating comapnies compared to $eth marketcap valued at $256 bill marketcap

imagine eth at 256 while nbis and iren combined below 100$ bill marketcap.

lesson there. either crypto overval or iren underval

Neocloud Ecosystem Cheat Sheet Part 1/2:

Bullet Point Positive vs. Negatives.

Full List by Marketcap:

$CRWV ($66.2B)

$NBIS ($32.85B)

$IREN ($16.52B)

$APLD ($9.69B)

$RIOT ($7.34B)

$CIFR ($7.3B)

$WULF ($6.36B)

$HUT($5.39B)

$CLSK ($5.01B)

$HIVE ($1.74B CAD)

$WYFI ($1.29B)

$WLAC($600m IPO)

$DGXX ($393M CAD)

$SLNH ($281.9M)

_

Summary

When comparing, a major source of alpha generation currently lies in the megawatt valuation arbitrage, which involves converting low-multiple Bitcoin power capacity into high-multiple AI hosting capacity.

The second major alpha is margin generation, which involves being vertically integrated from the bottom up from GPU orchestration to software.

Coreweave ( $CRWV ) - $66.2B Marketcap

🍏Positives

________________

- Sector leader by scale: quarterly revenue of $1.21B (+206.75% YoY) and EBITDA of $607.69M; on pace for $5B+ ARR in 2025.

- $30B+ backlog, anchored by:

- $14B Meta deal,

- OpenAI

- $6.3B NVIDIA GPU backstop agreement,

- growng Gov contracts via CRWV Federal .

- Expansion into U.S. government infrastructure is a major long-term moat if backstopped by federal workloads.

- NVIDIA partnership ensures utilization floor; de-risks GPU oversupply.

- Positioned as hyperscaler alternative with Tier 1 clients and national buildout footprint.

Negatives

________________

- Aggressive capex: Q3 spend of $2.9–3.4B, with 2025 full-year guidance of $20–23B.

- High-cost debt structure: Over $1B in projected annual interest, versus competors using low- or zero-interest convertible notes.

- Q2 GAAP net loss of $291M, signaling limited profitability despite scale.

- Execution risk remains high: e.g., failed $9B Core Scientific acquisition due to shareholder rejection.

- Competitors like Nebius are closing the full-stack gap, weakening CoreWeave's software moat.

Nebius ( $NBIS ) - $32.85B MarketCap

🍏Positives

________________

- $17.4B Microsoft deal for full-stack AI infrastructure (possibly rising to $19.4B).

- Active include many enterprises such as MSFT, Shopify, Accenture, governments, and AI startups.

- 71%+ gross margins on AI infra segment; profitable at the EBITDA level.

- 1 GW+ powr secured, targeting dense GPU deployments across new sites.

- Fully integrated software+hardware stack, which increases opex and is a moat.

- $10B+ in assets, from $5.8B+ cash, ownership of companies like Clickhouse that powers Anthropic, Meta, and others growing rapidly.

Negatives

________________

- Execution risks around full-stack delivery and latency SLAs could derail rollout.

- Microsoft is the primary anchor on forward revenue extreme contract dependency (high concentration risk projected AI revenue)

- 71% gross margin figure not representative of forward revenue or execution at scale and could lower to a more conservative 50-65% number.

$IREN - $16.52B marketcap

🍏Positives

________________

- 2.91 GW power secured, diversified across North America, and expanding more than 3GW in renewable power capacity.

- Full control over power, land, and data center construction = vertical efficiency and higher margin control compare to other bare metal.

- Targets customers (e.g., AI labs, hyperscalers) who might bring their own Type-1 orchestration and prefer bare-metal control.

- Historically the most efficient and profitable large-scale BTC miner and better positioned to handle rising GPU power/cooling requirements in B100/B200 generations for AI cloud pivot.

- Targeting an ARR of over $500 million by the first quarter of 2026 by buildouting out a fleet of 23,000 NVIDIA B200/B300 + AMD MI350X GPUs.

Downsides

________________

- No well-known enteprsie/hyperscaler contract visibility and limited disclosed large SLA deals yet

- Not a full-stack provider; acts as Tier-1 (shell/colocation) = lower margin and tenant risk and illustrative GPU target. Meaning it is unable to capture the highest-margin revenues associated with integrated, proprietary full-stack cloud

- Quoted 92% margins excludes expense recognition, and with D&A and would be much lower at scale.

- The substantial capital expenditure required for the large-scale GPU purchase risks negative returns if future utilization rates fail to meet expectations

$APLD

🍏Positives

________________

- $5B Macquarie financing facility, with first draw building 400MW AI campus.

- Tenant: CoreWeave fully leasing Polaris Forge 1 (400MW), scalable to 1GW.

- Proprietary waterless liquid cooling optimized for dense AI workloads

- Capex-light via preferred equity.

- AI-first buildout focused on latency, fiber, and power pairing in North Dakota.

Downsides

________________

- Large-scale buildout depends on continued draws from Macquarie’s $5B facility.

- 400MW CoreWeave lease is all-or-nothing; no clarity on tenant diversity.

- Execution risk at Polaris Forge: weather, zoning, grid integration delays.

- Exposed to single-tenant concentration and private-market GPU pricing dynamics.

$RIOT

🍏Positives

________________

- 600MW idle capacity in Corsicana, TX under AI redeployment review.

- Gigawatt-scale infrastructure in place, ready for rapid pivot.

- Leverages one of the lowest power costs in the U.S. (ERCOT access).

- TTM Gross Margin of nearly 60% as of Q2 2025, primarily derived from its core mining business. The successful implementation of this contract gives more confidence in converting additional existing mining sites into high-multiple HPC capacity.

Negatives

________________

- AI pivot is purely exploratory; no firm buildout announced.

- 600MW idle capacity = opportunity, but also dead capital for now.

- Canceling mining expansion (8.3 EH/s) may weaken near-term revenues.

- Needs permits, fiber, GPU supply, and anchor tenant before AI rollout can begin.

$CIFR

🍏Positives

________________

- 10-year, $3B+ computing 168MW agreement with Fluidstack + $GOOGL

- Agreement is substantially de-risked by a $1.4 billion commitment from Google to backstop the Fluidstack lease

- High-margin, low-risk hosting model with leased facilities.

Negatives

________________

- Fluidstack deal is 10-year but fixed-price, limiting upside if GPU rental rates increase.

- $1.3B convertible debt adds dilution risk if equity markets weaken.

- Site buildouts dependent on few customers, very high fill and utilization risk.

_

Since the data center sector is so nuanced and broad thought it would be helpful if I wrote created a full TLDR list for newcomers to see the tradeoffs of each approach.

I'll probably go back and add more stuff to $CIFR and $APLD and others in one final post since it didn't get enough justice.

I just didn't realize how much time this took to write up + please correct me if any figures are off lol.

Also would save me time if people helped fill out the rest lol so would appreciate it too for 2/2.

~~~ Help with the Crowdsourcing ~~~

Everyone keeps arguing about $NBIS investors switching to $IREN shares - both for and against this prediction. Meanwhile, you’re all missing the big picture.

For starters, you shouldn’t do such a thing, you should own BOTH companies. And, more importantly, $IREN is clearly undervalued to it’s peers (both $CRWV and $NBIS) and the chart TA is screaming to you that it will catch a bid and rise sharply in the coming weeks (in fact, this rise has already just started).

$NVDA option to buy shares at $70 teaches you this is the absolute FLOOR of where the stock needs to be today - but again more importantly, you all know very well $NVDA is not looking for a mere 10, 30, or even 50% gain in their investment. $IREN should be a $140-$150 stock if you’re comparing it to $NBIS financials. The more of a gap between the price of $CRWV / $NBIS vs $IREN, the greater a chance you will see $IREN skyrocket.

Honestly, it really is that simple.

Bookmark this post and check back in 1, 2 and 3 months. $65.33 closing price today. This price will look like a bargain by the end of summer.

And if you don’t believe the aforementioned - please go ahead and short it, and let us know how that goes for ya.

One of the new, buzzy jobs in Silicon Valley is the AI Forward Deployed Engineer (FDE), an engineer who is embedded within a client organization to help customize solutions, such as building and tuning agentic workflows that suit the client’s particular needs. I’ve heard from people who are wondering anew about the FDE career path since OpenAI and Anthropic started building new teams to place FDEs within client organizations.

The rise of FDEs for AI workloads is one way AI is creating new jobs (and why the jobpolcalypse narrative of upcoming job market collapse is false -- there will be many AI and non-AI jobs). However, I believe there will be far more AI Engineer jobs than FDEs, as I explain below.

The FDE role was pioneered about two decades ago by Palantir, which sent engineers to government locations to work on secure, air-gapped networks. In addition to having good technical skills, FDEs need communication skills and sometimes business skills. For example, they may need to speak with clients to understand their needs, formulate a strategy to prioritize projects, explain complex technology, and respectfully push back if a client asks for something unrealistic. They’re enjoying a resurgence because of the amount of work involved in taking an off-the-shelf LLM and building it into a custom agentic workflow that fits particular business needs.

However, I believe the number of AI Engineer jobs will be far larger. A company might accept a few FDEs to be embedded within its organization. But most companies will want far more of their own employees working on their projects. While my organizations do hire FDEs, we hire far more AI Engineers! Also, a common client concern is that it is hard to find vendor-neutral FDEs — they are, after all, there to deeply integrate a particular vendor’s product into a company. In this moment when it’s hard to predict which AI service will be the best one in a year’s time, optionality (the ability to pick whatever vendor turns out to fit best in the future) is very valuable. In contrast, letting FDEs tightly bind a company’s processes significantly reduces optionality.

Right now, I see surging demand for AI Engineers who can build software applications using AI software components (like LLM prompting, agentic frameworks, evals, etc.) and effectively use AI coding agents (like Claude Code, Codex, Antigravity CLI, and OpenCode). As the AI Engineer role matures, I expect it to fragment into more specialized roles, like the generic Software Engineer role from decades ago fragmented into frontend, backend, mobile, data engineering, devops, and so on.

What will be the future, specialized AI engineering roles? I don’t know. Perhaps there will be AI FDEs, LLMOps Engineers, Evals Engineers, AI Data Engineers, Harness Engineers, and other roles we don’t have names for yet. But for now, I see a lot of AI engineers who are generalists create a lot of value. Skilled AI Engineers are in very high demand! As our field continues to mature over the coming decade, I look forward to new specializations within AI Engineering that create even more job opportunities.

[Original text: The Batch newsletter]

![AndrewYNg's tweet photo. One of the new, buzzy jobs in Silicon Valley is the AI Forward Deployed Engineer (FDE), an engineer who is embedded within a client organization to help customize solutions, such as building and tuning agentic workflows that suit the client’s particular needs. I’ve heard from people who are wondering anew about the FDE career path since OpenAI and Anthropic started building new teams to place FDEs within client organizations.

The rise of FDEs for AI workloads is one way AI is creating new jobs (and why the jobpolcalypse narrative of upcoming job market collapse is false -- there will be many AI and non-AI jobs). However, I believe there will be far more AI Engineer jobs than FDEs, as I explain below.

The FDE role was pioneered about two decades ago by Palantir, which sent engineers to government locations to work on secure, air-gapped networks. In addition to having good technical skills, FDEs need communication skills and sometimes business skills. For example, they may need to speak with clients to understand their needs, formulate a strategy to prioritize projects, explain complex technology, and respectfully push back if a client asks for something unrealistic. They’re enjoying a resurgence because of the amount of work involved in taking an off-the-shelf LLM and building it into a custom agentic workflow that fits particular business needs.

However, I believe the number of AI Engineer jobs will be far larger. A company might accept a few FDEs to be embedded within its organization. But most companies will want far more of their own employees working on their projects. While my organizations do hire FDEs, we hire far more AI Engineers! Also, a common client concern is that it is hard to find vendor-neutral FDEs — they are, after all, there to deeply integrate a particular vendor’s product into a company. In this moment when it’s hard to predict which AI service will be the best one in a year’s time, optionality (the ability to pick whatever vendor turns out to fit best in the future) is very valuable. In contrast, letting FDEs tightly bind a company’s processes significantly reduces optionality.

Right now, I see surging demand for AI Engineers who can build software applications using AI software components (like LLM prompting, agentic frameworks, evals, etc.) and effectively use AI coding agents (like Claude Code, Codex, Antigravity CLI, and OpenCode). As the AI Engineer role matures, I expect it to fragment into more specialized roles, like the generic Software Engineer role from decades ago fragmented into frontend, backend, mobile, data engineering, devops, and so on.

What will be the future, specialized AI engineering roles? I don’t know. Perhaps there will be AI FDEs, LLMOps Engineers, Evals Engineers, AI Data Engineers, Harness Engineers, and other roles we don’t have names for yet. But for now, I see a lot of AI engineers who are generalists create a lot of value. Skilled AI Engineers are in very high demand! As our field continues to mature over the coming decade, I look forward to new specializations within AI Engineering that create even more job opportunities.

[Original text: The Batch newsletter]](https://pbs.twimg.com/media/HJvWmCHagAAnTxQ.jpg)